U.S Food Delivery Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Channel, Payment Mode, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Food Delivery Market Report Summary

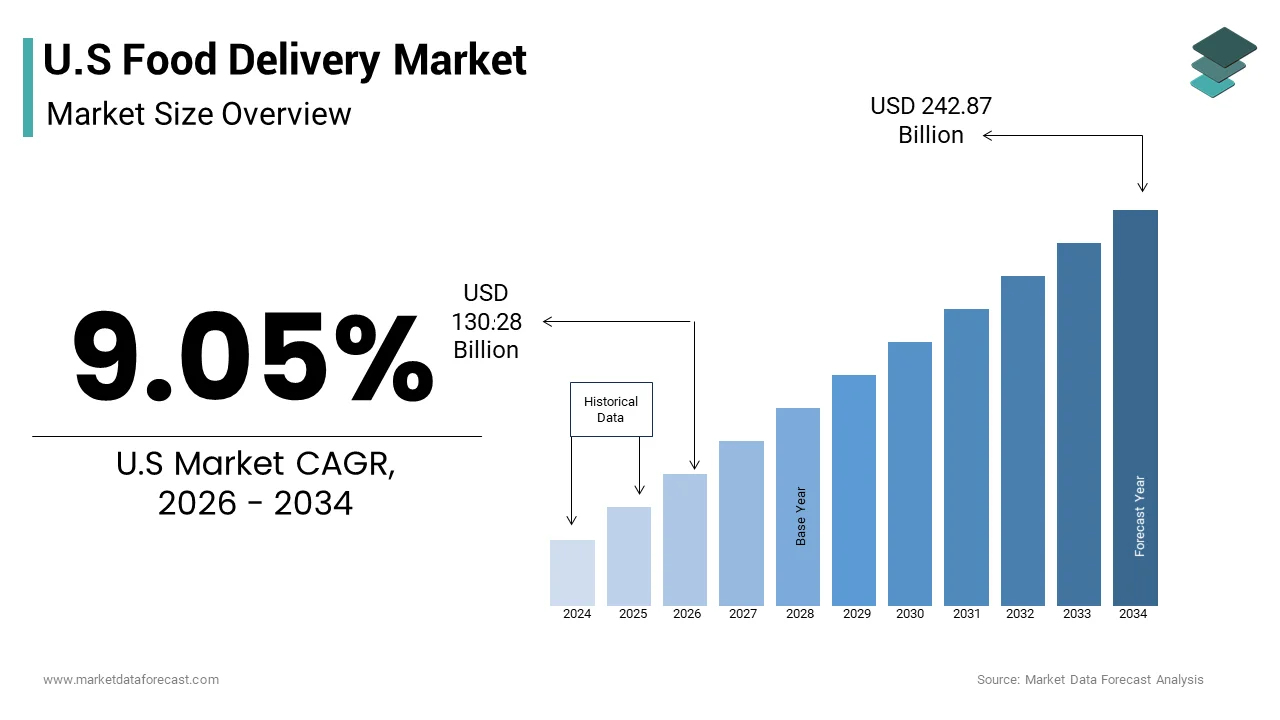

The United States food delivery market was valued at USD 119.46 billion in 2025 and is anticipated to reach USD 130.28 billion in 2026 and USD 242.87 billion by 2034, growing at a CAGR of 9.05% during the forecast period from 2026 to 2034. The growth of the U.S. food delivery market is driven by increasing consumer preference for convenience, rapid adoption of digital ordering platforms, and the expanding penetration of smartphones and internet connectivity. The rising demand for contactless delivery services, busy urban lifestyles, and growing partnerships between restaurants and delivery platforms are further accelerating market expansion. In addition, advancements in AI-based recommendations, real-time order tracking, and subscription-based loyalty programs are enhancing customer engagement and driving repeat purchases across the country.

Key Market Trends

- Rising adoption of mobile-based food ordering applications due to improved user experience, digital payment integration, and personalized recommendations.

- Increasing consumer preference for platform-to-consumer delivery models offering wider restaurant choices, faster delivery, and promotional discounts.

- Growing integration of AI, data analytics, and automation technologies to optimize delivery routes, customer targeting, and operational efficiency.

- Expansion of cloud kitchens and virtual restaurants to meet rising online food demand while reducing operational costs for restaurant operators.

- Increasing focus on sustainable packaging, electric delivery fleets, and eco-friendly operations among leading food delivery companies.

Segmental Insights

- Based on type, the platform-to-consumer segment was the largest and held 41.2% of the United States food delivery market share in 2025. The dominance of this segment is attributed to the increasing popularity of third-party delivery platforms that provide consumers with access to multiple restaurant options, convenient ordering systems, and faster delivery services.

- Based on channel, the mobile application segment accounted for 46.3% of the United States food delivery market share in 2025. The segment growth is driven by the widespread use of smartphones, user-friendly mobile interfaces, real-time tracking features, and attractive app-based offers and loyalty rewards.

- Based on payment mode, the online payment segment held a significant share of the United States food delivery market in 2025. The increasing adoption of digital wallets, contactless payment solutions, and secure online transaction systems has significantly contributed to the growth of this segment.

Regional Insights

The U.S. food delivery market is witnessing strong growth across metropolitan and suburban regions, supported by increasing internet penetration, changing food consumption habits, and the rapid expansion of delivery infrastructure. Major urban centers such as New York City, Los Angeles, and Chicago remain key contributors due to high consumer demand for convenience-based dining solutions and strong restaurant network presence. The growing adoption of food delivery services among younger demographics and working professionals continues to support nationwide market growth.

Competitive Landscape

The U.S. food delivery market is highly competitive, with major players focusing on technological innovation, faster delivery services, subscription programs, and strategic partnerships with restaurants and grocery providers. Companies are increasingly investing in AI-powered logistics, drone and autonomous delivery testing, and customer loyalty initiatives to strengthen market positioning. Expansion into grocery delivery and quick-commerce services is also creating new growth opportunities for industry participants.

Prominent players in the U.S. food delivery market include Uber Eats, Grubhub, Uber Technologies Inc., DoorDash, Domino’s Pizza, Just Eat Takeaway, Zomato, Food Panda, Swiggy, Deliveroo, and Postmates.

U.S Food Delivery Market Size

The U.S food delivery market size was valued at USD 119.46 billion in 2025 and is anticipated to reach USD 130.28 billion in 2026 to reach USD 242.87 billion by 2034, growing at a CAGR of 9.05% during the forecast period from 2026 to 2034.

MARKET OVERVIEW

The food delivery is the digital ecosystem connecting consumers with restaurants and grocery retailers through third party platforms and proprietary logistics networks. The definition extends beyond simple transaction facilitation to include complex last mile logistics algorithmic dispatching and real time tracking systems that ensure timely fulfillment. As per the Bureau of Labor Statistics approximately 60% of American households have two earners which significantly reduces the time available for meal preparation and increases reliance on external food sources. Furthermore, 97% of Americans own a mobile phone creating the necessary hardware foundation for ubiquitous app usage and on demand ordering, as per research. The integration of these devices into daily routines allows for seamless interaction with delivery platforms regardless of location. Consumer behavior has shifted toward valuing time efficiency and variety leading to frequent engagement with multiple delivery applications. These structural elements define the operational landscape where technology mediates the relationship between hungry consumers and food providers.

MARKET DRIVERS

Ubiquitous Smartphone Penetration and Digital Convenience

The pervasive adoption of smartphones by enabling instant access to diverse culinary options is propelling the growth of the United States food delivery market. Mobile devices function as the central interface for ordering allowing users to browse menus compare prices and track deliveries in real time. According to the study, the number of smartphone users in the United States reached 306 million in 2023, representing a penetration rate that ensures nearly universal access to delivery applications. This high level of connectivity means that consumers can place orders from virtually any location including offices homes and public spaces, which increases the frequency of transactions. The convenience of saving payment information and favorite orders reduces friction in the checkout process encouraging impulse purchases and repeat usage. Furthermore, the integration of location services allows platforms to provide accurate delivery estimates and optimize driver routes which enhances customer satisfaction. The ability to receive push notifications about promotions and order status keeps users engaged with the platform throughout the day. These technological synergies between hardware capability and software innovation ensure that smartphones remain the dominant channel for food delivery growth.

Changing Lifestyle Patterns and Dual Income Households

The shift in lifestyle patterns characterized by longer working hours and the prevalence of dual income households is another attribute fuelling the growth of the United States food delivery market. Modern consumers often lack the time or energy to cook after work leading them to seek convenient alternatives for meal consumption. As per the Bureau of Labor Statistics, the average American works approximately 8.5 hours per day, which leaves limited time for grocery shopping and meal preparation. This time scarcity creates a strong value proposition for delivery platforms that offer quick and reliable access to prepared meals. The rise of remote work has also blurred the lines between professional and personal time leading to increased demand for lunch and dinner delivery during traditional work hours. Furthermore, the growing number of single person households reduces the economic efficiency of cooking at home making delivery a cost effective option for individuals. The desire for variety and exploration of new cuisines without the effort of travel further motivates consumers to use delivery apps. These demographic and behavioral trends ensure that food delivery remains a integral solution for modern dietary needs.

MARKET RESTRAINTS

High Operational Costs and Thin Profit Margins

The high operational costs associated with last mile logistics and the resulting thin profit margins is limiting the growth of the United States food delivery market. Delivering individual orders to dispersed locations requires substantial investment in driver compensation insurance and technology infrastructure which erodes profitability. The average commission fee charged to restaurants ranges from 15 to 30%, which places a financial burden on already margin constrained food establishments, as per the study. This cost structure often leads to higher menu prices for delivery customers reducing the attractiveness of the service compared to dining in or takeout. The need to subsidize delivery fees to remain competitive further strains the financial viability of delivery platforms. Additionally, the volatility of fuel prices and vehicle maintenance costs adds unpredictability to operational expenses. Platforms struggle to balance affordability for consumers fair compensation for drivers and reasonable fees for restaurants. This triangular tension limits the ability of companies to achieve consistent profitability and scale efficiently. The economic model relies heavily on volume and density which are difficult to maintain in suburban and rural areas.

Regulatory Pressures on Labor Classification

The ongoing regulatory scrutiny regarding the classification of delivery workers, as independent contractors versus employees is another attribute hindering the growth of the United States food delivery market. Legal challenges and legislative efforts in various states aim to reclassify gig workers which would require platforms to provide benefits such as minimum wage healthcare and paid leave. As per the California Legislative Information Assembly Bill 5 established strict criteria for employee classification although subsequent propositions have created exemptions the legal uncertainty persists. This potential increase in expenses forces companies to raise prices for consumers or reduce driver incentives, which may negatively impact service quality and availability. Furthermore, differing regulations across states create a complex compliance landscape that increases administrative burdens and legal risks. The threat of costly litigation and penalties discourages investment and expansion in certain jurisdictions. Platforms must navigate this evolving legal environment while maintaining a flexible workforce that can scale with demand. The outcome of these regulatory battles will determine the future structure of the gig economy and the operational flexibility of delivery companies.

MARKET OPPORTUNITIES

Expansion into Grocery and Retail Delivery

The expansion of food delivery platforms into grocery and retail sectors by diversifying revenue streams and increasing order frequency is certainly to create new opportunities for the growth of the United States food delivery market. Consumers increasingly expect the same convenience for household essentials, as they do for prepared meals leading to a convergence of delivery services. Delivery platforms leverage their existing logistics networks and driver bases to fulfill grocery orders efficiently without significant additional infrastructure investment. The higher average order value of grocery transactions compared to restaurant meals improves unit economics and profitability. Furthermore, the integration of quick commerce models offering delivery within 15 to 30 minutes addresses the need for immediate convenience. This expansion allows platforms to become comprehensive lifestyle apps rather than just food services. The ability to cross sell products and offer bundled subscriptions enhances customer retention and lifetime value.

Integration of Autonomous Delivery Technologies

The integration of autonomous delivery technologies, such as drones and sidewalk robots to reduce labor costs and improve efficiency is another factor to amplify the growth of the United States food delivery market. These technologies address the challenge of driver shortages and rising labor expenses by automating the last mile delivery process. The several companies have received approval for commercial drone delivery operations in select US cities marking a regulatory milestone. Data from Starship Technologies indicates that autonomous robots have completed over 4 million deliveries globally demonstrating the scalability and reliability of this technology. Autonomous solutions can operate continuously without breaks reducing delivery times and increasing throughput during peak hours. The lower marginal cost of robot delivery compared to human drivers improves unit economics especially for short distance orders. Furthermore, autonomous vehicles can navigate traffic more efficiently and reduce the carbon footprint of delivery operations appealing to environmentally conscious consumers. Partnerships with technology firms and municipalities facilitate the deployment of these innovations in controlled environments.

MARKET CHALLENGES

Driver Retention and Workforce Stability

The retention and workforce stability due to the high turnover rates inherent in the gig economy is acting as a barrier for the growth of the United States food delivery market. Delivery platforms rely on a flexible pool of independent contractors, who often switch between multiple apps or leave the workforce entirely due to dissatisfaction with pay and working conditions. The instability leads to inconsistent service quality and delayed deliveries, particularly during peak hours when demand exceeds supply. The company spends hundreds of millions of dollars annually on driver incentives and bonuses to maintain adequate staffing levels. The lack of benefits and job security makes it difficult to build a loyal and experienced workforce. Furthermore, competition among platforms for drivers drives up compensation costs which impacts profitability. Fluctuations in gas prices and vehicle maintenance expenses further discourage individuals from continuing as drivers. The inability to guarantee consistent earnings leads to frustration and attrition among the workforce. Platforms must continually innovate their incentive structures and support systems to attract and retain drivers. Failure to address these workforce challenges can result in service disruptions and damage to brand reputation.

Food Quality and Temperature Control Issues

Maintaining food quality and temperature control during transit is affecting customer satisfaction and brand trust, which is to hinder the growth of the United States food delivery market. Prepared meals are sensitive to time and temperature fluctuations, which can degrade texture flavor and safety during the delivery process. Insufficient packaging and long delivery times contribute to soggy cold or spilled items which fail to meet consumer expectations. Complaints related to food condition account for a significant portion of customer support interactions requiring refunds and credits. The variability in driver handling and equipment, such as insulated bags further exacerbates the issue. Restaurants struggle to design packaging that withstands transit, while remaining eco-friendly and cost effective. Platforms face the difficulty of optimizing delivery routes to minimize time without compromising efficiency. The lack of direct control over the final handoff means that quality assurance is challenging to enforce. Negative experiences lead to negative reviews and churn which are costly to reverse.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.05% |

| Segments Covered | By Type, Channel, Payment Mode, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Uber Eats (U.S.), Grubhub (U.S.), Uber Technologies Inc, DoorDash (U.S.), Domino’s Pizza (U.S.), Just Eat Takeaway (Europe), Zomato (India), Food Panda (Singapore), Swiggy (India), Deliveroo (Europe), Postmates (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The platform to consumers segment was the largest by holding 41.2% of the United States food delivery market share in 2025. These third party platforms, such as DoorDash, Uber Eats, and Grubhub, allow consumers to browse menus from hundreds of local and chain restaurants without needing to visit individual websites or make phone calls. This centralization reduces search costs and decision fatigue for consumers who value variety and speed. The algorithms used by these platforms personalize recommendations based on past behavior which enhances user engagement and order frequency. Furthermore the integration of loyalty programs and subscription services like DashPass or Uber One encourages repeat usage by offering waived delivery fees. The extensive marketing budgets of these platforms also drive high brand awareness and customer acquisition.

The restaurants to consumers segment is lucratively growing at an anticipated CAGR of 12.3% from 2026 to 2034. Many restaurants are investing in their own proprietary delivery infrastructure and websites to avoid the high fees charged by aggregators, which can range from 15 to 30% per order. As per the National Restaurant Association, 40% of independent restaurant owners plan to increase investment in direct online ordering systems in 2024 to retain more revenue. Data from Toast indicates that restaurants using direct ordering channels see a 20% higher average order value compared to those relying solely on third party platforms. This financial incentive drives the rapid adoption of branded apps and web portals. Furthermore, direct channels allow restaurants to offer exclusive promotions and loyalty rewards that are not possible on aggregated platforms. The ability to customize the user experience and packaging reinforces brand loyalty and differentiation. As technology solutions for small businesses become more affordable and accessible the barrier to entry for direct delivery lowers. This shift empowers restaurants to capture a larger share of the value chain and reduce dependence on external intermediaries.

By Channel Insights

The mobile application segment was accounted in holding 46.3% of the United States food delivery market share in 2025 with a superior user experience with enhanced personalization features that drive engagement and convenience. Apps provide intuitive interfaces faster loading times and access to device specific functionalities, such as GPS location services and push notifications. Food delivery apps leverage this behavior to send targeted promotions reminders and order updates which keep users engaged and encourage frequent purchases. The ability to save payment methods addresses and favorite orders reduces friction and enables one click purchasing, which is for impulse buys. Furthermore, apps utilize machine learning to recommend restaurants and dishes based on individual preferences and order history creating a highly personalized experience. The integration of loyalty programs and gamification elements within apps further incentivizes usage and retention. Push notifications allow platforms to re engage dormant users with timely offers increasing conversion rates.

The website segment is esteemed to witness a fastest CAGR of 8.2% during the forecast period with the integration with voice search technologies and smart home devices. Consumers are increasingly using smart speakers and voice assistants to place orders, which often redirect them to mobile optimized websites or progressive web apps. Websites are easier to optimize for voice search queries compared to native applications which require specific opening commands. Progressive web apps combine the best features of websites and apps offering fast loading times and offline capabilities without requiring installation. This flexibility appeals to users who prefer not to download multiple applications for occasional use. Furthermore, websites are easily accessible via links shared on social media and email campaigns reducing the friction of discovery. The ability to index content for search engines improves visibility and organic traffic for delivery platforms.

By Payment Mode Insights

The online payment segment held a significant share of the United States food delivery market share in 2025 with enhanced security and convenience for digital transactions. Consumers prefer storing payment information securely within apps and websites to enable fast and effortless checkout experiences. Food delivery platforms integrate with trusted payment gateways and digital wallets such as Apple Pay, Google Pay, and PayPal, which utilize tokenization and encryption to protect sensitive data. The ability to split bills and manage expenses through digital records also appeals to users. Furthermore, online payments facilitate seamless refunds and dispute resolutions which are critical for maintaining customer trust in case of order issues. The reduction of physical contact during transactions has also boosted the preference for cashless options post pandemic. Platforms often offer incentives such as discounts or cashback for using specific digital payment methods, which further drives adoption.

The cash on delivery segment is likely to grow at an anticipated CAGR of 8.3% from 2026 to 2034 due to efforts to include unbanked or underbanked populations, who lack access to traditional digital payment methods. Although, less common than in other regions there is a niche demographic that relies on cash for financial transactions due to privacy concerns or lack of banking infrastructure. Some delivery platforms and local restaurants offer cash on delivery options to cater to these individuals ensuring broader market accessibility. Data from the National Endowment for Financial Education suggests that financial insecurity leads some consumers to prefer cash to avoid overdraft fees or debt accumulation. Furthermore, cash payments appeal to individuals, who are sharing financial data online due to security fears. While logistical challenges exist the social imperative to provide equitable access drives the gradual growth of this segment. Partnerships with community organizations and localized marketing efforts help raise awareness of cash payment options.

COMPETITIVE LANDSCPAE

The competition in the United States food delivery market is intense and characterized by rivalry among a few dominant platforms and numerous regional players. Major companies compete on delivery speed cost reliability and the breadth of restaurant selections available to consumers. Price wars and promotional discounts are common tactics used to attract new users and retain existing ones in a saturated market. Differentiation often comes from exclusive partnerships with popular restaurant chains and the integration of additional services like grocery delivery. Customer loyalty is fragile as switching costs are low and users frequently compare prices across multiple apps before placing orders. Innovation in technology such as AI driven logistics and personalized recommendations drives competitive advantage. Regulatory pressures regarding worker classification and commission fees add complexity to operational strategies. Platforms must balance profitability with market share growth while maintaining positive relationships with restaurant partners. The rise of direct ordering channels by restaurants also poses a threat to aggregator dominance.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S food delivery market are

- Uber Eats (U.S.)

- Grubhub (U.S.)

- Uber Technologies Inc

- DoorDash (U.S.)

- Domino’s Pizza (U.S.)

- Just Eat Takeaway (Europe)

- Zomato (India)

- Food Panda (Singapore)

- Swiggy (India)

- Deliveroo (Europe)

- Postmates (U.S.)

Top Players In The Market

- DoorDash Inc maintains a dominant position in the United States food delivery market by offering a comprehensive platform that connects consumers with local restaurants and retailers. The company leverages advanced logistics technology to optimize delivery routes and ensure timely service across urban and suburban areas. Recent actions include the expansion of its DashPass subscription program which provides members with free delivery and reduced service fees. DoorDash has also diversified its offerings by integrating grocery convenience store and alcohol delivery services to increase order frequency. The company invests heavily in merchant tools that help restaurants manage online orders and analyze customer data.

- Uber Technologies Inc contributes significantly to the US food delivery market through its Uber Eats platform which integrates seamlessly with its global mobility network. The company utilizes its extensive driver base to provide reliable and fast delivery services for meals and groceries. Recent strategies involve deepening partnerships with major restaurant chains and retail brands to offer exclusive menu items and promotions. Uber Eats has also enhanced its advertising platform allowing merchants to promote their listings directly to hungry customers. The integration of Uber One membership creates a unified subscription experience across ride hailing and delivery services. This cross platform synergy increases user retention and lifetime value.

- Grubhub Inc operates as a key player in the United States food delivery market by connecting diners with a vast network of local eateries and national chains. The company focuses on providing robust marketing and operational support to restaurant partners to help them grow their online presence. Recent actions include the integration with Amazon Prime which offers members free delivery benefits on eligible orders. Grubhub has also upgraded its app interface to improve user experience and streamline the ordering process. The platform emphasizes community engagement by highlighting local businesses and offering curated dining recommendations. Grubhub invests in data analytics to help merchants understand consumer preferences and optimize their menus.

Top Strategies Used By Key Market Participants

Key players in the United States food delivery market primarily focus on expanding into adjacent categories such as grocery and convenience retail to diversify revenue streams. Companies are increasingly investing in subscription models that offer waived delivery fees and exclusive perks to enhance customer loyalty and retention. Strategic partnerships with major restaurant chains and technology providers enable platforms to offer unique content and improved operational efficiency. Investment in autonomous delivery technologies including drones and robots aims to reduce long term labor costs and improve speed. Enhancing advertising platforms allows merchants to promote their offerings directly within apps creating new high margin revenue sources. Providers are also prioritizing sustainability initiatives such as eco-friendly packaging and carbon neutral delivery options to appeal to conscious consumers.

MARKET SEGMENTATION

This research report on the U.S food delivery market is segmented and sub-segmented into the following categories.

By Type

- Powder Platforms-to-consumers

- Restaurants- to-consumers

By Channel Type

- Mobile Application

- Websites

By Payment Mode

- Online Payment

- Cash-on-Delivery

By Business Model

- Grocery Delivery

- Meal Delivery

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is the U.S. food delivery market?

The U.S. food delivery market includes online platforms and services that deliver meals and beverages directly to consumers.

What is driving the growth of the U.S. food delivery market?

The market is growing due to increasing smartphone usage and rising demand for convenience-based services.

What types of food delivery services are available in the U.S.?

Common services include restaurant delivery, grocery delivery, cloud kitchens, and subscription meal services.

Which segment dominates the U.S. food delivery market?

Restaurant-to-consumer delivery dominates the market due to strong demand for online meal ordering.

How is technology impacting the U.S. food delivery market?

AI-based recommendations, real-time tracking, and digital payment systems are enhancing customer experience.

Who are the primary users of food delivery services in the U.S.?

Urban consumers, working professionals, students, and families are major users of food delivery platforms.

Why are mobile food delivery apps gaining popularity?

They provide quick ordering, flexible payment options, and convenient doorstep delivery services.

What challenges does the U.S. food delivery market face?

High operational costs, delivery delays, and intense competition can affect market growth.

How do cloud kitchens influence the food delivery market?

Cloud kitchens support faster delivery operations and lower infrastructure costs for food businesses.

What is the future outlook for the U.S. food delivery market?

The market is expected to grow steadily with increasing digital adoption and changing consumer lifestyles.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com