North America Telecom Analytics Market Size, Share, Trends & Growth Forecast Report By Deployment Model (Cloud and On-Premise), Organization Size, Component, Application, Country (The United States, Canada, and Rest of North America), Industry Analysis From 2024 to 2033

North America Telecom Analytics Market Size

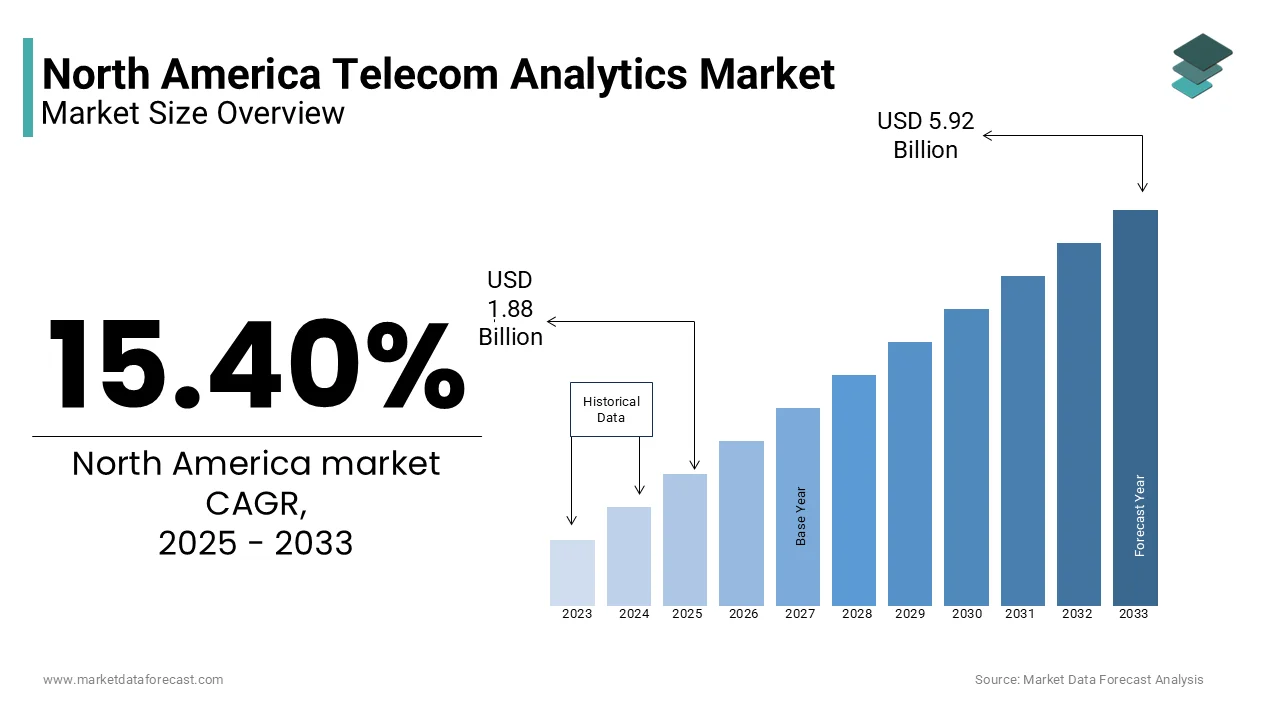

The size of the North America Telecom Analytics Market was worth USD 1.63 billion in 2024. The North America is expected to grow from USD 1.88 billion in 2025 to USD 5.92 billion by 2033, with a compound annual growth rate (CAGR) of 15.40% during the forecast period 2025 to 2033.

The telecom analytics encompasses a suite of software solutions and services designed to analyze data generated by telecommunications networks. These analytics tools enable telecom operators to gain insights into customer behavior, network performance, and operational efficiency. The telecom companies can optimize their services by enhancing customer experiences, and drive revenue growth. The growth of this market is driven by the increasing volume of data generated by telecom networks and the need for actionable insights to remain competitive. The telecom operators are investing in analytics solutions to manage network traffic, reduce churn, and improve service quality. Additionally, the integration of IoT devices and the expansion of 5G networks are further propelling the demand for telecom analytics, as these technologies generate vast amounts of data that require sophisticated analysis.

MARKET DRIVERS

Enhancing Customer Experience through Telecom Analytics

The increasing demand for enhanced customer experience is a primary driver of the North America telecom analytics market. There is a growing emphasis on understanding customer preferences and behaviors to tailor services accordingly as competition intensifies among telecom operators. Telecom analytics solutions enable companies to analyze customer data, identify trends, and develop targeted marketing strategies that enhance customer satisfaction and loyalty. According to a report by Deloitte, companies that prioritize customer experience can achieve revenue growth rates of 4-8% above their market average, underscoring the importance of analytics in driving business success. Moreover, the rise of digital transformation initiatives across the telecom sector is further fueling the demand for analytics solutions. The need for data-driven insights becomes paramount as telecom operators increasingly adopt digital technologies to streamline operations and improve service delivery. Operators can optimize their networks, reduce operational costs, and enhance service quality by positioning themselves for sustained growth in a rapidly evolving market.

IoT and 5G Revolution

The rapid expansion of IoT devices and the rollout of 5G networks are also significant drivers of the North America telecom analytics market. The proliferation of IoT devices generates vast amounts of data that require sophisticated analytics to manage effectively. Telecom operators are increasingly leveraging analytics to monitor network performance, optimize resource allocation, and ensure seamless connectivity for IoT applications. Furthermore, the deployment of 5G networks is expected to further enhance the demand for telecom analytics. 5G technology enables faster data transmission and lower latency, resulting in increased data generation from connected devices. According to the Global System for Mobile Communications Association, 5G connections are expected to reach 1.7 billion globally by 2025 by creating new opportunities for telecom operators to leverage analytics for improved service delivery and customer engagement. The demand for analytics solutions that can harness the power of IoT and 5G technologies is likely to grow by positioning the North America telecom analytics market for significant expansion.

MARKET RESTARINTS

Cost Barriers and Integration Challenges

One of the primary restraints affecting the North America telecom analytics market is the high cost associated with implementing advanced analytics solutions. While these systems offer significant benefits in terms of operational efficiency and customer insights, the initial investment required for software, hardware, and training can be substantial. According to a survey conducted by the National Association of Manufacturers, 60% of manufacturers cited high equipment costs as a significant barrier to adopting new technologies. This reluctance to invest in advanced analytics solutions can hinder market growth, as companies may opt for less sophisticated or outdated systems to manage their data. Additionally, the complexity of integrating analytics solutions with existing telecom infrastructure can pose challenges for operators. Many telecom companies have legacy systems in place, and the process of upgrading to new analytics platforms can be time-consuming and resource-intensive. The learning curve associated with mastering new analytics technologies can be steep for companies with limited experience in data analytics. The high costs and integration complexities associated with telecom analytics may restrict widespread adoption by ultimately impacting the growth of the North America telecom analytics market.

Another significant restraint is the regulatory environment surrounding data privacy and security. They must navigate complex regulations regarding data protection and privacy as telecom operators collect and analyze vast amounts of customer data. Compliance with laws such as the General Data Protection Regulation (GDPR) and various state-level privacy laws can impose additional costs and operational challenges for businesses. According to a report by the International Association of Privacy Professionals, 70% of organizations reported that compliance with data protection regulations is a significant challenge. Navigating the complex regulatory landscape can pose a significant challenge for telecom analytics providers by potentially impacting their ability to deliver solutions that meet regulatory requirements.

MARKET OPPORTUNITIES

Navigating Data Privacy Regulations

The increasing focus on network optimization presents a significant opportunity for the North America telecom analytics market. The demand for analytics solutions that can provide real-time insights into network performance is expected to rise as telecom operators strive to enhance the performance and reliability of their networks. Telecom analytics enables operators to monitor traffic patterns, identify bottlenecks, and optimize resource allocation by ultimately improving service quality and customer satisfaction.

Moreover, the rise of artificial intelligence (AI) and machine learning technologies is creating new opportunities for telecom analytics. These advanced technologies enable operators to analyze vast amounts of data more efficiently and derive actionable insights that can drive decision-making.

Personalization Through Analytics

The growing trend of personalized customer experiences also offers substantial opportunities for the North America telecom analytics market. As consumers demand more tailored services and experiences, telecom operators are leveraging analytics to gain insights into customer preferences and behaviors. This enables them to develop targeted marketing strategies and enhance customer engagement. According to a report by Salesforce, 70% of consumers say a company’s understanding of their personal needs influences their loyalty. The telecom operators can improve customer retention and drive revenue growth by utilizing analytics to create personalized experiences. The North America telecom analytics market is well-positioned to capitalize on this trend as the demand for personalized services continues to rise.

MARKET CHALLENGES

Rising Competition from Cloud-Based and Open-Source Solutions

One of the foremost challenges facing the North America telecom analytics market is the increasing competition from alternative data analytics solutions. The new technologies and methodologies are emerging that offer unique advantages over traditional telecom analytics as the market evolves. For instance, cloud-based analytics platforms and open-source solutions are gaining traction by providing organizations with cost-effective and flexible options for data analysis. According to a report by Gartner, the global cloud analytics market is projected to grow from $22 billion in 2020 to $84 billion by 2025 by indicating a shift in preference towards these advanced technologies. This competitive landscape necessitates that telecom analytics providers continuously innovate and improve their offerings to maintain market share.

Keeping Pace with Technological Advancements

Another significant challenge is the rapid pace of technological advancements, which can lead to obsolescence of existing analytics solutions. The telecom operators may find their current systems inadequate for meeting evolving business needs. This constant need for innovation can strain the resources of analytics providers for smaller companies that may struggle to keep up with the pace of change. Consequently, the challenge of maintaining technological relevance in a fast-evolving market landscape poses a significant challenge for the North America telecom analytics market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

15.40% |

|

Segments Covered |

By Deployment Model, Organization Size, Component, Application, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

The United States, Canada, Mexico, and Rest of North America |

|

Market Leaders Profiled |

Cisco Systems, Inc., IBM Corporation, Oracle Corporation, SAP SE, Microsoft Corporation, SAS Institute Inc., Huawei Technologies Co., Ltd., Nokia Corporation, Teradata Corporation, and TIBCO Software, Inc. |

SEGMENTAL ANALYSIS

By Deployment Model Insights

The cloud-based segment was the largest and held the North America telecom analytics market share of 58.6% in 2024. This dominance can be attributed to the growing preference for cloud solutions among telecom operators seeking scalable and flexible analytics options. Cloud-based analytics offers numerous advantages, including reduced infrastructure costs, remote access, and simplified maintenance by making it an attractive choice for businesses of all sizes. The demand for cloud-based telecom analytics solutions is expected to grow as organizations increasingly prioritize efficiency and performance in their operations. The ability of cloud-based analytics to provide real-time data and insights is particularly appealing for applications requiring quick response times and straightforward implementation. Additionally, the growing emphasis on energy efficiency and sustainability is driving the adoption of cloud-based solutions, as they often require less energy and generate less waste compared to traditional on-premise systems. The cloud-based deployment model is likely to maintain its leading position by ongoing advancements in technology and the increasing demand for effective telecom analytics solutions.

The on-premise segment is projected to grow at a CAGR of 9.4% in the next coming years. This growth can be attributed to the increasing demand for secure and controlled analytics solutions in various applications. On-premise analytics allows organizations to maintain complete control over their data and infrastructure, which is particularly appealing for industries with stringent security and compliance requirements. Furthermore, the rise of hybrid systems that combine both cloud and on-premise technologies is driving the adoption of on-premise analytics solutions. These hybrid systems allow organizations to leverage the benefits of both deployment models by providing a flexible and secure approach to data analysis. The demand for on-premise telecom analytics solutions is likely to grow by positioning this segment for significant expansion in the North America telecom analytics market.

By Organization Size Insights

The large enterprises segment was the largest in the North America telecom analytics market by accounting significant share in 2024. This dominance can be attributed to the substantial resources and investments that large organizations can allocate towards advanced analytics solutions. Large enterprises often have complex operations and extensive data sets, necessitating sophisticated analytics tools to derive actionable insights. According to a report by the International Data Corporation, large enterprises are expected to increase their spending on analytics solutions by 15% annually that is reflecting the growing importance of data-driven decision-making in their operations. The ability of large enterprises to leverage telecom analytics for optimizing network performance, enhancing customer experiences, and driving operational efficiency is particularly appealing. Additionally, the growing emphasis on data security and compliance is driving the adoption of analytics solutions among large organizations, as they seek to ensure that their data management practices align with regulatory requirements. The large enterprises segment is likely to maintain its leading position due to its support by ongoing advancements in technology and the increasing demand for effective telecom analytics solutions.

The small and mid-sized enterprises (SMEs) segment is lucratively to grow with an estimated CAGR of 12.7% in the next coming years. This growth can be attributed to the increasing recognition among SMEs of the value of data analytics in driving business growth and improving operational efficiency. According to a survey conducted by Deloitte, 60% of SMEs reported that they plan to invest in analytics solutions to enhance their decision-making processes. Furthermore, the rise of affordable cloud-based analytics solutions is making it easier for SMEs to adopt advanced analytics technologies without the need for significant upfront investments. These solutions provide SMEs with access to powerful analytics tools that were previously only available to larger organizations. The demand for telecom analytics solutions tailored to their needs is likely to grow by positioning this segment for significant expansion in the North America telecom analytics market.

By Component Insights

The solutions segment was the largest by occupying 65.1% of the total North America telecom analytics market share in 2024. This dominance can be attributed to the increasing demand for advanced analytics tools that enable telecom operators to derive actionable insights from their data. Telecom analytics solutions encompass a wide range of functionalities, including network performance monitoring, customer behavior analysis, and revenue assurance. The demand for telecom analytics solutions is expected to grow as organizations increasingly prioritize efficiency and performance in their operations. The ability of analytics solutions to provide real-time data and insights is particularly appealing for applications requiring quick response times and straightforward implementation. Additionally, the growing emphasis on energy efficiency and sustainability is driving the adoption of analytics solutions, as they enable better monitoring and control of telecom networks. The solutions segment is likely to maintain its leading position by ongoing advancements in technology and the increasing demand for effective telecom analytics solutions.

The services segment is esteemed to achieve a CAGR of 14.3% in the next coming years. This growth can be attributed to the increasing demand for consulting, implementation, and support services related to telecom analytics solutions. They are increasingly turning to service providers for expertise in deploying and optimizing these solutions as organizations seek to maximize the value of their analytics investments. The rise of complex telecom environments, characterized by the integration of various technologies and platforms, is driving the demand for specialized services. Organizations often require assistance in customizing analytics solutions to meet their specific needs, as well as training staff to effectively utilize these tools. Additionally, the growing emphasis on data security and compliance is prompting telecom operators to seek expert guidance in navigating regulatory requirements associated with data management and analytics.

By Application Insights

The customer management application segment dominated the North America telecom analytics market by occupying 30.4% of the share in 2024. This dominance can be attributed to the critical role that analytics plays in enhancing customer experiences and driving customer retention in the highly competitive telecom industry. Telecom operators utilize analytics to gain insights into customer behavior, preferences, and usage patterns, enabling them to tailor their services and marketing strategies accordingly. According to a report by Deloitte, companies that prioritize customer experience can achieve revenue growth rates of 4-8% above their market average due to the importance of analytics in driving business success. The ability of customer management analytics to provide actionable insights in real-time is particularly appealing for telecom operators seeking to improve customer satisfaction and loyalty. Additionally, the growing emphasis on personalized services and targeted marketing is driving the adoption of analytics solutions in customer management applications, as organizations strive to meet the evolving expectations of their customers. The customer management application segment is likely to maintain its leading position which was supported by ongoing advancements in technology and the increasing demand for effective analytics solutions.

The network management segment is swiftly emerging with a dominant CAGR of 12.4% during the forecast period. This growth can be attributed to the increasing need for telecom operators to optimize network performance and ensure service reliability in the face of rising data traffic and user demands. According to the Cisco Visual Networking Index, global internet traffic is expected to reach 4.8 zettabytes per year by 2022 with the urgent need for effective network management solutions. Furthermore, the rise of 5G technology and the proliferation of IoT devices are driving the demand for advanced network management analytics. These technologies generate vast amounts of data that require sophisticated analysis to manage effectively. Telecom operators are increasingly leveraging analytics to monitor network performance, identify bottlenecks, and optimize resource allocation by ultimately improving service quality and customer satisfaction. The demand for analytics solutions in network management applications is likely to grow by positioning this segment for significant expansion in the North America telecom analytics market.

REGIONAL ANALYSIS

The United States was the top performer in the North America telecom analytics market by accounting for 70.6% of the share in 2024. The U.S. market is characterized by a robust demand for analytics solutions across various sectors, including telecommunications, media, and technology. According to the U.S. Federal Communications Commission, the telecommunications industry in the U.S. generated approximately $1.5 trillion in revenue in 2020 with the significant investment in analytics technologies to enhance operational efficiency and customer engagement. The rapid adoption of advanced technologies, such as AI and machine learning, is also contributing to the growth of the telecom analytics market in the U.S., as organizations seek to leverage data for improved decision-making.

Moreover, the presence of key players and a well-established technology ecosystem in the United States enhances the market's competitive landscape. Major companies such as IBM, Oracle, and SAP are actively involved in developing innovative telecom analytics solutions is driving technological advancements in the industry. The United States is expected to maintain its leading position owing to the ongoing investments in research and development and the increasing demand for efficient analytics solutions.

Canada telecom analytics market is anticipated to witness a fastest CGAR of 20.3% during the forecast period. The Canadian market is driven by a growing interest in data analytics and digital transformation initiatives, as organizations seek to enhance their operational efficiency and customer experiences. According to Statistics Canada, the telecommunications industry in Canada generated approximately CAD 50 billion in revenue in 2020 due to the significant investment in analytics technologies. The increasing adoption of cloud-based solutions and the expansion of 5G networks are also contributing to the demand for telecom analytics in Canada.

KEY MARKET PLAYERS

The major players in the North America analytics market include Cisco Systems, Inc., IBM Corporation, Oracle Corporation, SAP SE, Microsoft Corporation, SAS Institute Inc., Huawei Technologies Co., Ltd., Nokia Corporation, Teradata Corporation, and TIBCO Software, Inc.

TOP PLAYERS IN THE MARKET

In the North America telecom analytics market, several key players have established themselves as leaders, contributing significantly to the overall market dynamics. IBM is one of the foremost manufacturers, renowned for its high-quality analytics solutions that cater to various applications, including telecommunications, media, and technology. The company's commitment to innovation and extensive product portfolio has positioned it as a market leader, with a strong focus on developing advanced analytics technologies that enhance performance and reliability.

Another major player is Oracle, a well-known name in the analytics industry. Oracle offers a diverse range of telecom analytics solutions that are widely used in various applications, including customer management, network optimization, and revenue assurance. The company's emphasis on research and development has led to the introduction of cutting-edge technologies that meet the evolving needs of customers.

SAP is also a prominent player in the telecom analytics market, recognized for its innovative analytics solutions and commitment to customer success. SAP's analytics tools are widely used in various industries, including telecommunications, finance, and manufacturing, making them integral to the transition towards data-driven decision-making. The company's focus on developing high-performance, user-friendly analytics solutions has resonated with businesses seeking to leverage data for improved operational efficiency by enhancing its reputation as a trusted manufacturer in the North America telecom analytics market.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the North America telecom analytics market employ a variety of strategies to strengthen their market position and enhance competitiveness. One prominent strategy is the focus on innovation and technological advancement. Companies like IBM and Oracle invest heavily in research and development to create cutting-edge analytics solutions that improve performance, scalability, and user experience. These manufacturers can meet evolving consumer demands and comply with stringent regulatory standards, thereby maintaining their competitive edge in the market.

Another significant strategy is the expansion of product portfolios to cater to diverse consumer needs. Manufacturers are increasingly offering a wide range of analytics solutions, including cloud-based, on-premise, and hybrid systems, to appeal to various applications. For instance, SAP has introduced a range of analytics tools specifically designed for telecom operators, addressing the growing demand for advanced data management capabilities.

Strategic partnerships and collaborations also play a crucial role in enhancing market presence. Companies often collaborate with technology providers and system integrators to expand their reach and improve distribution channels. For example, partnerships with telecommunications companies enable analytics providers to integrate their technologies into a wider array of applications, thereby increasing sales and market penetration.

COMPETITIVE LANDSCAPE

The competition in the North America telecom analytics market is characterized by a mix of established players and emerging manufacturers, all vying for market share in a rapidly evolving landscape. Major companies such as IBM, Oracle, and SAP dominate the market by leveraging their strong brand recognition, extensive distribution networks, and commitment to innovation. These market key players continuously invest in research and development to enhance analytics performance, scalability, and compliance with stringent security regulations, thereby maintaining their competitive advantage.

Emerging players are also entering the market, often focusing on niche segments or innovative technologies, such as AI-driven analytics and cloud-based solutions. This influx of new entrants intensifies competition, as they seek to capture market share by offering unique value propositions and addressing the growing demand for intelligent analytics solutions. Additionally, the increasing consumer preference for integrated analytics systems is prompting established manufacturers to adapt their offerings and invest in cleaner technologies, further heightening competition.

Price competition is another significant factor influencing the market dynamics. As manufacturers strive to attract price-sensitive consumers, they may engage in competitive pricing strategies, which can impact profit margins. However, companies that prioritize quality, performance, and customer service are likely to differentiate themselves and build brand loyalty, allowing them to navigate the competitive landscape effectively. Overall, the North America telecom analytics market is poised for continued growth, driven by innovation, evolving consumer preferences, and a dynamic competitive environment.

REGIONAL ANALYSIS

- In March 2023, IBM launched a new suite of AI-driven telecom analytics solutions designed to enhance network performance and customer experience, reinforcing its commitment to innovation and market leadership.

- In January 2023, Oracle introduced a new series of cloud-based analytics tools aimed at telecom operators, catering to the growing demand for flexible and scalable solutions.

- In February 2023, SAP expanded its product portfolio by launching a new range of analytics solutions specifically designed for the telecommunications industry, addressing the increasing demand for advanced data management capabilities.

- In April 2023, Cisco partnered with a leading telecom provider to integrate its analytics solutions into a new line of smart city initiatives, enhancing its market presence.

- In May 2023, TIBCO Software acquired a small analytics technology firm to strengthen its capabilities in the telecom analytics market and expand its product offerings.

- In June 2023, SAS Institute announced a strategic collaboration with a major telecommunications company to develop advanced analytics solutions for customer management and network optimization.

- In July 2023, Microsoft launched a new series of analytics tools designed for telecom operators, reflecting its commitment to innovation and addressing the growing demand for data-driven decision-making.

- In August 2023, Tableau introduced a new line of visualization tools aimed at the telecom sector, targeting the increasing demand for user-friendly analytics solutions.

- In September 2023, Qlik expanded its distribution network by partnering with major telecom providers to increase the availability of its analytics solutions across North America.

- In October 2023, Alteryx unveiled a new series of analytics solutions designed for the telecommunications industry, aiming to capture a larger share of the market.

MARKET SEGMENTATION

This research report on the North American Telecom Analytics market has been segmented and sub-segmented based on the following categories.

By Deployment Model

- Cloud

- On-Premise

By Organization Size

- Large Enterprises

- Small & Mid-Sized Enterprises

By Component

- Solutions

- Network Analytics

- Customer Analytics

- Service Analytics

- Subscriber Analytics

- Location Analytics

- Price Analytics

- Other Solutions Type

- Services

By Application

- Customer Management

- Sales & Marketing Management

- Network Management

- Risk & Compliance Management

- Workforce Management

- Other Application

By Region

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

Which countries are the major contributors to the North America Telecom Analytics Market?

The major contributors are the United States and Canada, with the US holding the largest market share due to its advanced telecom infrastructure and high adoption of analytics technologies.

What are the key drivers of growth in the North America Telecom Analytics Market?

Key drivers include the rapid adoption of 5G technology, increasing use of big data analytics, a growing focus on customer experience management, and the rising need for fraud detection and prevention.

What are the primary applications of telecom analytics in the North American market?

Primary applications include customer analytics, network management, fraud detection, revenue management, and marketing analytics. These applications help telecom companies optimize their operations and enhance customer satisfaction.

What role does artificial intelligence (AI) play in the North America Telecom Analytics Market?

AI plays a crucial role by enabling advanced predictive analytics, automated customer service solutions like chatbots, network optimization, and proactive maintenance. AI-driven analytics helps telecom companies make data-driven decisions and improve operational efficiency.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]