North America Renewable Diesel Market Size, Share, Trends & Growth Forecast Report By Feedstock Type (Waste Oils, Vegetable Oils), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis From 2025 to 2033.

North America Renewable Diesel Market Size

The size of the North America renewable diesel market was worth USD 4.35 billion in 2024. The North America market is anticipated to grow at a CAGR of 6.87% from 2025 to 2033 and be worth USD 7.91 billion by 2033 from USD 4.65 billion in 2025.

MARKET DRIVERS

Regulatory Support and Environmental Policies

Stringent environmental policies and regulatory frameworks are primary drivers of the renewable diesel market in North America. Governments across the region have implemented mandates to reduce greenhouse gas emissions and promote cleaner energy alternatives. For instance, the U.S. Renewable Fuel Standard (RFS) program, as per the EPA, mandates the blending of 36 billion gallons of renewable fuels into transportation fuels annually by 2025, with renewable diesel being a key contributor. Similarly, California’s Low Carbon Fuel Standard (LCFS) provides financial incentives for low-carbon fuels, driving demand for renewable diesel. These policies not only incentivize production but also encourage end-users, such as fleet operators and airlines, to adopt renewable diesel.

Growing Demand for Sustainable Aviation Fuel (SAF)

Another significant driver is the increasing demand for sustainable aviation fuel (SAF), a segment where renewable diesel plays a crucial role. As per the International Air Transport Association (IATA), the aviation industry aims to achieve net-zero carbon emissions by 2050, with SAF accounting for 65% of the required emission reductions. Renewable diesel, often referred to as “drop-in” fuel, can be blended with conventional jet fuel without requiring modifications to existing infrastructure or aircraft engines.

MARKET RESTRAINTS

High Production Costs and Feedstock Availability

One of the primary restraints impeding the growth of the renewable diesel market is the high production costs associated with feedstock procurement and processing. According to a study by BloombergNEF, the cost of producing renewable diesel can be up to 30% higher than conventional diesel due to the reliance on premium feedstocks like vegetable oils and waste fats. The availability of these feedstocks is also a concern, as per the U.S. Department of Agriculture, which reports that the supply of waste oils and animal fats is insufficient to meet the growing demand. Vegetable oils, while abundant, face competition from the food industry is leading to price volatility.

Infrastructure Limitations

Another significant restraint is the lack of adequate infrastructure to support widespread adoption of renewable diesel. Existing refineries and distribution networks are predominantly designed for conventional fossil fuels by necessitating substantial investments to accommodate renewable diesel. Additionally, the distribution network for renewable diesel remains underdeveloped in rural areas by limiting accessibility for end-users. As per a study by the National Renewable Energy Laboratory, less than 10% of fueling stations in the U.S. currently offer renewable diesel by creating logistical challenges for fleet operators and consumers.

MARKET OPPORTUNITIES

Expansion in Marine and Heavy-Duty Transportation

The marine and heavy-duty transportation sectors present significant opportunities for the renewable diesel market in North America. These industries are under increasing pressure to reduce carbon emissions by making renewable diesel an attractive alternative to conventional fuels. According to the International Maritime Organization (IMO), the shipping industry must reduce its carbon intensity by 40% by 2030 by driving demand for cleaner fuels. Renewable diesel, with its compatibility with existing engines and ability to reduce lifecycle emissions by up to 80%, is well-positioned to meet this demand. In 2022, Maersk announced a partnership with Neste to procure renewable diesel for its fleet, with the growing interest in sustainable maritime fuels. Similarly, heavy-duty trucking companies, such as Ryder System, are transitioning to renewable diesel to comply with state-level regulations like California’s LCFS.

Technological Advancements in Feedstock Diversification

Advancements in feedstock diversification represent another promising opportunity for the renewable diesel market. Researchers are exploring alternative feedstocks, such as algae and municipal solid waste, to address the limitations of traditional sources like vegetable oils and waste fats. According to a report by the U.S. Department of Energy, algae-based biofuels have the potential to replace up to 17% of U.S. imported oil by offering a sustainable and scalable solution. Additionally, startups like LanzaTech are developing technologies to convert industrial carbon emissions into renewable diesel by aligning with circular economy principles. A study by Lux Research estimates that advanced feedstocks could account for 30% of renewable diesel production by 2030 by reducing reliance on conventional feedstocks.

MARKET CHALLENGES

Competition from Electric Vehicles (EVs)

One of the foremost challenges facing the renewable diesel market is the growing competition from electric vehicles (EVs). The rapid adoption of EVs, driven by government incentives and advancements in battery technology, poses a threat to the long-term demand for renewable diesel. This shift is particularly evident in the passenger vehicle segment, where EVs are increasingly seen as a zero-emission alternative to internal combustion engines. The declining demand for liquid fuels in the passenger vehicle market could impact overall market growth.

Policy Uncertainty and Market Volatility

Another significant challenge is the uncertainty surrounding policy frameworks and market volatility. The changes in government priorities or shifts in political dominance could undermine these programs, while current regulations like the RFS and LCFS provide strong incentives for renewable diesel. According to the Congressional Budget Office, proposed amendments to the RFS program could reduce blending mandates by up to 20% by impacting demand for renewable diesel. Additionally, market volatility, driven by fluctuating feedstock prices and geopolitical tensions that creates financial risks for producers.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Feedstock Type, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

United States, Canada, Mexico, and the Rest of North America. |

|

Market Leaders Profiled |

Neste OYJ (Finland), Chevron Renewable Energy Group (U.S.), PBF Energy Inc. (U.S.), Valero Energy Corporation (U.S.), Gevo, Inc. (U.S.), and others |

SEGMENTAL ANALYSIS

By Feedstock Type Insights

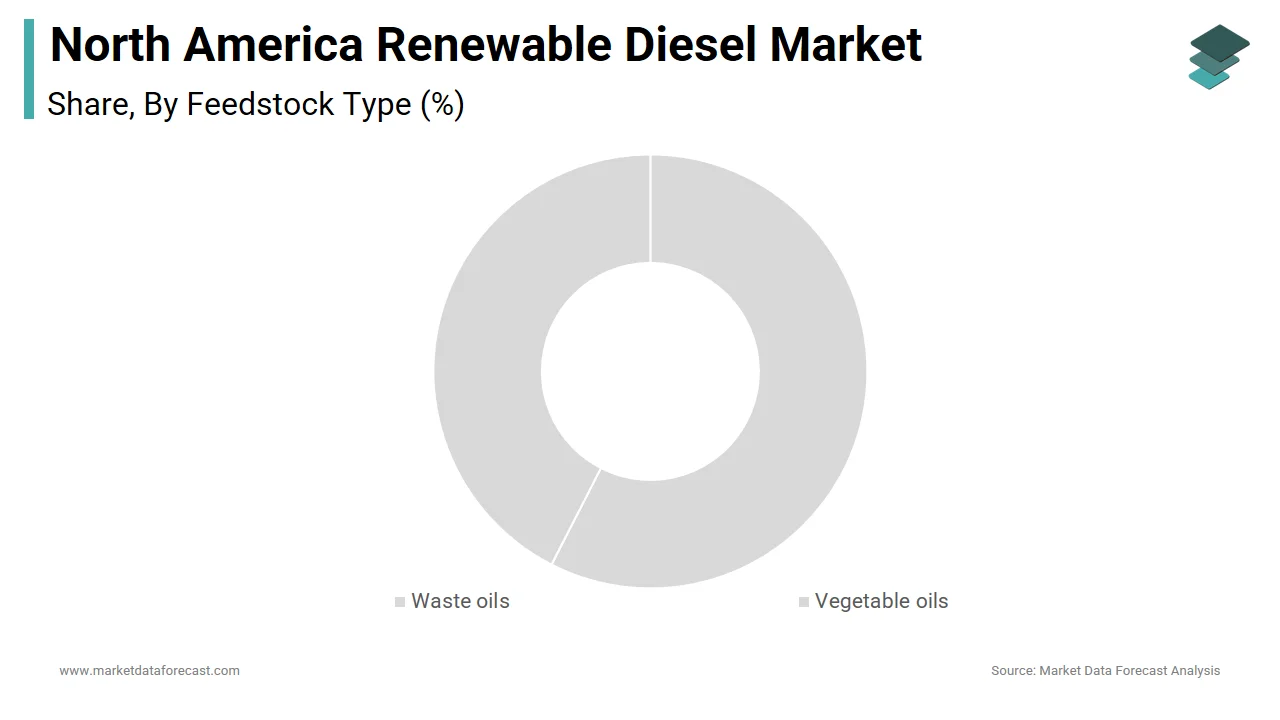

The waste oils segment was the largest and held 60.4% of the North American renewable diesel market share in 2024 due to their cost-effectiveness and alignment with circular economy principles. According to the U.S. Department of Energy, waste oils, including used cooking oil and animal fats, are widely available and generate fewer lifecycle emissions compared to vegetable oils. The segment’s growth is further driven by partnerships between renewable diesel producers and waste management companies.

The vegetable oils segment is projected to exhibit a CAGR of 18.4% throughout the forecast period. This growth is fueled by the increasing availability of soybean and canola oils in agricultural regions like the Midwest. Additionally, technological advancements enabling the co-processing of vegetable oils with waste fats have enhanced their appeal.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North America renewable diesel market by accounting for 80.6% of the share in 2024 owing to the country’s robust regulatory framework, which includes federal mandates like the Renewable Fuel Standard (RFS) program and state-level initiatives such as California’s Low Carbon Fuel Standard (LCFS). According to the Environmental Protection Agency (EPA), the U.S. produced over 1 billion gallons of renewable diesel in 2022, driven by investments in sustainable fuels and decarbonization goals. Additionally, the Biden administration’s commitment to achieving net-zero emissions by 2050 has spurred investments in renewable diesel infrastructure, with companies investing over $4 billion in new refineries and retrofit projects.

Canada held 15.4% of the North American renewable diesel market share in 2024 by aiming to achieve net-zero emissions by 2050, with renewable diesel playing a pivotal role in reducing carbon intensity in the transportation sector. The province of Alberta has emerged as a leader in renewable diesel production due to its abundant feedstock resources, including canola oil and animal fats. Furthermore, Canada’s Clean Fuel Regulations, introduced in 2022, mandate a 15% reduction in the carbon intensity of liquid fuels by 2030 by creating a favorable environment for renewable diesel adoption.

MARKET KEY PLAYERS

Companies playing a dominant role in the North America renewable diesel market profiled in this report are Neste OYJ (Finland), Chevron Renewable Energy Group (U.S.), PBF Energy Inc. (U.S.), Valero Energy Corporation (U.S.), Gevo, Inc. (U.S.), and others

TOP LEADING PLAYERS IN THE MARKET

Neste Corporation

Neste Corporation is a global leader in the North America renewable diesel market. The company’s dominance stems from its innovative approach to feedstock diversification and its focus on sustainability. In 2022, Neste launched a pilot project to produce renewable diesel from algae-based feedstocks, aligning with its goal to reduce reliance on traditional vegetable oils and waste fats. The company’s partnership with Darling Ingredients, a leading supplier of waste oils, ensures a stable and cost-effective feedstock supply chain. Neste’s strategic investments in refining capacity, including the expansion of its Rotterdam facility, have enabled it to meet growing demand across North America.

Valero Energy Corporation

Valero Energy Corporation is another prominent player. The company’s success lies in its ability to leverage its extensive refinery network to co-process renewable diesel with conventional fuels. In 2023, Valero completed the retrofit of its St. Charles refinery in Louisiana, increasing its renewable diesel production capacity by 50%. Additionally, the company’s partnership with Darling Ingredients to secure waste oils and animal fats has strengthened its feedstock procurement capabilities. Valero’s focus on scalability and efficiency has positioned it as a key player in the competitive renewable diesel market.

World Energy

World Energy specializes in producing renewable diesel for aviation and marine applications, addressing the unique needs of hard-to-abate sectors. In 2023, World Energy announced a $500 million investment to expand its renewable diesel refinery in Paramount, California, positioning itself as a leader in sustainable aviation fuel (SAF) production. The company’s collaboration with major airlines, such as United Airlines, promotes its ability to meet the stringent requirements of the aviation industry. World Energy has carved out a distinct niche in the renewable diesel market by catering to segments often overlooked by larger competitors.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the North American renewable diesel market employ a variety of strategies to maintain their competitive edge and drive growth. One prevalent strategy is feedstock diversification, with companies exploring alternative sources such as algae, municipal solid waste, and agricultural residues to address limitations associated with traditional feedstocks. For instance, Neste Corporation’s pilot project to produce renewable diesel from algae-based feedstocks exemplifies this approach. Another widely adopted strategy is forming strategic partnerships with feedstock suppliers, technology providers, and end-users to create a seamless value chain. Valero Energy Corporation’s collaboration with Darling Ingredients promotes this trend by ensuring a stable and cost-effective feedstock supply. Geographic expansion is also a critical focus, with companies investing in new refineries and retrofitting existing facilities to enhance production capacity. Lastly, companies emphasize sustainability and compliance with regulatory frameworks by leveraging incentives like LCFS credits to improve profitability. These strategies collectively enable players to address diverse market demands while staying ahead in a highly competitive landscape.

COMPETITION OVERVIEW

The North American renewable diesel market is characterized by intense competition, with key players vying for dominance through innovation, quality, and strategic initiatives. Companies like Neste Corporation, Valero Energy Corporation, and World Energy dominate the landscape, each leveraging unique strengths to capture market share. Neste leads the pack with its cutting-edge feedstock diversification strategies and global presence by allowing it to cater to large-scale projects in sectors like aviation and marine transportation. Valero differentiates itself through its extensive refinery network and focus on co-processing renewable diesel with conventional fuels, enabling it to scale production efficiently. World Energy excels in providing tailored solutions for niche markets, particularly aviation and marine applications, appealing to customers seeking high-performance fuels. Despite their individual strengths, all players face challenges such as policy uncertainty, feedstock availability, and competition from electric vehicles.

RECENT MARKET DEVELOPMENTS

- In April 2024, Neste Corporation launched a pilot project to produce renewable diesel from algae-based feedstocks, enhancing feedstock diversity and reducing reliance on traditional sources.

- In June 2023, Valero Energy Corporation partnered with Darling Ingredients to secure a stable supply of waste oils and animal fats, strengthening its feedstock procurement capabilities.

- In March 2023, World Energy announced a $500 million investment to expand its renewable diesel refinery in California, positioning itself as a leader in sustainable aviation fuel production.

- In January 2023, Neste acquired a Canadian waste management firm to bolster its feedstock supply chain and expand its geographic presence in North America.

- In October 2022, Valero completed the retrofit of its St. Charles refinery in Louisiana, increasing its renewable diesel production capacity by 50% to meet growing demand.

MARKET SEGMENTATION

This research report on the North America renewable diesel market is segmented and sub-segmented into the following categories.

By Feedstock Type

- Waste oils

- Vegetable oils

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What factors are driving the growth of the renewable diesel market in North America?

Growth is driven by stringent environmental policies, government mandates for low-carbon fuels, and increasing demand from sectors like transportation and aviation for sustainable fuel alternatives.

2. What are the main challenges facing the renewable diesel market in this region?

The market faces challenges such as high production costs, limited feedstock availability, underdeveloped distribution infrastructure, and competition from electric vehicles and policy uncertainties.

3. What opportunities are emerging in the North America renewable diesel market?

Significant opportunities include expanding use in marine and heavy-duty transportation, advancements in alternative feedstocks like algae and municipal waste, and partnerships to secure stable supply chains and scale production.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]