U.S. Consulting Market Size, Share, Trends & Growth Forecast Report - Segmented By Service, Client Organization Size, End-User and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Consulting Market Report Summary

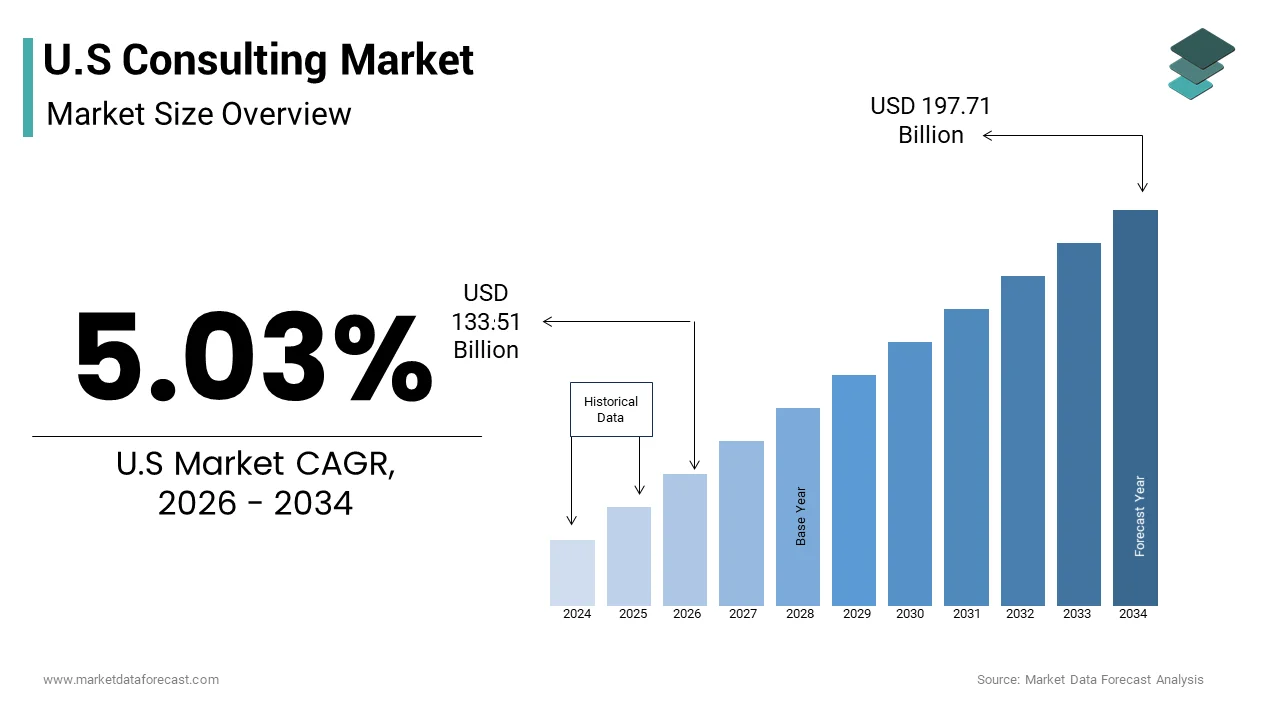

The U.S. consulting market was valued at USD 127.12 billion in 2025, is estimated to reach USD 133.51 billion in 2026, and is projected to reach USD 197.71 billion by 2034, growing at a CAGR of 5.03% during the forecast period from 2026 to 2034. The growth of the U.S. consulting market is driven by the increasing need for digital transformation, rising demand for business process optimization, and growing investments in enterprise modernization across industries. Organizations are increasingly partnering with consulting firms to strengthen operational efficiency, improve customer experience, navigate regulatory complexities, and accelerate technology adoption. The rapid integration of artificial intelligence, cloud computing, cybersecurity solutions, and data analytics into business operations is further fueling demand for specialized consulting services. Additionally, expanding mergers and acquisitions, sustainability initiatives, and evolving workforce strategies continue to create long-term growth opportunities for consulting providers across the United States.

Key Market Trends

- Growing adoption of AI, generative AI, and advanced analytics consulting to support enterprise-wide digital transformation initiatives.

- Increasing demand for cybersecurity, cloud migration, and IT modernization services as organizations strengthen digital resilience.

- Rising focus on environmental, social, and governance (ESG) consulting to meet evolving regulatory and sustainability requirements.

- Expansion of strategy and operational consulting services to improve cost efficiency, supply chain resilience, and organizational agility.

- Increasing use of industry-specific consulting solutions tailored to sectors such as financial services, healthcare, manufacturing, and technology.

Segmental Insights

Based on service, the operations consulting segment accounted for the largest share of the U.S. consulting market in 2025. The segment's dominance is attributed to growing demand from enterprises seeking to optimize business processes, improve operational efficiency, reduce costs, and strengthen supply chain performance amid an increasingly competitive business environment.

Based on client organization size, the large enterprises segment held the major share of the U.S. consulting market in 2025. Large organizations continue to lead demand due to their extensive digital transformation initiatives, complex business structures, global operations, and continuous investments in strategic consulting, technology implementation, and organizational change management.

Based on end-user industry, the BFSI (Banking, Financial Services, and Insurance) segment led the U.S. consulting market in 2025. The segment's leadership is driven by ongoing regulatory compliance requirements, digital banking transformation, cybersecurity investments, risk management initiatives, and the adoption of advanced financial technologies to enhance operational performance and customer engagement.

Regional Insights

The United States continues to serve as one of the world's largest and most influential consulting markets, supported by its mature corporate ecosystem, rapid technological innovation, and strong presence of multinational enterprises. The country is expected to remain the primary driver of global consulting standards and revenue over the coming years, fueled by sustained investments in digital transformation, artificial intelligence, cloud infrastructure, business strategy, and operational excellence. Strong demand from industries including BFSI, healthcare, manufacturing, retail, and technology continues to reinforce market expansion, while increasing adoption of specialized consulting services positions the U.S. as a global hub for consulting innovation and expertise.

Competitive Landscape

The U.S. consulting market is highly competitive, with global consulting firms and specialized advisory companies competing through innovation, industry expertise, and comprehensive service portfolios. Leading firms are expanding their capabilities in artificial intelligence, digital transformation, cybersecurity, cloud consulting, sustainability advisory, and data analytics to address evolving client requirements. Strategic mergers and acquisitions, partnerships with technology providers, investments in proprietary digital platforms, and the expansion of sector-specific consulting practices remain key growth strategies across the market. Companies are also strengthening their global delivery networks, enhancing customer-centric consulting models, and investing in highly skilled talent to deliver integrated business solutions. As organizations accelerate modernization and operational transformation, consulting firms continue to differentiate themselves through specialized expertise, technology-enabled services, and outcome-driven advisory solutions.

Prominent players in the U.S. consulting market include Deloitte, PwC, Accenture, McKinsey & Company, EY, KPMG, Boston Consulting Group, Bain & Company, Booz Allen Hamilton, Kearney, IBM Consulting, Cognizant Consulting, Grant Thornton, Oliver Wyman, Protiviti, Alvarez & Marsal, L.E.K. Consulting, Huron Consulting Group, Guidehouse, Slalom, West Monroe Partners, and Publicis Sapient.

U.S. Consulting Market Size

The U.S consulting market size was valued at USD 127.12 billion in 2025 and is anticipated to reach USD 133.51 billion in 2026 to reach USD 197.71 billion by 2034, growing at a CAGR of 5.03% during the forecast period from 2026 to 2034.

Consulting represents a sophisticated ecosystem of professional services designed to assist organizations in improving performance through the analysis of existing organizational problems and the development of plans for improvement. This sector encompasses a broad spectrum of advisory services including strategy, operations, technology, human resources, and risk management. The industry serves as a critical bridge between complex business challenges and actionable solutions, leveraging specialized expertise that internal teams often lack. As per data from the Bureau of Labor Statistics, employment in management analysis roles is projected to grow 9% from 2024 to 2034, which is much faster than the average for all occupations. The modern consulting landscape is increasingly defined by digital transformation initiatives, where firms help clients navigate the integration of artificial intelligence, cloud computing, and data analytics into their core operations. According to the National Science Foundation, business expenditure on research and development performed in the United States totaled $937 billion in 2023, and the estimate for 2024 indicates a further increase to $993 billion. The shift towards hybrid work models has also reshaped service delivery, with consultants utilizing virtual collaboration tools to engage with clients across geographies. This evolution underscores the adaptability of the consulting profession in responding to macroeconomic shifts and technological advancements. The sector is not merely a support function but a strategic partner in driving competitive advantage, operational efficiency, and sustainable growth for enterprises across diverse industries in the U.S.

MARKET DRIVERS

Accelerating Digital Transformation and Technology Integration Needs

The urgent need for organizations to undergo comprehensive digital transformation to remain competitive in an increasingly technology driven economy is one of the major factors contributing to the U.S. consulting market growth. Companies across sectors are seeking external expertise to implement advanced technologies such as artificial intelligence, machine learning, and block chain, which require specialized knowledge that is often scarce within traditional corporate structures. As per a Federal Reserve report from April 2026, about 18% of U.S. firms had adopted AI by the end of 2025, and over 20% of firms expect to use AI in the first half of 2026. Consultants play a pivotal role in assessing current technological infrastructure, identifying gaps, and designing roadmaps for seamless integration of new systems. This process involves not only technical implementation but also change management to ensure employee adoption and operational continuity. According to the Census Bureau, 94% of companies worldwide use cloud computing in their operations, and 85% of organizations are projected to embrace a cloud-first principle by 2025. The complexity of these transitions necessitates professional guidance to mitigate risks and optimize return on investment. Furthermore, the rapid pace of technological innovation means that best practices evolves constantly, requiring ongoing advisory support. Organizations rely on consulting firms to stay abreast of emerging trends and leverage them for strategic advantage. This continuous need for technological upgradation and strategic alignment drives sustained demand for consulting services across the corporate landscape.

Increasing Regulatory Complexity and Compliance Requirements

The rising complexity of regulatory environments that compels organizations to seek expert guidance to ensure compliance and mitigate legal risks is further boosting the U.S. market expansion. Businesses operate under a myriad of federal, state, and local regulations covering areas such as data privacy, environmental protection, financial reporting, and labor standards. According to the Federal Register, the number of new regulations published annually remains high, creating a dynamic and challenging compliance landscape for corporations. Consulting firms provide specialized expertise in navigating these regulatory frameworks, helping companies develop robust compliance programs and avoid costly penalties. The introduction of laws such as the California Consumer Privacy Act and various healthcare regulations has increased the demand for legal and operational consulting services. Data from the Society for Human Resource Management indicates that a majority of organizations face challenges in keeping up with changing employment laws, necessitating external support for policy development and training. Additionally, global expansion efforts expose U.S. companies to international regulations, further amplifying the need for cross border compliance expertise. Consultants assist in conducting risk assessments, implementing internal controls, and training staff on regulatory requirements. This proactive approach to compliance not only protects organizations from legal repercussions but also enhances their reputation and operational integrity. The constant evolution of regulatory standards ensures a steady demand for consulting services in this critical domain.

MARKET RESTRAINTS

Talent Shortages and High Costs of Specialized Expertise

The persistent shortage of highly skilled talent coupled with the escalating costs associated with acquiring and retaining specialized expertise is also hindering the U.S. consulting market growth. The demand for consultants with advanced skills in areas such as data science, cybersecurity, and strategic management often outstrips the available supply of qualified professionals. As per the Bureau of Labor Statistics, the median annual wage for management analysts was $101,190 in May 2024, reflecting the high costs of specialized talent. This scarcity drives up salary expectations and compensation packages, increasing operational costs for consulting firms. Furthermore, the competitive nature of the industry leads to high turnover rates as professionals seek better opportunities or start their own ventures. According to the Society for Human Resource Management, replacement costs for an employee can equal six to nine months of that employee’s salary. The inability to scale teams quickly in response to client demands can result in project delays and reduced service quality. Additionally, the rise of remote work has expanded the talent pool globally but also intensified competition for top tier candidates. Firms must invest heavily in training and development to bridge skill gaps, which further strains resources. These factors collectively constrain the growth potential and profitability of consulting organizations in the U.S.

Client Budget Constraints and Economic Uncertainty

The fluctuating economic conditions that lead to budget constraints and reduced spending on external advisory services are further hampering the consulting market growth in the U.S. During periods of economic uncertainty or recession, corporations tend to tighten their belts and prioritize essential operational expenses over discretionary consulting engagements. According to the Conference Board, CEO confidence indices often decline during volatile economic periods, leading to cautious spending behavior and deferred strategic initiatives. Consulting services are frequently viewed as non essential costs that can be cut to preserve cash flow and maintain profitability. Data from the Federal Reserve indicates that business investment in services can contract during economic downturns, impacting the revenue streams of consulting firms. Clients may also choose to insource certain functions or rely on internal teams to reduce reliance on expensive external providers. The pressure to demonstrate immediate and tangible return on investment from consulting projects has intensified, making it harder for firms to secure long term contracts. Additionally, the rise of alternative service providers such as boutique firms and independent contractors offers lower cost options that compete with traditional large scale consultancies. This price sensitivity and demand for cost effective solutions force established firms to adjust their pricing models and value propositions. Economic volatility thus poses a significant challenge to the stability and growth of the consulting sector.

MARKET OPPORTUNITIES

Expansion into Emerging Niche Specializations and Industries

The expanding services into emerging niche specializations and underserved industries are a prominent opportunity for the U.S. consulting market. Areas such as sustainability, environmental, social, and governance (ESG) criteria, and cybersecurity present lucrative avenues for consultants to offer tailored solutions. According to the Environmental Protection Agency, there is increasing regulatory and consumer pressure on companies to adopt sustainable practices, creating a need for strategic guidance in this domain. Consulting firms can develop specialized practices focused on helping organizations measure and improve their ESG performance, thereby attracting clients who prioritize corporate responsibility. Additionally, the healthcare and life sciences sectors are undergoing rapid transformation due to technological advancements and regulatory changes, offering opportunities for consultants with domain specific knowledge. Data from the National Institutes of Health highlights the substantial investment in biomedical research and development, which requires strategic planning and commercialization support. The rise of the gig economy and remote work models also creates demand for HR consulting services focused on workforce management and organizational culture. By diversifying their service offerings and targeting high growth niches, consulting firms can reduce dependence on traditional markets and capture new revenue streams. This strategic expansion allows firms to differentiate themselves and build deeper relationships with clients facing unique and complex challenges.

Leveraging Artificial Intelligence and Advanced Analytics

The integration of artificial intelligence and advanced analytics into consulting methodologies is a substantial opportunity for firms to enhance service delivery and create new value propositions. AI powered tools can analyze vast amounts of data to uncover insights, predict trends, and automate routine tasks, enabling consultants to provide more accurate and timely recommendations. According to the McKinsey Global Institute, the adoption of AI technologies has the potential to deliver significant economic benefits by improving productivity and decision making processes. Consulting firms can develop proprietary algorithms and platforms that offer clients real time monitoring and predictive capabilities, transforming traditional advisory services into continuous support models. This shift towards data driven consulting allows for more personalized and impactful solutions that address specific client needs. According to the National Science Foundation, business funding for R&D increased by $17 billion between 2023 and 2024, reflecting the recognition of the strategic importance of innovation. By leveraging these technologies, firms can reduce project timelines, lower costs, and improve the scalability of their services. Furthermore, the ability to demonstrate measurable outcomes through data analytics enhances client trust and retention. The development of AI enabled consulting products also opens up new revenue streams through software licensing and subscription models. Embracing technological innovation positions consulting firms at the forefront of industry evolution and drives long term growth.

MARKET CHALLENGES

Intensifying Competition from Boutique Firms and Independent Consultants

The intensifying competition from boutique firms and independent consultants who offer specialized services at lower costs is a significant challenge to the growth of the U.S. consulting market. These smaller entities often possess deep expertise in specific niches and can provide more agile and personalized solutions compared to large generalist firms. According to the Small Business Administration, small businesses accounted for 99.9% of all U.S. businesses in 2024, contributing significantly to the fragmentation of the professional services market. Clients are increasingly willing to engage boutique firms for targeted projects where specialized knowledge is more valuable than broad strategic oversight. This trend erodes the market share of traditional large scale consultancies and pressures them to justify their higher fees. Data from industry surveys indicates that many corporations are adopting a multi-vendor strategy, engaging multiple smaller firms rather than relying on a single large partner. The flexibility and cost effectiveness of independent consultants also appeal to businesses looking to minimize overhead costs. Large firms must therefore continuously innovate and demonstrate superior value to retain clients. The proliferation of online platforms that connect freelancers with businesses further facilitates this shift towards decentralized consulting services. This competitive landscape requires established players to adapt their business models and enhance their differentiation strategies to maintain relevance and profitability.

Data Security Risks and Confidentiality Concerns

The increasing reliance on digital tools and data analytics in consulting exposes the U.S. market to significant data security risks and confidentiality concerns, which is further challenging the expansion of the U.S. consulting market. Consulting firms handle sensitive client information, including financial data, strategic plans, and proprietary technologies, making them attractive targets for cyberattacks. According to the Federal Trade Commission, data breaches in the professional services sector have risen in frequency and severity, posing a serious threat to client trust and brand reputation. A single security incident can result in substantial financial losses, legal liabilities, and long term damage to client relationships. Ensuring robust cybersecurity measures requires continuous investment in advanced encryption technologies, monitoring systems, and employee training, which increases operational costs. Data from the National Institute of Standards and Technology highlights the growing complexity of cyber threats and the need for comprehensive security frameworks. Clients are becoming more stringent in their vendor selection processes, demanding rigorous security certifications and compliance with data protection standards. Failure to meet these expectations can result in lost business opportunities and contractual penalties. Additionally, the use of third party software and cloud platforms introduces additional vulnerabilities that must be managed effectively. Navigating these security challenges while maintaining operational efficiency is a critical issue for consulting firms. Addressing these risks is essential for sustaining client confidence and ensuring the long term viability of the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.03% |

| Segments Covered | By Service, Client Organization Size, End-User, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Deloitte, PwC, Accenture, McKinsey and Company, EY, KPMG, Boston Consulting Group, Bain and Company, Booz Allen Hamilton, Kearney, IBM Consulting, Cognizant Consulting, Grant Thornton, Oliver Wyman, Protiviti, Alvarez and Marsal, L.E.K. Consulting, Huron Consulting Group, Guidehouse, Slalom, West Monroe Partners, Publicis Sapient |

SEGMENTAL ANALYSIS

By Service Insights

The operations consulting segment accounted for the highest share of the U.S. consulting market in 2025. The dominance of operations consulting segment in the U.S. market is attributed to the constant pressure to improve efficiency, reduce costs, and streamline complex supply chains. In an era of tight margins and economic uncertainty, businesses prioritize operational excellence to maintain profitability and competitive advantage. According to the Bureau of Labor Statistics, productivity growth in the nonfarm business sector has been modest, prompting companies to seek external expertise to identify inefficiencies and implement process improvements. Operations consultants specialize in analyzing workflows, optimizing resource allocation, and integrating lean management principles that directly impact the bottom line. Data from the Institute for Supply Management indicates that supply chain disruptions continue to pose significant challenges for U.S. manufacturers and retailers, driving demand for strategic operational guidance. The ability of operations consulting to deliver tangible and measurable results, such as reduced cycle times and lower inventory costs, makes it a preferred service type for executive leadership. Furthermore, the complexity of global operations requires specialized knowledge in logistics, procurement, and production planning, which internal teams often lack. This segment dominates because it addresses the fundamental need for sustainable operational performance in a volatile market environment. The focus on continuous improvement and risk mitigation ensures that operations consulting remains a cornerstone of corporate strategy across various industries in the U.S.

However, the technology consulting segment is expected to showcase a promising CAGR in the U.S. consulting market during the forecast period owing to the rapid adoption of cloud computing and the urgent need for digital infrastructure modernization. Organizations are migrating legacy systems to cloud platforms to enhance scalability, flexibility, and security, which requires specialized technical expertise. According to the Synergy Research Group, spending on cloud services in the U.S. continues to surge as businesses accelerate their digital transformation journeys. Technology consultants assist in selecting appropriate cloud providers, designing migration pathways, and ensuring data integrity during the transition. According to the Census Bureau, 59% of businesses reported that cloud-based technology was very important to their processes or methods. The complexity of multi cloud environments and hybrid architectures necessitates professional guidance to optimize performance and manage costs effectively. Furthermore, the rise of remote work has intensified the demand for secure and reliable digital collaboration tools, which technology consultants help implement. This segment is growing at a compound annual growth rate that outpaces other service types due to the critical nature of digital infrastructure in modern business operations. The continuous evolution of technology standards and the emergence of new platforms ensure a steady demand for advisory services in this dynamic domain.

By Client Organization Size Insights

The large enterprises segment accounted for the major share of the U.S. consulting market in 2025. The growth of the large enterprises segment in the U.S. market is attributed to their substantial budgets for strategic initiatives and complex organizational transformations. These organizations operate on a global scale with intricate structures that require specialized expertise to navigate regulatory compliance, market expansion, and technological integration. According to the Fortune 500 list, the combined revenue of large U.S. corporations represents a significant portion of the national economy, enabling them to invest heavily in external advisory services. Large firms often engage consultants for long term strategic projects such as mergers and acquisitions, digital transformation, and sustainability initiatives, which require extensive resources and multidisciplinary teams. Data from the Securities and Exchange Commission filings indicates that large publicly traded companies frequently disclose significant expenditures on professional services, reflecting their reliance on external expertise. The complexity of managing diverse business units across different geographies necessitates standardized processes and best practices that consultants help establish. Furthermore, large enterprises face higher scrutiny from shareholders and regulators, requiring robust risk management and governance frameworks. Consultants provide the objective analysis and strategic guidance needed to meet these expectations. The ability of large firms to sustain long term engagements and invest in high value projects ensures their dominance in the consulting market. This segment drives the majority of revenue for consulting firms due to the scale and scope of services required.

On the other end, the small and medium enterprises (SMEs) segment is estimated to record a prominent CAGR in the U.S. market during the forecast period due to the increasing accessibility of scalable and modular consulting solutions. Traditionally, SMEs lacked the resources to engage large consulting firms, but the emergence of boutique firms and digital platforms has democratized access to professional advice. According to the Small Business Administration, small businesses accounted for 45.9% of U.S. employees and contributed a net increase of 2.6 million jobs between 2022 and 2023. Boutique firms offer targeted services such as marketing strategy, financial planning, and human resources management at affordable rates, making them attractive to smaller businesses. Data from the Federal Reserve indicates that SMEs are increasingly investing in professional services to improve competitiveness and drive growth. The modular nature of these services allows SMEs to engage consultants for specific projects without committing to long term contracts. This flexibility aligns with the agile nature of small businesses that need to adapt quickly to market changes. Furthermore, the rise of remote consulting has reduced geographical barriers, enabling SMEs in rural areas to access top tier expertise. This trend towards accessible and flexible consulting services is driving rapid growth in the SME segment.

By End-User Industry Insights

The BFSI segment led the market with the highest share of the U.S. consulting market in 2025. The dominance of BFSI segment in the U.S. market is attributed to the stringent regulatory compliance and risk management requirements. Financial institutions operate in a highly regulated environment where adherence to laws such as the Dodd Frank Act and anti money laundering regulations is mandatory. According to the Office of the Comptroller of the Currency, banks face significant penalties for non compliance, driving the need for expert guidance in regulatory affairs. Consulting firms provide specialized services in compliance auditing, risk assessment, and policy development, helping institutions navigate complex legal frameworks. Data from the Federal Deposit Insurance Corporation indicates that regulatory examinations and enforcement actions remain frequent, prompting banks to invest in robust compliance programs. The evolving nature of financial regulations requires continuous monitoring and adaptation, which consultants facilitate through ongoing advisory services. Furthermore, the increasing sophistication of financial crimes necessitates advanced detection systems and investigative capabilities. Consultants assist in implementing these technologies and training staff to identify and report suspicious activities. The critical importance of maintaining regulatory integrity and avoiding reputational damage ensures that BFSI institutions remain major consumers of consulting services. This segment drives significant revenue due to the high stakes and complexity of financial regulation.

However, the life sciences and healthcare segment is predicted to register a prominent CAGR in the U.S. market during the forecast period owing to the regulatory changes and the shift towards value based care models. Healthcare providers and pharmaceutical companies are navigating complex reforms aimed at improving patient outcomes and reducing costs. According to the Centers for Medicare and Medicaid Services, the transition to value based payment models requires significant operational adjustments and data analytics capabilities. Consulting firms assist organizations in redesigning care delivery processes, implementing electronic health records, and managing population health initiatives. Data from the Agency for Healthcare Research and Quality indicates that healthcare spending continues to rise, prompting stakeholders to seek efficiency improvements. Consultants provide expertise in regulatory compliance, clinical trial management, and market access strategies, which are critical for pharmaceutical companies. The introduction of new drugs and therapies requires rigorous testing and approval processes that benefit from strategic guidance. Furthermore, the aging population and increasing prevalence of chronic diseases drive demand for innovative healthcare solutions. Consulting services help organizations adapt to these demographic trends and develop sustainable care models. This dynamic environment and the need for strategic adaptation propel the rapid growth of the life sciences and healthcare segment.

U.S COUNTRY ANALYSIS

The U.S. is likely to continue its path as the primary driver of global consulting standards and revenue for the next few years, maintaining its position as the dominant and most mature market. The country serves as a hub for innovation and strategic thinking, attracting top talent and leading firms from around the world. According to the Bureau of Economic Analysis, the professional and business services sector contributes significantly to the U.S. GDP, reflecting the critical role of consulting in the national economy. The market status is characterized by a high degree of specialization and fragmentation, with numerous firms catering to diverse industry needs. The presence of major multinational corporations and government agencies creates a robust demand for strategic advisory services. According to the Bureau of Labor Statistics, management analysts held about 1.1 million jobs in 2024, with 34% of these roles concentrated in professional, scientific, and technical services. These hubs foster collaboration and knowledge exchange, which is driving continuous improvement in service quality. The U.S. market is also influenced by strong intellectual property protections and a favorable business environment that encourages investment in professional services. The maturity of the market requires firms to differentiate themselves through niche expertise and technological innovation. This leadership position ensures that the U.S. remains the primary driver of trends and standards in the global consulting industry.

COMPETITIVE LANDSCAPE

The competition in the U.S. consulting market is intense and characterized by the presence of global giants boutique firms and independent consultants vying for client attention. Major firms differentiate themselves through brand reputation extensive resources and comprehensive service offerings that span strategy operations and technology. Boutique firms compete by offering specialized expertise in niche areas such as digital marketing supply chain optimization or regulatory compliance often at lower costs. The rise of freelance platforms has further fragmented the market allowing clients to hire individual experts for specific projects. Price sensitivity and demand for measurable return on investment drive firms to demonstrate clear value propositions. Innovation in service delivery through artificial intelligence and automated tools is becoming a key differentiator. Client loyalty is increasingly based on the ability to deliver rapid results and adapt to changing business needs. Collaborative models where multiple firms work together on complex projects are gaining traction. This dynamic landscape requires continuous adaptation and strategic positioning to sustain growth and profitability in a saturated market.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S consulting market are

- Deloitte

- PwC

- Accenture

- McKinsey and Company

- EY

- KPMG

- Boston Consulting Group

- Bain and Company

- Booz Allen Hamilton

- Kearney

- IBM Consulting

- Cognizant Consulting

- Grant Thornton

- Oliver Wyman

- Protiviti

- Alvarez and Marsal

- L.E.K. Consulting

- Huron Consulting Group

- Guidehouse

- Slalom

- West Monroe Partners

- Publicis Sapient

Top Players In The Market

- McKinsey and Company maintains a strong presence across Europe by delivering high level strategic advice to governments and multinational corporations. The firm focuses on digital transformation sustainability and organizational restructuring to help clients navigate complex market dynamics. Recent actions include expanding its digital capabilities through the acquisition of specialized tech firms and establishing new innovation hubs in major European cities. McKinsey actively collaborates with public sector entities to address societal challenges such as climate change and healthcare efficiency. The company invests heavily in talent development and diversity initiatives to strengthen its workforce. By leveraging deep industry expertise and global insights McKinsey continues to influence corporate strategy and policy making throughout the region while reinforcing its reputation as a premier advisory partner for critical business decisions.

- Boston Consulting Group contributes significantly to the Europe market by offering innovative solutions in strategy technology and people organization. The firm emphasizes sustainable growth and digital acceleration helping clients adapt to rapid technological changes. Recent strategies involve launching dedicated centers for artificial intelligence and green energy transitions across key European markets. BCG has strengthened its partnerships with leading universities and research institutions to drive thought leadership and innovation. The company also focuses on enhancing client relationships through long term transformation programs that deliver measurable results. By integrating advanced analytics and human centric design BCG provides tailored services that address unique regional challenges. This approach enables the firm to maintain its competitive edge and support diverse industries in achieving their strategic objectives within the dynamic European landscape.

- Bain and Company plays a vital role in the Europe consulting market by focusing on private equity mergers and acquisitions and operational performance. The firm is known for its results oriented approach and deep collaboration with client teams to implement effective strategies. Recent actions include expanding its digital and analytics practices to help clients leverage data for competitive advantage. Bain has established specialized units focused on sustainability and customer experience to meet evolving market demands. The company actively engages in knowledge sharing through global conferences and publications that highlight best practices. By fostering a culture of excellence and innovation Bain supports organizations in navigating uncertainty and capturing growth opportunities. Its commitment to delivering tangible outcomes strengthens its position as a trusted advisor to leading businesses and investors across the European continent.

Top Strategies Used By Key Market Participants

- Key players in the U.S. consulting market primarily focus on digital transformation and artificial intelligence integration to enhance service delivery and client outcomes. Firms are investing heavily in proprietary technologies and data analytics platforms to provide actionable insights and automate routine tasks. Strategic acquisitions of niche technology boutiques allow large consultancies to expand their capabilities in cybersecurity cloud computing and software development. Talent retention and upskilling remain critical strategies as companies compete for specialized expertise in emerging fields. Diversification into sustainability and environmental social and governance consulting helps firms address growing regulatory and consumer demands. Partnerships with academic institutions and technology providers foster innovation and thought leadership. These approaches enable consultancies to differentiate their offerings and maintain relevance in a rapidly evolving business environment.

MARKET SEGMENTATION

This research report on the U.S Consulting market is segmented and sub-segmented into the following categories.

By Service Type

- Operations Consulting

- Strategy Consulting

- Financial Advisory

- Technology Advisory

- HR Consulting

- Risk and Compliance Consulting

- Other Service Type

By Client Organisation Size

- Large Enterprises

- Small and Medium Enterprises

By Consulting Domain

- Enterprise Strategy

- Front-Office Transformation

- Supply-Chain and Operations

- Digital Transformation

- Cyber-Risk and Regulation

- M&A and Restructuring

- Other Consulting Domain

By End-User Industry

- BFSI

- Life Sciences and Healthcare

- IT and Telecommunications

- Manufacturing and Industrial

- Other End-User Industry

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is the U.S. consulting market?

The U.S. consulting market includes professional advisory services that help organizations improve strategy, operations, and business performance.

What is driving the growth of the U.S. consulting market?

The market is growing due to rising digital transformation initiatives and increasing demand for specialized business expertise.

What types of consulting services are commonly offered?

Common services include management consulting, IT consulting, financial advisory, HR consulting, and strategy consulting.

Which segment dominates the U.S. consulting market?

Management consulting dominates the market due to strong demand for operational and strategic business guidance.

Who are the primary users of consulting services in the U.S.?

Corporations, government agencies, healthcare providers, and financial institutions are the main users of consulting services.

How is technology influencing the U.S. consulting market?

AI, cloud computing, and data analytics are transforming consulting services and improving business decision-making.

Why is digital transformation increasing consulting demand?

Businesses require expert guidance to modernize operations, improve efficiency, and adopt advanced technologies.

What challenges does the U.S. consulting market face?

Intense competition, talent shortages, and changing client expectations can affect market growth.

How is artificial intelligence impacting the consulting industry?

AI is improving automation, predictive analysis, and service delivery across consulting operations.

What is the future outlook for the U.S. consulting market?

The market is expected to grow steadily with increasing demand for technology-driven and specialized consulting solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com