U.S. Dental Market Size, Share, Trends & Growth Forecast Report By Specialty, Financing Source, Practice Type, Zone, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Dental Market Report Summary

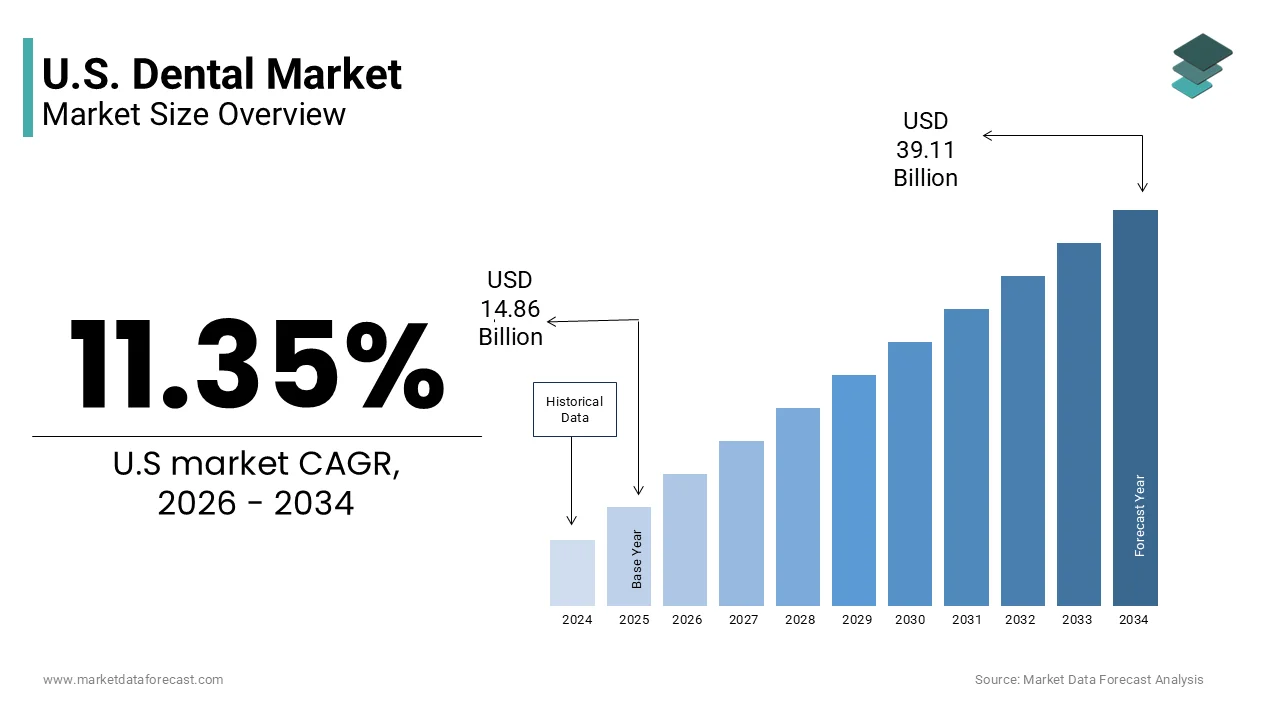

The U.S. dental market was valued at USD 14.86 billion in 2025, is estimated to reach USD 16.55 billion in 2026, and is projected to reach USD 39.11 billion by 2034, growing at a CAGR of 11.35% during the forecast period. Market growth is driven by increasing awareness of oral health, rising demand for cosmetic dentistry, and advancements in dental technologies. The growing aging population and expanding insurance coverage are further contributing to higher dental service utilization. Additionally, innovations in digital dentistry, including imaging and orthodontic solutions, are supporting strong market expansion across the United States.

Key Market Trends

- Rising awareness of oral hygiene and preventive care is driving market growth.

- Increasing demand for cosmetic and aesthetic dental procedures is boosting demand.

- Growing adoption of advanced dental technologies and digital solutions is supporting market expansion.

- Expansion of dental insurance coverage is improving treatment accessibility.

- Rising geriatric population is increasing demand for dental services.

Segmental Insights

- Based on specialty, the general dentistry segment held a dominant share of the U.S. dental market in 2025. This dominance is attributed to routine dental procedures such as checkups, cleanings, and preventive treatments.

- Based on financing source, the private health insurance segment held a significant share of the U.S. dental market in 2025, driven by widespread insurance coverage and reimbursement support.

- Based on practice type, the solo practices segment accounted for 43.2% of the U.S. dental market share in 2025, supported by the large number of independent dental practitioners across the country.

Competitive Landscape

The U.S. dental market is highly competitive, with key players focusing on technological innovation, product development, and expansion of service offerings to strengthen their market position. Companies are investing in digital dentistry, orthodontic solutions, and advanced dental materials. Prominent players in the U.S. dental market include Dentsply Sirona, Align Technology, Inc., SHOFU INC., VATECH, 3M, Zimmer Biomet, Institut Straumann AG, Ultradent Products Inc., and Bien-Air Medical Technologies.

U.S. Dental Market Size

The U.S. dental market was valued at USD 14.86 billion in 2025, is estimated to reach USD 16.55 billion in 2026, and is projected to reach USD 39.11 billion by 2034, growing at a CAGR of 11.35% from 2026 to 2034.

The dental is the clinical service, diagnostic technology, and digital solutions to maintain oral health and aesthetic appearance. According to the American Dental Association, approximately 64% of Americans visited a dentist in 2022, reflecting consistent but uneven utilization rates across demographic groups. As per the Centers for Disease Control and Prevention, nearly half of all adults aged 30 years or older show signs of gum disease, indicating a substantial underlying demand for periodontal care and preventive services. The integration of digital dentistry, including computer aided design and computer aided manufacturing systems, is transforming clinical workflows and patient experiences. Regulatory frameworks enforced by the Food and Drug Administration ensure the safety and efficacy of dental devices and materials. Consumer awareness regarding the link between oral health and systemic conditions, such as cardiovascular disease and diabetes is driving proactive care seeking behavior. The market also faces significant disparities in access to care, particularly among rural and low income populations. Insurance coverage limitations often dictate treatment choices, influencing the adoption of advanced procedures.

MAREKT DRIVERS

Aging Population and Increased Prevalence of Oral Diseases

The aging population and the corresponding increase in the prevalence of oral diseases is greatly influencing the growth of the United States dental market.As life expectancy increases, older adults retain their natural teeth for longer periods by necessitating complex restorative and maintenance care. According to the US Census Bureau, the number of individuals aged 65 and older is projected to reach 95 million by 2060 by creating a expanding base of patients requiring specialized geriatric dental services. The older adults are disproportionately affected by root caries, periodontal disease, and tooth loss, which drives demand for implants, dentures, and periodontal therapy. The correlation between oral health and systemic conditions, such as diabetes and heart disease that further motivates this demographic to seek regular dental care to manage overall health. Medicare coverage limitations for dental services often result in higher out of pocket spending, yet the critical nature of these treatments ensures consistent demand. The complexity of treating older patients requires advanced diagnostic tools and skilled specialists, fostering growth in specialized segments. Additionally, the desire for aesthetic improvement among seniors contributes to the uptake of cosmetic procedures such as veneers and whitening.

Rising Awareness of Oral Systemic Health Connections

The rising awareness of the connections between oral health and systemic well-being by encouraging preventive care and early intervention is fuelling the growth of the United States dental market. Consumers are increasingly informed about the links between periodontal disease and conditions such as diabetes, respiratory infections, and adverse pregnancy outcomes. The gum disease may contribute to the risk of heart disease, prompting healthcare providers to emphasize oral hygiene as part of holistic health management. As per the Surgeon General’s Report on Oral Health, public health initiatives have successfully promoted the importance of regular dental visits for maintaining overall health, leading to increased utilization of preventive services. Educational campaigns by dental associations and healthcare organizations reinforce the message that oral health is integral to general wellness. This shift in perception encourages individuals to view dental care as a necessity rather than a luxury, driving routine check ups and cleanings. Employers and insurance providers are also recognizing the cost benefits of preventive care, leading to improved coverage options for diagnostic and preventive procedures. The integration of dental health into primary care settings further facilitates early detection and treatment.

MARKET RESTRAINTS

High Cost of Care and Limited Insurance Coverage

The high cost of dental care and limited insurance coverage by restricting access for a significant portion of the population is restricting the growth of the United States dental care. Dental services are often expensive, and many procedures are considered elective or cosmetic, excluding them from standard insurance plans. According to the Kaiser Family Foundation, approximately 74 million adults in the United States lack dental insurance, forcing them to pay out of pocket for necessary treatments. The high deductibles and annual coverage limits often cap benefits at levels insufficient for major restorative work, discouraging patients from seeking comprehensive care. The lack of universal dental coverage means that low-income individuals frequently delay or forego treatment until emergencies arise by leading to more complex and costly interventions later. This financial barrier disproportionately affects vulnerable populations, including children in low-income families and elderly individuals on fixed incomes. The uncertainty of reimbursement rates also influences provider decisions, potentially limiting the availability of certain services in underserved areas. Without broader insurance reform or affordable financing options, a substantial segment of the population remains unable to access routine dental care.

Workforce Shortages and Geographic Maldistribution

The workforce shortages and the geographic maldistribution of dental professionals by limiting access to care in rural and urban areas is declining the growth of the United States dental market. Many regions face critical shortages of dentists and hygienists, exacerbating access disparities. According to the Health Resources and Services Administration, over 60 million Americans live in designated Dental Health Professional Shortage Areas, where residents struggle to find available providers. The distribution of dental professionals is skewed toward affluent urban centers by leaving rural communities with inadequate coverage. The high cost of dental education and student loan debt discourages new graduates from practicing in low income or remote areas, perpetuating the imbalance. Additionally, an aging workforce of dentists is retiring faster than new practitioners can replace them in certain regions, further straining capacity. The shortage of dental hygienists and assistants also impacts practice efficiency, limiting the number of patients that can be seen daily. These workforce challenges result in long wait times and reduced availability of appointments, deterring patients from seeking care.

MARKET OPPORTUNITIES

Integration of Digital Dentistry and Teledentistry

The integration of digital dentistry and teledentistry by enhancing efficiency, accessibility, and patient engagement is certainly ascribed to create new opportunities for the growth of the United States dental market. Digital technologies, such as intraoral scanners, 3D printing, and computer aided design software streamline clinical workflows and improve treatment precision. According to the American Dental Association, the adoption of digital impressions has grown rapidly, reducing chair time and improving patient comfort compared to traditional methods. Teledentistry allows for remote consultations, triage, and monitoring, extending care to underserved areas and reducing unnecessary office visits. This virtual care model is particularly valuable for follow up appointments and minor inquiries, improving practice efficiency and patient satisfaction. The use of artificial intelligence in diagnostic imaging enhances early detection of cavities and oral cancers, leading to better outcomes. Dental practices that adopt these technologies can differentiate themselves by offering superior convenience and quality. Reimbursement policies for teledentistry are evolving, creating new revenue streams for providers.

Expansion of Cosmetic and Aesthetic Dental Services

The expansion of cosmetic and aesthetic dental services by catering to the growing consumer demand for enhanced appearance and confidence is additionally to expand the growth of the United States dental market in coming years. Social media influence and cultural emphasis on physical appearance have driven increased interest in procedures, such as teeth whitening, veneers, and clear aligners. A significant majority of adults believe that an attractive smile is an important social asset, motivating investment in aesthetic improvements. The use of clear aligners has surged among both teenagers and adults, driven by their discreet appearance and convenience. The development of minimally invasive cosmetic techniques allows for quicker recovery times and lower costs, making these procedures accessible to a broader audience. Dental practices are marketing cosmetic services as lifestyle enhancements by appealing to younger demographics and professionals. The rise of direct to consumer orthodontic models has also expanded market reach, although professional oversight remains crucial for complex cases. Innovations in materials and bonding technologies improve the durability and natural appearance of restorations.

MARKET CHALLENGES

Regulatory Complexity and Compliance Burdens

The regulatory complexity and compliance burdens by increasing operational costs and administrative workload for providers is to be a challenge for the growth of the United States dental market. Dental practices must adhere to strict regulations regarding infection control, patient privacy, and radiation safety, which require continuous training and monitoring. The compliance with bloodborne pathogens standards and hazardous waste disposal rules demands significant resources and documentation. The adherence to Health Insurance Portability and Accountability Act regulations for protecting patient data involves robust cybersecurity measures and staff training. The varying state level licensing requirements and scope of practice laws for dental hygienists and assistants create inconsistencies that complicate multi state operations for corporate groups. Changes in reimbursement policies from insurance providers and government programs add further uncertainty to revenue planning. Non-compliance can result in severe penalties, legal liabilities, and reputational damage. Small independent practices often struggle to keep pace with evolving regulatory demands due to limited administrative support. The burden of maintaining compliance diverts attention from patient care and business growth.

Supply Chain Volatility and Material Costs

The supply chain volatility and fluctuating material costs by impacting practice profitability and treatment availability is another factor to impede the growth of the United States dental market. Dental practices rely on a steady supply of consumables, instruments, and equipment, many of which are sourced globally. According to the Bureau of Labor Statistics, inflationary pressures have increased the cost of dental supplies, including personal protective equipment, composites, and implants. As per the American Dental Association, disruptions in global supply chains have led to shortages of critical items, forcing practices to delay procedures or seek alternative suppliers at higher prices. Price volatility makes budgeting difficult for independent practices operating on thin margins. The transition to digital dentistry requires significant upfront investment in equipment and software, which is exacerbated by rising technology costs. Practices must balance the need for high quality materials with cost containment strategies, often passing expenses onto patients. This economic pressure can deter patients from pursuing recommended treatments, affecting case acceptance rates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.35% |

| Segments Covered | By Specialty, Financing Source, Practice Type, Zone, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Dentsply Sirona, Align Technology, Inc., SHOFU INC., VATECH, Anson Dental Supply, 3M, Zimmer Biomet, Institut Straumann AG, Ultradent Products Inc., and Bien-Air Medical Technologies |

SEGMENTAL ANALYSIS

By Specialty Insights

The general dentistry segment is expected to hold a dominant share of the United States dental market in 2025 with the primary entry point for oral healthcare and accounts for the highest volume of patient visits. Most individuals seek routine check-ups cleanings and basic restorative procedures, such as fillings and crowns from general practitioners before being referred to specialists. According to the American Dental Association, general dentists constitute approximately 80% of the active dentist workforce in the United States, ensuring widespread accessibility and availability of services. The broad scope of practice allows general dentists to address a wide array of common oral health issues, making them indispensable to the healthcare system. Insurance plans typically cover preventive and basic restorative services provided by general dentists at higher reimbursement rates than specialized procedures by encouraging patients to utilize these services regularly. The foundational role of general dentistry in maintaining overall oral health ensures that it remains the largest segment by revenue and patient volume. The integration of general practices with digital diagnostic tools further enhances their efficiency and capacity to handle high patient loads.

The orthodontics segment is esteemed to grow at a fastest CAGR of 7.9% from 2026 to 2034 with the surging demand for aesthetic aligners and increasing treatment adoption among adults. Traditional metal braces are being replaced by clear aligner systems that offer a discreet and convenient alternative for correcting misaligned teeth. The number of adult patients seeking orthodontic treatment has increased significantly in recent years, as social stigma decreases and aesthetic preferences evolve. The convenience of remote monitoring and fewer office visits appeals to busy professionals and teenagers alike. Social media influence and the emphasis on smile aesthetics have further motivated individuals to invest in orthodontic correction. The development of accelerated orthodontic techniques reduces treatment time making it more attractive to patients. Insurance coverage for orthodontics is also expanding in some plans recognizing the functional benefits of proper alignment.

By Financing Source Insights

The private health insurance segment was the largest by holding a significant share of the US dental market in 2025 due to the prevalence of employer sponsored dental benefits. According to the data, approximately 54% of Americans under age 65 have dental insurance through their employer or union by making it the most common source of coverage. The private insurance accounts for the largest share of dental expenditures, facilitating access to preventive and restorative services for insured individuals. Employer sponsored plans often negotiate favorable rates with providers, encouraging employees to utilize in network services. The structure of these plans typically includes preventive care with little to no cost sharing, promoting regular dental visits. The stability of employer based coverage ensures consistent revenue streams for dental practices. The administrative infrastructure supporting private insurance is well established, simplifying billing and reimbursement processes for providers. The reliance on employment based benefits creates a strong linkage between labor market trends and dental care utilization.

The out of pocket and others segment is likely to witness a fastest CAGR of 7.2% during the forecast period with the rise of high deductible health plans and gaps in insurance coverage. Many employers are shifting toward high-deductible plans to control costs by leaving employees responsible for a larger portion of their dental expenses until deductibles are met. Millions of Americans lack dental insurance entirely by forcing them to pay for all services out of pocket. The limited coverage for adult dental care under Medicare and varying state Medicaid programs further expands the uninsured population. Consumers are increasingly using health savings accounts and flexible spending accounts to manage these costs, but direct out of pocket payments remain significant. The transparency of pricing offered by some dental providers appeals to cash paying patients who seek to avoid insurance complexities.

By Practice Type Insights

The solo practices segment was the largest by holding 43.2% of the US dental market share in 2025 due to the historical prevalence of independent ownership and the desire for professional autonomy among dentists. The majority of dental offices in the United States are owned and operated by individual practitioners, who maintain full control over clinical and business decisions. According to the American Dental Association, approximately 75% of dentists operate in solo or small group practices, reflecting the traditional structure of the profession. Solo practitioners are the ability to customize their practice culture patient relationships and treatment approaches without corporate oversight. The lower overhead costs associated with smaller operations can enhance profitability for efficient practitioners. The established reputation of long standing solo practices provides a stable patient base. The flexibility to adopt new technologies and services at their own pace appeals to many dentists.

The Dental Support Organizations (DSOs) segment is likely to grow at a fastest CAGR of 11.4% during the forecast period with the advantages of economies of scale and operational efficiency. DSOs provide non clinical support services, such as billing marketing and procurement allowing dentists to focus on patient care, while reducing administrative burdens. The number of practices affiliated with DSOs has grown significantly as independent owners seek to mitigate rising operational costs. The DSOs leverage bulk purchasing power to negotiate lower prices for supplies and equipment improving profit margins. Centralized management systems streamline scheduling insurance verification and compliance reducing overhead expenses. The ability to share resources such as specialized equipment and staff across multiple locations enhances productivity. This operational efficiency attracts dentists who seek financial stability and work life balance. The scalable model of DSOs facilitates rapid expansion into new markets.

COMPETITIVE LANDSCAPE

The competition in the United States dental market is intense and characterized by a highly fragmented landscape of independent solo practices alongside rapidly growing Dental Support Organizations. Major players compete on the basis of service quality patient experience technological adoption and pricing transparency to attract and retain patients. The market sees significant consolidation as DSOs acquire independent practices to leverage economies of scale and standardized operations. Independent dentists differentiate themselves through personalized care community involvement and specialized services that large chains may not offer. Technological advancement drives competition with practices investing in digital workflows and teledentistry to improve efficiency. Insurance networks play a crucial role in patient acquisition influencing which providers consumers choose based on coverage. New entrants including direct to consumer aligner companies disrupt traditional orthodontic models by offering lower cost alternatives. Regulatory compliance and staffing challenges also impact competitive dynamics requiring robust operational management. The rise of consumerism in healthcare empowers patients to compare providers and prices online.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. dental market include

- Dentsply Sirona (U.S.)

- Align Technology, Inc. (U.S.)

- SHOFU INC. (Japan)

- VATECH (South Korea)

- Anson Dental Supply (U.S.)

- 3M (U.S.)

- Zimmer Biomet (U.S.)

- Institut Straumann AG (Switzerland)

- Ultradent Products Inc. (U.S.)

- Bien-Air Medical Technologies (Switzerland)

Top Players in the Market

- Align Technology Inc is a global leader in digital dentistry and orthodontics best known for its Invisalign clear aligner system. The company has revolutionized orthodontic treatment by offering a discreet and removable alternative to traditional braces. Align leverages proprietary three dimensional imaging and software platforms to create customized treatment plans for patients worldwide. Recent actions include expanding its manufacturing capabilities and enhancing its digital ecosystem through strategic acquisitions of intraoral scanner companies. The company focuses on increasing provider adoption by offering comprehensive training and support programs. These initiatives strengthen its market position by creating a loyal network of clinicians and improving patient outcomes. Align continues to invest in research and development to expand its product portfolio beyond orthodontics into restorative solutions.

- Dentsply Sirona Inc is the worlds largest manufacturer of professional dental products and technologies with a broad portfolio of equipment and consumables. The company provides essential tools for dentists and laboratories including imaging systems CAD CAM units and endodontic instruments. Dentsply Sirona operates globally serving millions of customers with innovative solutions that enhance clinical efficiency. Recent actions involve streamlining its operational structure and investing in digital workflow integration to improve customer experience. The company focuses on sustainability initiatives and product innovation to meet evolving market demands. These efforts strengthen its market position by ensuring reliable supply chains and high quality standards. Dentsply Sirona collaborates with dental professionals to develop solutions that address specific clinical challenges.

- Envista Holdings Corporation is a leading global dental technology company that owns prominent brands such as KaVo Kerr Nobel Biocare and Ormco. The company specializes in equipment instruments and implant solutions that support various dental specialties. Envista serves dental professionals worldwide with a focus on precision engineering and clinical excellence. Recent actions include optimizing its portfolio through strategic divestitures and acquisitions to focus on high growth segments. The company invests heavily in digital dentistry and implant technologies to drive innovation. These strategies strengthen its market position by offering comprehensive solutions for complex dental procedures. Envista prioritizes customer engagement and education to build strong relationships with practitioners.

Top Strategies Used by Key Market Participants

Key players in the United States dental market employ several major strategies to maintain competitiveness and drive growth. Consolidation through mergers and acquisitions is central to these efforts allowing Dental Support Organizations to expand their networks and achieve economies of scale. Investment in digital technologies such as intraoral scanners and practice management software enhances operational efficiency and patient experience. Strategic partnerships with insurance providers and financing companies improve access to care for patients and stabilize revenue streams. Product innovation focuses on minimally invasive techniques and aesthetic solutions to meet consumer demand for cosmetic dentistry. Marketing efforts emphasize brand recognition and patient education to drive appointment bookings. Expansion into underserved rural and urban areas helps capture new market segments. These combined strategies enable participants to adapt to regulatory changes and sustain long term profitability in a fragmented and evolving industry landscape.

MARKET SEGMENTATION

This research report on the U.S. dental market is segmented and sub-segmented into the following categories.

By Specialty

- General Dentistry

- Oral and Maxillofacial Surgery

- Endodontics

- Orthodontics

- Others

By Financing Source

- Private Health Insurance

- Public Health Insurance

- Out of pocket and Others

By Practice Type

- Solo Practices

- DSO and Group Practices

- Others

By Zone

- Northeast

- Midwest

- South

- West

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is the current size of the U.S. dental market?

The market is experiencing steady growth driven by increasing demand for dental procedures, rising awareness of oral health, and advancements in dental technologies.

2.What factors are driving growth in the U.S. dental market?

Key drivers include an aging population, increasing prevalence of dental disorders, growing cosmetic dentistry demand, and technological advancements.

3.What are the most common dental procedures in the U.S.?

Common procedures include preventive care, restorative treatments, orthodontics, endodontics, and cosmetic dentistry.

4.Who are the major players in the U.S. dental market?

Leading companies include Dentsply Sirona, Align Technology, Inc., 3M, Zimmer Biomet, and Institut Straumann AG.

5.What role does insurance play in the U.S. dental market?

Private and public health insurance significantly influence patient access to dental services and treatment affordability.

6.How is technology transforming the dental industry?

Technologies such as digital imaging, CAD and CAM systems, 3D printing, and teledentistry are improving treatment precision and efficiency.

7.What is the impact of cosmetic dentistry trends?

Increasing demand for aesthetic procedures such as teeth whitening, veneers, and aligners is boosting market growth.

8.Which segment dominates the U.S. dental market?

General dentistry holds a major share due to high demand for routine checkups and preventive care.

9.What challenges does the U.S. dental market face?

Challenges include high treatment costs, limited insurance coverage, workforce shortages, and regulatory complexities.

10.What are the emerging trends in the U.S. dental market?

Key trends include digital dentistry adoption, minimally invasive procedures, and growing use of clear aligners.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com