North America System Integration Market Size, Share, Trends & Growth Forecast Report By Service Type (Infrastructure Integration, Application Integration, and Consulting), Enterprise Size, Industry Vertical, Country (The United States, Canada, and Rest of North America), Industry Analysis From 2024 to 2033

North America System Integration Market Size

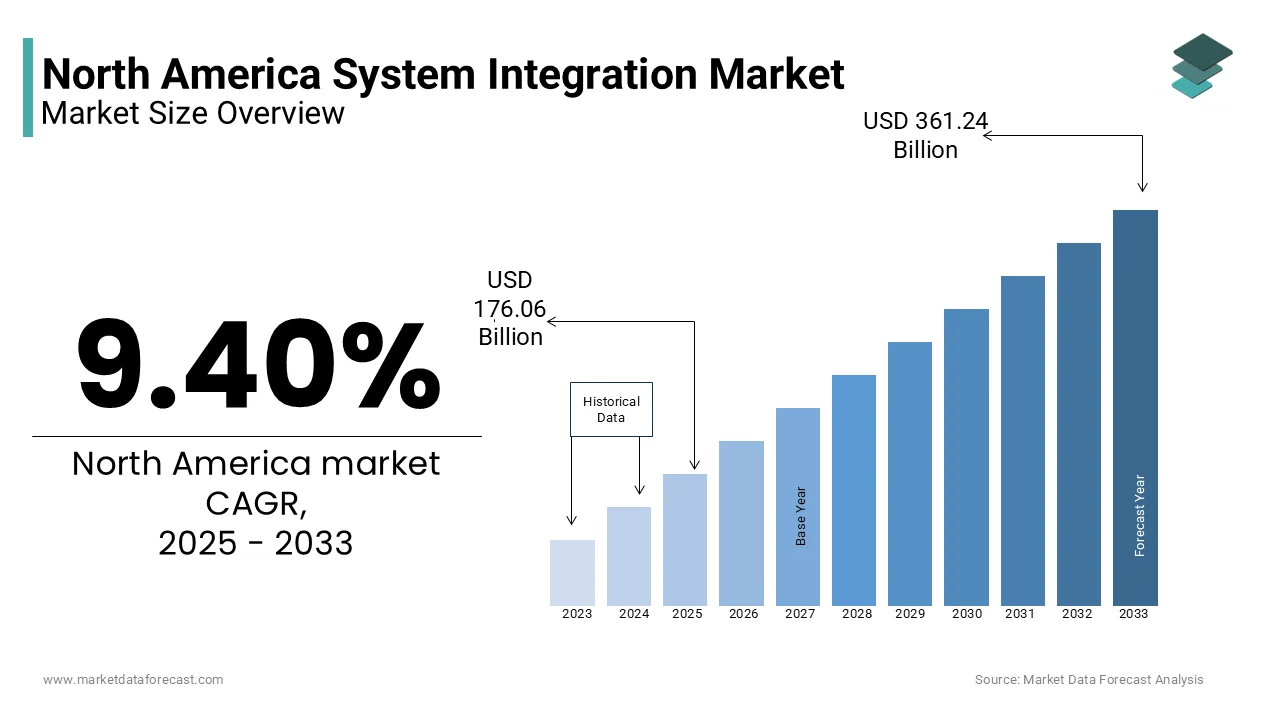

The North America system integration market was worth USD 160.93 billion in 2024. The North America market is projected to reach USD 361.24 billion by 2033 from USD 176.06 billion in 2025, rising at a CAGR of 9.40% from 2025 to 2033.

The system integration involves the process of aligning different IT systems, software applications, and hardware components to streamline operations, enhance efficiency, and improve data flow across an organization. The industries seeking to optimize their technology investments and achieve seamless interoperability among diverse systems is majorly to propel the growth of the market. This growth is driven by the increasing complexity of IT environments, the rising demand for cloud-based solutions, and the need for organizations to enhance their operational efficiency. The system integration market in North America is poised for significant expansion by offering innovative solutions to meet the evolving demands of modern enterprises.

MARKET DRIVERS

Growing Demand for Cloud-Based Solutions

The growing demand for cloud-based solutions is a significant driver of the North America system integration market. They require robust integration services to ensure seamless connectivity between on-premises systems and cloud applications as organizations increasingly migrate their operations to the cloud. Cloud-based solutions offer numerous advantages, including scalability, flexibility, and cost-effectiveness by allowing businesses to adapt quickly to changing market conditions. Additionally, the COVID-19 pandemic has accelerated the shift to remote work, further emphasizing the need for integrated cloud solutions that facilitate collaboration and data access from anywhere. The demand for system integration services that support cloud adoption is expected to rise significantly by driving growth in the North America system integration market.

Increasing Complexity of IT Environments

The increasing complexity of IT environments is another key driver propelling the North America system integration market. The need for effective integration solutions becomes paramount as organizations adopt a multitude of technologies, including IoT devices, big data analytics, and artificial intelligence. According to a survey conducted by the International Data Corporation (IDC), 70% of organizations reported that their IT environments have become more complex over the past few years. This complexity necessitates the implementation of system integration services to ensure that disparate systems can communicate effectively and share data seamlessly. Furthermore, the rise of hybrid IT environments, where organizations utilize a combination of on-premises and cloud-based solutions, further complicates integration efforts. System integration services enable organizations to streamline their operations, improve data visibility, and enhance decision-making capabilities. The demand for system integration solutions is expected to grow significantly in North America as businesses continue to navigate the complexities of modern IT landscapes.

MARKET RESTRAINTS

High Implementation Costs

One of the primary restraints affecting the North America system integration market is the high implementation costs associated with integration projects. Organizations often face significant expenses related to software licenses, hardware, and consulting services, which can deter them from pursuing comprehensive integration solutions. According to a report by Deloitte, the average cost of implementing a system integration project can range from $100,000 to $500,000 by depending on the size and complexity of the organization. Additionally, ongoing costs related to maintenance, upgrades, and training can further strain budgets. This financial barrier can lead to a slower rate of technology adoption among small and medium-sized enterprises (SMEs) that is limiting their ability to compete effectively in the market. The system integration vendors must focus on offering more affordable solutions and flexible pricing models that cater to the needs of smaller organizations, thereby facilitating broader adoption of their services.

Complexity of Integration Processes

Another significant restraint impacting the North America system integration market is the complexity of integration processes. Integrating diverse systems, applications, and technologies can be a daunting task, often requiring specialized skills and expertise. According to a survey by the Project Management Institute, 60% of organizations reported that they encounter challenges related to the complexity of integration projects. This complexity can lead to extended timelines, increased costs, and potential disruptions to business operations. Additionally, the lack of standardization among different systems can complicate integration efforts by making it difficult for organizations to achieve seamless interoperability. To address these challenges, organizations must invest in comprehensive planning and project management strategies to ensure successful integration. The organizations can mitigate the risks associated with complex integration processes and enhance the effectiveness of their system integration efforts by prioritizing clear communication, stakeholder engagement, and thorough testing.

MARKET OPPORTUNITIES

Rise of IoT and Smart Technologies

The rise of the Internet of Things (IoT) and smart technologies presents a significant opportunity for growth in the North America system integration market. The need for effective integration solutions to manage and analyze the vast amounts of data generated by these devices is becoming increasingly critical. The demand for robust system integration services that can facilitate data exchange and interoperability among these devices is elevating the growth of the market. Organizations are seeking to leverage IoT technologies to enhance operational efficiency, improve decision-making, and create new revenue streams. System integration services enable businesses to connect IoT devices with existing systems by allowing for real-time monitoring, data analytics, and automation of processes. The demand for system integration solutions that support these initiatives is expected to drive significant growth in the North America market.

Digital Transformation Initiatives

The ongoing digital transformation initiatives across various industries represent another major opportunity for growth in the North America system integration market. Organizations are increasingly recognizing the importance of leveraging technology to enhance their operations, improve customer experiences, and drive innovation. According to a report by McKinsey, companies that have embraced digital transformation have seen a 20-30% increase in operational efficiency. As businesses seek to integrate new technologies such as cloud computing, artificial intelligence, and big data analytics into their existing systems, the demand for effective system integration services is on the rise. These services enable organizations to streamline their processes, enhance data visibility, and improve collaboration across departments. Furthermore, the shift towards remote work and the need for agile business models have accelerated the adoption of digital solutions that further propels the demand for system integration.

MARKET CHALLENGES

Data Security and Compliance Issues

A significant challenge facing the North America system integration market is the increasing concern over data security and compliance issues. The risk of data breaches and cyberattacks becomes a pressing concern. According to a report by Cybersecurity Ventures, cybercrime is projected to cost the world $10.5 trillion annually by 2025 with the urgent need for robust security measures. Organizations must ensure that their integration processes comply with various regulations, such as the General Data Protection Regulation (GDPR) and the Health Insurance Portability and Accountability Act (HIPAA). Failure to address these security and compliance concerns can result in severe financial penalties, reputational damage, and loss of customer trust. Organizations must invest in comprehensive security strategies, including encryption, access controls, and regular security audits. Addressing data security and compliance issues will be critical for the success of system integration initiatives in North America as the threat landscape continues to evolve.

Rapid Technological Advancements

The rapid pace of technological advancements in the system integration landscape presents a challenge for organizations seeking to implement and maintain integration solutions. The organizations must continuously adapt their integration strategies to keep up with the evolving landscape. According to a report by Forrester, 60% of organizations struggle to keep their integration systems aligned with the latest technological trends. This challenge can lead to increased complexity in managing integration projects, as organizations may need to invest in regular updates, training, and integration with new technologies. Additionally, the constant introduction of new features and functionalities can overwhelm users is leading to difficulties in adoption and utilization. To navigate this challenge, organizations must prioritize ongoing training and development for their employees, ensuring they are equipped with the skills and knowledge necessary to leverage the full potential of their integration solutions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

9.40% |

|

Segments Covered |

By Service Type, Enterprise Size, Industry Vertical, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

The United States, Canada, Mexico, and Rest of North America |

|

Market Leaders Profiled |

John Wood Group, Tesco Controls, Inc., Burrow Global LLC, Prime Controls LP, MAVERICK Technologies, Barry-Wehmiller, INTECH Process Automation, Siemens AG, Schneider Electric, Emerson Electric Co., Honeywell International Inc., ABB Ltd, Rockwell Automation, Inc., Yokogawa Electric Corporation, Wunderlich-Malec Engineering, Inc., Deloitte, and Baker Hughes. |

SEGMENTAL ANALYSIS

By Service Type Insights

The professional services segment was the largest by accounting for 50.6% of the total North America system integration market share in 2024. This dominance can be attributed to the increasing demand for consulting, system integration, and implementation services as organizations seek to optimize their IT operations. The rising need for expert guidance in navigating complex IT environments is augmented in prompting the growth of the market. Professional services enable organizations to leverage the expertise of IT consultants to assess their needs, design tailored solutions, and implement best practices. Additionally, the growing emphasis on digital transformation and the adoption of emerging technologies further propels the demand for professional services.

The managed services segment is projected to experience a CAGR of 15.4% during the forecast period. This growth can be attributed to the increasing demand for outsourced IT management and support services as organizations seek to enhance operational efficiency and reduce costs. The rising adoption of cloud-based solutions and the need for enhanced cybersecurity. Managed services allow organizations to offload their IT operations to third-party providers by enabling them to focus on their core business functions while relying on experts to manage their infrastructure, applications, and security.

By Enterprise Size Insights

The large enterprises segment dominated the North America system integration market by accounting for significant share in 2024. This dominance is driven by the significant investments made by large organizations in system integration solutions to enhance their operational capabilities and maintain a competitive edge. The large enterprises are increasingly adopting advanced system integration solutions to streamline their operations and improve efficiency. The complexity of large-scale IT environments necessitates robust integration services that can handle extensive data and provide real-time visibility. Additionally, large enterprises often have dedicated IT teams and resources, enabling them to implement and optimize system integration solutions effectively.

The small and medium-sized enterprises (SMEs) segment is projected to experience a CAGR of 20.3% from 2025 to 2033. This growth can be attributed to the increasing recognition among SMEs of the importance of system integration solutions in enhancing operational efficiency and competitiveness. According to a survey by the Small Business Administration, 60% of SMEs reported that they plan to invest in system integration technologies to improve their business operations. The adoption of system integration solutions is becoming essential as SMEs seek to leverage technology to optimize their processes and enhance customer experiences. Additionally, the availability of cost-effective solutions tailored for SMEs is making it easier for these organizations to implement advanced integration technologies.

By Industry Vertical Insights

The retail and consumer goods segment was the largest by accounting 30.4% of the North Ameerica System integration market share in 2024. This dominance is driven by the critical need for retailers to manage complex supply chains effectively in the face of increasing consumer demand for fast and reliable delivery. According to a report by eMarketer, U.S. retail e-commerce sales are projected to reach $1 trillion by 2025 due to the growing importance of effective system integration in the retail sector. System integration solutions enable retailers to optimize inventory levels, streamline logistics, and enhance customer satisfaction by ensuring timely product availability. The rise of omnichannel retailing, where consumers expect a seamless shopping experience across various platforms, further propels the demand for advanced system integration solutions.

The healthcare segment is projected to experience a CAGR of 25.4% from 2025 to 2033. This growth can be attributed to the increasing digitization of healthcare services and the rising demand for integrated IT solutions that enhance patient care and operational efficiency. According to a report by the American Hospital Association, U.S. hospitals are expected to invest over $50 billion in health IT solutions by 2025 with the growing importance of technology in healthcare delivery. System integration solutions enable healthcare organizations to streamline their operations, improve patient engagement, and ensure compliance with regulations. Additionally, the expansion of telehealth and remote patient monitoring solutions is driving the demand for system integration in the healthcare sector. The demand for integration solutions that cater to the unique challenges of healthcare delivery is expected to drive significant growth in this segment.

REGIONAL ANALYSIS

The United States held a dominant position in the North America system integration market with an estimated share of 80.3% in 2024. The country's advanced technological infrastructure and the presence of major technology companies driving innovation in the system integration sector. The U.S. market growth is attributed with the significant investments in research and development by leading to the introduction of innovative system integration solutions that cater to the evolving needs of businesses. Additionally, the growing adoption of cloud-based system integration services among U.S. organizations is propelling the demand for these solutions.

Canada system integration market is likely to experience a CAGR of 6.4% during the forecast period. This growth can be attributed to the increasing demand for system integration solutions driven by the expansion of the technology sector and the rising adoption of digital transformation initiatives. The strong emphasis on quality and customer service, with organizations increasingly recognizing the importance of system integration in enhancing operational efficiency is amplifying the growth of the market. Additionally, government initiatives aimed at promoting innovation and technology adoption further support this trend. Canada is poised for substantial growth in the system integration sector due to ongoing investments in technology and infrastructure.

KEY MARKET PLAYERS

The major players in the North America system integration market include John Wood Group, Tesco Controls, Inc., Burrow Global LLC, Prime Controls LP, MAVERICK Technologies, Barry-Wehmiller, INTECH Process Automation, Siemens AG, Schneider Electric, Emerson Electric Co., Honeywell International Inc., ABB Ltd, Rockwell Automation, Inc., Yokogawa Electric Corporation, Wunderlich-Malec Engineering, Inc., Deloitte, and Baker Hughes.

TOP KEY PLAYERS IN THE MARKET

IBM

IBM is a leading player in the North America system integration market, known for its comprehensive suite of solutions that cater to various industries. The company's services include consulting, system integration, and managed services, enabling organizations to optimize their operations and enhance decision-making. IBM's commitment to innovation and research has positioned it as a dominant force in the system integration market, with a significant share of the North American landscape.

Accenture

Accenture is another major player in the North America system integration market, recognized for its consulting and technology services that help organizations navigate digital transformation. The company's focus on delivering tailored solutions and leveraging advanced technologies, such as AI and blockchain, has enabled it to capture a significant share of the market. Accenture's extensive industry expertise and global reach further enhance its competitive position in the system integration sector.

Deloitte

Deloitte is a prominent player in the North America system integration market, offering a wide range of consulting and technology services to organizations across various sectors. The company's services include IT strategy, implementation, and managed services, enabling clients to enhance their operational efficiency and drive innovation. Deloitte's strong brand reputation and commitment to delivering high-quality solutions have made it a trusted partner for businesses seeking to optimize their IT operations.

STRATEGIES EMPLOYED BY KEY PLAYERS

Key players in the North America system integration market employ various strategies to strengthen their market position and enhance competitiveness. One prominent strategy is the focus on innovation and research and development, enabling companies to introduce cutting-edge system integration solutions that meet the evolving needs of organizations. For instance, IBM continuously invests in enhancing its integration capabilities to incorporate advanced features and functionalities that align with industry trends.

Additionally, strategic partnerships and collaborations play a crucial role in expanding market reach and enhancing product offerings. Accenture, for example, has formed alliances with various technology providers to ensure a diverse range of high-quality solutions for its users, allowing organizations to differentiate themselves in a competitive landscape.

Furthermore, companies are increasingly prioritizing customer-centric approaches, offering tailored solutions and support services to address specific requirements of their clients. This focus on customer engagement not only fosters loyalty but also enhances the overall value proposition of their offerings.

Moreover, many key players are actively pursuing educational initiatives to empower organizations in their system integration implementations. Deloitte, for instance, provides extensive resources and training programs to help users navigate the complexities of its solutions. By leveraging these strategies, companies in the North America system integration market are positioning themselves to capitalize on emerging opportunities and navigate the challenges of a rapidly evolving industry landscape.

COMPETITIVE LANDSCAPE

The competition in the North America system integration market is characterized by a dynamic landscape where innovation, efficiency, and customer experience are paramount. Major players are continuously striving to differentiate themselves through advanced technologies and comprehensive solutions. The market is witnessing a surge in the adoption of system integration services, driven by increasing consumer demand for operational efficiency and integrated business processes. As organizations prioritize digital transformation and seek to enhance their software capabilities, companies that provide reliable, user-friendly platforms and robust functionalities are gaining a competitive edge.

Furthermore, the presence of both established players and emerging startups fosters a competitive environment that encourages rapid technological advancements. The ongoing digital transformation across various sectors is further intensifying competition, as organizations seek to optimize their operations through system integration solutions. In this context, companies must remain agile and responsive to market trends to maintain their competitive advantage in the North America system integration market.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, IBM announced the launch of a new AI-driven integration platform designed to enhance data connectivity across various systems.

- In February 2024, Accenture expanded its system integration services by acquiring a leading cloud consulting firm, aiming to enhance its capabilities in cloud migration.

- In March 2024, Deloitte introduced a new suite of integration tools focused on improving collaboration between IT and business units.

- In April 2024, Oracle announced enhancements to its integration cloud services, focusing on improving interoperability with third-party applications.

- In May 2024, Capgemini launched a new system integration framework that leverages machine learning to optimize integration processes.

- In June 2024, Infosys announced a partnership with a major technology provider to enhance its system integration offerings in the healthcare sector.

- In July 2024, Wipro introduced a new set of managed services aimed at helping organizations streamline their integration efforts.

- In August 2024, TCS launched a new platform that combines system integration with advanced analytics to improve operational efficiency.

- In September 2024, HCL Technologies announced a major update to its integration services, focusing on enhancing security and compliance features.

- In October 2024, Fujitsu expanded its system integration capabilities by acquiring a firm specializing in IoT solutions, aiming to enhance its offerings in smart technology integration.

MARKET SEGMENTATION

This research report on the North America system integration market is segmented and sub-segmented into the following categories.

By Service Type

- Infrastructure Integration

- Application Integration

- Consulting

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises

By Industry Vertical

- IT & Telecom

- Defense & Security

- BFSI

- Oil & Gas

- Healthcare

- Transportation

- Retail

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What factors are driving the growth of the North America system integration market?

The market is driven by increasing demand for automation, cloud computing adoption, rising cybersecurity concerns, and the need for efficient IT infrastructure.

Which industries are the primary users of system integration services in North America?

Key industries include IT & telecom, healthcare, BFSI (banking, financial services, and insurance), manufacturing, retail, and government sectors.

How is AI and automation affecting system integration services?

AI-driven automation is streamlining integration processes, improving efficiency, and enabling predictive analytics for IT and business operations.

What is the future outlook for the North America system integration market?

The market is expected to grow due to increased adoption of emerging technologies like IoT, AI, 5G, and blockchain, driving demand for seamless system integration.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]