U.S. Health and Wellness Market Size, Share, Trends, and Growth Analysis Report, Segmented By Product Type (Beauty and personal care products, Health and wellness food, Wellness tourism, Fitness equipment, Preventive and personalized health), Distribution Channel, End Use, Category Type & Region ( New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado), Industry Forecast From 2025 to 2033

U.S. Health and Wellness Market Size

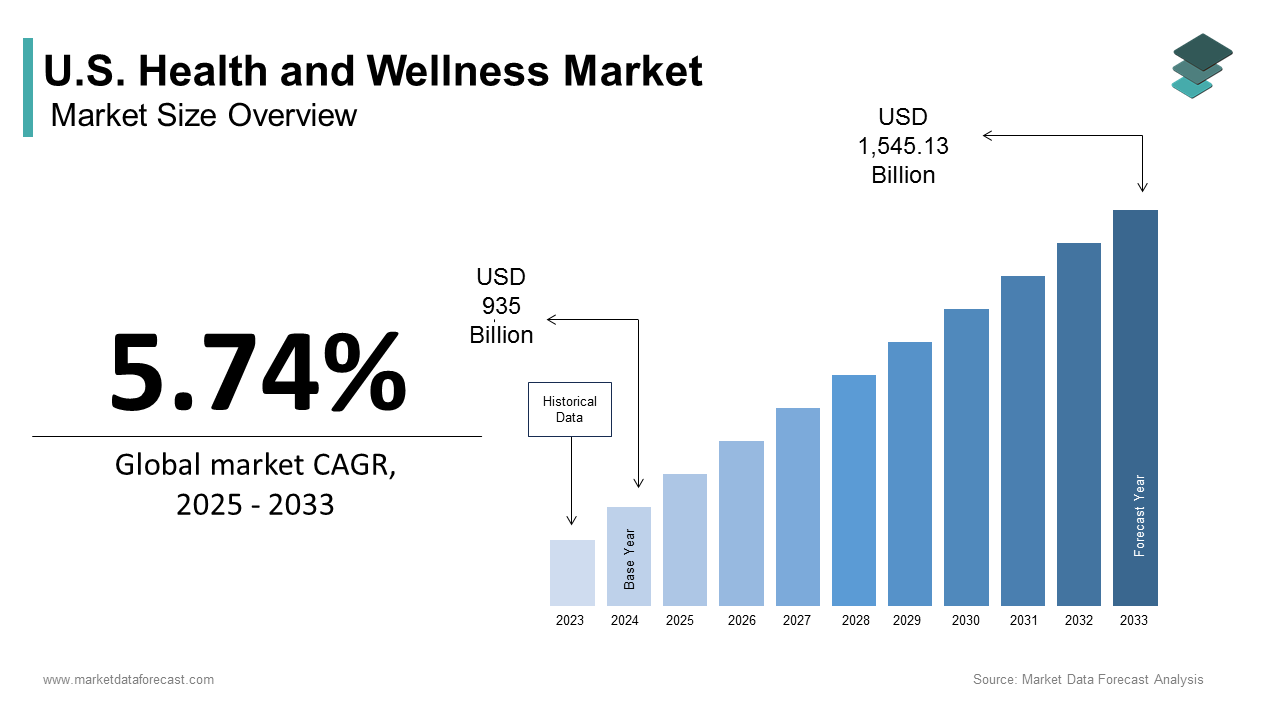

The U.S. health and wellness market size was valued at USD 935 billion in 2024 and is anticipated to reach USD 988.67 billion in 2025 and USD 1,545.13 billion by 2033, growing at a CAGR of 5.74% during the forecast period from 2025 to 2033.

Health and wellness are products, services, and behavioral interventions aimed at enhancing physical vitality, mental resilience, and preventive self-care beyond clinical treatment. As per the Centers for Disease Control and Prevention, 42.4% of American adults are clinically obese, a condition linked to 7 of the top 10 causes of death, while the National Institute of Mental Health confirms that 21% of U.S. adults experienced a mental illness in the past year. According to research, Americans spend more on fitness, supplements, and mindfulness apps than on tobacco or alcohol. This cultural pivot reflects not mere trend adoption but a structural recalibration of personal responsibility for health, driven by disillusionment with reactive medicine and empowered by digital self-tracking.

MARKET DRIVERS

The escalating burden of metabolic and lifestyle-related chronic diseases, which compel consumers to seek non-pharmaceutical interventions for prevention and symptom mitigation, drives the growth of the U.S. health and wellness market. As per the CDC’s National Diabetes Statistics Report, 96 million U.S. adults, over one-third of the population, live with prediabetes, 80% of whom are unaware of their condition. Simultaneously, as per the American Heart Association documents, only 24% of Americans meet minimum physical activity guidelines, while 45% sleep fewer than seven hours nightly, a triad that fuels insulin resistance and systemic inflammation. In response, a portion of adults use dietary supplements for metabolic support, according to sources, with magnesium, berberine, and omega-3s ranking among the top sellers for glucose and lipid modulation.

The mainstreaming of mental and emotional well-being as non-negotiable components of holistic health, caused by pandemic-era psychological strain and Gen Z’s destigmatization of self-care, propels the expansion of the U.S. health and wellness market. As per the American Psychological Association’s 2023 Stress in America survey, 76% of adults report experiencing health-impacting stress, while 59% say anxiety disrupts daily functioning. This has triggered mass adoption of mindfulness technologies. Also, according to research, millions of U.S. downloads, with peer-reviewed studies confirming that weeks of app-guided meditation reduce cortisol levels. Corporate wellness programs now embed mental resilience modules, which transform emotional hygiene from luxury to workplace necessity.

MARKET RESTRAINTS

Pervasive misinformation and pseudoscientific claims propagated through social media, which distort consumer understanding of evidence-based wellness, restrict the growth of the U.S health and wellness market. As per sources, a portion of viral “wellness hacks” on TikTok and Instagram, including celery juice cures and parasite cleanses, lack peer-reviewed validation, yet reach millions of users monthly. The Federal Trade Commission points out an increase in enforcement actions against supplement brands for unsubstantiated disease claims. This noise drowns out credible interventions. According to research, only a portion of consumers can distinguish FDA-evaluated structure/function claims from fraudulent therapeutic assertions, which leads to wasted expenditure and delayed clinical care for conditions like thyroid dysfunction or clinical depression.

Socioeconomic disparity in access to premium wellness resources, which entrenches health inequities under the guise of personal optimization, is another barrier hindering the expansion of the U.S. health and wellness market. As per the U.S. Census Bureau, households earning a notable amount annually spend a portion of their income on fitness and supplements, more than the proportional outlay of households earning, yet remain less likely to afford organic groceries, boutique fitness, or mental health apps, according to data from the Economic Policy Institute. According to the Robert Wood Johnson Foundation, food deserts and “fitness deserts” overlap in a portion of low-income zip codes, while Medicaid rarely covers nutrition counseling or stress-reduction programs. Consequently, wellness becomes a privilege. Life expectancy in affluent U.S. counties exceeds that in deprived ones by up to 20 years, as per NIH longitudinal data.

MARKET OPPORTUNITIES

The integration of continuous biometric sensing with AI-driven behavioral nudges, transforming passive tracking into proactive health orchestration, provides major opportunities for the growth of the U.S. health and wellness market. As per research, wearables detecting resting heart rate variability and nocturnal HR trends can predict inflammatory flare-ups hours in advance with notable accuracy. The National Science Foundation has awarded funds to startups developing closed-loop systems, such as WHOOP’s strain coach and Levels’ glucose-guided meal planner, that translate raw data into personalized action.

Employer-sponsored metabolic health programs that combine diagnostics, coaching, and financial incentives to reduce long-term healthcare costs which opens new opportunities for the expansion of the U.S. health and wellness market. As per the Integrated Benefits Institute, employees with prediabetes cost employers $1,200 more annually in absenteeism and presenteeism than metabolically healthy peers. In response, firms like Amazon and General Motors offer continuous glucose monitors paired with registered dietitian coaching. According to the Society for Human Resource Management, a portion of large employers plan to expand such offerings, particularly as CMS permits HSA funds for preventive digital therapeutics. This shift repositions wellness from perk to productivity infrastructure.

MARKET CHALLENGES

Regulatory ambiguity surrounding digital therapeutics and wellness apps that border on medical claims without FDA clearance challenges the growth of the U.S. health and wellness market. As per sources, a large number of mental health and nutrition apps operate without clinical validation or data privacy certification, despite influencing behaviors for depression, eating disorders, and hypertension. The FDA’s enforcement discretion policy for “low-risk general wellness” tools, last updated in 2019, fails to address AI-driven diagnostic features embedded in apps. As per research, a share of users treat app-generated health scores as clinical advice, risking mismanagement of conditions like PCOS or adrenal fatigue, syndromes often misdiagnosed by algorithmic questionnaires lacking differential analysis.

Consumer fatigue and skepticism stemming from the commodification of self-care, where wellness is marketed as consumable rather than cultivatable, also impedes the expansion of the U.S. health and wellness market. Many Americans feel burdened by the sheer number of wellness products and contradictory guidance, which often leads them to give up on routines quickly, as per research. According to studies, social pressures and unrealistic standards promoted online contribute to feelings of shame that can influence mental health support-seeking. Subscription-based wellness services also face high cancellation rates, as per sources, suggesting that models focused on short-term novelty struggle to maintain long-term engagement without grounding in behavioral science principles.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.74% |

| Segments Covered | By Product Type, Distribution Channel, Category Type, End User, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado |

| Market Leaders Profiled | Procter & Gamble, Herbalife Nutrition Ltd., Abbott Laboratories, Amway Corp., Humana Inc., Virgin Pulse, ComPsych Corporation, EXOS, Privia Health, Wellsource Inc., United Natural Foods Inc. (UNFI), GNC Holdings LLC, Medifast Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2024, the health and wellness food segment led the U.S. health and wellness market by occupying 38.5% share 2024. The convergence of metabolic urgency and culinary convenience has significantly contributed to the growth of the health and wellness food segment in the global market. A portion of American adults actively seek foods labeled gut-health supporting or blood sugar balancing, according to the International Food Information Council. As per studies, a share of adults with prediabetes modify their diet before considering medication, a behavioral pivot driving sales of fiber-enriched bars, plant sterol-fortified spreads, and low-glycemic meal replacements. Simultaneously, retailers like Kroger and Whole Foods have tripled shelf space for condition-specific nutrition, which embeds dietitian-curated bundles for inflammation, sleep, and stress.

The preventive and personalized health segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 16.2% from 2025 to 2033. The rapid growth of the preventive and personalized health segment is propelled by consumer access to at-home biomarker testing and AI-driven coaching platforms. Simultaneously, the NIH’s All of Us Research Program has enrolled over 750,000 Americans in genomic and metabolic profiling, normalizing data-driven self-optimization. Employers now subsidize these services. A portion of Fortune firms reimburse personalized nutrition subscription.

By Distribution Channel Insights

The offline retail segment held a leading share of 61.7% of the U.S. health and wellness market in 2024. The prominence of the offline retail segment is due to tactile trust and immediacy. According to studies, a majority of supplement buyers still prefer receiving guidance from pharmacists or nutritionists during in-store visits. As per sources, large retail chains are redesigning store layouts to include wellness-focused spaces, which combine expert consultations with tailored product placement. According to research, most purchases of organic and functional foods happen in physical supermarkets, where customers value the ability to assess products through sensory cues like texture, scent, and ingredient visibility.

The online channels segment is expected to exhibit a noteworthy CAGR of 21.4% during the forecast period. Algorithmic personalization and subscription fatigue mitigation are boosting the growth of the online channels segment in the global market. Amazon’s “Health & Personal Care” category now recommends products based on Prime member purchase history and Alexa-voiced symptom queries, a model increasing conversion compared to static search, as per internal Amazon Retail Science disclosures. Simultaneously, direct-to-consumer brands like Ritual and Care/of deploy quiz-based customization and auto-replenishment, reducing decision paralysis. The pandemic’s digital acceleration endures.

By End User Insights

The adults aged 25–64 segment dominated the U.S. health and wellness market by accounting for a substantial share in 2024. The growth of the adults aged 25–64 segment is fuelled by peak earning power with escalating metabolic and psychological stressors. As per the CDC, 44% of working-age adults have at least one chronic condition, including hypertension, anxiety, or insulin resistance, which are driving demand for condition-specific supplements, sleep aids, and fitness tech. Corporate wellness penetration amplifies this. A portion of employers with staff offer subsidized gym memberships or mindfulness apps, as per studies. Furthermore, a share of millennial parents prioritize spending, organic groceries, air purifiers, and non-toxic cleaning, which embeds health-conscious habits early, a trend quantified by Euromonitor’s household consumption tracker.

The seniors aged 65+ segment is predicted to witness the highest CAGR of 12.8% from 2025 to 2033. The swift expansion is due to demographic factors, the U.S. Census Bureau projects millions of seniors by 2040, and behavioral aspects, a portion of older adults now proactively invest in mobility aids, cognitive supplements, and fall-prevention tech. Older adults who combine physical strength exercises with proper nutritional supplementation show significant improvements in managing age-related frailty, as per research. In response to this shift, retailers are developing store formats that cater specifically to senior needs by offering accessible product displays and comfortable consultation areas, according to studies.

By Category Type Insights

The organic products segment was the largest segment and captured 42.7% of the U.S. health and wellness market in 2024. The dominance of the organic products segment is due to consumer perception of purity and regulatory trust. Most consumers associate the “USDA Organic” label with complete avoidance of synthetic pesticides and genetically modified ingredients, as per sources. The CDC’s National Health and Nutrition Examination Survey confirms organic consumers exhibit 65% lower urinary pesticide metabolites than conventional eaters. Retailers amplify this. Whole Foods dedicates 89% of shelf space to certified organic SKUs, while Kroger’s Simple Truth line embeds organic defaults across 1,200 SKUs BY normalizing premium pricing for perceived safety.

The functional foods segment is estimated to register the fastest CAGR of 18.7% over the forecast period, owing to condition-specific formulation and clinical substantiation. Brands like Olipop (prebiotic soda) and Huel (meal-replacement shakes) cite peer-reviewed studies in packaging. According to studies, functional beverages containing prebiotic ingredients have been shown to improve gut health within a short time frame. As per sources, updated U.S. regulatory guidelines now allow health-related claims for certain beneficial nutrients, expanding product availability in retail stores. According to research, younger consumers increasingly prefer foods and drinks that offer specific health benefits rather than focusing solely on taste.

REGIONAL ANALYSIS

The U.S. health and wellness market was the top performer in 2024 because of high disposable income, fragmented healthcare disillusionment, digital self-tracking penetration, and entrepreneurial product innovation. A large share of adults in the United States actively engage in wellness practices each week, reflecting a growing focus on preventive health, as per research. Spending patterns also show that Americans now allocate more of their budget to fitness, nutritional products, and mental wellness tools than to conventional indulgences like alcohol or fast food, according to studies.

Product personalization anchored in biomarker feedback remains central, with firms embedding AI quizzes, at-home test integration, and dynamic replenishment. Strategic retail theater — in-store wellness zones with diagnostic kiosks and live coaching — transforms passive shopping into experiential health engagement. Companies aggressively pursue FDA-qualified health claims and third-party clinical validation to combat consumer skepticism. Collaborative employer programs embed products into corporate benefits, shifting cost from discretionary to reimbursed. Lastly, cultural hybridization by merging Western science with Eastern botanicals unlocks relevance in the Asia Pacific while differentiating U.S. offerings through “global wisdom” narratives.

The U.S. health and wellness market is a hyper-fragmented, ideologically charged arena where multinational CPG giants compete with digitally native vertical brands through clinical credibility, algorithmic personalization, and retail experience innovation. Incumbents leverage shelf dominance and insurance partnerships, while disruptors target micro-segments, perimenopausal women, biohackers, and neurodivergent professionals, with hyper-specific formulations. Regulatory arbitrage defines velocity: firms exploit the FDA’s structure/function claim loophole while racing to secure qualified health claims. Simultaneously, consolidation accelerates as beauty, food, and pharma converge. Competition is no longer product-centric; it’s identity-driven, demanding brands that align with consumers’ self-concept as “optimized,” “clean,” or “bio-individual.”

KEY MARKET PLAYERS

A few of the dominating players in the U.S. health and wellness market include

- Procter & Gamble

- Herbalife Nutrition Ltd.

- Abbott Laboratories

- Amway Corp.

- Humana Inc.

- Virgin Pulse

- ComPsych Corporation

- EXOS

- Privia Health

- Wellsource, Inc.

- United Natural Foods, Inc. (UNFI)

- GNC Holdings, LLC

- Medifast, Inc.

MARKET SEGMENTATION

This research report on the U.S. health and wellness market is segmented and sub-segmented into the following categories.

By Product Type

- Beauty and personal care products

- Health and wellness food

- Wellness tourism

- Fitness equipment

- Preventive and personalized health

By Distribution Channel

- Online

- Offline

By End Use

- Adults

- Children

- Seniors

By Category Type

- Organic

- Natural

- Functional Foods

- Plant-Based

By Region

- New York

- Massachusetts

- Pennsylvania

- Illinois

- Ohio

- Michigan

- Texas

- Florida

- Georgia

- California

- Washington

- Colorado

Frequently Asked Questions

1. What factors are driving the growth of this market?

Rising awareness about preventive healthcare, growing emphasis on mental health and stress management, increased spending on personal wellness products, expansion of digital health and fitness platforms, and an aging population, and chronic disease prevention

2. Who are the major players in the U.S. health & wellness market?

Major companies include Procter & Gamble, Herbalife Nutrition Ltd., Abbott Laboratories, Amway Corp., Humana Inc., Virgin Pulse, ComPsych Corporation, EXOS, Privia Health, Wellsource Inc., United Natural Foods Inc. (UNFI), GNC Holdings LLC, and Medifast Inc.

3. What role does technology play in this market?

Technology enables remote health monitoring, personalized wellness solutions, fitness tracking, telemedicine, and digital mental health support, making wellness more accessible and effective.

4. Which consumer trends are shaping the market?

Focus on natural and organic products, Personalized wellness plans, Demand for mental health support, Home-based fitness solutions, and Corporate wellness adoption

5. How important is mental health in this market?

Mental wellness is a fast-growing segment, with rising demand for stress management tools, therapy apps, workplace wellness programs, and meditation services.

6. How is the corporate wellness sector contributing to growth?

Companies are investing in wellness programs to improve employee productivity, reduce healthcare costs, and enhance job satisfaction, driving significant demand for corporate wellness services.

7. What challenges does the market face?

The Challenges in the market are high costs of premium wellness products, unequal access to wellness services, regulatory and compliance issues in healthcare segments, and an overcrowded market with varying quality standards

8. How are sustainability and clean living trends influencing this market?

Consumers are demanding eco-friendly packaging, clean-label products, cruelty-free personal care, and organic nutritional supplements, pushing brands to adopt sustainable practices.

9. What opportunities exist for new entrants in this market?

The Opportunities in the market are the development of digital health and fitness platforms, Affordable wellness products for underserved segments, Innovative mental health services, and Personalized nutrition and lifestyle offerings

10. What is the future outlook of the U.S. health & wellness market?

The market is expected to continue growing strongly, driven by lifestyle shifts, aging demographics, technological innovation, and increasing consumer focus on holistic well-being.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com