North America Sandblasting Media Market Size, Share, Trends & Growth Forecast Report By Product ( Aluminium Oxide, Sodium Bicarbonate), End User, And Country (US, Canada, And Rest Of North America), Industry Analysis From 2025 To 2033

North America Sandblasting Media Market Size

The North America Sandblasting Media Market size was calculated to be USD 3.96 billion in 2024 and is anticipated to be worth USD 7.34 billion by 2033, from USD 4.24 billion in 2025, growing at a CAGR of 7.11% during the forecast period.

MARKET DRIVERS

Growing Demand in the Automotive Industry

The automotive sector stands as a pivotal driver of the North American sandblasting media market, primarily due to its extensive use in surface preparation and coating removal processes. Automakers rely heavily on sandblasting to achieve smooth, clean surfaces before applying protective coatings or finishes, ensuring durability and aesthetic appeal. Like, vehicle production in North America stood at 15.6 million units in 2022, reflecting steady growth despite global supply chain disruptions. This surge in production directly translates into heightened demand for sandblasting media. Furthermore, the increasing adoption of lightweight materials like aluminum and composites in automobile manufacturing necessitates advanced surface treatment techniques, further propelling the market growth. Also, aluminum usage in vehicles is expected to increase significantly by 2030, creating a sustained need for specialized blasting solutions.

Expansion of the Oil and Gas Sector

Another significant driver is the burgeoning oil and gas industry, particularly in regions like Texas and Alberta. Sandblasting media plays a critical role in pipeline maintenance, tank cleaning, and equipment refurbishment, ensuring operational efficiency and safety. Similarly, crude oil production in the United States increased to over 10.5 million bpd in 2022. This production boom has spurred investments in infrastructure, including refineries and storage facilities, where sandblasting is indispensable. Additionally, aging infrastructure in the sector demands frequent surface treatments to prevent corrosion and extend asset life. The Canadian Energy Pipeline Association estimates that over CAD 20 billion will be invested in pipeline projects by 2030, further amplifying demand for sandblasting solutions.

MARKET RESTRAINTS

Stringent Environmental Regulations

Environmental concerns are a significant restraint impacting the North American sandblasting media market, particularly due to the use of traditional abrasive materials like silica sand. Silica-based blasting generates respirable crystalline silica dust, which poses severe health risks, including silicosis and lung cancer. In response, regulatory bodies such as the Occupational Safety and Health Administration (OSHA) have imposed strict guidelines limiting permissible exposure levels to 50 micrograms per cubic meter of air. Compliance with these regulations often requires companies to invest in advanced containment systems and alternative media, increasing operational costs. Like, over 2.3 million workers in the U.S. are exposed to silica dust annually, underscoring the scale of the issue. These stringent measures have led to a gradual decline in the use of silica sand, forcing manufacturers to pivot toward safer but more expensive alternatives like garnet or recycled glass.

Fluctuating Raw Material Prices

Another major challenge is the volatility in raw material prices, which significantly affects production costs and profit margins. Key materials used in sandblasting media, such as aluminum oxide and steel grit, are subject to price fluctuations driven by global supply chain disruptions and geopolitical tensions. For instance, aluminum prices surged significantly in 2022 due to export restrictions in China, a leading producer. Similarly, steel prices experienced a 25% increase in the same year, attributed to rising energy costs and trade tariffs. Also, these price swings create uncertainty for manufacturers and end-users, who must absorb additional costs or pass them on to customers. Such instability hampers long-term investment decisions and stifles market growth, particularly for small and medium-sized enterprises operating on tighter budgets.

MARKET OPPORTUNITIES

Adoption of Recycled and Eco-Friendly Media

The growing emphasis on sustainability presents a lucrative opportunity for the North American sandblasting media market through the adoption of recycled and eco-friendly materials. Industries are increasingly turning to alternatives like crushed glass, walnut shells, and corn cobs, which offer comparable performance to traditional abrasives while minimizing environmental impact. According to the Environmental Protection Agency, recycling one ton of glass saves approximately 1,330 pounds of sand, reducing resource extraction and landfill waste. This shift aligns with corporate sustainability goals and consumer preferences for greener solutions. Moreover, governments are incentivizing the use of eco-friendly media through tax breaks and grants. For example, the U.S. Department of Agriculture offers funding under its Rural Energy for America Program to support sustainable practices.

Expansion into Emerging Applications

Another promising opportunity lies in expanding sandblasting media applications beyond traditional sectors into emerging fields like renewable energy and cultural heritage preservation. In the renewable energy sector, wind turbine maintenance requires regular surface treatments to combat corrosion and ensure optimal performance. According to the American Wind Energy Association, the U.S. installed over 13,000 megawatts of new wind capacity in 2022, creating a steady demand for specialized blasting solutions. Similarly, the preservation of historical monuments and artifacts involves precise sandblasting techniques to restore surfaces without causing damage.

MARKET CHALLENGES

High Initial Investment Costs

A foremost challenge facing the North American sandblasting media market is the substantial initial investment required for setting up advanced blasting equipment and infrastructure. Modern sandblasting systems, particularly those designed for eco-friendly media or precision applications, often involve sophisticated technologies such as robotic arms, automated containment units, and dust collection systems. This financial barrier disproportionately affects small and medium-sized enterprises, which may lack the capital to adopt cutting-edge solutions. Furthermore, the ongoing expenses associated with maintenance, training, and compliance with safety standards add to the financial burden. Also, a notable number of small manufacturers cite high upfront costs as a deterrent to adopting new technologies, thereby limiting market penetration and innovation.

Intense Competition and Price Wars

A further pressing challenge is the intense competition within the market, exacerbated by the presence of numerous players vying for market share. This competitive environment often leads to price wars, eroding profit margins and making it difficult for companies to sustain long-term growth. Smaller players frequently undercut prices to attract customers, while larger companies struggle to differentiate their offerings in a saturated market. Additionally, the influx of low-cost imports from countries like China and India further intensifies pricing pressures. The U.S. International Trade Commission reports that imported abrasives accounted for over 25% of the domestic market in 2022, driving down prices and squeezing local manufacturers.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

7.11% |

|

Segments Covered |

By Product, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

Us, Canada, And Rest of North America |

|

Market Leaders Profiled |

GMA Garnet Group, Saint-Gobain Abrasives, Harsco Corporation, ABShot Tecnics S.L., ALOX GmbH, Barton International, Abrasives Inc., Opta Minerals, Winoa Group, Kramer Industries, Inc., Blast-One International, AGSCO Corporation, U.S. Silica Holdings, Inc., American Industrial Minerals, Manus Abrasive Systems, Silica Holdings, Inc., Eurogrit B.V., Abrasive Products & Equipment, LLC, Graco Inc., Empire Abrasive Equipment Company |

SEGMENTAL ANALYSIS

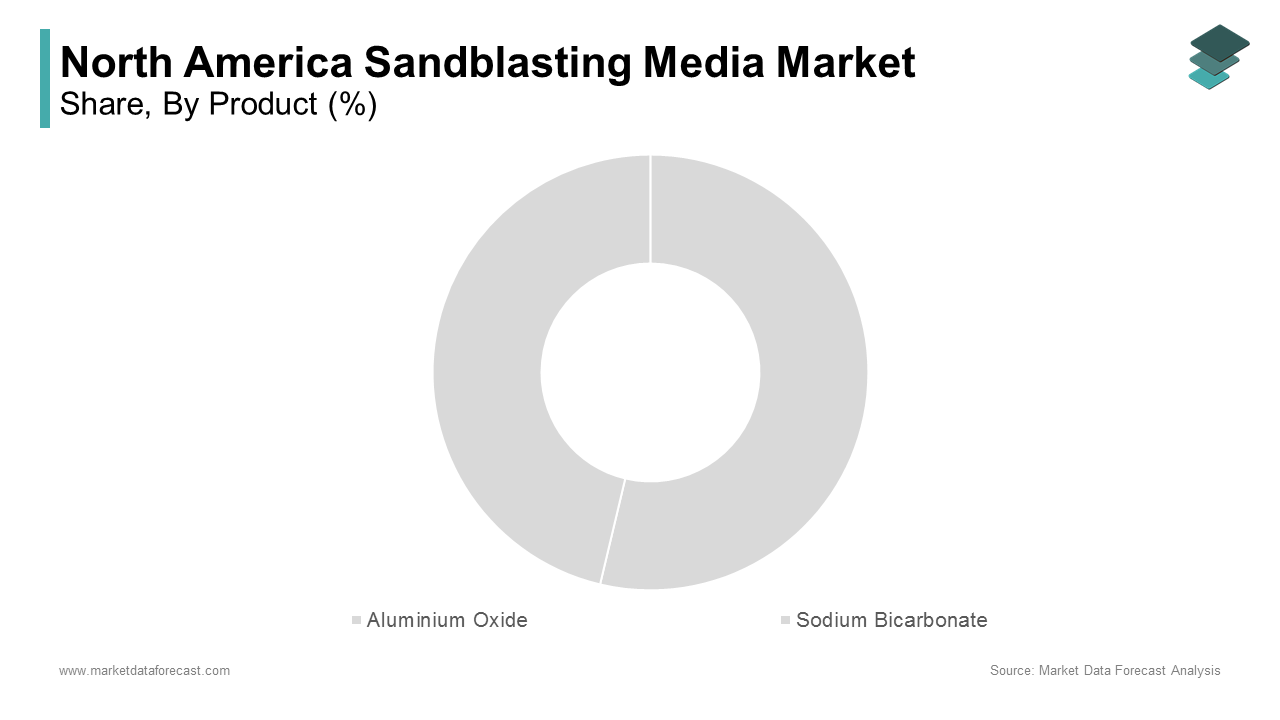

By Product Insights

The aluminum oxide segment dominated the North American sandblasting media market by commanding a market share of 25.6% in 2024. This is attributed to its exceptional hardness, recyclability, and versatility across industries such as aerospace, automotive, and metalworking. In addition, a key propelling aspect is its widespread use in the aerospace sector, where stringent quality standards necessitate high-performance abrasives. The U.S. Federal Aviation Administration estimates that over 30,000 aircraft undergo maintenance annually, with aluminum oxide being the abrasive of choice for turbine blade cleaning and airframe refurbishment.

One more factor bolstering its dominance is the growing demand for eco-friendly blasting solutions. Aluminum oxide can be reused multiple times, reducing waste and aligning with sustainability goals. Like, industries adopting reusable abrasives have greatly reduced landfill contributions. Furthermore, technological advancements in manufacturing processes have lowered production costs, making aluminum oxide more accessible.

Sodium bicarbonate is the fastest-growing segment in the North American sandblasting media market, with a projected CAGR of 7.5% from 2025 to 2033. This rapid growth is driven by its non-toxic and biodegradable properties, which cater to the rising demand for environmentally friendly alternatives. For instance, the National Park Service has utilized sodium bicarbonate to restore historic monuments, citing its ability to clean without etching or discoloration.

A second aspect propelling this growth is its suitability for sensitive applications, particularly in healthcare and electronics. Also, sodium bicarbonate is ideal for cleaning medical equipment due to its mildness and lack of residue. Additionally, the electronics industry uses it for PCB cleaning, ensuring no electrical conductivity issues arise post-treatment. Another driver is the increasing focus on workplace safety. The Occupational Safety and Health Administration reports that sodium bicarbonate generates significantly less dust compared to silica-based abrasives, reducing respiratory risks for workers. These attributes position sodium bicarbonate as a transformative solution in the evolving industrial landscape

By End-User Insights

The automotive industry represents the largest end-user segment in the North American sandblasting media market, with 30.5% of the total revenue share in 2024. This growth of the segment is because of the extensive use of sandblasting in surface preparation, rust removal, and coating applications critical to vehicle manufacturing and maintenance. A key factor is the shift toward lightweight materials like aluminum and carbon fiber, which require specialized blasting techniques to achieve optimal adhesion for coatings. Another contributing factor is the aftermarket segment, which relies heavily on sandblasting for refurbishing components such as engine blocks and wheels. Similarly, the U.S. automotive aftermarket is reflecting sustained demand for restoration services. Also, regulatory compliance plays a role; stringent emission standards necessitate regular maintenance of exhaust systems, often involving sandblasting.

The aerospace sector came up as the swiftest advancing end-user segment, with a CAGR of 8.2% predicted from 2025 to 2033. This development is influenced by the increasing complexity of aircraft designs and the need for precise surface treatments. Also, the global airline fleet is expected to double by 2040, with North America accounting for a significant share. This expansion drives demand for advanced abrasives capable of meeting aerospace-grade requirements. For example, aluminum oxide and garnet are widely used to clean turbine blades and prepare fuselages for painting, ensuring aerodynamic efficiency and corrosion resistance.

A different point is the rise in maintenance, repair, and overhaul (MRO) activities. Besides, the growing adoption of sustainable aviation initiatives promotes the use of eco-friendly blasting media. The International Air Transport Association notes that airlines aim to reduce carbon emissions by 50% by 2050, prompting manufacturers to adopt greener practices, including the use of recycled abrasives.

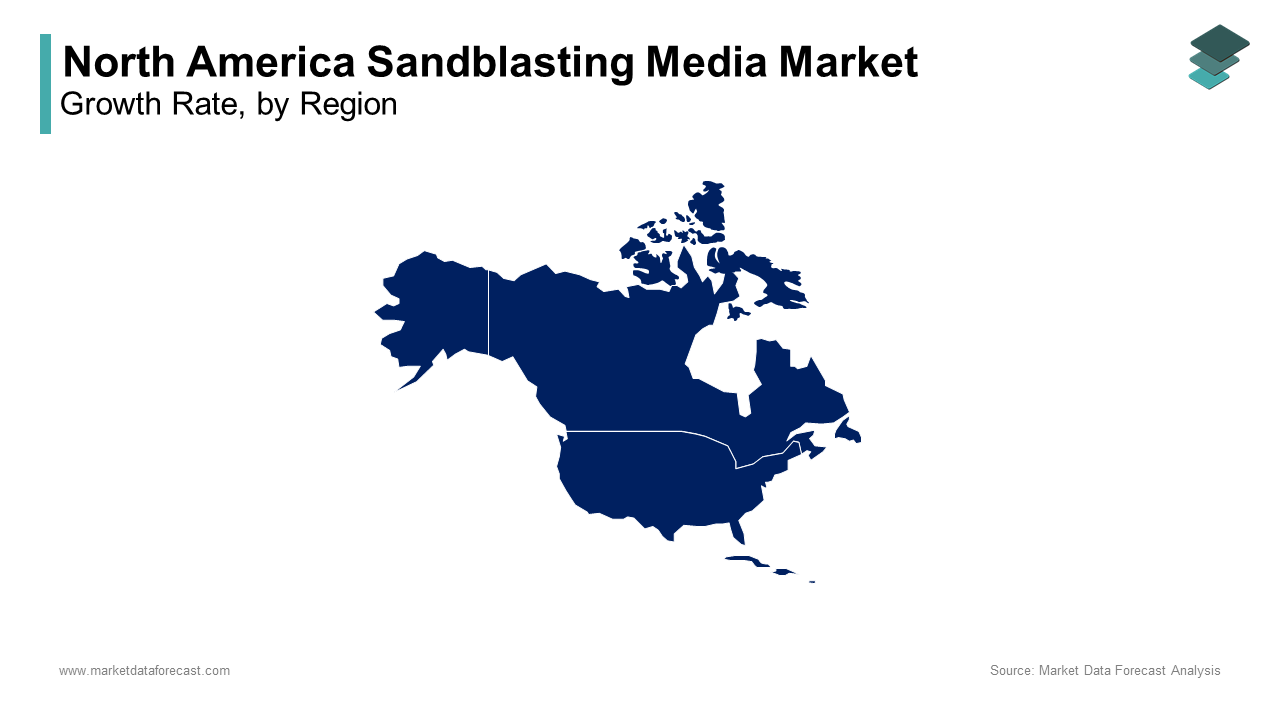

REGIONAL ANALYSIS

The United States spearheaded the North American sandblasting media market with a 70.5% of the regional share in 2024. It is rooted in a robust industrial base and significant investments in infrastructure development. Also, the U.S. government allocated USD 1.2 trillion for projects spanning roads, bridges, and public transit systems, all of which rely on sandblasting for surface preparation. Further, a main aspect is the country's leadership in the automotive sector, which produces over 10 million vehicles annually. This production volume fuels the demand for abrasives in manufacturing and aftermarket services.

Another factor is the stringent regulatory environment promoting safer and greener abrasives. The Occupational Safety and Health Administration mandates reduced exposure to silica dust, encouraging the adoption of alternatives like garnet and sodium bicarbonate. Similarly, recycling rates for industrial abrasives have increased majorly over the past decade, reflecting a shift toward sustainability.

Canada holds a market share of 20.6%. It is driven by the oil and gas sector, which accounts for a substantial portion of media consumption. Like, a substantial amount will be invested in pipeline projects by 2030, creating a steady demand for sandblasting in maintenance and corrosion prevention. Additionally, the country's cold climate necessitates regular surface treatments for infrastructure resilience, further boosting consumption.

A further crucial factor is Canada’s commitment to environmental sustainability. The federal government has introduced incentives for using eco-friendly abrasives, such as recycled glass and walnut shells. In addition, these initiatives have reduced industrial waste annually. Furthermore, the country’s strong manufacturing sector, particularly in Ontario and Quebec, supports demands for abrasives in metalworking and automotive applications. These elements position Canada as a vital contributor to the regional market.

Mexico holds a smaller but growing share of the North American sandblasting media market and is supported by its expanding manufacturing and construction sectors. In addition, the country’s manufacturing output grew in 2022, with automotive production being a key contributor. This industrial activity fuels the demand for abrasives in surface finishing and component refurbishment. Further, Mexico’s strategic location as a trade gateway between North and South America enhances its market potential.

A different aspect is the rising adoption of cost-effective abrasives, such as coal slag and iron slag, which align with budget constraints in emerging markets. Moreover, government initiatives to improve infrastructure, such as the Maya Train project, create new opportunities for sandblasting applications.

The Rest of North America contributes marginally to the market but shows potential for growth. Also, infrastructure investments in these regions are expected to rise in the coming years, driving demand for abrasives in construction and maintenance. Additionally, tourism-driven economies prioritize aesthetic restoration, increasing the use of media like sodium bicarbonate for heritage preservation.

One more factor is the growing emphasis on renewable energy projects, such as wind farms in the Caribbean. Similarly, renewable energy capacity in these regions is projected to expand notably by 2030, creating opportunities for specialized abrasives.

LEADING PLAYERS IN THE NORTH AMERICAN SANDBLASTING MEDIA MARKET

3M Company

3M Company is a global leader in industrial abrasives and has made significant contributions to the North American sandblasting media market through its innovative product portfolio. The company offers high-performance abrasives like aluminum oxide and garnet, catering to industries such as automotive, aerospace, and metalworking. In recent years, 3M has focused on sustainability by introducing eco-friendly media solutions, aligning with regulatory trends. Additionally, the company has invested in advanced manufacturing technologies to enhance product efficiency and reduce environmental impact. Its commitment to research and development ensures it remains at the forefront of industry advancements.

Saint-Gobain Abrasives

Saint-Gobain Abrasives is a key player renowned for its premium-quality blasting media, including silicon carbide and steel grit. The company has strengthened its position in North America by expanding its production facilities and enhancing supply chain capabilities. It focuses on delivering customized solutions tailored to specific industrial needs, particularly in the oil and gas sector. Recent initiatives include launching recyclable abrasives and collaborating with end-users to optimize surface preparation processes.

Barton International

Barton International specializes in high-performance garnet abrasives, widely used in sandblasting applications across North America. The company has established itself as a leader by ensuring consistent product quality and reliability. Barton has recently invested in expanding its distribution network to improve accessibility for customers in remote regions. Additionally, the company has partnered with environmental organizations to promote sustainable practices, such as recycling spent abrasives.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the North American sandblasting media market employ strategies such as product innovation, strategic partnerships, and sustainability initiatives to maintain their competitive edge. Product innovation involves developing advanced abrasives that meet evolving industry standards, particularly in eco-friendly materials like recycled glass and sodium bicarbonate. Strategic partnerships with end-users and distributors help companies expand their reach and tailor solutions to specific needs. Sustainability initiatives focus on reducing environmental impact through recyclable media and energy-efficient manufacturing processes. Additionally, investments in R&D and facility expansions enable firms to enhance production capacities and deliver high-quality products.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the North America sandblasting media market include GMA Garnet Group, Saint-Gobain Abrasives, Harsco Corporation, ABShot Tecnics S.L., ALOX GmbH, Barton International, Abrasives Inc., Opta Minerals, Winoa Group, Kramer Industries, Inc., Blast-One International, AGSCO Corporation, U.S. Silica Holdings, Inc., American Industrial Minerals, Manus Abrasive Systems, Silica Holdings, Inc., Eurogrit B.V., Abrasive Products & Equipment, LLC, Graco Inc., Empire Abrasive Equipment Company

The North American sandblasting media market is characterized by intense competition, driven by the presence of global leaders and regional players striving to innovate and capture market share. Companies are investing heavily in R&D to develop cutting-edge products, such as biodegradable abrasives and precision blasting solutions, to cater to diverse industrial needs. The market is also witnessing a surge in collaborations, mergers, and acquisitions, enabling firms to consolidate their positions and expand their portfolios. Regulatory pressures to adopt safer and greener alternatives have further intensified competition, pushing companies to align with sustainability goals. Additionally, price wars and aggressive marketing tactics are common, particularly among smaller players seeking to challenge established brands.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, 3M Company launched an eco-friendly line of aluminum oxide abrasives, designed to reduce environmental impact while maintaining high performance.

- In June 2023, Saint-Gobain Abrasives expanded its production facility in Ohio, USA, to meet rising demand for silicon carbide media in the oil and gas sector.

- In August 2023, Barton International partnered with a recycling firm to develop a closed-loop system for reusing spent garnet abrasives, promoting circular economy practices.

- In November 2023, Norton Saint-Gobain introduced a digital platform to streamline customer orders and provide real-time technical support for abrasive solutions.

- In February 2024, 3M acquired a startup specializing in sodium bicarbonate blasting technology, enhancing its portfolio for sensitive surface applications.

MARKET SEGMENTATION

This research report on the North American sandblasting media market has been segmented and sub-segmented based on product, end user, and region.

By Product

- Aluminium Oxide

- Sodium Bicarbonate

By End User

- Automotive

- Aerospace

By Region

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. How is the North America sandblasting media market expected to grow in the coming years?

The market is projected to grow steadily due to increasing industrial activities, rising demand for surface finishing in manufacturing, and growing construction and infrastructure development in the region.

2. What are the key drivers of market growth in North America?

Key drivers include rapid industrialization, increased demand for metal finishing, stricter surface preparation standards, and the rise in renovation and maintenance projects across industries.

3. Who are the key end-users of sandblasting media in this region?

Key end-users include the automotive industry, aerospace and defense, shipbuilding, oil & gas, construction, and metal fabrication sectors.

4. Which factors influence the selection of sandblasting media?

The choice of media depends on the surface material, the desired finish, abrasiveness, cost, and whether the media is reusable or disposable.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]