Global Pesticide Intermediates Market Size, Share, Trends, And Growth Forecasts Report – Segmented By Product Type (Chemical Pesticide And Bio-Pesticide), Application (Insecticide, Bactericide, Weeding And Others) And By Region (North America, Latin America, Asia Pacific, Europe, Middle East and Africa) - Industry Analysis From 2025 to 2033

Global Pesticide Intermediates Market Size

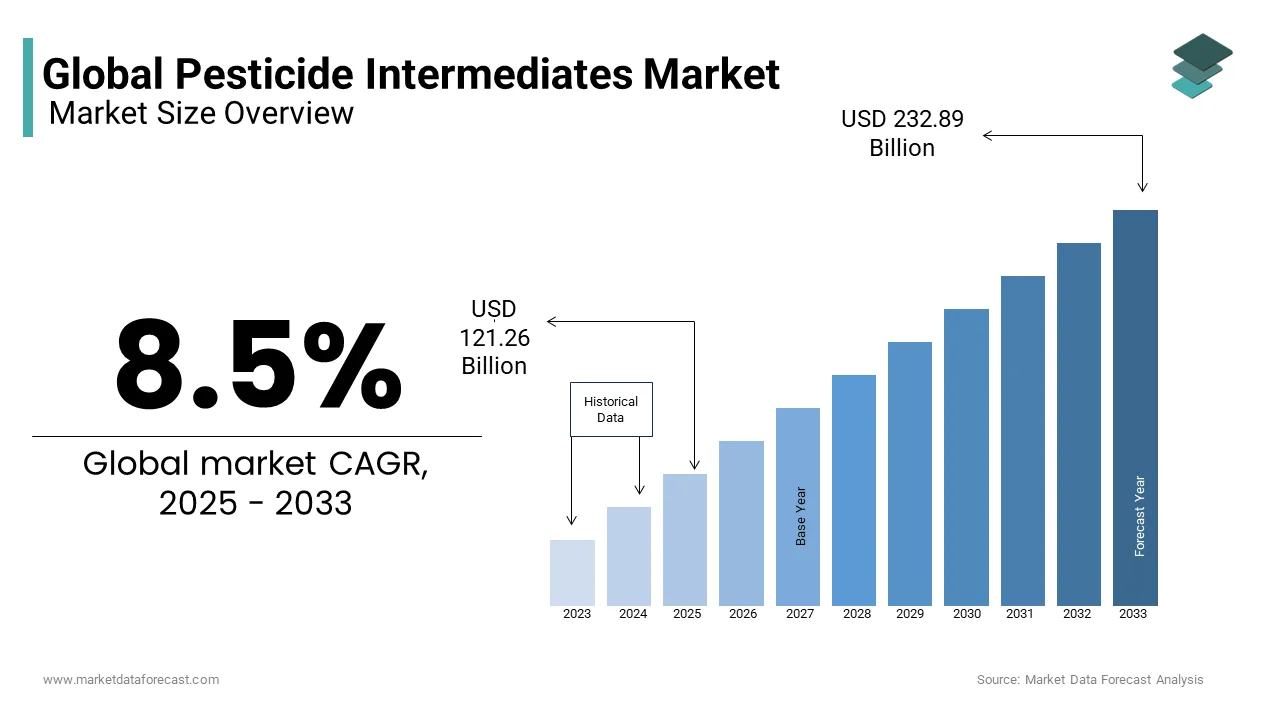

The global pesticide intermediates market was valued at USD 111.76 billion in 2024 and is anticipated to reach USD 121.26 billion in 2025 from USD 232.89 billion by 2033, growing at a CAGR of 8.5% during the forecast period from 2025 to 2033.

Pesticide intermediates are foundational building blocks for the synthesis of pesticides. These chemical compounds play an indispensable role in enhancing crop yields by controlling pests, diseases, and weeds, thereby ensuring food security on a global scale. The pesticide intermediates are anticipated to experience steady demand over the forecast period due to the increasing agricultural activities, population growth, and the rising demand for high-quality food. According to the United Nations Environment Programme (UNEP), over 60% of global agricultural practices are shifting toward eco-friendly solutions, positioning bio-pesticide intermediates as a key growth driver. This trend has significantly impacted the chemical pesticide segment, which remains dominant but faces increasing scrutiny due to environmental concerns. For instance, according to Statista, the use of bio-pesticide intermediates increased by 15% in 2022 alone, which is reflecting a shift toward greener alternatives. Additionally, advancements in biotechnology and chemical engineering have enhanced the efficiency and specificity of pesticide intermediates, which is further bolstering their adoption.

MARKET DRIVERS

Increasing Global Food Demand

The escalating global population has intensified the demand for food production, which is driving the need for effective pest management solutions. Pesticide intermediates, which form the backbone of modern agrochemicals, are essential for protecting crops from pests and diseases. A study by the World Health Organization (WHO) reveals that pest infestations cause up to 40% of global crop losses annually, underscoring the critical role of pesticide intermediates in mitigating these losses. In 2022, North America reported a 12% increase in the use of pesticide intermediates for high-value crops such as corn and soybeans. This driver underscores the importance of pesticide intermediates in ensuring food security and meeting the dietary needs of a growing population.

Advancements in Agricultural Biotechnology

Advancements in agricultural biotechnology have significantly influenced the pesticide intermediates market. Innovations in bio-pesticide intermediates that are derived from natural sources such as plant extracts and microorganisms, have gained traction due to their eco-friendly properties and reduced environmental impact. As per a report by the European Biotechnology Industry Association, bio-pesticide intermediates accounted for 25% of new product launches in 2022, particularly in regions like Europe and Asia Pacific. Additionally, precision farming technologies have enabled the targeted application of pesticide intermediates, which is reducing waste and enhancing efficacy. For instance, India reported a 20% increase in bio-pesticide intermediate usage in organic farming during the same period. This driver emphasizes the role of technological innovation in shaping the future of pest management.

MARKET RESTRAINTS

Stringent Environmental Regulations

Stringent environmental regulations governing the use of chemical pesticides pose a significant restraint for the pesticide intermediates market. Many countries have implemented strict guidelines to minimize the ecological impact of agrochemicals, including restrictions on the use of certain hazardous intermediates. A study by the European Chemicals Agency, over 30% of chemical pesticide intermediates face potential bans or phase-outs due to their adverse effects on biodiversity and water quality. This restraint is particularly evident in regions like Europe, where the EU’s Green Deal aims to reduce pesticide usage by 50% by 2030. For instance, Germany reported a 10% decline in chemical pesticide intermediate sales following the introduction of stricter regulations. This challenge underscores the need for manufacturers to develop safer and more sustainable alternatives.

High Production Costs and Price Volatility

High production costs and price volatility of raw materials pose another significant restraint for the pesticide intermediates market. Fluctuations in the prices of petrochemical derivatives and natural gas, which are critical inputs for chemical synthesis, have led to increased production expenses. A report by the U.S. Energy Information Administration reveals that global natural gas prices surged by 25% in 2022, impacting the affordability of pesticide intermediates for manufacturers. This restraint is particularly evident in developing regions like Latin America and Africa, where economic instability exacerbates price sensitivity. Additionally, logistical challenges caused by geopolitical tensions have delayed raw material procurement, further straining production schedules. For instance, Brazil experienced a 15% decline in pesticide intermediate imports during the first half of 2022. This challenge highlights the need for cost-effective production methods and stable sourcing strategies.

MARKET OPPORTUNITIES

Growing Adoption of Bio-Pesticides

The growing adoption of bio-pesticides presents a significant opportunity for the pesticide intermediates market. Bio-pesticides that are derived from natural sources such as plant extracts and microorganisms are gaining popularity due to their eco-friendly properties and reduced environmental impact. As per a study by the Indian Council of Agricultural Research, bio-pesticide intermediates accounted for 30% of new product launches in 2022, with a particular focus on organic farming and integrated pest management. This trend is particularly prominent in Asia Pacific, where countries like China and India are investing heavily in sustainable agriculture. For instance, China reported a 25% increase in bio-pesticide intermediate production during the same period. This opportunity underscores the potential for manufacturers to innovate and diversify their product portfolios to meet evolving consumer needs.

Expansion into Emerging Markets

The expansion of pesticide intermediates into emerging markets offers immense growth potential due to the rising agricultural activities and government initiatives to boost food production. According to a report by the Brazilian Agricultural Research Corporation, pesticide intermediate usage in Latin America increased by 18% in 2022, particularly in countries like Brazil and Argentina, which are major exporters of soybeans and maize. Additionally, the Middle East and Africa are witnessing increased investments in agricultural infrastructure, creating new avenues for market penetration. For instance, Kenya reported a 20% surge in pesticide intermediate imports for horticultural crops during the holiday season. This opportunity emphasizes the importance of aligning production practices with regional demands to capitalize on the growing agricultural sector.

MARKET CHALLENGES

Intense Competition from Alternative Pest Control Methods

The pesticide intermediates market faces stiff competition from alternative pest control methods such as biological controls, crop rotation, and genetically modified organisms (GMOs). These substitutes are gaining popularity due to their perceived safety and sustainability. According to a study by the Canadian Food Inspection Agency, alternative pest control methods accounted for 40% of new agricultural practices in 2022. This competition has fragmented the market, making it challenging for traditional pesticide intermediate manufacturers to maintain their share. For instance, Australia reported a 12% decline in chemical pesticide intermediate sales in favor of biological controls. This challenge underscores the need for differentiation through branding, quality, and innovation to sustain competitive advantage.

Public Perception and Resistance to Chemical Pesticides

Public perception and resistance to chemical pesticides pose significant hurdles for the pesticide intermediates market. Growing awareness of the health risks associated with chemical residues in food has led to increased consumer skepticism and regulatory scrutiny. According to the Swedish Environmental Research Institute, pesticide intermediate usage in Europe declined by 8% in 2022 following negative publicity about their environmental and health impacts. Additionally, farmers in developed regions are increasingly adopting organic farming practices, reducing reliance on chemical intermediates. For instance, Denmark reported a 10% decline in pesticide intermediate sales following campaigns promoting organic agriculture. This challenge emphasizes the importance of addressing public concerns and aligning with sustainable practices.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.5% |

|

Segments Covered |

By Product, Application, and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Syngenta AG, Bayer, Dow AgroSciences, Monsanto Company, BASF SE,E. I. du Pont de Nemours and Company, ADAMA Agricultural Solutions Ltd, Nufarm Ltd, FMC Corporation, Lanxess, and Others. |

SEGMENT ANALYSIS

By Product Type

The chemical pesticide segment dominated the market by holding the most significant share of the global market in 2024 owing to their widespread use in conventional agriculture. Chemical pesticides are effective and cost-efficient. North America and Asia Pacific are the largest contributors to this segment, with combined sales exceeding $8.5 billion. As per a report by the U.S. Department of Agriculture, chemical pesticide intermediates are particularly popular in high-value crops such as corn, soybeans, and cotton, representing 50% of their total usage.

The bio-pesticide segment is estimated to grow at a notable CAGR of 8.2% over the forecast period owing to the increasing adoption of bio-pesticides in organic farming and integrated pest management. As per a study by the Swiss Organic Agriculture Association, bio-pesticide intermediates accounted for 25% of new formulations in 2022. The potential of bio-pesticides to tap into the booming sustainable agriculture market, particularly in regions like Europe and Asia Pacific, is also contributing to the expansion of the segment in the global market.

By Application

The insecticides segment accounted for 45.5% of the global market share in 2024. The domination of the insecticides segment is driven by their critical role in controlling crop-damaging insects. As per a report by the Indian Council of Agricultural Research, insecticide intermediates are predominantly used in high-value crops such as rice, wheat, and vegetables, representing 40% of their total usage. The ability of insecticides to meet the demands of diverse agricultural practices while maintaining consistent efficacy is likely to boost the segmental expansion in the market during the forecast period.

The wedding segment is predicted to grow at a CAGR of 7.5% over the forecast period. Factors such as the increasing adoption of herbicide-resistant crops and precision farming technologies are propelling the growth of the wedding segment in the global market. According to a study by the French Agricultural Research Institute, weeding intermediates accounted for 30% of new product launches in 2022.

REGIONAL ANALYSIS

Asia-Pacific led the pesticide intermediates market by accounting for 36.3% of the global market share in 2024. The dominance of Asia-Pacific in the global market is attributed to its vast agricultural base and high demand for food production, particularly in countries like China and India. According to the Chinese Ministry of Agriculture, pesticide intermediates are a staple in rice and wheat cultivation, representing 50% of their total usage.

North America held a substantial share of the global market in 2024 and is projected to progress at a notable CAGR during the forecast period. The growth of North American market is majorly attributed to its advanced agricultural practices and high-value crops. A report by the U.S. Department of Agriculture reveals that corn and soybean farming alone accounts for 40% of national sales.

Europe is a prominent regional market for pesticide intermediates. The strong emphasis on sustainable and eco-friendly solutions in Europe is driving the European market growth. European consumers spend an average of €15 annually on bio-pesticide intermediates, reflecting their affinity for high-quality ingredients.

Latin America holds a substantial share of the global market owing to the focus on export-oriented crops such as soybeans and coffee. Brazilian farmers prioritize cost-effectiveness and yield enhancement, making it a key market for pesticide intermediates.

The Middle East and Africa is renowned for their high adoption of pest control solutions in horticulture. Kenyan consumers exhibit a strong preference for bio-pesticide intermediates, driving segment growth.

KEY MARKET PLAYERS

Syngenta AG, Bayer, Dow AgroSciences, Monsanto Company, BASF SE, E. I. du Pont de Nemours and Company, ADAMA Agricultural Solutions Ltd, Nufarm Ltd, FMC corporation, Lanxess. Some of market players dominate the global pesticide intermediate market.

MARKET SEGMENTATION

This market research report on the global Pesticide Intermediates Market is segmented and sub-segmented into the following categories:

By Product Type

- Chemical pesticide

- Bio-pesticide

By Application

- Insecticide

- Bactericide

- Weeding and others

By Region

- North America

- Latin America

- Asia-Pacific

- Middle East and Africa

- Europe

Frequently Asked Questions

What is the current market size of the global pesticides market?

The current market size of the global pesticide intermediates market was valued at USD 121.26 billion in 2025

What kind of market drivers are driving the global pesticides market?

Pesticide intermediates are vital substances used for the production of active ingredients used in the formulation of pesticides. Hence, extensive demand for agricultural products is driving the pesticide intermediate market.

Who are the market players that are dominating the global pesticides market?

Syngenta AG, Bayer, Dow AgroSciences, Monsanto Company, BASF SE, E. I. du Pont de Nemours and Company, ADAMA Agricultural Solutions Ltd, Nufarm Ltd, FMC corporation, Lanxess. These are the market players that dominate the global pesticide intermediate market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]