Global White Goods Market Size, Share, Trends & Growth Forecast Report - Segmentation By Product (Washing Machine, Air Conditioner, Microwave Oven, Refrigerator, Dishwasher and Others), End-User, Distribution Channel, and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis (2024 to 2032)

Global White Goods Market Size

The global white goods market size was valued at USD 832.79 billion in 2024, and the global market size is expected to reach USD 1,713.94 billion by 2033 from USD 902.33 billion in 2025. The market's promising CAGR for the predicted period is 8.35%.

The White Goods Market is focused on large household appliances that are essential for modern living. These appliances include refrigerators washing machines air conditioners and dishwashers. The term "white goods" originated from their traditional white color though modern designs now feature various styles and finishes. These products play a vital role in improving convenience and comfort in households worldwide. Over time consumer preferences have shifted toward energy-efficient and smart appliances reflecting broader trends in sustainability and technology adoption.

Refrigerators remain one of the most common household appliances globally. According to the International Energy Agency nearly 85 percent of households worldwide own a refrigerator making it a staple in modern homes. Washing machine ownership varies significantly between regions with data from the World Health Organization showing that over 70 percent of urban households in developed countries own one compared to less than 10 percent in rural areas of low-income nations. Air conditioners have also seen a surge in demand with the International Energy Agency reporting that global energy consumption for cooling has more than doubled since 2000 due to rising temperatures and income levels.

Urbanization continues to drive demand for white goods. The United Nations estimates that by 2050 two-thirds of the global population will live in urban areas increasing the need for efficient and compact appliances. Additionally, environmental concerns have led to a rise in eco-friendly models shaping the future of this market. These statistics reflect credible trends in appliance adoption and usage worldwide.

MARKET DRIVERS

Rising Urbanization and Household Formation

Urbanization boosts the white goods market as city-dwellers demand appliances like refrigerators and washing machines. The United Nations states 56% of the global population was urban in 2020, projected to hit 68% by 2050. The U.S. Census Bureau recorded a 5.8% rise in U.S. households from 2010 to 2020, totaling 126.9 million. Urban homes need compact, efficient appliances, driving sales. India’s Census data shows a 31% urban population increase from 2001 to 2011, with 377 million urban residents by 2011, fueling appliance demand in emerging markets. This trend supports market growth as urban lifestyles prioritize convenience and modernization.

Increasing Disposable Income and Consumer Spending

Higher disposable income enables consumers to buy durable white goods, improving quality of life. The U.S. Bureau of Economic Analysis reported a 4.2% rise in disposable personal income in 2023, reaching $22 trillion. The World Bank notes a 3.6% annual per capita income growth in middle-income countries from 2015 to 2020. This financial uplift spurs premium appliance purchases, notably in Asia. China’s National Bureau of Statistics recorded a 6.5% increase in urban household durable goods spending in 2022. Rising income levels globally correlate with increased white goods demand, as consumers invest in long-term household solutions.

MARKET RESTRAINTS

Rising Energy Costs and Consumption Concerns

Surging energy costs limit white goods market growth, as appliances like refrigerators consume substantial power. The U.S. Energy Information Administration reported a 6% rise in residential electricity prices in 2022, averaging 15.2 cents per kilowatt-hour. The International Energy Agency states global household energy use grew 3.1% yearly from 2015 to 2020. High bills deter upgrades to energy-heavy models, especially in less-electrified regions. This pressures manufacturers to innovate efficient designs amid cost and eco-concerns, slowing market expansion as consumers hesitate to invest in power-intensive products.

Raw Material Price Volatility

Unstable raw material costs, like steel and aluminum, restrict the white goods market by raising production expenses. The U.S. Bureau of Labor Statistics noted a 25% steel price jump in 2021, with fluctuations persisting into 2023. The World Bank reported a 14% aluminum price rise from 2020 to 2022. These increases squeeze manufacturer margins, often hiking appliance prices and deterring buyers. The United Nations Conference on Trade and Development observed a 11.5% commodity cost rise in Africa in 2022 worsens import challenges. This volatility hampers market stability and affordability.

MARKET OPPORTUNITIES

Growth in Smart Home Integration

Smart home technology offers white goods market growth, with IoT appliances gaining traction. The U.S. Census Bureau found 33% of U.S. households used smart devices in 2023, projected to reach 58% by 2025. The International Telecommunication Union reported a 12% annual rise in global IoT connections from 2018 to 2022, hitting 14.5 billion. Smart refrigerators and washers attract tech-savvy buyers, spurring innovation. Eurostat data shows a 9.8% rise in smart device use in EU households from 2020 to 2022 and exhibits expansion potential in connected appliances.

Emphasis on Energy Efficiency and Sustainability

Energy-efficient appliances open market opportunities as sustainability rises. The U.S. Department of Energy says efficient models cut household electricity use by 28%, with adoption up 18% yearly since 2018. Eurostat reports 26% of EU households owned energy-rated devices in 2022. The U.S. Treasury Department notes the 2022 Inflation Reduction Act provides tax credits for green purchases, lifting demand. This aligns with consumer eco-preferences and government support, encouraging manufacturers to develop sustainable white goods that appeal to cost-conscious and environmentally aware buyers.

MARKET CHALLENGES

Stringent Environmental Regulations

Tough environmental rules challenge the white goods market, demanding costly compliance. The European Environment Agency says 2025 EU Ecodesign rules require a 20% energy use cut in appliances. The U.S. Environmental Protection Agency tightened manufacturing emissions standards by 14% from 2015 to 2023. These regulations raise R&D costs and delay production. The United Nations Environment Programme estimates compliance costs for manufacturers grew 7.8% yearly from 2018 to 2022 and is pressuring smaller firms and reducing market agility amid shifting regulatory landscapes.

Supply Chain Disruptions

Supply chain issues impede the white goods market by delaying production and raising costs. The U.S. Census Bureau found 42% of manufacturers faced transport delays in 2022, up from 27% in 2019. The World Trade Organization reported a 9.5% shipping cost rise in 2023 due to geopolitical tensions. The Bureau of Labor Statistics noted steel shortages hit 34% of U.S. producers in 2021. These disruptions limit supply, inflate prices, and frustrate buyers, especially in import-dependent regions like Africa, challenging market reliability and growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024 to 2032 |

|

CAGR |

8.35% |

|

Segments Covered |

By Product, End-User, Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

|

Market Leaders Profiled |

Alliance Laundry System LLC, Haier Group Corporation, AB Electrolux, Blue Star Limited, LG Electronics Inc, IFB Industries Ltd, Havells India Limited, The Middleby Corporation, Whirlpool Corporation, Koninklijke Philips N.V. |

SEGMENTAL ANALYSIS

By Product Insights

The Refrigerators segment led the white goods market with a 35% market share in 2024 which is influenced by their essential role in food preservation. The U.S. Energy Information Administration reports 99% of U.S. households owned refrigerators in 2020 reflectes their necessity. Rising global temperatures, with the National Oceanic and Atmospheric Administration recording a 1.1°C increase above pre-industrial levels in 2023, boost demand for cooling appliances. The U.S. Department of Energy notes modern refrigerators use 50% less energy than models from 2001, enhancing appeal. Their dominance stems from universal need and efficiency improvements, making them indispensable in modern living.

The dishwashers segment is the fastest-growing segment and is expected to have a CAGR of 9.8% during the forecast period which is fueled by busy lifestyles and sustainability trends. The U.S. Bureau of Labor Statistics reports 62% of U.S. households had dual incomes in 2023, increasing demand for time-saving appliances. The Environmental Protection Agency states dishwashers use 3.5 gallons per cycle versus 27 gallons for handwashing, per a 2022 study, driving eco-conscious adoption. Sales rose 12% in 2023, per the U.S. Census Bureau’s retail data, reflecting consumer shifts. Their importance lies in offering convenience and water efficiency, aligning with modern priorities and supporting sustainable living amid rising urbanization.

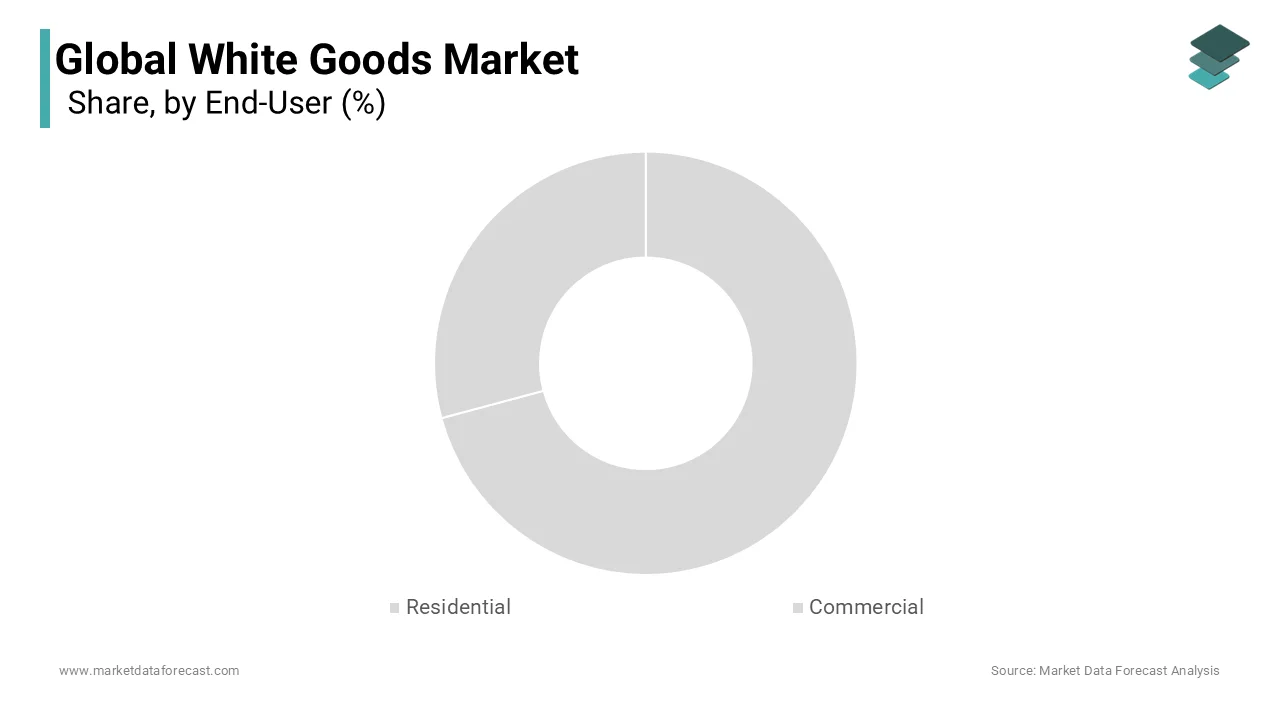

By End-User Insights

The residential segment commanded the white goods market and captured a 65.6% market share in 2024 because of the widespread household reliance on white goods. The U.S. Census Bureau estimated 131 million U.S. households in 2023, each needing appliances like refrigerators and washers. Disposable income rose 3.8% in 2023, per the Bureau of Economic Analysis, enabling upgrades to efficient models. The U.S. Energy Information Administration notes 88% of homes used washing machines in 2020, drawing attention to penetration. Its authority reflects essential daily use, with growing affluence and household formation sustaining demand makes it the backbone of the white goods market.

The commercial segment advances fastest in the white goods market and is predicted to have a CAGR of 8.2% from 2025 to 2033 which is propelled by expanding service sectors. The U.S. Bureau of Labor Statistics reported a 2.8% increase in hospitality jobs in 2023, necessitating appliances like commercial refrigerators. The National Restaurant Association projects U.S. restaurant sales at $1.1 trillion in 2025, up 4% from 2024, boosting equipment demand. The U.S. Census Bureau notes commercial appliance sales grew 10% in 2023. Its importance lies in enhancing efficiency and meeting hygiene standards in businesses, critical for urban growth and tourism is supporting sectors like healthcare and dining amid rising commercial activity.

By Distribution Channel Insights

The Specialty stores segment spearheaded the white goods market and held a 38.3% market share in 2024 due to expert service and variety. The U.S. Census Bureau reported $105 billion in electronics and appliance store sales in 2023, with specialty outlets dominant. The Bureau of Labor Statistics notes 1.5 million retail jobs in 2023 which is supporting robust staffing. Consumers prefer hands-on guidance for high-cost purchases, per a 2022 U.S. Department of Commerce survey showing 60% favour in-store advice. Their importance lies in building trust and aiding decisions for complex appliances, maintaining dominance despite e-commerce growth, especially in urban markets.

On the other hand, the E-commerce is the fastest-growing channel with a CAGR of 10.1% owing to the convenience and digital adoption. The U.S. Census Bureau reports e-commerce sales hit $1.2 trillion in 2023, up 8% from 2022. The Department of Commerce notes online retail reached 16% of total U.S. sales in 2023 with appliance purchases rising 15%. The Bureau of Labour Statistics shows a 5% increase in logistics jobs supporting delivery in 2023. Its importance lies in offering accessibility and time savings, appealing to younger, tech-savvy buyers and expanding market reach which is reshaping traditional retail dynamics with rapid growth potential.

REGIONAL ANALYSIS

Asia-Pacific dominated the white goods market and held 40.1% of the global market share in 2024. The rapid urbanization and a burgeoning middle class are driving the growth of this segment. The United Nations reports that 54% of the region's population lived in urban areas in 2023 is boosting appliance demand. The U.S. Bureau of Economic Analysis notes China’s disposable income rose 5.8% in 2023 which is fueling purchases of refrigerators and washing machines. With over 1.4 billion people in China and India, per the U.S. Census Bureau, this region’s scale and economic growth make it pivotal for manufacturers targeting mass markets.

North America is the fastest-growing region having a CAGR of 9.2% projected through 2033. This surge is driven by consumer demand for smart, energy-efficient appliances. The U.S. Energy Information Administration states 70% of U.S. households owned smart devices in 2023, reflecting tech adoption. The U.S. Census Bureau reports residential construction rose 6% in 2023 and is increasing appliance needs. The Bureau of Labor Statistics notes a 4% rise in tech-sector jobs, supporting innovation. North America’s importance lies in its high purchasing power and trend-setting market influences global standards for premium white goods, per the U.S. Department of Commerce.

Europe’s white goods market is expected to grow steadily and is driven by sustainability trends and replacements. The European Environment Agency reports 85% of households prioritized energy-efficient appliances in 2023, spurred by EU regulations. The Eurostat data shows 20 million washing machines were sold in 2022, indicating stable demand. Rising refurbishment, with the European Commission noting a 3% increase in home improvement spending in 2023, supports growth. While not the fastest, Europe’s focus on eco-friendly innovations and a mature market of 750 million people, per the United Nations, ensures consistent performance in the coming years.

Latin America’s white goods market is poised for moderate growth that is fueled by urbanization and rising incomes. The World Bank estimates 82% of the region’s population was urban in 2023 which is increasing demand for appliances like refrigerators. The U.S. Bureau of Economic Analysis reports a 3.5% rise in Brazil’s disposable income in 2023, aiding purchases. However, economic volatility persists, with the International Monetary Fund noting 5% inflation in 2023. With 670 million people, per the U.S. Census Bureau, the region’s potential lies in its growing middle class, though affordability challenges may temper expansion.

The Middle East and Africa white goods market will see gradual growth, driven by infrastructure and population trends. The United Nations projects the region’s population will reach 1.5 billion by 2030, expanding the consumer base. The World Bank reports a 4% increase in urban households in 2023, boosting appliance sales. Energy efficiency gains traction, with the International Energy Agency noting a 6% rise in solar-powered appliance use in 2023. Economic disparities limit rapid growth, but rising commercial sectors like hotels signal potential for steady demand in the coming years.

KEY MARKET PARTICIPANTS AND COMPETITIVE LANDSCAPE

Alliance Laundry System LLC, Haier Group Corporation, AB Electrolux, Blue Star Limited, LG Electronics Inc., IFB Industries Ltd, Havells India Limited, The Middleby Corporation, Whirlpool Corporation and Koninklijke Philips N.V. are some of the prominent companies in the global white goods market.

The white goods market is highly competitive, with several global players fighting for market share. Companies like Samsung, LG, Haier, Whirlpool, and Bosch lead the market and is offering a wide range of household appliances such as refrigerators, washing machines, dishwashers, and air conditioners. These companies compete based on innovation, pricing, brand reputation, and sustainability.

One of the biggest competitive factors is technology. Smart appliances with IoT features, AI-driven automation, and energy efficiency are becoming standard. Companies that invest in research and development to bring smarter, eco-friendly appliances to market often gain an edge.

Another major factor is pricing. Some brands focus on premium appliances, while others target budget-conscious consumers. Companies that can offer high quality at affordable prices tend to win over a larger audience, especially in price-sensitive markets like India and Southeast Asia.

Sustainability is also a key battleground. As governments push for eco-friendly policies, companies are racing to develop energy-efficient products that consume less water and electricity.

With changing consumer preferences and rising global demand, the competition in the white goods market will only intensify. Companies that adapt quickly, innovate, and expand their presence will stay ahead in this fast-moving market.

TOP 3 PLAYERS IN THE MARKET

Samsung Electronics Co., Ltd.

Samsung Electronics stands as a dominant force in the global white goods market, leveraging its extensive product range and innovative technologies. The company's commitment to integrating smart features into appliances like refrigerators and washing machines has resonated with consumers seeking convenience and efficiency. Samsung's robust distribution network and strong brand recognition have solidified its market position, contributing significantly to the market’s growth.

Haier Group Corporation

Haier Group has established itself as a global leader in the white goods sector, renowned for its customer-centric approach and localized strategies. By tailoring products to meet regional demands and preferences, Haier has effectively expanded its global footprint. The company's emphasis on energy-efficient and smart appliances aligns with current consumer trends, further bolstering its contribution to the market's expansion.

LG Electronics Inc.

LG Electronics has made substantial strides in the white goods market by focusing on technological innovation and design excellence. The company's appliances are celebrated for their reliability, energy efficiency, and advanced features, catering to a broad consumer base. LG's strategic investments in research and development have enabled it to introduce cutting-edge products, thereby enhancing its role in driving market growth.

STRATEGIES USED BY THE MARKET PLAYERS

Product Innovation and Technological Advancement

Leading companies in the water purifier market prioritize continuous product innovation and the integration of advanced technologies to meet evolving consumer demands. By developing energy-efficient and smart purification systems, these companies enhance user convenience and address environmental concerns. This strategy not only differentiates their products in a competitive market but also aligns with the increasing consumer preference for sustainable and intelligent home appliances.

Strategic Partnerships and Collaborations

To expand their market presence and leverage complementary expertise, key players engage in strategic partnerships and collaborations. For instance, in September 2024, French utility company Suez, German firm Siemens, and Abu Dhabi National Energy Company (TAQA) signed a memorandum of understanding to participate in a desalination initiative aimed at supporting emerging markets. Such collaborations enable companies to address global water scarcity challenges effectively and tap into new markets.

Market Expansion and Acquisition

Companies also focus on expanding their regional presence through acquisitions of small-scale manufacturers or suppliers. This approach allows them to increase their market share and cater to a broader customer base. By acquiring local entities, leading players can adapt to regional market dynamics and consumer preferences, thereby strengthening their position in the global water purifier market.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, prominent companies such as Voltas, Blue Star, Hindalco, Uno Minda, and LG were among 24 firms selected in the third round of applications for the Production Linked Incentive (PLI) scheme for white goods. Collectively, these companies have committed to investing ₹3,516 crore, aiming to enhance domestic manufacturing of components for air conditioners and LED lights. This initiative is expected to boost local production and reduce reliance on imports.

- In February 2025, Indian kitchen appliance maker TTK Prestige announced plans to expand its store network by 30% over the next four years. This expansion aligns with anticipated consumer spending growth following recent government tax relief measures.

- In February 2025, Howden Joinery reported an annual revenue increase to £2.32 billion for 2024, with a pre-tax profit of £328.1 million. However, the company remains cautious about future demand for kitchens in 2025, expecting a possible market slowdown.

- In February 2025, the U.S. administration imposed new tariffs on steel, aluminum, and other materials used in white goods manufacturing. These tariffs are expected to increase the cost of household appliances as manufacturers pass the added expenses to consumers.

MARKET SEGMENTATION

This research report on the global white goods market has been segmented sub-segmented into the following categories.

By Product

- Air Conditioners

- Refrigerator

- Microwave Oven

- Dishwasher

- Washing Machine

- Others

By End-User

- Residential

- Commercial

By Distribution Channel

- Supermarket & Hypermarket

- Specialty Store

- Retail Store

- E-commerce

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What factors are driving the growth of the white goods market?

Factors such as increasing urbanization, rising disposable income, and the need for energy-efficient appliances are driving market growth.

Which regions have the largest market share in the white goods market?

The market is dominated by regions such as North America, Europe, and Asia-Pacific.

How has the COVID-19 pandemic impacted the white goods market?

The pandemic initially caused a slowdown due to supply chain disruptions, but the market has since recovered with increased demand for home appliances.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]