U.S. Car Leasing Market Size, Share, Trends & Growth Forecast Report By End User, By Type, By Vehicle Type, and By Country (California, Texas, Florida, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Car Leasing Market Size

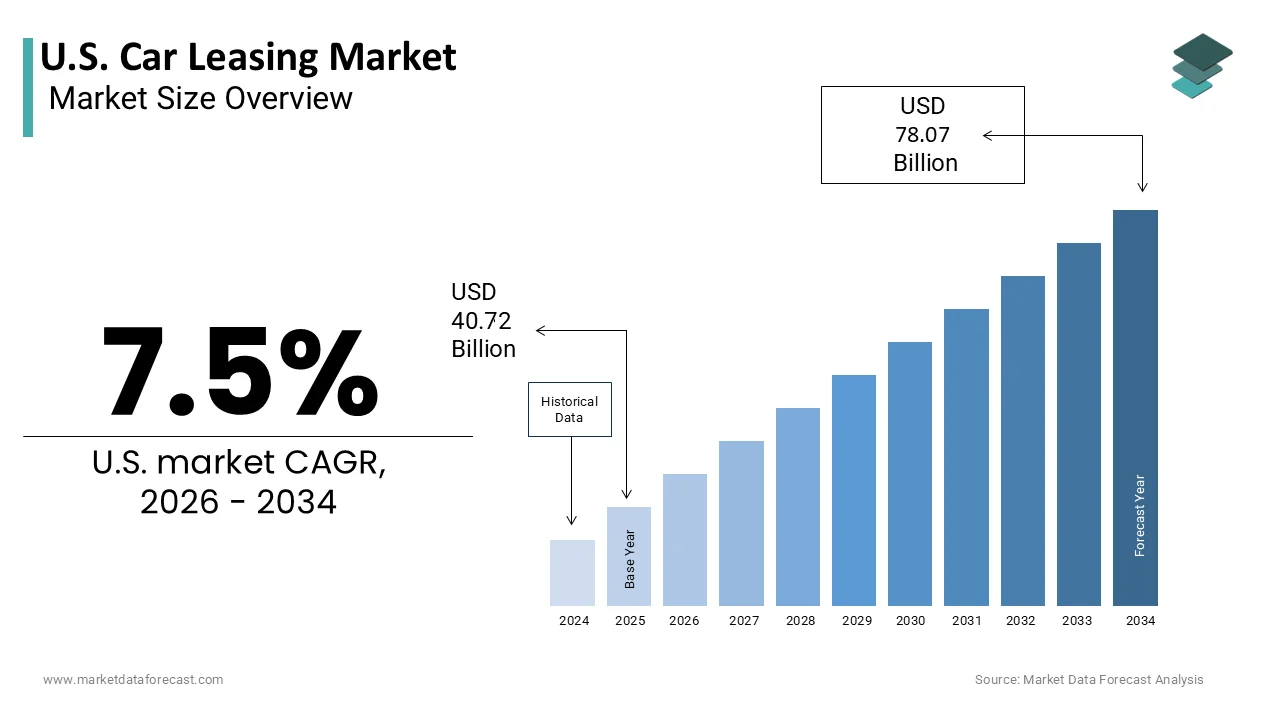

The U.S. Car Leasing Market was valued at USD 40.72 billion in 2025, is estimated to reach USD 43.78 billion in 2026, and is projected to reach USD 78.07 billion by 2034, growing at a CAGR of 7.5% from 2026 to 2034.

The U.S. car leasing market represents a sophisticated financial mechanism wherein consumers secure the right to operate a vehicle for a predetermined period in exchange for monthly payments without acquiring outright ownership. This arrangement appeals primarily to individuals seeking lower monthly expenditures and the flexibility to upgrade to newer models frequently. The structural integrity of this sector relies heavily on residual value predictions and creditworthiness assessments. According to Cox Automotive, the average monthly lease payment for a new vehicle reached approximately $580 in recent quarters, reflecting the premium nature of modern automotive technology. Consumer behavior indicates a strong preference for premium segments, with luxury brands accounting for a disproportionate share of leased units compared to purchased ones. As per the Bureau of Transportation Statistics, the total number of registered vehicles in the U.S. exceeded 283 million, providing a vast base for potential leasing conversions. The demographic profile of lessees skews toward higher income brackets, according to Federal Reserve data showing that households in the top 20% of income distribution hold the majority of lease contracts. This dynamic underscores the market role as a barometer for discretionary spending power among affluent consumers. The integration of digital platforms has streamlined the application process, reducing approval times significantly. Industry participants now leverage telematics to monitor vehicle health, ensuring that returned assets meet stringent condition standards. This operational efficiency supports the sustainability of lease portfolios by minimizing unexpected depreciation costs associated with poor maintenance.

MARKET DRIVERS

Elevated Consumer Preference for Frequent Vehicle Upgrades Drives Leasing Adoption

The desire for access to the latest automotive technologies and safety features is primarily driving the expansion of the U.S. car leasing market. Modern vehicles incorporate advanced driver assistance systems and connectivity features that become obsolete rapidly, prompting consumers to prefer short-term commitments over long-term ownership. As per S&P Global Mobility, the average age of light vehicles on American roads has risen to 12.6 years, yet lessees typically turn over their vehicles every 36 to 48 months. This disparity highlights a distinct segment of the population that values novelty and technological currency. The proliferation of electric vehicles further amplifies this trend, as battery technology evolves quickly, making long-term ownership risky due to potential degradation and obsolescence. According to Edmunds, electric vehicle leases constitute a growing portion of the market, with manufacturers offering attractive terms to mitigate consumer anxiety regarding residual values. The ability to switch to newer models with extended range and faster charging capabilities without the burden of selling a used asset appeals to tech-savvy demographics. Furthermore, corporate fleets utilize leasing to maintain a modern image and ensure employee safety with the latest crash avoidance technologies. This corporate demand reinforces the infrastructure supporting consumer leases, creating economies of scale in vehicle processing and remarketing. The psychological benefit of driving a new car under warranty eliminates repair costs, which is a significant factor for budget-conscious yet quality-oriented consumers who prioritize predictable monthly expenses over equity building.

Financial Flexibility and Lower Monthly Outlays Attract Budget-Conscious Consumers

The economic advantage of reduced monthly payments compared to financing a purchase remains a compelling driver for the U.S. car leasing market. Leasing agreements typically require lower capital outlays initially and result in smaller monthly obligations because the consumer pays only for the depreciation during the lease term rather than the entire vehicle value. According to Experian, the average monthly payment for a new car loan reached $735, whereas lease payments remained substantially lower, often by 20% to 30%. This differential allows consumers to allocate funds to other financial priorities or afford higher trim levels than they might otherwise purchase. The structure of leasing also preserves credit lines for other uses, as the liability does not appear as a large installment loan on balance sheets in the same manner. For young professionals and individuals in transient life stages, this liquidity is invaluable. As per the Consumer Financial Protection Bureau, total auto debt has surged to approximately $1.6 trillion, prompting many to seek alternatives that do not tie up capital in depreciating assets. The tax implications for business owners also favor leasing, as portions of the lease payment may be deductible if the vehicle is used for commercial purposes. This financial engineering appeals to small business owners and independent contractors who form a significant subset of the leasing demographic. The predictability of costs facilitates better personal financial planning, shielding lessees from the volatility of major repair bills that often accompany out-of-warranty owned vehicles.

MARKET RESTRAINTS

Volatility in Residual Values Creates Pricing Uncertainty for Lessors

The stability of the leasing model depends heavily on accurate predictions of future vehicle values, yet market fluctuations introduce significant risk for leasing companies, which is hampering the U.S. car leasing market growth. Residual values determine the monthly payment structure, and incorrect forecasts can lead to substantial losses when vehicles are returned and sold at auction. According to the Manheim Used Vehicle Value Index, used car prices decreased by 14.7% year over year in early 2024, showing the sharp corrections that occur as inventory normalizes. This volatility makes it challenging for lessors to set competitive yet profitable lease terms. When residual values drop unexpectedly, lessors face losses on the backend of the lease cycle, which may lead to tighter credit standards or higher money factors for consumers. As per Cox Automotive, the deviation between predicted and actual residual values can impact profitability by billions of dollars across the industry. The rapid evolution of electric vehicle technology exacerbates this issue, as uncertainty regarding battery longevity and secondary market demand makes forecasting difficult. Lessors must build larger buffers into their pricing models, which can make leases less attractive to price-sensitive consumers. Furthermore, economic downturns can suppress demand for used vehicles, forcing lessors to hold inventory longer or sell at a loss. This financial exposure restricts the willingness of captive finance arms to offer aggressive lease incentives during periods of economic ambiguity. The need for sophisticated data analytics to predict residuals adds operational complexity and cost, which ultimately filters down to the consumer in the form of less favorable terms.

Rising Interest Rates Increase the Cost of Leasing Capital

The macroeconomic environment, characterized by elevated interest rates, directly impacts the affordability and attractiveness of leasing arrangements, which further impedes the U.S. car leasing market growth. Leasing companies borrow capital to acquire vehicles, and higher borrowing costs are passed on to consumers through increased money factors, which function similarly to interest rates in loans. As per the Federal Reserve, the federal funds rate was maintained at a 23-year high of 5.25% to 5.5% throughout much of 2024, influencing the prime rate and subsequently the cost of auto financing. This increase raises the total cost of leasing, narrowing the gap between leasing and buying. For consumers, the higher monthly payments diminish the financial appeal of leasing, particularly for those who are sensitive to cash flow changes. According to Bankrate, the average auto loan rate for new cars recently surpassed 7%, and lease money factors adjusted upward in tandem. This environment discourages marginal lessees who may opt to keep their current vehicles longer or switch to purchasing used cars instead. The higher cost of capital also constrains the ability of leasing firms to expand their fleets, potentially limiting inventory availability for popular models. Furthermore, tight monetary policy often coincides with broader economic slowing, which can reduce consumer confidence and discretionary spending. The combination of higher payments and economic uncertainty leads to a contraction in lease origination volumes. Lessors must navigate this landscape by balancing risk management with competitive pricing, a difficult task when the cost of funds remains elevated. This financial pressure tests the resilience of the leasing model and may lead to a structural shift in consumer preferences toward ownership or alternative mobility solutions.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Leasing Programs Offers Growth Potential

The transition toward electrification is a significant opportunity for the car leasing market in the U.S., as manufacturers and lessors develop specialized programs to address consumer concerns about electric vehicles. Many buyers hesitate to purchase electric cars due to fears about battery degradation and rapid technological obsolescence, making leasing an ideal solution that transfers these risks to the lessor. According to the International Energy Agency, electric vehicle sales reached approximately 1.4 million units in the U.S. in 2023, with a substantial portion occurring through lease channels due to federal and state incentives. The Inflation Reduction Act in the U.S. provides tax credits that are often more accessible through leasing structures, allowing consumers to benefit from savings even if they do not meet strict income or assembly requirements for purchase credits. As per the Department of Energy, the commercial clean vehicle credit allows lessors to pass up to $7,500 in savings to lessees, making them competitive with internal combustion engine counterparts. Manufacturers are leveraging this dynamic to promote their electric portfolios, offering bundled maintenance and charging benefits within lease packages. This holistic approach simplifies the ownership experience and encourages adoption among mainstream consumers. Furthermore, corporate sustainability goals drive fleet electrification, with many companies preferring to lease electric vehicles to manage lifecycle costs and ensure compliance with environmental regulations. The development of robust secondary markets for used electric vehicles will further enhance leasing viability, as lessors gain confidence in residual values. This segment represents a high-growth area where leasing can serve as a bridge technology, facilitating the broader transition to sustainable mobility while generating steady revenue streams for lessors.

Integration of Digital Platforms Enhances Customer Acquisition and Retention

The digital transformation of the automotive retail landscape offers leasing companies the opportunity to streamline operations and improve customer engagement through online channels. Consumers increasingly expect seamless digital experiences, from initial research to contract signing, and lessors that invest in robust online platforms gain a competitive advantage. According to McKinsey, approximately 80% of car buyers begin their journey online, and those who complete the process digitally report higher satisfaction levels. Leasing companies are implementing artificial intelligence and machine learning to personalize offers, assess credit risk more accurately, and predict customer needs. This technological integration reduces administrative costs and accelerates approval times, making leasing more accessible to a broader audience. As per Cox Automotive, 67% of consumers are now interested in completing their entire vehicle acquisition online, which increases conversion rates by providing transparent pricing and flexible terms. The ability to manage lease accounts, schedule maintenance, and initiate end-of-lease processes through mobile applications enhances customer loyalty and reduces churn. Furthermore, data analytics enable lessors to identify cross-selling opportunities, such as insurance or extended warranty products, thereby increasing revenue per customer. The shift toward subscription-based models, which blend elements of leasing and renting, is facilitated by these digital infrastructures, allowing for greater flexibility and customization. By embracing digital innovation, leasing companies can differentiate themselves in a crowded market and build lasting relationships with tech-savvy consumers who value convenience and transparency. This digital-first approach also supports remote work trends, enabling nationwide reach without the constraints of physical dealership networks.

MARKET CHALLENGES

Supply Chain Disruptions Constrain Inventory Availability for Lease Fleets

The lingering effects of global supply chain interruptions continue to pose a significant challenge to the U.S. car leasing market. Semiconductor shortages and logistical bottlenecks have reduced the production volume of new cars, forcing lessors to compete intensely for limited inventory. According to the United States Department of Commerce, the global semiconductor shortage resulted in a production loss of several million vehicles, leading to a decline in lease originations. This scarcity drives up the acquisition cost of vehicles, which is passed on to consumers in the form of higher capitalized costs and reduced incentives. The lack of inventory also limits the variety of models available for lease, restricting consumer choice and potentially driving them toward competitors or alternative transportation modes. As per Kelley Blue Book, the average transaction price for new vehicles remained above $48,000 due to supply constraints, impacting the economics of leasing. Lessors face the dilemma of either paying premium prices to maintain fleet size or accepting smaller portfolios with reduced market presence. This situation disrupts the traditional cycle of leasing, where steady inflows of new vehicles are essential for maintaining competitive offerings. The uncertainty surrounding future supply conditions makes long-term planning difficult, as lessors cannot guarantee the availability of specific models for upcoming lease terms. This operational friction increases costs and reduces profitability, challenging the sustainability of current leasing models. Recovery depends on the stabilization of global manufacturing networks, which remain subject to geopolitical and economic variables beyond the control of individual leasing firms.

Regulatory Complexities Regarding Emissions and Consumer Protection Increase Compliance Costs

The evolving regulatory landscape in the U.S. introduces additional layers of complexity and cost for leasing companies, particularly concerning emissions standards and consumer protection laws, which further challenge the car leasing market expansion in the U.S. Stricter environmental regulations require lessors to manage fleets with lower carbon footprints, necessitating investments in cleaner vehicles and compliance monitoring systems. According to the Environmental Protection Agency, the Multi-Pollutant Emissions Standards for Model Years 2027-2032 mandate significant reductions in greenhouse gas outputs, pushing manufacturers and lessors toward electrification and hybrid technologies. Compliance with these standards involves substantial administrative effort and financial investment, which can erode profit margins. Additionally, consumer protection agencies are scrutinizing leasing practices more closely, requiring greater transparency in advertising and contract terms. As per the Consumer Financial Protection Bureau, oversight of auto leasing has intensified, compelling companies to overhaul their compliance frameworks. These regulatory demands require legal expertise and ongoing training for staff, adding to operational overhead. The variation in state-level regulations further complicates national leasing strategies, as companies must navigate a patchwork of laws governing disclosures, fees, and end-of-lease procedures. This fragmented regulatory environment increases the risk of non-compliance and potential litigation. Lessors must remain agile to adapt to changing rules, which can shift rapidly in response to political and social pressures. The cost of maintaining compliance diverts resources from innovation and customer service, potentially hindering competitive positioning. Navigating this complex web of regulations requires strategic foresight and robust governance structures to ensure sustainable operations in a highly scrutinized industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End User, Type, Vehicle Type, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Enterprise Holdings, Inc., Hertz Global Holdings, Inc., Avis Budget Group, Inc., LeasePlan Corporation N.V., Element Fleet Management Corp., Wheels, Inc., ALD Automotive, Arval, Sixt SE, ARI Fleet Management Company, Ally Financial Inc., Toyota Financial Services |

SEGMENTAL ANALYSIS

BY End User Insights

The non-commercial segment dominated the market in 2025 and is likely to remain the dominating position in the U.S. car leasing market over the next few years, owing to the widespread adoption of leasing among affluent households who prioritize lower monthly payments and the ability to drive new models without the long-term commitment of ownership. According to Experian, individual consumers account for approximately 78% of all new vehicle leases in the U.S., reflecting the strong appeal of leasing structures to personal users. The primary driver for this segment is the desire to avoid the risks associated with vehicle depreciation and maintenance costs after the warranty period expires. As per S&P Global Mobility, the average lease term for non-commercial users is 36 months, allowing consumers to upgrade frequently to vehicles equipped with the latest safety and connectivity technologies. Furthermore, the tax benefits available to certain self-employed individuals and high-income earners enhance the attractiveness of leasing for personal use. The Federal Reserve reports that households in the top decile of wealth are significantly more likely to lease than to finance, citing liquidity preservation as a key motive. This demographic trend ensures that the non-commercial segment remains the cornerstone of the leasing industry, supported by robust marketing efforts from captive finance companies targeting retail customers. The ease of digital leasing platforms has further accelerated adoption among younger consumers who value convenience and transparency in financial transactions.

However, the commercial segment is expected to show robust expansion over the next few years as companies increasingly adopt leased fleets to meet corporate sustainability goals and optimize capital. Businesses are increasingly leveraging leasing to manage vehicle lifecycles, reduce capital expenditure, and align with sustainability goals. As per the National Association of Fleet Administrators, corporate fleets are expanding their leased portfolios by approximately 5% annually, as companies seek to optimize the total cost of ownership. A major factor driving this growth is the transition to electric vehicles, where leasing allows corporations to mitigate risks related to battery technology evolution and residual value uncertainty. According to the Department of Energy, the Alternative Fuel Vehicle Refueling Property Credit and related leasing incentives have spurred a 15% increase in corporate EV adoption through leasing channels. Additionally, the rise of mobility as a service models has prompted companies to prefer flexible leasing arrangements that allow for scalable fleet adjustments based on demand. The Bureau of Labor Statistics indicates that industries such as logistics and professional services are increasing their reliance on leased vehicles to maintain operational agility without tying up balance sheet capital. This strategic approach enables businesses to allocate resources to core competencies while outsourcing vehicle management to specialized lessors. The integration of telematics and data analytics in commercial leases further enhances value by providing insights into driver behavior and fuel efficiency, supporting broader corporate sustainability and cost reduction objectives.

BY Type Insights

The closed-end lease segment led the market in 2025 and is expected to continue its market leadership over the next few years as it remains the standard for consumer-facing automotive finance in the U.S. In a closed-end lease, the lessee returns the vehicle at the end of the term with no further financial obligation beyond excess wear and tear or mileage penalties, making it the preferred choice for individual consumers. According to the Consumer Financial Protection Bureau, approximately 85% of consumer auto leases in the U.S. are structured as closed-ended agreements, highlighting the strong preference for fixed liability structures. The primary driver for this dominance is the peace of mind it offers regarding vehicle depreciation, as the lessor assumes the risk of the asset's future market value. As per Edmunds, this structure allows consumers to budget effectively without worrying about fluctuating used car prices at the end of the lease term. Furthermore, regulatory frameworks such as the Consumer Leasing Act provide clear guidelines for closed-end leases, enhancing consumer confidence and transparency. The Federal Trade Commission emphasizes that closed-end leases offer standardized disclosure requirements, which help consumers compare offers more easily. This regulatory clarity, combined with the financial security of knowing the maximum liability upfront, sustains the leading position of closed-end leases. Manufacturers and banks favor this model as well, as it facilitates predictable remarketing strategies and steady revenue streams from vehicle sales at auction.

On the other side, the open-ended lease segment is likely to experience the fastest growth during the forecast period due to the high adoption rates within the logistics and service sectors over the next few years, due to the flexibility it offers commercial operators. Unlike closed-ended leases, open-ended leases place the residual value risk on the lessee, which appeals to businesses that can better manage asset valuation and tax implications. According to the National Vehicle Leasing Association, the open-ended segment is expected to grow at a CAGR of 4.5% over the next five years, outpacing the consumer-focused closed-ended market. The primary factor driving this growth is the flexibility it offers to commercial entities in managing fleet assets and claiming tax deductions. As per the Internal Revenue Service, businesses can often deduct the full lease payments as an operating expense, providing significant financial advantages. This structure is particularly attractive for heavy-duty vehicles and specialized equipment where usage patterns vary widely. The Bureau of Economic Analysis notes that increased business investment in transportation equipment is fueling demand for open-ended leases, as companies seek to align vehicle costs with actual usage. Additionally, the rise of gig economy platforms and logistics firms has created a need for flexible leasing solutions that allow for early termination or modification, features more commonly available in open-ended contracts. This adaptability supports the rapid expansion of the segment as businesses prioritize operational agility over fixed cost structures.

By Vehicle Type Insights

The passenger cars segment held the major share of the U.S. car leasing market in 2025 and is expected to maintain a significant presence in the lease market over the next few years as sedans remain a popular entry point for brand-conscious and budget-oriented lessees. This segment dominates due to the high volume of retail leases initiated by individual consumers who prioritize comfort, fuel efficiency, and brand prestige. According to Cox Automotive, passenger cars account for approximately 60% of all leased vehicles in the U.S. market, despite the broader market shift toward sport utility vehicles. The primary driver for this leadership is the aggressive leasing incentives offered by manufacturers on passenger car models to maintain production volumes and market share. As per Kelley Blue Book, lease deals on compact and mid-size sedans often feature lower monthly payments compared to larger vehicles, attracting budget-conscious consumers and first-time lessees. Furthermore, the luxury passenger car segment remains a stronghold for leasing, as high-net-worth individuals prefer to upgrade to the latest models every few years. The Federal Reserve data indicate that spending on durable goods, including luxury automobiles, remains robust among top income earners, supporting steady lease originations in this category. The availability of advanced technology features in newer passenger car models also drives turnover, as consumers seek improved safety and connectivity options. Captive finance arms of major automakers continue to promote passenger car leases through subsidized money factors, ensuring that this segment retains its dominant position in the overall leasing landscape.

On the other hand, the commercial vehicles segment is on the rise and is likely to be the primary driver of fleet-based leasing growth over the next few years as the e-commerce sector continues to expand its delivery capabilities. This segment includes light trucks, vans, and specialized vehicles used for business purposes, which are increasingly acquired through leasing arrangements to support logistical operations. According to the American Trucking Associations, the demand for commercial vehicle leasing is rising at a CAGR of 5.2%, driven by the need for flexible fleet management solutions. The primary factor behind this growth is the surge in online shopping, which has increased the requirement for delivery vehicles that can be scaled up or down based on seasonal demand. As per the U.S. Department of Commerce, e-commerce sales reached $1.1 trillion in 2023, prompting logistics companies to lease rather than purchase vehicles to maintain liquidity and adapt to changing routes. Additionally, the transition to electric commercial vehicles is accelerating lease adoption, as businesses leverage federal incentives and manufacturer programs to test new technologies without long-term commitment. The Environmental Protection Agency highlights that commercial fleets are under pressure to reduce emissions, making leasing an attractive option for accessing newer, cleaner vehicles. This dynamic is further supported by the development of specialized leasing products tailored to the unique usage patterns of commercial operators, including higher mileage allowances and maintenance packages. These factors collectively contribute to the rapid expansion of the commercial vehicles segment within the leasing market.

COUNTRY LEVEL ANALYSIS

U.S.

The U.S. is likely to remain at the forefront of automotive financial innovation for the next few years as the country continues to refine its digital leasing infrastructure and EV support systems. As the world's second-largest auto market, the U.S. exhibits a mature and highly sophisticated leasing ecosystem that serves as a global benchmark for financial innovation and consumer adoption. The market status is characterized by high penetration rates among affluent demographics and a robust infrastructure supporting vehicle remarketing and residual value management. According to the Federal Reserve Bank of New York, auto loan and lease balances in the U.S. reached $1.6 trillion in early 2024, underscoring the critical role of leasing in household finance and automotive consumption. The primary driving factor for this market stature is the cultural preference for frequent vehicle upgrades and the widespread availability of credit. As per Experian, the leasing penetration rate in the U.S. hovers around 20% to 25% of new vehicle transactions, a figure that remains stable despite economic fluctuations. This stability is supported by strong competition among captive finance companies and banks, which offer competitive terms to attract high-quality borrowers. The presence of major automotive manufacturers with dedicated leasing arms ensures a steady supply of vehicles and innovative lease products. Furthermore, the regulatory environment, including federal tax laws and consumer protection statutes, provides a clear framework that fosters confidence among both lessors and lessees. The integration of digital technologies in the leasing process has further enhanced market efficiency, allowing for seamless transactions and personalized offerings. This combination of financial depth, consumer demand, and operational sophistication cements the U.S. position as the dominant force in the regional car leasing landscape.

COMPETITIVE LANDSCAPE

The competitive landscape of the U.S. car leasing market is characterized by intense rivalry among captive finance companies, banks,s and independent leasing firms. Captive finance arms of major automakers hold a distinct advantage due to their ability to control vehicle supply and influence residual values through coordinated remarketing efforts. These entities leverage brand loyalty and integrated dealership networks to offer subsidized lease rates that independent competitors struggle to match. Banks and credit unions compete by providing flexible terms and appealing to customers with established banking relationships who prioritize interest rate competitiveness over brand affiliation. The entry of fintech companies introduces further disruption by offering streamlined digital experiences and alternative credit scoring models that expand access to leasing for non-traditional borrowers. Competition is also driven by innovation in product offerings, such as subscription-based models that blend leasing with rental flexibility. Companies must continuously adapt to changing consumer preferences for electric vehicles and digital convenience while managing risks associated with residual value volatility and regulatory compliance. This dynamic environment requires constant investment in technology and customer service to differentiate offerings and retain market relevance amidst shifting economic conditions and technological advancements in the automotive sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Car Leasing Market include

- Enterprise Holdings, Inc.

- Hertz Global Holdings, Inc.

- Avis Budget Group, Inc.

- LeasePlan Corporation N.V.

- Element Fleet Management Corp.

- Wheels, Inc.

- ALD Automotive (Société Générale Group)

- Arval (BNP Paribas Group)

- Sixt SE

- ARI Fleet Management Company

- Ally Financial Inc.

- Toyota Financial Services

TOP LEADING PLAYERS IN THE MARKET

- Toyota Financial Services operates as a pivotal entity within the U.S. car leasing landscape by providing tailored financial products to retail and commercial clients. The company leverages its strong brand reputation to offer competitive lease terms on a wide array of Toyota and Lexus vehicles. Recent initiatives focus on integrating digital tools that streamline the application process and enhance customer experience through mobile platforms. Toyota has also expanded its electric vehicle leasing options to align with evolving consumer preferences for sustainable mobility solutions. By investing in data analytics, the company improves residual value forecasting accuracy, which reduces risk and enables more attractive pricing structures for lessees. These strategic moves reinforce its position as a preferred partner for consumers seeking reliability and innovation in their leasing arrangements while supporting broader corporate sustainability goals through increased adoption of hybrid and electric models in leased fleets across the nation.

- Ford Motor Credit Company serves as a cornerstone of the U.S. car leasing market by offering comprehensive financing and leasing solutions for Ford and Lincoln vehicles. The company actively promotes leasing through aggressive incentive programs and partnerships with dealerships to drive volume. Recently,y it has focused on enhancing its digital infrastructure to provide seamless online leasing experiences that cater to tech-savvy consumers. Ford Motor Credit has also introduced flexible lease-end options and maintenance packages that add value for customers seeking convenience and predictability. Its commitment to electrification is evident in specialized lease offers for electric models, which help mitigate consumer concerns about battery life and resale value. By leveraging advanced telematics and customer data insight,s the company optimizes risk management and tailors products to specific demographic needs, ds thereby strengthening its competitive stance and fostering long-term customer loyalty in a dynamic automotive financial environment.

- Honda Finance Corporation plays a significant role in the U.S. car leasing market by delivering robust leasing products for the Honda and Acura brands. The company emphasizes customer-centric services that include flexible terms and transparent pricing structures to attract a diverse clientele. Recent efforts have been directed toward expanding its digital capabilities, allowing borrowers to complete lease transactions entirely online with minimal friction. Honda Finance has also prioritized sustainability by promoting leases for hybrid and electric vehicles,s which aligns with regulatory trends and consumer demand for greener transportation options. Through strategic collaborations with technology firms, ms the company enhances its credit assessment processes using artificial intelligence to improve approval rates and reduce default risks. These actions demonstrate a commitment to innovation and customer satisfaction, ensuring that Honda Finance remains a key contributor to the growth and stability of the leasing sector while adapting to shifting market dynamics and technological advancements in the automotive industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. car leasing market employ several strategic initiatives to maintain competitiveness and drive growth. Digital transformation stands out as a primary strategy where companies invest heavily in online platforms and mobile applications to streamline the leasing process and enhance user experience. This approach allows for faster approvals and greater transparency w, which appeals to modern consumers. Another critical strategy involves the expansion of electric vehicle leasing portfolios. Manufacturers and finance arms are creating specialized lease products for electric cars to address consumer anxiety regarding battery degradation and residual values. Partnerships with technology firms enable better data analytics for risk assessment and personalized marketing. Additionally, our company's focus is on flexible lease-end options and maintenance bundles to increase customer retention. These strategies collectively aim to reduce operational costs while improving service quality and adapting to regulatory changes surrounding emissions and consumer protection laws in the automotive financial sector.

MARKET SEGMENTATION

This research report on the U.S. car leasing market which is segmented and sub-segmented into the following categories

By End User

- Non-Commercial

- Commercial

By Type

- Closed-Ended Lease

- Open-Ended Lease

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Country

- California

- Texas

- Florida

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com