Global Pain Management Devices Market Size, Share, Trends, Growth Analysis Report – Segmented By Device Type ( Neurostimulation Devices , Ablation Devices ), Application, Mode of Purchase and Region - Industry Forecast (2025 to 2033)

Global Pain Management Devices Market Size

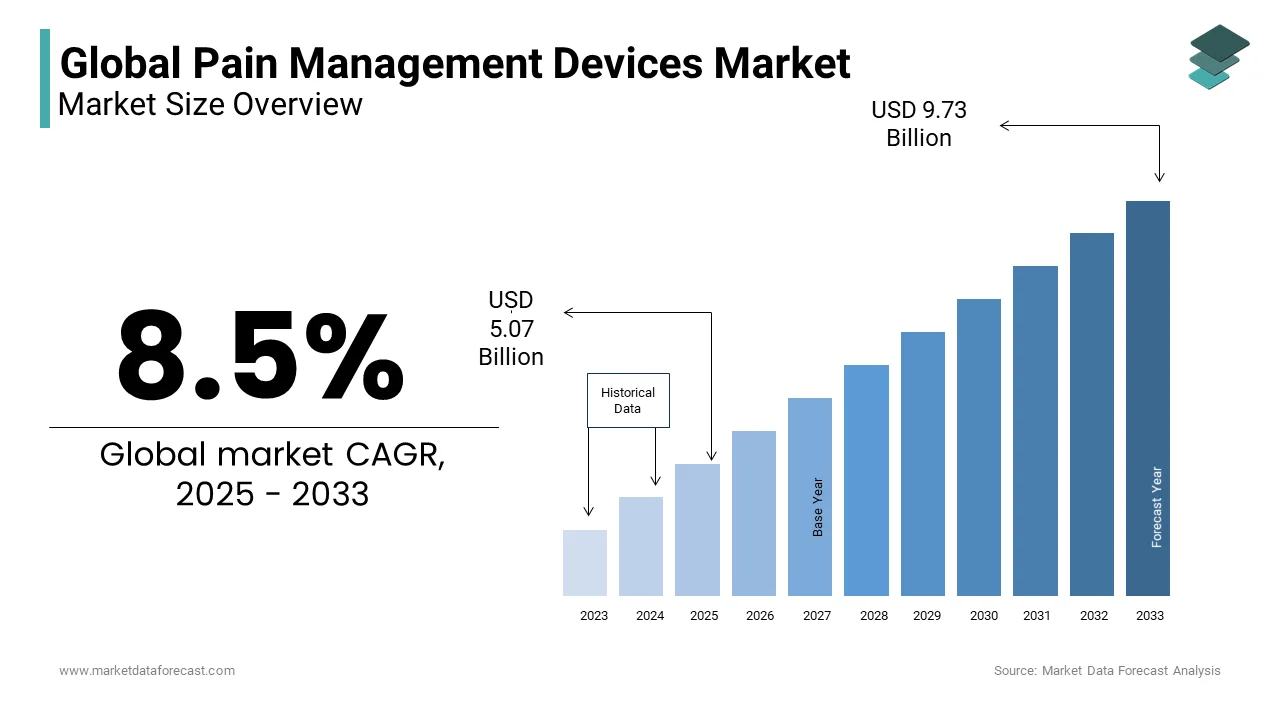

In 2024, the global pain management devices market was valued at USD 4.67 billion and it is expected to reach USD 9.73 billion by 2033 from USD 5.07 billion in 2025, growing at a CAGR of 8.5 % during the forecast period.

Pain management is the branch of medical science that deals with minimizing patients' pain. The global market will witness an uptrend in growth rate and revenue due to technological advancements. Furthermore, more companies entering the market with advanced solutions ensure that more devices are available for better pain management.

MARKET DRIVERS

The growing patient population suffering from chronic pain is majorly propelling the pain management devices market growth.

An estimated one person in every five people, or approximately 1.5 billion adults worldwide, is suffering from chronic pain. As per the statistics published by the Centers for Disease Prevention and Control (CDC), an estimated 50 million adults or 20.4% of the adult population in the U.S., suffer from chronic pain. According to the data published by the European Pain Federation, an estimated 100 million people in the European region are suffering from chronic pain. The incidence of chronic pain can be seen more in women compared to men. As per the data published by the American Academy of Pain Medicine, the incidence of chronic pain conditions such as fibromyalgia, rheumatoid arthritis, and chronic fatigue syndrome is high among women compared to men. The patient count suffering from chronic pain has gradually grown over the last few years. The demand for non-pharmacological pain management options such as pain management devices has grown significantly in recent years due to the increasing awareness among people regarding the risks associated with the long-term use of opioids and other pain medications.

The growing demand for minimally invasive surgeries is further fuelling the pain management devices market growth.

The usage of pain management devices in minimally invasive surgeries offers improved patient outcomes and satisfaction. Patient-controlled analgesia (PCA) pumps, transcutaneous electrical nerve stimulation (TENS) units and peripheral nerve blocks are some of the most used pain management devices in minimally invasive surgeries. In recent years, the usage of pain management devices has also been promoted in minimally invasive surgeries by healthcare policies and regulations around limiting the usage of opioids and increasing the adoption of alternative pain management methods. For instance, the Centers for Medicare and Medicaid Services (CMS) in the U.S. included policies to promote the usage of alternative pain management options to reduce the usage of opioids for patients undergoing surgeries.

In addition, the rapid adoption of technological developments to develop new and advanced pain management devices such as neurostimulation devices, radiofrequency ablation devices, and others contributes to the growth of the pain management devices market. Factors such as increasing awareness among patients and healthcare providers regarding the benefits of pain management devices in developing and underdeveloped countries, favorable reimbursement policies for pain management devices in several countries, and increasing healthcare expenditure are propelling the growth of the pain management devices market. Owing to the growing adoption of remote patient monitoring, home healthcare and telemedicine, the demand for pain management devices is growing as these devices allow greater flexibility and convenience. The demand for pain management devices is further fuelled by the growing number of surgeries being performed worldwide, as these devices are effectively used in pain management procedures during and after the surgeries.

Furthermore, factors such as increasing demand for portable and wearable pain management devices, growing adoption of pain management devices in developing regions, rising usage of combination therapies and growing emphasis on patient-centric care are promoting the growth of the pain management devices market.

MARKET RESTRAINTS

The stringent regulatory environment for pain management devices is one of the key factors hampering the market growth.

Due to this, many manufacturers of pain management devices are hesitating to launch their products into the market considering the high costs involved with the development and approval process. The high costs of pain management devices are another notable factor limiting the adoption of these devices and hindering the market’s growth rate. Poor awareness levels regarding the benefits of pain management devices among patients and healthcare providers in many countries are another notable obstacle to the growth of the pain management devices market. Side effects associated with using pain management devices are limiting the adoption of these devices and showcasing a negative impact on the market growth. Unfavorable reimbursement policies for pain management devices are further impeding market growth. In addition, factors such as limited efficacy, the presence of alternative treatment methods, patient preferences, technical limitations and resistance from healthcare providers in some countries to adopt pain management devices are further inhibiting the market’s growth rate.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.5 % |

|

Segments Analysed |

By Device Type, Application, Mode of Purchase, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Analysed |

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

|

Market Leader Profiled |

St. Jude Medical, Inc., Boston Scientific Corporation, Medtronic plc, Baxter International |

SEGMENTAL ANALYSIS

By Device Type Insights

The neurostimulation devices segment held the major share of the global pain management devices market and is predicted to continue holding the leading share of the worldwide market during the forecast period. Spinal cord stimulators (SCS), deep brain stimulators (DBS), and sacral neurostimulators are some of the most used neurostimulation devices for pain management. The segment's growth is majorly driven by its ability to stimulate the spinal cord, deep brain, sacral nerve, vagus nerve, and respiratory electrical stimulation. Neurostimulation devices are more efficient than traditional methods of reducing pain, which is one of the key factors boosting the adoption of these devices and contributing to the growth of the segment. In addition, the increasing adoption of neurostimulation devices and the rising patient population suffering from chronic diseases are propelling segmental growth.

Due to their extensive usage in chronic pain management, the radiofrequency ablation devices segment is projected to grow in the years to come at the fastest rate as it prevents the flow of pain signals to the brain without affecting tissues. The growing adoption of radiofrequency ablation devices in cancer treatment procedures is majorly accelerating segmental growth.

The analgesic Infusion pumps segment is expected to witness a notable growth rate during the forecast period. The growing number of surgeries being performed worldwide is one of the key factors propelling the segmental growth. The benefits of analgesic infusion pumps such as infections, device malfunction, and over- or under-dosing of medication is another major factor promoting the growth rate of the segment.

By Application Insights

The neuropathic pain segment is estimated to hold the largest share of the global pain management devices market during the forecast period. The rising usage of pain management devices such as spinal cord stimulators or peripheral nerve stimulators to treat neuropathic pain is majorly driving the growth of the segment. The growing need for effective pain management options including pain management devices for neuropathic pain is another notable attribute contributing to the segmental growth. During the forecast period, the neuropathic pain segment is expected to register the fastest CAGR.

The cancer pain segment is one of the most lucrative and is projected to witness a healthy CAGR in the coming years. Radiofrequency ablation devices play an essential role in the management of cancer pain. These devices act through high-temperature thermal therapy, which heating tissue to 100°C induces the coagulation of necrotic cells. The RFA device helps kill cancer cells, allowing effective pain relief.

The musculoskeletal pain segment is anticipated to hold a considerable share of the global market during the forecast period. The growing aging population and increasing adoption of sedentary lifestyles are the major reasons behind the growing incidence of musculoskeletal pain among people. Patients and healthcare providers are employing various options including pain management devices for the management of musculoskeletal pain, which is resulting in segmental growth. In addition, the rising adoption of non-invasive or minimally invasive surgical treatments for musculoskeletal pain is promoting the growth rate of the segment.

By Mode of Purchase Insights

Based on the mode of purchase, the over-the-counter segment held the leading share of the global pain management devices market in 2023 and the domination of the segment is predicted to continue during the forecast period. The growth of the segment is majorly driven by the advantages associated with the over-the-counter segment, such as convenience, affordability, and self-treatment preference. The over-the-counter pain management devices are non-invasive and do not require the supervision of a healthcare provider to use for the need, which is another major factor propelling the segmental growth.

On the other hand, the prescription segment is predicted to hold a considerable share of the worldwide market during the forecast period. The higher efficacy, safety, and customization to a patient's specific pain condition of prescription-based devices are majorly contributing to the growth of the segment.

REGIONAL ANALYSIS

The North American region dominated the pain management devices market in 2023 and the domination of the regional market is likely to continue during the forecast period owing to the growing adoption of the devices among healthcare professionals and people the availability of well-established healthcare infrastructure. In addition, good medical support that facilitates advanced pain management equipment access contributes to regional market growth. Also, government initiatives such as precision medicine and affordable care laws, coupled with carefully planned reimbursement policies, led to the North American market growth. Furthermore, increasing awareness and high purchasing power parity fuel the market’s growth rate.

Europe is expected to grow at a promising CAGR during the forecast period. The increasing geriatric population and the high quality of healthcare facilities are the main positive contributing factors to the market.

Asia-Pacific is expected to grow rapidly due to the large aging population in this region. The regional market growth is primarily driven by the increasing government support to improve healthcare infrastructure. In addition, with their healthcare facilities, India and China's increasing population and high disposable incomes will help this region grow.

Latin America is expected to hold a considerable share of the global market during the forecast period. The growing awareness regarding the available options for pain management is anticipated to play a significant role in promoting market growth in Latin America. Currently, the Latin American region lacks specialized pain clinics and trained pain management professionals, limiting the market’s growth rate. However, the conditions are changing in the Latin American region, and improvements are emerging, which are expected to result in regional market growth during the forecast period.

The MEA is expected to showcase a steady CAGR in the coming years.

KEY MARKET PLAYERS

Some major companies leading the global pain management devices market are St. Jude Medical, Inc., Boston Scientific Corporation, Medtronic plc, Baxter International, Stryker Corporation, Pfizer, Codman and Shurtleff, B Braun Melsungen AG, and DJO Global LLC.

RECENT HAPPENINGS IN THIS MARKET

- In September 2020, WaveWriter Alpha Spina Cord Stimulator Systems was launched by Boston Scientific to personalize pain relief.

- In June 2020, Abbott agreed to a partnership with Tandem Diabetics care to develop integration diabetics solutions.

- In June 2020, a tool was launched by Boston Scientific to monitor the effect of radiofrequency energy delivery over the cardiac ablation processes known as DIRECTSENSE.

- In May 2015, St. Jude Medical, Inc. purchased Spinal Modulation, Inc., an Axium Neurotransmitter system developer targeting a neuronal structure in the spine, to expand its product portfolio in pain management products.

MARKET SEGMENTATION

This research report on the global pain management devices market has been segmented based on the device type, application, mode of purchase, and region.

By Device Type

- Neurostimulation Devices

- Transcutaneous Electrical Nerve Stimulation devices

- Spinal Cord Stimulation devices

- Ablation Devices

- Radiofrequency Ablation Devices

- Cryo Ablation Devices

- Analgesia Infusion Pumps

- Intrathecal Infusion Pumps

- External Infusion Pumps

By Application

- Neuropathic Pain

- Facial Pain

- Migraine

- Musculoskeletal Pain

- Cancer Pain

- Others

By Mode of Purchase

- Counter Purchase

- Prescription Based Purchase

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How much was the global pain management devices market worth in 2024?

The APAC region is anticipated to grow at the fastest CAGR in the global market during the forecast period.

Which region is growing the fastest in the global pain management devices market?

St. Jude Medical, Inc., Boston Scientific Corporation, Medtronic plc, Baxter International, Stryker Corporation, Pfizer, Codman and Shurtleff, B Braun Melsungen AG, and DJO Global LLC. are some of the noteworthy companies in the pain management devices market.

What are pain management devices?

Pain management devices are medical tools designed to alleviate chronic or acute pain. These devices include TENS units, neurostimulators, analgesic infusion pumps, and RF ablation devices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]