Global Sciatica Treatment Market Size, Share, Trends & Growth Forecast Report By Type (Acute and Chronic), Drug Class (Steroids, Antidepressants, Corticosteroids, Nonsteroidal Anti-Inflammatory Drugs (NSAIDs) and Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and Online Pharmacies) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Sciatica Treatment Market Size

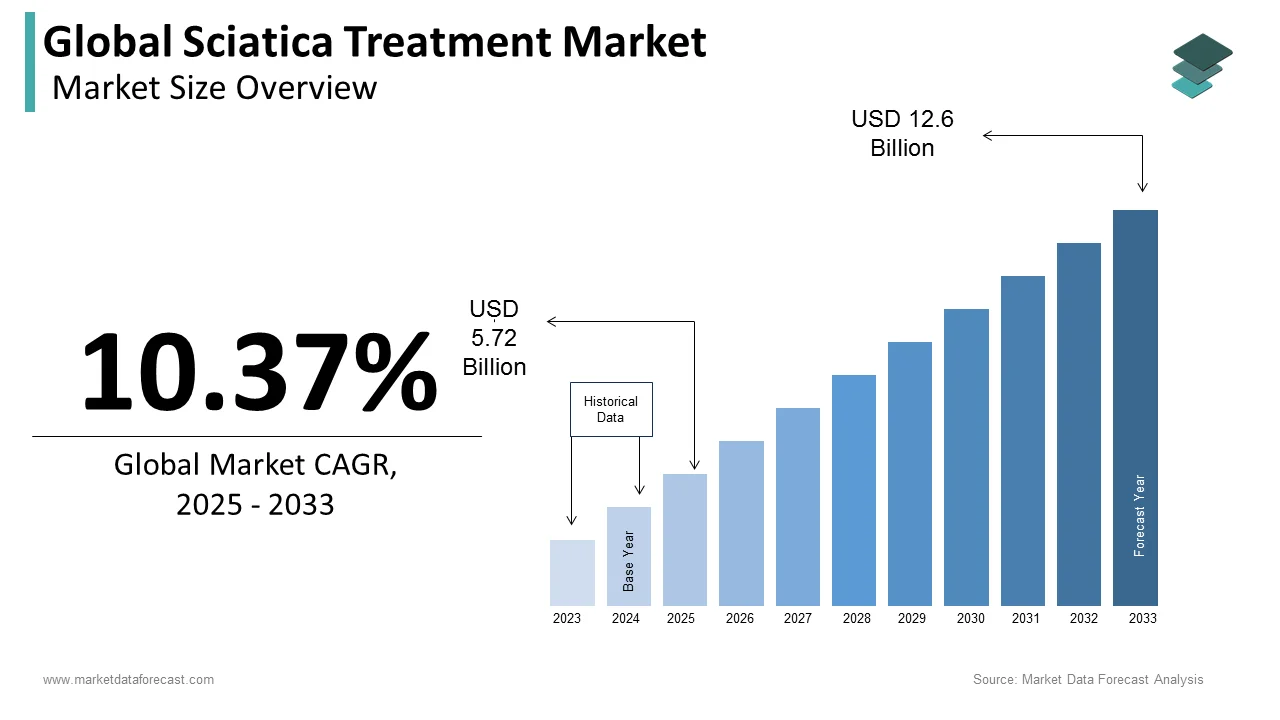

The global sciatica treatment market size was estimated at USD 5.18 billion in 2024 and is expected to be worth USD 5.72 billion in 2025 and USD 12.6 billion by 2033, growing a CAGR of 10.37% from 2025 to 2033.

The sciatica nerve extends from the buttocks down each leg. Sciatica is known to be the pain that travels along the path of the sciatica nerve. Sciatica mostly happens when a herniated disk or an overgrowth of bone puts pressure on the lumbar spine nerve roots. The most common symptom of sciatica is lower back pain, which radiates down the buttock and thigh bone; in severe cases, numbness and weakness are observed.

Sciatica occurs when irritation, inflammation, pinching, or compression affects one or more nerves that run from the lower back to the legs. Sciatica is not considered dangerous, and most people get better on their own with time and self-care treatments. However, severe cases may need surgery. Sciatica is a prevalent condition among people. About 40% of people in the U.S. experience some form of sciatica during their lifetime. It only happens before age 20 if it is injury-related. The sciatica treatment market has accounted for significant growth in the past years and is projected to have notable growth in the coming years. The rising prevalence of sciatica across the globe is a significant factor contributing to global market growth. According to the data published by the National Library of Medicine, the lifetime incidence of sciatica is reported to be between 10% to 40%, and the annual incidence is 1% to 5%. Technological advancements and ongoing research activities will provide growth opportunities for the sciatica treatment market during the forecast period.

MARKET DRIVERS

Rising Prevalence of Sciatica Cases Globally

According to an article published by Hindawi Limited in 2022, the annual incidence of an episode of sciatica ranges from 1.0% to 5,0% in the global population. The lifetime incidence varies from 13% to 40%. The rising incidence of herniated discs or overgrowth of spinal bone among people worldwide and the growing trauma cases leading to injuries are inducing sciatica, which enlarges the demand for sciatica treatment, leading to market share growth. The increasing adoption of over-the-counter drugs, which includes corticosteroids, opioids, and antidepressants for the treatment of mild to moderate sciatica pain, boosts the market revenue growth worldwide. The rising awareness among people regarding pain management and treatment options is enhancing the demand for sciatica treatment, fueling the market growth. According to data published by the Mayo Clinic in 2021, it was estimated that 80% of the U.S. population is expected to experience lower back pain at some point in their lives. The ongoing trend of non-invasive and minimally invasive procedures is estimated to positively impact the expansion of the sciatica treatment market due to rising demand for non-drug methods for sciatica pain. The growing geriatric population worldwide and rising chronic disease conditions will propel the market growth.

MARKET RESTRAINTS

The Complications Associated with Sciatica Surgical Treatment

Complications such as meningitis and epidural abscess limit the adoption of sciatica treatment. The high costs associated with sciatica treatment, rising healthcare costs, and hospital stays are all estimated to limit the adoption of surgical sciatica treatment, hindering the market size expansion. According to Cureus statistics published in November 2022, sciatica treatment accounts for significant medical expenses annually, which are USD 617.3 million in direct costs and almost USD 4.93 billion in indirect costs in the U.K. High costs regarding the research and development activities impede the market revenue growth. The availability of other treatment methods and limited adoption by healthcare professionals restrain the global market growth. The side effects associated with the drugs used in the treatment of sciatica and the need for awareness among people regarding pain management options hinder the market growth rate.

MARKET OPPORTUNITIES

The growing investments by the major market players in research and development activities to accelerate the innovations in sciatica treatment where these advancements are expected to be cost-effective with high efficacy therapeutics. These R&D investments will propel the market growth opportunities in the coming years. The growing technological advancements will enhance research activities and support sciatica pain management; the increasing healthcare expenditure in developing nations is estimated to create growth opportunities for the sciatica treatment market.

MARKET CHALLENGES

Stringent regulations regarding product approvals and launches challenge manufacturers in market expansion. Failures in the different phases of drug clinical trials will make manufacturers hesitate to invest in R&D activities, challenging the global market expansion.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

10.37% |

|

Segments Covered |

By Type, Drug Class, Distribution Channel and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Abbott Laboratories, Amneal Pharmaceuticals LLC, Bayer AG, Bristol Myers Squibb, Eliem Therapeutics, Novartis AG, Pfizer Inc, Scilex Holding, Sinfonia Biotherapeutics, Sorrento Therapeutics, Alkem Laboratories Limited, Aurobindo Pharma, Johnson and Johnson, Sun Pharmaceutical Industries Ltd, Teva Pharmaceutical Industries Limited, Zydus Group, SpineThera Inc, Vita Lifesciences LLC, Endo International plc, GSK plc, Glenmark Pharmaceuticals Ltd, Jubilant Life Sciences Ltd, Hikma Pharmaceuticals PLC, Mylan NV, Horizon Therapeutics Plc, SCILEX Pharmaceuticals Inc, Seikagaku Corporation and Kolon Life Science Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The chronic segment held the dominant share in the global sciatica treatment market in 2024 and is expected to grow at a notable CAGR during the forecast period due to the increased prevalence of chronic sciatica among the general population. The growing adoption of epidural injections and opioids to treat the disorder across the healthcare industry is driving the segment growth. According to a research study published by SpineThera, Inc., in September 2023, approximately 3.5 million lumbar transforaminal epidural injections were performed annually in the U.S. to manage sciatica pain. The prevalence of chronic sciatica varies widely, with study reports ranging from 1.6% to 43%. Various factors that induce chronic pain are sedentary lifestyles, the aging population, and rising incidence of conditions like herniated discs and spinal stenosis, which are majorly driving the segment growth. The growing trend towards conservative management involving non-invasive or minimally invasive treatments over surgical methods will boost segmental growth.

The acute segment is expected to have moderate growth during the forecast period due to increasing cases of lumbar disc herniation and nerve compression among the people.

By Drug Class Insights

The nonsteroidal anti-inflammatory drugs segment dominated the global sciatica treatment market and had a prominent share. The rising prevalence of lower back pain among people is enhancing the consumption of pain relievers for managing acute sciatica pain, which drives segment growth. As per the data published by Harvard Health in October 2020, about 15% of the U.S. population takes an NSAID regularly, and more than 30 billion doses are taken each year. NSAIDs will reduce the common symptoms of sciatica treatment, which is often prescribed as the first line of treatment for mild to moderate pain, which fuels the growth rate of the segment in the global market.

The corticosteroids segment is expected to grow significantly in the coming years due to rising demand for epidural steroid injections to treat chronic back pain. The increasing number of product launches by market players focusing on injectable steroids for pain management is boosting the segmental expansion.

By Distribution Channel Insights

The retail pharmacies segment held the largest share of the global market in 2024 and is estimated to grow at a prominent CAGR during the forecast period due to the presence of a wide distribution network. The increasing number of retail pharmacy stores globally, which are most preferred by people, is driving the segment growth. The easy availability and cost-effective presence of a range of medications for pain management across retail channels will boost segment expansion.

The online pharmacies segment is projected to grow the fastest due to the enlargement of the e-commerce sector around the world. The growing adoption of digital platforms, the availability of diverse brand and generic medications, and ease of payment are expected to propel the segment's growth in the coming years.

REGIONAL ANALYSIS

North American region dominated the global sciatica treatment market with a dominant share of 48.3% in 2023. The increasing awareness of sciatica management and the rising demand for prescribed drugs drive major regional markets. The escalating disease prevalence and presence of well-established healthcare systems across the region, crucial R&D activities in the U.S., and rising healthcare professionals across the region are boosting the market share of the North American region. According to Sorrento Therapeutics Inc., data published in 2021, annually, more than 40% of U.S. opioid prescriptions are for the treatment of Chronic Low Back Pain (CLBP).

The European region is expected to expand at a moderate growth rate during the forecast period. The growing prevalence of sciatica among the European population, the increasing number of sciatica patients, and the presence of advanced healthcare infrastructure are expected to enhance pain management services, leading to regional market expansion.

The Asia Pacific region is expected to grow fastest during the forecast period due to rising lower back problems among people across the region. The increasing government initiatives for clinical management and rising awareness among people regarding early diagnosis and pain management procedures will fuel the market growth in the region.

KEY MARKET PARTICIPANTS

Companies playing a noteworthy role in the global sciatica treatment market include Abbott Laboratories, Amneal Pharmaceuticals LLC, Bayer AG, Bristol Myers Squibb, Eliem Therapeutics, Novartis AG, Pfizer Inc, Scilex Holding, Sinfonia Biotherapeutics, Sorrento Therapeutics, Alkem Laboratories Limited, Aurobindo Pharma, Johnson and Johnson, Sun Pharmaceutical Industries Ltd, Teva Pharmaceutical Industries Limited, Zydus Group, SpineThera Inc, Vita Lifesciences LLC, Endo International plc, GSK plc, Glenmark Pharmaceuticals Ltd, Jubilant Life Sciences Ltd, Hikma Pharmaceuticals PLC, Mylan NV, Horizon Therapeutics Plc, SCILEX Pharmaceuticals Inc, Seikagaku Corporation and Kolon Life Science Inc.

RECENT HAPPENINGS IN THE MARKET

- In October 2023, Sollis Therapeutics, Inc. announced the phase 3 clinical trial study to evaluate the efficacy and safety of clonidine micropellets for treating pain associated with lumbosacral radiculopathy in adults.

- In November 2022, Sinfonia Biotherapeutics prepared its NeuRepair product SB0101 for clinical Phase IIb studies in sciatica. This development marks a significant step in advancing potential treatment options for sciatica.

- In May 2022, Sorrento Therapeutics announced the highly positive results of pivotal Phase 3 SEMDEXATM in sciatica patients following an epidural injection and presented the data at the annual American Society of Interventional Pain 2022 meeting.

- In August 2022, The Food and Drug Administration (FDA) authorized Olinvyk (oliceridine), an opioid agonist produced by Trevena, Inc., for the treatment of moderate to severe acute pain in adults.

- In July 2022, Vertex Pharmaceuticals Inc. announced plans to move the selective NaV1.8 inhibitor VX-548 into Phase 3 clinical trials to treat neuropathic pain.

MARKET SEGMENTATION

This research report on the global sciatica treatment market has been segmented and sub-segmented based on type, drug class, distribution channel and region.

By Type

- Acute

- Chronic

By Drug Class

- Steroids

- Corticosteroids

- Antidepressants

- Nonsteroidal Anti-Inflammatory Drugs (NSAIDs)

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]