Global Semiconductor Equipment Market Size, Share, Trends & Growth Forecast Report By Front-end Equipment (Lithography, Wafer Surface Conditioning) Back-end Equipment (Assembly and Packaging, Dicing)Fab Facility Equipment(Automation,Chemical Control) Product Type (Memory ,Foundry) Dimension (2D ICs,2.5D ICs) and Region (North America, Europe, APAC, Latin America, Middle East And Africa), Industry Analysis From 2025 to 2033

Global Semiconductor Equipment Market Size

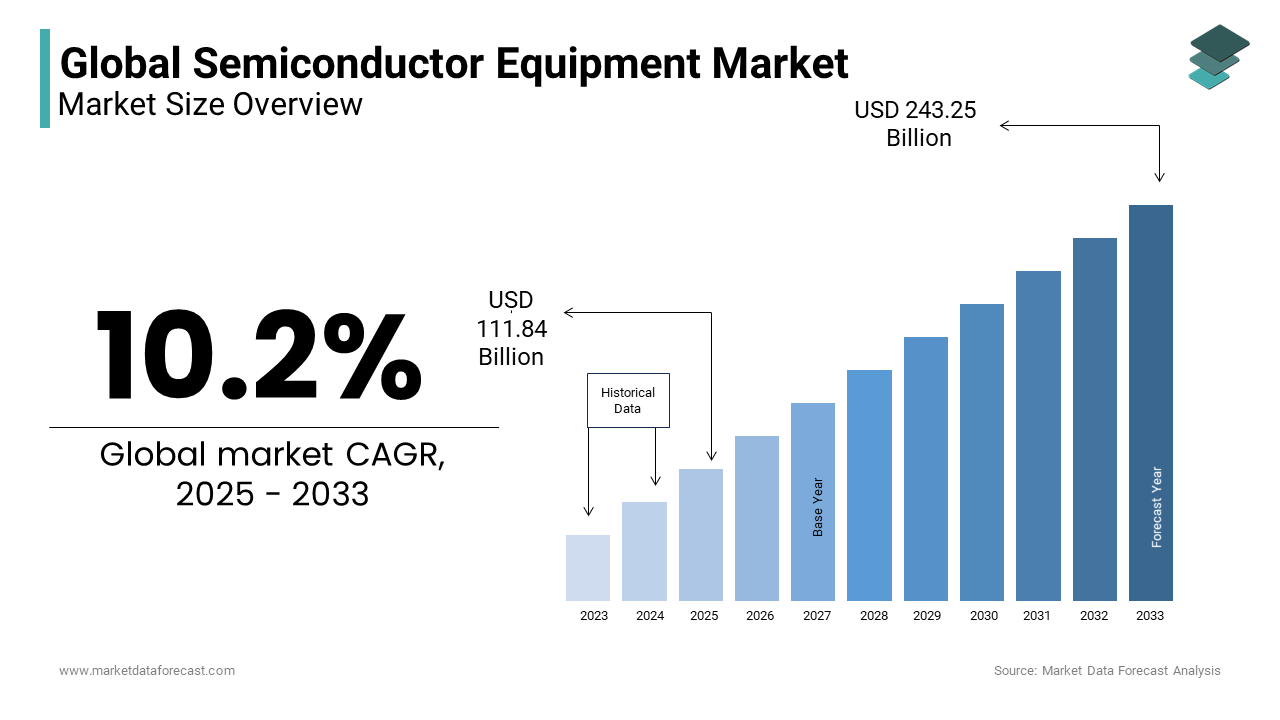

The global semiconductor equipment market size was valued at USD 101.49 billion in 2024. The semiconductor equipment market Size is expected to have 10.2 % CAGR from 2025 to 2033 and be worth USD 243.25 billion by 2033 from USD 111.84 billion in 2025.

The Semiconductor Equipment Market is an essential part of the global technology industry. It provides the advanced machines needed to manufacture semiconductor chips. These chips are found in almost every modern device, from mobile phones and laptops to cars, airplanes, and communication systems. The demand for semiconductor equipment is increasing due to new technologies. For example, artificial intelligence (AI) is expected to need 1,000 times more computing power by 2030 than in 2023, meaning chip-making must become more advanced. The car industry also relies heavily on semiconductors. Today’s electric vehicles (EVs) use over 1,400 chips per car, which is far more than older gasoline-powered cars.

With digital technology growing fast, over 90% of the world's data has been created in just the last two years. This has increased the need for high-performance chips. The switch to 5G networks is also pushing data usage higher, with traffic expected to rise by over 400% by 2027. This puts pressure on semiconductor factories to work faster and more efficiently. Making chips also requires a lot of natural resources. A single 12-inch wafer factory (called a fab) uses about 10 million gallons of water per day. Because of this, manufacturers are focusing on sustainable practices like recycling water and using less energy. This helps them reduce their environmental impact while keeping production running smoothly.

MARKET DRIVERS

Government Initiatives and Investments

Governments worldwide are making major efforts to support semiconductor manufacturing because of its strategic importance. In the United States, the CHIPS and Science Act, passed in August 2022, provides $52.7 billion for improving domestic semiconductor production and research. This is intended to make supply chains stronger and reduce dependence on foreign suppliers. Similarly, the European Chips Act, introduced in 2023, aims to increase Europe’s share of global semiconductor production to 20% by 2030. These large investments by governments show a strong global trend of securing semiconductor supply chains and boosting domestic production through significant public funding and support.

Geopolitical Shifts and Supply Chain Realignments

Rising political tensions, especially between the United States and China, have forced companies to change where they manufacture semiconductor products. Many companies are now moving their production to other countries, including Vietnam, India, Malaysia, and Mexico, to reduce risks from overreliance on China. This shift has made Southeast Asia a fast-growing hub for semiconductor production, attracting heavy investment from global technology firms. Malaysia’s Penang region has become a key location for semiconductor factories. These changes in supply chains help companies reduce risks from trade restrictions, improve supply stability, and strengthen global semiconductor production resilience in uncertain political conditions.

MARKET RESTRAINTS

Skilled Labor Shortages

One of the biggest challenges in the semiconductor market is the shortage of skilled workers. The U.S. CHIPS and Science Act aims to boost semiconductor production, but the country is expected to face a shortfall of about 67,000 skilled technicians, engineers, and scientists by 2030, according to the Semiconductor market Association in 2023. This problem is worsened by low enrollment in technical education programs and visa restrictions for international talent. Leading semiconductor companies like TSMC and Intel have reported delays in their U.S. projects due to a lack of skilled workers. For example, TSMC's Arizona factory has faced delays, with the company stating that the shortage of skilled workers is one of the main reasons. This labor issue could slow down future expansion in the semiconductor market.

Geopolitical Tensions and Trade Restrictions

Political and economic conflicts and especially between the U.S. and China, have made it harder for semiconductor companies to do business. In October 2022, the U.S. Department of Commerce introduced strict export controls, which block China from buying advanced semiconductor equipment and computing chips. These restrictions aim to limit China’s progress in AI and defense technologies. However, this also affects companies that sell semiconductor equipment. Applied Materials, a major semiconductor equipment provider, announced in February 2025 that it expects to lose about $400 million in revenue this year, with half of that impact hitting in the second quarter. These trade restrictions increase supply chain risks, reduce market access and force companies to rethink their global business strategies.

MARKET OPPORTUNITIES

Expansion of Semiconductor Manufacturing Capacity

The semiconductor market is expected to grow quickly in the coming years, creating big opportunities for semiconductor equipment suppliers. A report from the Semiconductor Industry Association (SIA) and the Boston Consulting Group predicts that the U.S. will triple its domestic semiconductor manufacturing capacity between 2022 and 2032, a 203% increase which is the highest projected growth worldwide. This expansion is mostly due to government policies like the CHIPS and Science Act, which encourages more chip production in the United States. As a result, demand for semiconductor manufacturing tools and technologies is expected to grow significantly, making it a huge business opportunity for equipment suppliers.

Technological Advancements in Semiconductor Manufacturing

New semiconductor technology is creating demand for highly advanced equipment. The National Institute of Standards and Technology (NIST) states that developing better measurement standards and manufacturing techniques is important for the future of semiconductor production. Modern innovations, such as extreme ultraviolet (EUV) lithography and advanced packaging techniques, require extremely precise and sophisticated machines. Companies are working to create smaller, faster, and more energy-efficient chips, which increases the demand for cutting-edge semiconductor manufacturing equipment. As technology advances, semiconductor equipment providers will have greater opportunities to grow by offering solutions that help meet the evolving needs of the market.

MARKET CHALLENGES

Supply Chain Vulnerabilities

The semiconductor equipment market is highly sensitive to supply chain disruptions, which can cause serious delays and financial losses. The global chip shortage from 2020 to 2023, worsened by the COVID-19 pandemic, exposed weaknesses in semiconductor supply chains. Problems such as factory closures, rising demand for electronics, and transport delays created severe shortages that impacted multiple industries. This crisis highlighted the need for a more resilient and diverse supply chain to reduce risks. Companies are now investing in supply chain improvements, securing alternative suppliers, and expanding manufacturing locations to ensure they can handle future disruptions and avoid major losses.

Environmental and Regulatory Challenges

Producing semiconductor chips uses a lot of water and energy, which raises concerns about its environmental impact. Taiwan, one of the world’s largest semiconductor producers, faced its worst drought in over 50 years in 2021, creating serious issues for chip manufacturers that require huge amounts of water. TSMC, the world’s largest contract chipmaker, uses millions of gallons of water per day in its factories. Due to these challenges, companies are adopting new technologies to reduce water consumption and improve sustainability. Governments are also introducing stricter environmental regulations, forcing semiconductor companies to invest in greener manufacturing methods to comply with new laws while maintaining production efficiency.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

10.2 % |

|

Segments Covered |

By Front-end Equipment, Back-end Equipment ,Fab Facility Equipment, Product Type, Dimension and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leader Profiled |

Tokyo Electron Limited (Japan),Lam Research Corporation (US),ASML (Netherlands). |

SEGMENTAL ANALYSIS

By Front-end Equipment Insights

The lithography segment dominated the market by capturing 22.2% of the global market share in 2024. Its pivotal role in advanced node fabrication is driving the growth of this segment in the global market. According to ASML’s 2022 annual report, EUV systems alone accounted for €6.3 billion in revenue, underscoring their criticality. The U.S. Department of Commerce reported that lithography drives over 50% of process innovations in semiconductors, enabling advancements like 3nm nodes. Additionally, EUV adoption reduces patterning costs by up to 25% compared to DUV at advanced nodes. Its importance is further validated by TSMC’s reliance on EUV for 70% of its 5nm production.

The EUV lithography is predicted to witness the highest CAGR of 31.4% from 2025 to 2033 due to the escalating demand for high-performance chips below 5nm, where EUV eliminates multi-patterning inefficiencies. ASML reported shipping 83 EUV systems in 2022, a 40% increase from 2021, reflecting surging adoption. The Semiconductor Industry Association states that EUV reduces manufacturing steps by approximately 30%, lowering defect rates significantly. Furthermore, BloombergNEF forecasts that global semiconductor revenues will reach $1 trillion by 2030, with EUV playing a central role. The IEEE corroborates this, noting that EUV enables faster scaling for AI and IoT applications, solidifying its transformative impact.

By Back-end Equipment Insights

The Assembly and packaging segment led the back-end semiconductor equipment market and held a 40.2% share in 2024 owing to the growing adoption of advanced packaging technologies like 3D stacking and fan-out wafer-level packaging, which improve chip performance and reduce power consumption. The U.S. Department of Commerce stated that advanced packaging reduces interconnect delays by up to 40%, enabling faster data processing. Additionally, McKinsey notes that packaging innovations contribute to 25% cost savings in semiconductor manufacturing, making it critical for scaling next-generation applications.

The Wafer testing/IC testing segment is estimated to register the fastest CAGR of 8.5% from 2025 to 2033. This growth is fueled by increasing complexity in semiconductor designs, requiring more rigorous testing protocols. The Semiconductor Industry Association states that testing ensures 95% defect detection, preventing costly post-production failures. BloombergNEF reports that the rise of AI, 5G, and IoT applications will drive demand for precision testing, with the global semiconductor testing equipment market expected to reach $10 billion by 2026. ASML revealed that advanced nodes below 5nm require 50% more test points, driving innovation in testing technologies. The IEEE emphasizes that efficient testing reduces yield losses by up to 30%, underscoring its importance in maintaining semiconductor quality and reliability.

By Fab Facility Equipment Insights

The Gas control equipment segment held the leading share of 42.5% share in 2024. This leadership stems from its critical role in maintaining precise gas purity and flow, which directly impacts semiconductor yield and quality. The U.S. Department of Energy found that even trace impurities at parts-per-billion levels can reduce chip yields by up to 25%. Additionally, efficient gas control systems improve process stability by 20%, making them indispensable for high-volume manufacturing.

The Automation segment is anticipated to witness the fastest CAGR of 9.8%. The increasing adoption of Industry 4.0 technologies in fabs to enhance efficiency and reduce human error is fuelling the segment’s growth. The International Federation of Robotics reports that semiconductor fabs deployed over 2,000 industrial robots in 2022, a 15% increase from 2021. BloombergNEF forecasts that automated material handling systems will reduce production cycle times by 30%, boosting output. ASML stated that automation minimizes contamination risks, improving yields by 10-15%. The Semiconductor Industry Association emphasizes that smart automation enables real-time monitoring, reducing downtime by 25% and supporting the transition to fully autonomous fabs.

By Product Type Insights

The Foundry segment was the largest segment in the semiconductor equipment market and held a 32.9% share in 2024 because of the increasing demand for outsourced chip manufacturing, particularly for advanced nodes below 5nm. The U.S. Department of Commerce reported that foundries account for over 75% of global semiconductor production capacity. According to TrendForce, TSMC captured 54% of the global foundry market in 2022. Additionally, McKinsey notes that foundries enable fabless companies like NVIDIA and AMD to focus on design innovation, reducing their capital expenditure by up to 35%. Foundries are critical for scaling AI, 5G, and IoT applications.

The Memory is likely to experience the fastest CAGR of 9.6% due to the rising demand for high-density DRAM and NAND flash memory in data centers, AI, and edge computing. The Semiconductor Industry Association states that memory chips accounted for 28% of global semiconductor sales in 2022, reaching $150 billion. BloombergNEF forecasts that hyperscale data centers will double their memory requirements by 2030, driving innovation in 3D NAND and HBM technologies. Samsung reports that advancements in memory reduce power consumption by 25% while increasing storage capacity by 50%. The IEEE emphasizes that memory innovations are pivotal for enabling real-time processing in autonomous vehicles and cloud computing, underscoring its transformative role

By Dimension Insights

The 2D ICs dominated the semiconductor equipment market and captured a 58.3% share in 2024. This leadership stems from their widespread use in consumer electronics, automotive, and industrial applications due to cost efficiency and mature manufacturing processes. The U.S. Department of Commerce reported that 2D ICs account for over 65% of chips used in IoT devices. . Additionally, 2D ICs reduce production costs by up to 35% compared to advanced packaging solutions, making them vital for high-volume applications.

The 3D ICs segment is on the rise and is expected to be the fastest growing segment in the global market by witnessing a CAGR of 14.2%. This growth is fueled by the increasing demand for high-performance computing (HPC) and AI applications requiring higher transistor density. The Semiconductor Industry Association states that 3D ICs improve interconnect speed by 40% while reducing power consumption by 25%. BloombergNEF forecasts that 3D IC adoption will grow alongside the rise of 5G and autonomous vehicles, with revenues projected to exceed $35 billion by 2030. ASML showed that 3D stacking enables up to 8x higher integration density than 2D ICs. The IEEE emphasizes that 3D ICs are pivotal for enabling compact, energy-efficient designs in next-generation technologies like quantum computing and edge AI.

REGIONAL ANALYSIS

The Asia-Pacific region led in the semiconductor equipment market by contributing 68.6% share in 2024. This is mainly due to large investments in chip manufacturing by China, South Korea, Taiwan, and Japan. These countries are spending billions to increase their semiconductor production capacity. For example, China invested $29.6 billion in chip-making equipment in 2021, which was 58% more than in 2020, according to the Semiconductor Equipment Association of Japan. Such heavy investments show that Asia-Pacific is committed to maintaining its position in the global semiconductor market. As demand for chips continues to grow, this region will remain a key player in the world’s semiconductor supply chain.

The semiconductor equipment market in Europe is growing quickly. From 2025 to 2033, it is expected to grow at a CAGR of 8.9% which is making it one of the fastest-growing regions in this market. One major reason for this rapid growth is the European Chips Act, which was introduced to increase Europe's semiconductor production to 20% of the global market by 2030. This program has brought together over €43 billion in public and private investments to improve research, chip design, and manufacturing capabilities. This will help Europe become less dependent on other countries for semiconductor supply. As a result, Europe is strengthening its role in the global semiconductor market and reducing risks associated with global supply chain disruptions.

The North American semiconductor equipment market plays an important role in global chip production. This is largely due to strong investments and advancements in technology. In the United States, the government passed the CHIPS and Science Act, which set aside over $52 billion to increase semiconductor manufacturing and research. This law aims to make U.S. supply chains stronger and reduce reliance on foreign suppliers. The U.S. is also a major exporter of semiconductors, with chip exports reaching $62 billion in 2021. These numbers show that North America remains a critical region for semiconductor production. With more investments in manufacturing, the region will continue to play a key role in the future of the global semiconductor market.

The semiconductor equipment market in Latin America is expected to grow gradually in the coming years. Right now, the region has a small share of the global market, but countries like Brazil and Mexico are working hard to attract investments in semiconductor manufacturing. These nations are offering government incentives and policies to improve their technology workforce and infrastructure. As global semiconductor companies look for new locations to manufacture chips, Latin America could become an important part of the global supply chain. With a strategic location and increasing technological capabilities, the region has great potential to grow in semiconductor manufacturing in the future.

The Middle East and Africa are emerging markets in the semiconductor equipment market. While the region currently holds a small market share, some governments are investing in semiconductor research and education to prepare for future growth. For example, Israel has launched several initiatives focused on research and development in semiconductor technologies. These efforts aim to attract global semiconductor companies and boost local technology industries. Even though this region is still developing its semiconductor capabilities, ongoing investments in technology, policy improvements, and education programs could help the Middle East and Africa become more involved in the global semiconductor supply chain in the next decade.

Top 3 Players in the market

ASML Holding

ASML Holding is the most important company in the semiconductor equipment market. It is based in the Netherlands and is the only company in the world that makes extreme ultraviolet (EUV) lithography machines. These machines are needed to make the most advanced chips used in AI, high-performance computing, and 5G networks. The biggest chip manufacturers like TSMC, Samsung, and Intel rely on ASML’s technology. The company is constantly improving its machines, and it is working on High-NA EUV systems, which will help create even smaller and more powerful chips. ASML plays a key role in making sure that semiconductor technology keeps advancing quickly.

Applied Materials

Applied Materials is one of the biggest American semiconductor equipment companies. It creates advanced tools for making semiconductor chips, including deposition, etching, and metrology machines. These tools are important for producing modern chips that are smaller, faster, and more energy-efficient. Applied Materials has helped develop 3D transistors, advanced memory technologies, and powerful logic chips. The company works closely with major semiconductor producers like Intel, TSMC, and Samsung. In addition, it is investing in AI-driven chip manufacturing to make production more efficient. By focusing on innovation, Applied Materials ensures that chipmakers can continue to improve their semiconductor designs.

Tokyo Electron Limited (TEL)

Tokyo Electron Limited (TEL) is a Japanese company that specializes in making equipment for wafer fabrication. It is well known for its deposition, cleaning, and etching tools, which are used to make advanced logic and memory chips. TEL has been a leader in developing process equipment for chips smaller than 5nm, helping chipmakers improve power efficiency and performance. It is also heavily involved in gate-all-around (GAA) transistors, a new chip technology that will be essential for future semiconductor generations. With a strong global presence and key partnerships, TEL continues to play an important role in pushing semiconductor technology forward.

Top strategies used by the key market participants

Technological Innovation and R&D Investment

The semiconductor market is constantly evolving, and companies must invest heavily in research and development (R&D) to stay ahead. ASML, Applied Materials, and Tokyo Electron Limited (TEL) all spend billions of dollars to create new and improved semiconductor equipment. For example, ASML is working on High-NA EUV lithography, which will allow chipmakers to make even smaller and more powerful chips. Applied Materials and TEL are also focusing on new materials and manufacturing processes to help create faster and more efficient semiconductors. By constantly innovating, these companies ensure that they remain essential to the semiconductor market.

Strategic Partnerships and Collaborations

Collaboration is an important strategy for semiconductor equipment companies. They work with leading chipmakers, universities, and governments to develop new technologies. ASML partners with TSMC, Samsung, and Intel to improve lithography machines. Applied Materials collaborates with chip manufacturers to create advanced transistor designs, such as gate-all-around (GAA) transistors. These partnerships help accelerate the development of next-generation chips while also ensuring a steady demand for semiconductor equipment. By working together, companies can develop better technologies faster and gain a competitive advantage.

Expansion of Global Manufacturing and Supply Chains

To reduce risks and meet the growing demand for semiconductor equipment, companies are expanding their manufacturing capabilities in different regions. ASML is increasing its production in Europe to ensure steady supplies, despite political and trade tensions. Applied Materials and TEL are investing in new factories in the U.S., Japan, and Taiwan to increase their manufacturing capacity. By expanding their operations globally, these companies lower their dependency on any single region and make their supply chains more resilient against unexpected disruptions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the global semiconductor equipment market include Tokyo Electron Limited (Japan),Lam Research Corporation (US),ASML (Netherlands),Applied Materials, Inc. (US)KLA Corporation (US),SCREEN Holdings Co., Ltd. (Japan),Teradyne, Inc. (US) ,Advantest Corporation (Japan)Hitachi, Ltd. (Japan) Plasma-Therm (US).

The semiconductor equipment market is highly competitive because it requires constant innovation, high investments, and compliance with strict regulations. A few companies dominate the market, including ASML, Applied Materials, and Tokyo Electron Limited (TEL). These companies have an advantage because of their advanced technology and long-term relationships with leading chip manufacturers. For example, ASML is the only company that provides extreme ultraviolet (EUV) lithography machines, making it indispensable to TSMC, Intel, and Samsung.

To stay competitive, companies focus on innovation, mergers, acquisitions, and global expansion. They invest heavily in R&D to develop next-generation chipmaking technologies, such as High-NA EUV, gate-all-around (GAA) transistors, and 3D chip packaging. They also form partnerships with semiconductor manufacturers and governments to secure long-term contracts and financial support.

Another challenge in the market is geopolitical tensions. Trade restrictions between the United States and China have made it harder for companies to sell semiconductor equipment to certain markets. Export controls on advanced chipmaking machines have forced companies to find new customers and expand their manufacturing to different regions. Additionally, new semiconductor companies in China and South Korea are entering the market, making competition even tougher. Overall, the semiconductor equipment market remains a fast-changing and highly competitive field.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, South Korea announced plans to secure 10,000 high-performance Graphics Processing Units (GPUs) to strengthen its AI computing infrastructure. This initiative aims to enhance the country's competitiveness in AI development and semiconductor manufacturing.

- In December 2024, the U.S. Department of Commerce implemented new export controls restricting China's access to 24 types of semiconductor manufacturing equipment and AI chip components. These measures aim to curb China's advancements in AI and semiconductor technology.

MARKET SEGMENTATION

This research report on the Semiconductor Equipment Market has been segmented and sub-segmented into the following categories.

By Front-end Equipment

-

Lithography

- DUV Lithography

- EUV Lithography

- Wafer Surface Conditioning

- Etching

- Chemical Mechanical Planarization (CMP)

- Wafer Cleaning

- Single-wafer Spray System

- Single-wafer Cryogenic System

- Batch Immersion Cleaning System

- Batch Spray Cleaning System

- Scrubber

- Deposition

- PVD

- CVD

Other Front-end Equipment

By Back-end Equipment

- Assembly and Packaging

- Dicing

- Metrology

- Bonding

- Wafer Testing/ IC Testing

By Fab Facility Equipment

- Automation

- Chemical Control

- Gas Control

- Other Fab Facility Equipment

By Product Type

- Memory

- Foundry

- Logic

- MPU

- Discrete

- Analog,

- MEMS

- Others

By Dimension

- 2D ICs

- 2.5D ICs

- 3D ICs

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What factors are driving the growth of the semiconductor equipment market?

The growth is driven by technological advancements such as 5G wireless technologies and artificial intelligence, leading to increased demand for high-performance, low-cost semiconductors.

What is the role of technological innovation in this market?

Technological innovation is crucial, with companies like ASML leading in advanced lithography systems essential for producing cutting-edge semiconductors.

What challenges are affecting the semiconductor equipment market?

Challenges include overcapacity in certain regions, geopolitical tensions leading to export controls, and dependency on foreign technologies for critical equipment components.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]