North America Vacuum Insulated Pipe Market Size, Share, Trends & Growth Forecast Report By Product (Standard, Customized), Application, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Vacuum Insulated Pipe Market Size

The Vacuum Insulated Pipe market size in North America was valued at USD 257.16 million in 2024 and is predicted to be worth USD 386.47 million by 2033 from USD 269.07 million in 2025 and grow at a CAGR of 4.63% from 2025 to 2033.

MARKET DRIVERS

Rising Demand for LNG Infrastructure

The escalating demand for liquefied natural gas (LNG) infrastructure is a primary driver for the vacuum insulated pipe market in North America. LNG is increasingly used as a cleaner alternative to coal and oil, particularly in power generation and transportation. According to the International Gas Union, global LNG trade reached 380 million tons in 2022, with North America emerging as a key exporter. The U.S., specifically, exported approximately 11.5 billion cubic feet per day of LNG in 2022, as per the U.S. Energy Information Administration. This surge necessitates advanced insulation systems, such as vacuum insulated pipes, to maintain cryogenic temperatures during storage and transport. These pipes minimize heat ingress by ensuring energy efficiency and cost savings.

Growth in Cryogenic Applications Across Industries

Another significant driver is the expansion of cryogenic applications across industries like pharmaceuticals, aerospace, and electronics. Cryogenics requires precise temperature control, which vacuum insulated pipes excel at providing. The pharmaceutical industry, for instance, relies on cryogenic storage for vaccines and biologics. Electronics manufacturing also benefits from cryogenic testing, which ensures component reliability. The Semiconductor Industry Association estimates that North America’s semiconductor market will grow by 10% annually through 2025. These trends collectively fuel the demand for vacuum insulated pipes by making them indispensable in modern industrial processes.

MARKET RESTRAINTS

High Initial Costs

One of the primary restraints impeding the growth of the vacuum insulated pipe market is the high initial costs associated with their production and installation. Vacuum insulated pipes are technologically advanced and require specialized materials, such as stainless steel and multilayer insulation, which significantly drive-up expenses. This financial barrier often deters small and medium-sized enterprises (SMEs) from adopting VIPs in price-sensitive industries like food and beverage. Additionally, the complexity of installation demands skilled labor that is increasing overall project costs.

Limited Awareness and Expertise

Another significant restraint is the limited awareness and technical expertise surrounding vacuum insulated pipes. Many end-users in emerging applications like electronic manufacturing and cryogenic testing are lack comprehensive knowledge about the benefits and operational nuances of VIPs. Only few industrial stakeholders in North America are familiar with the full range of applications for vacuum insulated pipes. This knowledge gap often leads to hesitation in adopting the technology that despite its proven advantages. Furthermore, the scarcity of trained professionals capable of designing and maintaining VIP systems adds another layer of complexity. Data from the U.S. Bureau of Labor Statistics indicates that the number of qualified technicians in advanced manufacturing has grown by just 5% annually, lagging behind the demand for specialized skills.

MARKET OPPORTUNITIES

Expansion in Renewable Energy Projects

The growing emphasis on renewable energy projects presents a significant opportunity for the vacuum insulated pipe market in North America. The technologies facilitating energy efficiency, such as vacuum insulated pipes as governments and private entities strive to meet sustainability goals are gaining traction. The U.S. Department of Energy allocated $9.5 billion in 2022 for hydrogen infrastructure development, as per their official announcements. Similarly, solar thermal energy plants, which utilize molten salts at high temperatures, benefit from VIPs' superior insulation properties.

Advancements in Cold Chain Logistics

The rapid evolution of cold chain logistics offers another promising avenue for vacuum insulated pipe adoption. The rise in e-commerce and the need for temperature-controlled supply chains have intensified demand for efficient cryogenic solutions. Vacuum insulated pipes play a crucial role in maintaining ultra-low temperatures for perishable goods, pharmaceuticals, and biologics. A study by Deloitte revealed that investments in North America grew by 18% in 2021 alone. Moreover, advancements in IoT-enabled monitoring systems enhance the functionality of VIPs, ensuring real-time tracking and optimization.

MARKET CHALLENGES

Stringent Regulatory Compliance

One of the foremost challenges facing the vacuum insulated pipe market is the stringent regulatory compliance required for their production and application. Vacuum insulated pipes must adhere to rigorous safety and environmental standards, which vary across industries and regions. According to the Environmental Protection Agency, non-compliance with federal regulations can result in fines exceeding $100,000 per violation. For instance, the pharmaceutical and food processing sectors demand adherence to Good Manufacturing Practices (GMP) and Hazard Analysis Critical Control Point (HACCP) protocols, as per the Food and Drug Administration. These requirements necessitate additional testing and certification processes, increasing operational costs and timelines. Furthermore, the lack of standardized guidelines for cryogenic applications creates ambiguity, complicating compliance efforts.

Intense Market Competition

Another significant challenge is the intense competition within the vacuum insulated pipe market owing to the presence of numerous players offering similar products. This competitive landscape often leads to price wars, which is eroding profit margins and hindering innovation. According to a study by Frost & Sullivan, the top five players in the North American VIP market collectively hold approximately 60% of the market share by leaving smaller companies struggling to gain visibility. Additionally, the influx of low-cost imports from Asia-Pacific nations, particularly China and India, exacerbates pricing pressures. The U.S. International Trade Commission reports that imports of industrial piping systems increased by 15% in 2022 by intensifying competition domestically. Furthermore, rapid technological advancements necessitate continuous R&D investments to stay ahead, which smaller firms often cannot afford.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

4.63% |

|

Segments Covered |

By Product, Application, and Region |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

The United States, Canada, Mexico, and Rest of North America |

|

Market Leaders Profiled |

Acme Cryogenics, Air Liquide SA, Chart Industries Inc., Cryeng Group Pty Ltd., Cryofab; Cryowork, Inc., Senior Flexonics; and TMK, and others |

SEGMENTAL ANALYSIS

By Product Insights

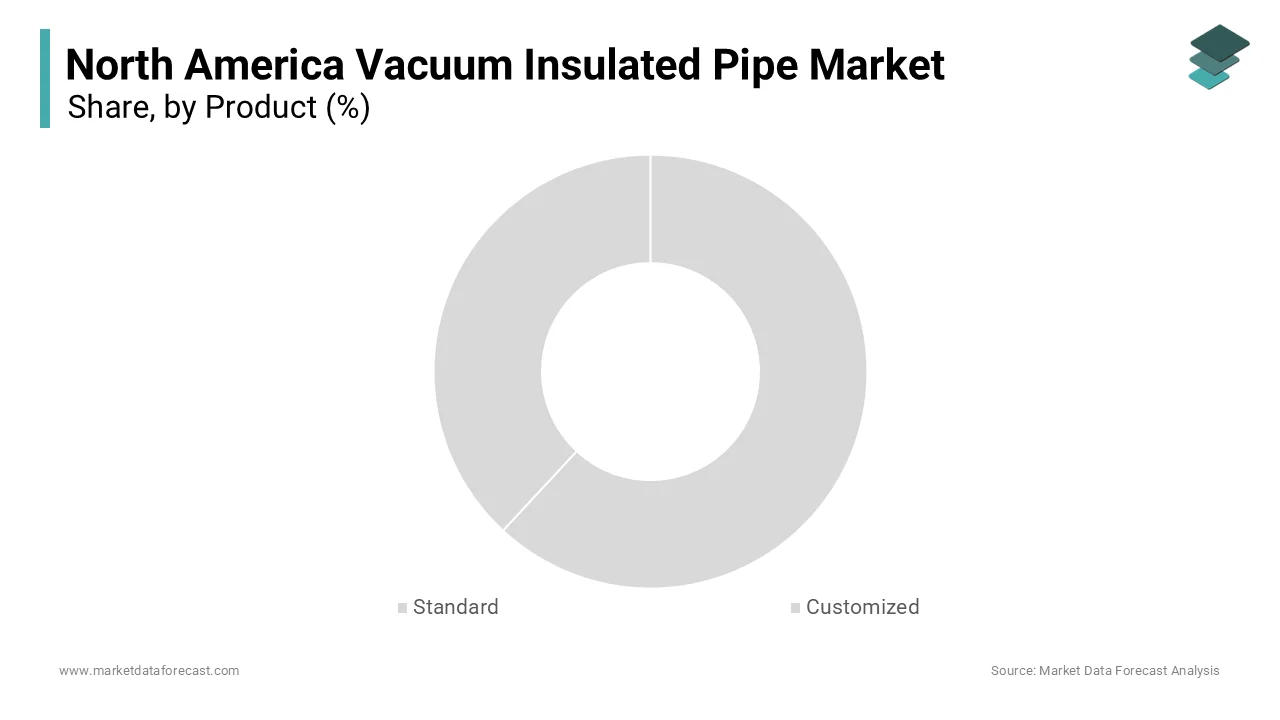

The standard vacuum insulated pipes segment dominated the North American market by accounting for 65.3% of the total share in 2024. Their widespread adoption stems from their versatility and cost-effectiveness compared to customized alternatives. Industries such as LNG and food processing favor standard pipes due to their compatibility with existing infrastructure and ease of installation. Additionally, the pharmaceutical sector, which relies heavily on cryogenic storage, prefers standard pipes for their proven reliability. A study by the Pharmaceutical Research and Manufacturers of America reveals that 70% of biologics manufacturers prioritize standard components to ensure seamless operations.

The customized vacuum insulated pipes segment is anticipated to register a CAGR of 8.5% throughout the forecast period. This growth is fueled by the increasing demand for tailored solutions in niche applications, such as aerospace and electronics manufacturing. According to NASA, the Artemis program requires specialized cryogenic piping systems capable of withstanding extreme conditions, driving customization needs. The flexibility offered by customized pipes allows for enhanced performance in complex environments, making them indispensable. Furthermore, advancements in additive manufacturing have reduced production lead times, making customization more accessible.

By Application Insights

The food and beverage sector was accounted in holding 40.3% of the North America vacuum insulated pipe market share in 2024 with the rising demand for cold chain logistics, driven by the proliferation of perishable goods and frozen foods. The U.S. Department of Agriculture states that frozen food sales in the U.S. grew by 20% in 2021 with the need for efficient cryogenic solutions. Vacuum insulated pipes ensure minimal thermal loss during storage and transport, preserving product quality and extending shelf life. Additionally, the increasing popularity of plant-based and organic products, which require precise temperature controls that further amplifies demand.

The aerospace sector is anticipated to grow with a projected CAGR of 9.2% in the next coming years. This growth is propelled by the increasing use of cryogenic fuels in space exploration and commercial aviation. These developments necessitate advanced cryogenic infrastructure by positioning aerospace as the segment with the highest growth potential.

REGIONAL ANALYSIS

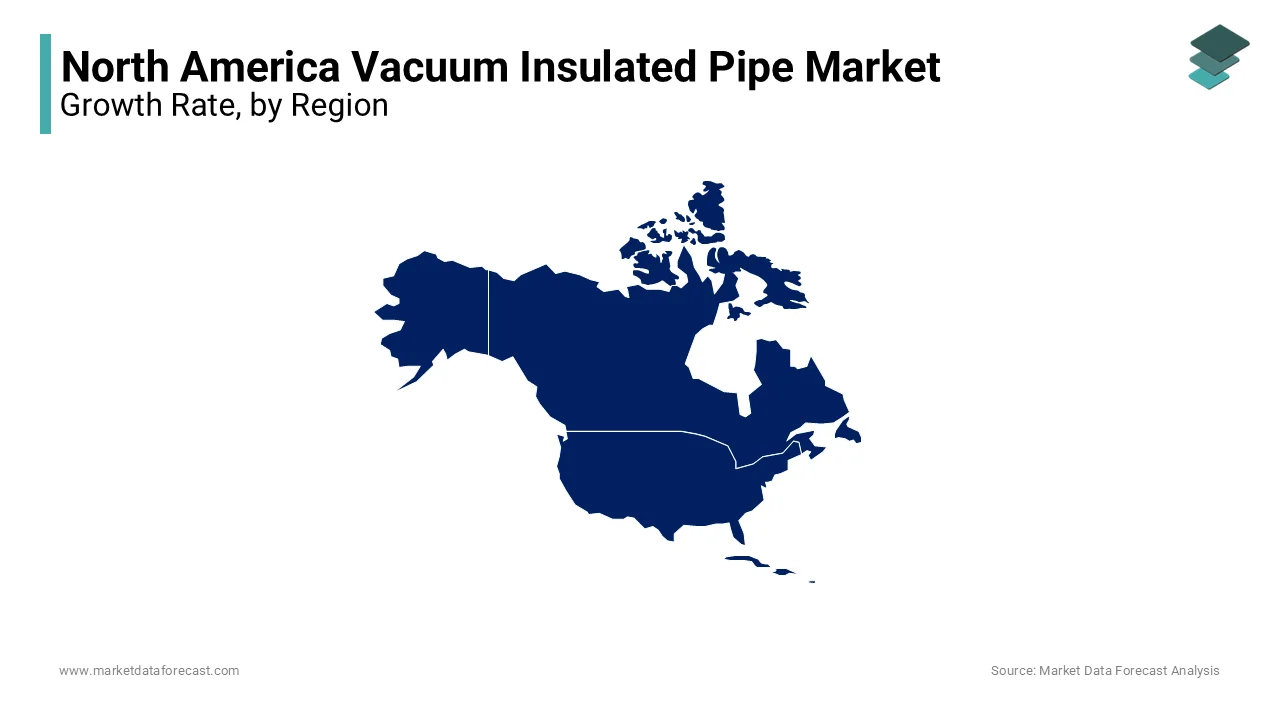

The United States was the top performer in the North American vacuum insulated pipe market with 70.4% of the share in 2024 with the country's advanced industrial infrastructure, robust energy sector, and significant investments in cryogenic applications. Vacuum insulated pipes are integral to maintaining cryogenic temperatures during LNG transport and storage by driving demand for these products. Furthermore, the pharmaceutical industry, which relies heavily on biologics and vaccines requiring precise temperature control, contributes significantly to the market's growth. Additionally, government initiatives promoting clean energy, including a $9.5 billion investment in hydrogen infrastructure announced by the U.S. Department of Energy, further fuel the adoption of vacuum insulated pipes.

Canada held 20.4% of the North American vacuum insulated pipe market share in 2024. Cryogenic fuels, essential for rocket propulsion systems, rely on vacuum insulated pipes to maintain ultra-low temperatures, thereby boosting demand for these solutions. Moreover, Canada’s commitment to renewable energy projects, with Natural Resources Canada allocating $15 billion to green initiatives, amplifies the need for efficient cryogenic infrastructure. The country’s strategic focus on hydrogen production and storage, as outlined in the Canadian Hydrogen Strategy, positions vacuum insulated pipes as critical components in achieving sustainability goals.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Acme Cryogenics, Air Liquide SA, Chart Industries Inc., Cryeng Group Pty Ltd., Cryofab; Cryowork, Inc., Senior Flexonics; and TMK are playing dominating role in the North America vacuum insulated pipe market.

The North American vacuum insulated pipe market is characterized by intense competition, with key players vying for dominance through innovation, quality, and strategic initiatives. Companies like Chart Industries, Cryofab, Inc., and Acme Cryogenics dominate the landscape, each leveraging unique strengths to capture market share. Chart Industries leads the pack with its extensive experience in cryogenic solutions and robust global network by allowing it to cater to large-scale projects in the LNG and hydrogen sectors. Cryofab, Inc., on the other hand, differentiates itself through its focus on customization, particularly in niche applications like aerospace and electronics manufacturing. Acme Cryogenics excels in providing cost-effective solutions tailored to the food and beverage industry, making it a preferred choice for budget-conscious customers.

TOP PLAYERS IN THE MARKET

Chart Industries

Chart Industries stands out as a dominant player in the North American vacuum insulated pipe market. The company’s expertise lies in providing cryogenic solutions tailored to industries such as LNG, pharmaceuticals, and aerospace. Its acquisition of SES Cryo Technologies in 2021 marked a strategic move to expand its product portfolio and enhance its technological capabilities. Chart Industries has also capitalized on the growing demand for hydrogen infrastructure by developing specialized VIPs capable of handling extreme conditions required for hydrogen storage and transport.

Cryofab, Inc.

Cryofab, Inc. is another leading player, renowned for its innovative approach to customized vacuum insulated pipes designed for niche applications. Cryofab’s strong foothold in the aerospace sector is evident through its collaborations with prominent organizations like NASA and SpaceX. In 2022, Cryofab supplied specialized VIPs for NASA’s Artemis program, which aims to establish a sustainable human presence on the moon. These pipes were specifically engineered to withstand the extreme conditions associated with cryogenic fuels used in space missions. Additionally, Cryofab has made significant strides in the electronics manufacturing sector, where its products facilitate precise temperature control during semiconductor fabrication.

Acme Cryogenics

Acme Cryogenics rounds out the list of top players to the North American vacuum insulated pipe market. The company specializes in standard vacuum insulated pipes by catering primarily to the food and beverage industry. Its cost-effective solutions have earned it a reputation as a trusted supplier among major food processors. Acme Cryogenics’ collaboration with Tyson Foods in 2022 exemplifies its ability to meet the stringent requirements of the food processing sector. The company also emphasizes sustainability, aligning with global trends toward eco-friendly practices. For example, Acme launched a line of recyclable VIPs in early 2023 by targeting environmentally conscious customers.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the North American vacuum insulated pipe market employ a range of strategies to consolidate their positions and drive growth. One prevalent strategy is mergers and acquisitions, enabling companies to expand their product portfolios and enter new markets. For instance, Chart Industries’ acquisition of SES Cryo Technologies in 2021 allowed it to enhance its cryogenic offerings and strengthen its presence in the hydrogen economy. Another widely adopted strategy is forming strategic partnerships with industry leaders and government agencies. Cryofab, Inc.’s collaboration with NASA and SpaceX promotes its commitment to delivering tailored solutions for high-stakes applications like space exploration. Product innovation is also a cornerstone of success, with companies investing heavily in R&D to develop advanced VIPs capable of meeting evolving industry needs. Acme Cryogenics, for example, introduced a line of recyclable pipes in 2023, addressing growing concerns about environmental sustainability. Lastly, geographic expansion plays a critical role, as evidenced by Chart Industries’ efforts to establish a stronger presence in emerging markets across Latin America and Asia-Pacific.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, Chart Industries acquired SES Cryo Technologies to bolster its cryogenic product offerings and expand into the hydrogen economy.

- In June 2023, Cryofab, Inc. partnered with NASA to design and supply vacuum insulated pipes for the Artemis program by enhancing its reputation in the aerospace sector.

- In March 2023, Acme Cryogenics unveiled a new line of recyclable vacuum insulated pipes, targeting environmentally conscious customers in the food and beverage industry.

- In January 2023, Cryofab, Inc. collaborated with SpaceX to provide customized VIPs for cryogenic fuel storage systems used in rocket propulsion.

- In October 2022, Chart Industries invested $50 million in R&D to develop next-generation VIPs capable of supporting large-scale LNG and hydrogen projects.

MARKET SEGMENTATION

This research report on the North America Vacuum Insulated Pipe market has been segmented and sub-segmented based on the following categories.

By Product

- Standard

- Customized

By Application

- Cryogenic

- Food & Beverage

- Aerospace

- Electronic Manufacturing & Testing

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What are the key opportunities in the North America Vacuum Insulated Pipe Market?

Opportunities stem from the increasing demand for efficient cryogenic transportation in LNG, industrial gas, and aerospace sectors, along with expanding investments in clean energy infrastructure.

2. What are the major challenges facing the North America Vacuum Insulated Pipe Market?

Challenges include high initial installation costs, complex manufacturing requirements, and limited availability of skilled labor for maintenance and assembly.

3. Who are the major players in the North America Vacuum Insulated Pipe Market?

Leading players include Chart Industries, Cryofab Inc., Acme Cryogenics, Vacuum Barrier Corporation, and PHPK Technologies, known for their innovation and strong distribution networks.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]