North America Power Tools Market Research Report - Segmentation By Tool Type (Material Removal, Drilling & Fastening), End-Use (Construction, House Hold/Residential Use), Power Source (Pneumatic Power Tools, Electric Power Tools), Industry Analysis on Size, Share, Trends, Growth, Landscape & Forecast ( 2025 to 2033).

North America Power Tools Market Size

The size of the north america power tools market was worth USD 9.76 billion in 2024. The north america market is anticipated to grow at a CAGR of 3.70% from 2024 to 2033 and be worth USD 13.54 billion by 2033 from USD 10.12 billion in 2025.

Power tools, which include electric, pneumatic, and hydraulic devices, are utilized to enhance productivity and efficiency in tasks ranging from drilling and cutting to fastening and demolition. The market has been experiencing robust growth owing to the increasing construction activities, rising DIY trends, and advancements in technology that enhance tool performance and user experience. This growth is further supported by the increasing adoption of cordless power tools, which offer greater convenience and flexibility for users. As the market continues to evolve, manufacturers are focusing on innovation, sustainability, and smart technologies to meet the changing demands of consumers and professionals alike by positioning the North America power tools market for continued expansion.

MARKET DRIVERS

Surge in Construction Activities

A significant driver of the North America power tools market is the surge in construction activities across the region. The construction industry has been experiencing a renaissance is fueled by increased investments in infrastructure, residential, and commercial projects. According to the U.S. Census Bureau, construction spending in the United States reached approximately $1.6 trillion in 2022 by reflecting a robust growth trajectory. This expansion is driven by various factors, including government initiatives aimed at improving infrastructure, rising housing demand, and the need for commercial space in urban areas. The demand for power tools is expected to rise correspondingly as construction projects become more complex and require specialized tools. Additionally, the trend towards smart construction practices, which emphasize efficiency and sustainability, is further propelling the adoption of advanced power tools that enhance productivity on job sites.

Growing DIY Culture

The growing do-it-yourself (DIY) culture among consumers is another major driver of the North America power tools market. The demand for power tools has surged as more individuals take on home improvement projects, renovations, and repairs. According to a survey conducted by the Home Improvement Research Institute, approximately 75% of U.S. homeowners engaged in DIY projects in 2022, with many citing the desire to personalize their living spaces and save on labor costs as key motivators. This trend has led to increased sales of power tools among novice users who seek user-friendly and versatile equipment. Retailers have responded to this demand by expanding their offerings of power tools and accessories by catering to a wide range of skill levels and project types. Furthermore, the proliferation of online tutorials and DIY content on social media platforms has empowered consumers to undertake more ambitious projects that further drives the need for reliable and efficient power tools. The North America power tools market is expected to experience sustained growth, with manufacturers focusing on developing tools that appeal to this expanding consumer base, as per the Home Improvement Research Institute.

MARKET RESTRAINTS

High Cost of Power Tools

One of the primary restraints affecting the North America power tools market is the high cost associated with purchasing quality power tools. The initial investment required for high-performance equipment can be a significant barrier for many consumers for those engaging in DIY projects. According to industry estimates, the average cost of a professional-grade power tool can range from $100 to $1,000 or more by depending on the type and specifications of the tool. This financial consideration can deter potential buyers, especially those who may be uncertain about their long-term commitment to DIY projects or professional use. Additionally, the economic impact of the COVID-19 pandemic has led to increased financial constraints for many households that further limits discretionary spending on power tools. As a result, consumers may opt for lower-cost alternatives or delay their purchases altogether that can hinder market growth. To address this challenge, power tool manufacturers and retailers may need to explore financing options, promotions, or bundled packages to make their products more accessible to a broader audience, as noted by the National Retail Federation.

Intense Competition and Market Saturation

The intense competition between the market players can pose challenges for manufacturers and retailers that is likely to hinder the growth of the North America power tools market. The market is populated by a mix of established global brands and emerging local players, each vying for market share in a competitive landscape. This competitive environment can lead to price wars, which may erode profit margins and compel companies to invest heavily in marketing and innovation to differentiate their offerings. Additionally, the rapid pace of technological advancements necessitates continuous investment in research and development. Smaller companies may struggle to compete with larger firms that have greater access to capital and established brand recognition. The intense competition in the power tools market can pose challenges for companies seeking to maintain profitability and market position.

MARKET OPPORTUNITIES

Technological Advancements in Power Tools

The North America power tools market presents significant opportunities driven by technological advancements that enhance the performance and functionality of power tools. Innovations such as brushless motors, smart technology integration, and improved battery technology are transforming the landscape of power tools, making them more efficient, durable, and user-friendly. Smart power tools equipped with IoT capabilities allow users to monitor performance, receive maintenance alerts, and optimize usage, thereby enhancing productivity and safety on job sites. Additionally, advancements in battery technology, such as lithium-ion batteries that have led to longer run times and faster charging by making cordless power tools more appealing to consumers. The market is expected to benefit from these technological advancements as manufacturers continue to invest in research and development to enhance power tool performance.

Expansion of E-commerce and Online Retail

The expansion of e-commerce and online retail channels represents another major opportunity for the North America power tools market. The demand for power tools through digital channels is expected to rise significantly as consumer purchasing behavior shifts towards online platforms. According to a report by eMarketer, U.S. e-commerce sales in the home improvement sector grew by over 30% in 2021 with a growing trend of consumers seeking convenience and accessibility in their shopping experiences. Online retailers offer a wide range of power tools, often at competitive prices, and provide consumers with the ability to compare products, read reviews, and access detailed specifications. Additionally, the COVID-19 pandemic has accelerated the shift towards online shopping, as many consumers turned to e-commerce for their home improvement needs during lockdowns. The power tool manufacturers and retailers can capitalize on this trend by enhancing their digital presence and offering tailored promotions to attract online shoppers. This shift towards e-commerce presents a significant growth opportunity for the North America power tools market, as per the Home Improvement Research Institute.

MARKET CHALLENGES

Supply Chain Disruptions

The North America power tools market faces significant challenges from supply chain disruptions, particularly in the wake of the COVID-19 pandemic. The power tools market relies on a complex network of suppliers for components and materials, and the pandemic has exposed vulnerabilities in these supply chains. According to a survey conducted by the National Association of Manufacturers, nearly 80% of manufacturers reported supply chain disruptions due to the pandemic is leading to delays in production and project timelines. These disruptions can result in increased costs for power tool manufacturers, as they may need to source materials from alternative suppliers or expedite shipping to meet project deadlines. Additionally, the ongoing global semiconductor shortage has further exacerbated supply chain challenges by impacting the availability of critical components for power tools. They may face difficulties in fulfilling orders and maintaining customer satisfaction companies navigate these disruptions which can hinder growth and market expansion. The need for robust supply chain management strategies has become increasingly important for power tool companies to mitigate the impact of these challenges, as noted by the Equipment Leasing and Finance Association.

Regulatory Compliance and Safety Standards

The North America power tools market is also constrained by stringent regulatory compliance and safety standards that must be adhered to during the design, manufacturing, and distribution of power tools. Various federal and state regulations govern safety standards, emissions, and environmental impact by imposing rigorous requirements on power tool manufacturers. According to the Occupational Safety and Health Administration, compliance with safety regulations can require significant investments in testing, certification, and quality control processes. These regulatory requirements can create barriers to entry for smaller manufacturers and increase operational costs for established companies. Additionally, the evolving nature of safety regulations can create uncertainty for power tool manufacturers, as they must continuously adapt to new standards and ensure that their products remain compliant. This regulatory burden can deter some companies from investing in new product development or limit the ability of existing players to innovate and expand their offerings.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.70 % |

|

Segments Covered |

By Tool Type,End-Use,Power Source and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

The U.S., Canada and Rest of North America |

|

Market Leader Profiled |

Stanley Black & Decker (US), Techtronic Industries (Hong Kong), Robert Bosch (Germany), Makita Corporation (Japan) |

SEGMENTAL ANALYSIS

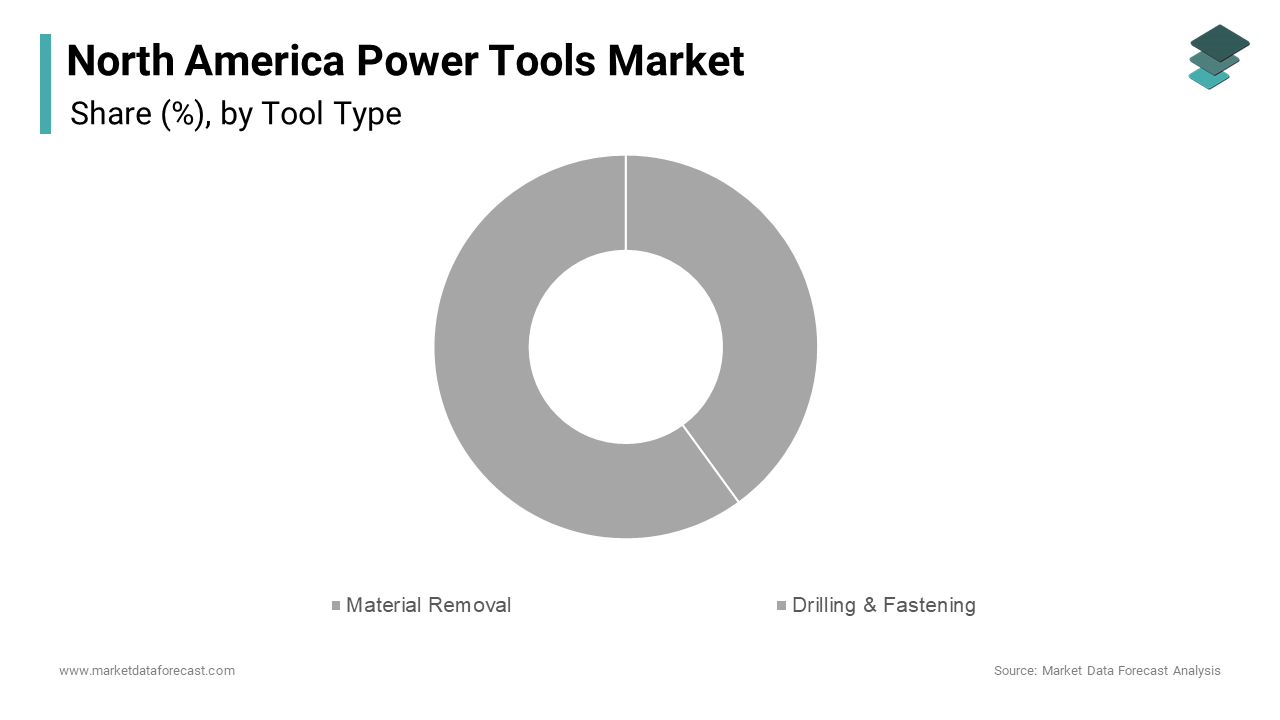

By Tool Type Insights

The material removal segment was the largest and held 40.1% of the North America power tools market share in 2024 owing to the widespread use of material removal tools, such as grinders, sanders, and saws, in various applications, including construction, woodworking, and metalworking. The versatility of material removal tools makes them essential for a wide range of tasks, from surface preparation to finishing, which further enhances their appeal among professionals and DIY enthusiasts alike. Additionally, the growing trend of home improvement and renovation projects is driving the demand for material removal tools, as consumers seek to undertake more complex tasks in their homes.

The drilling and fastening segment is projected to grow at a CAGR of 6.4% from 2025 to 2033. This growth can be attributed to the increasing demand for drilling and fastening tools in both residential and commercial applications. The versatility of drilling and fastening tools, such as cordless drills and impact drivers that makes them essential for a wide range of tasks from assembling furniture to installing fixtures. Additionally, advancements in battery technology and tool design are enhancing the performance and convenience of these tools.

By End-Use Insights

The construction segment was accounted by holding 50.3% of the North America power tools market share in 2024. This dominance is primarily driven by the increasing construction activities across the region, fueled by rising investments in residential, commercial, and infrastructure projects. According to the U.S. Census Bureau, construction spending in the United States reached approximately $1.6 trillion in 2022. The demand for power tools in construction applications is further fueled by the need for efficiency and productivity on job sites, where high-quality tools are essential for completing tasks quickly and effectively. The growing trend of smart construction practices, which emphasize the use of advanced tools and technologies that is driving the adoption of power tools that enhance productivity and safety.

The household/residential segment is projected to grow at a CAGR of 7.5% from 2025 to 2033. This growth can be attributed to the increasing interest in DIY home improvement projects among consumers in the wake of the COVID-19 pandemic, which prompted many individuals to invest in personal fitness equipment for home use. The convenience and flexibility of home improvement projects have made them increasingly appealing for those with busy schedules or limited access to traditional contractors. The demand for power tools tailored to residential applications is anticipated to rise significantly as the trend towards DIY home improvement continues to gain traction.

By Power Source Insights

The electric power tools segment was the largest by capturing a significant share in the North America power tools market in 2024. This dominance is primarily driven by the widespread adoption of electric power tools in both professional and DIY applications, owing to their convenience, efficiency, and availability. The electric power tools segment is projected to reach a valuation of $10 billion by 2025 that is fueled by the increasing demand for tools such as drills, saws, and grinders that operate on electric power. The advantages of electric power tools, including consistent performance and reduced noise levels compared to their pneumatic counterparts to make them a preferred choice for a wide range of tasks. Additionally, advancements in battery technology have led to the rise of cordless electric tools that further enhancing their appeal among consumers seeking flexibility and portability.

The pneumatic power tools segment is likely to experience to grow at a CAGR of 5.4% from 2025 to 2033. This growth can be attributed to the increasing demand for pneumatic tools in industrial and automotive applications, where high power-to-weight ratios and durability are essential. Pneumatic tools, which are powered by compressed air, offer several advantages, including lightweight design, high torque output, and reduced risk of electric shock, making them ideal for heavy-duty applications. The automotive industry, in particular, has seen a significant increase in the use of pneumatic tools for tasks such as assembly, painting, and maintenance, as they provide the necessary power and efficiency to meet production demands. Additionally, the growing trend of automation in industrial settings is further propelling the demand for pneumatic tools, as they can be easily integrated into automated systems.

Country Level Analysis

The United States dominated in the North America power tools market by holding a substantial share of 75.6% in 2024. The U.S. power tools market is characterized by its size and diversity, with significant investments in construction, manufacturing, and home improvement sectors. According to the U.S. Census Bureau, construction spending in the United States reached approximately $1.6 trillion in 2022. The demand for power tools is driven by the increasing focus on health and wellness among the population with a growing number of individuals seeking to improve their fitness levels and overall well-being. Additionally, the rise of digital fitness solutions and home workout trends has further stimulated the market as consumers invest in personal fitness equipment to support their health goals. The U.S. market is also characterized by a high level of innovation with manufacturers continuously introducing advanced fitness technologies and smart equipment to meet the evolving needs of consumers.

Canada power tools market is likely to showcase a lucrative growth rate with an estimated CAGR of 5.8% during the forecast period. The Canadian power tools market has been experiencing steady growth, driven by increasing health awareness and a rising number of fitness facilities. According to Statistics Canada, the number of fitness and recreational sports centers in the country reached over 6,000 in 2022 by reflecting a growing interest in health and wellness among Canadians. The demand for power tools in Canada is influenced by the need for specialized machinery to meet the diverse requirements of fitness enthusiasts and commercial establishments. Additionally, the increasing focus on preventive healthcare and the promotion of active lifestyles are prompting consumers to invest in fitness solutions. The demand for innovative and high-quality fitness equipment is expected to grow as the Canadian fitness market continues to evolve.

KEY MARKET PLAYERS

The key players of the North America Power Tools Market include Stanley Black & Decker (US), Techtronic Industries (Hong Kong), Robert Bosch (Germany), Makita Corporation (Japan), Hilti Corporation (Liechtenstein), Atlas Copco (Sweden), Apex Tool Group (US), Ingersoll-Rand (Ireland), KOKI Holdings (Japan), and Snap-on Incorporated (US)

MARKET SEGMENTATION

This research report on the North America Power Tools Market has been segmented and sub-segmented into the following categories.

By Tool Type

- Material Removal

- Drilling & Fastening

By End-Use

- Construction

- House Hold/Residential Use

By Power Source

- Pneumatic Power Tools

- Electric Power Tools

By Country

- US

- Canada

- Rest of North America

Frequently Asked Questions

What are the key applications of power tools in North America?

Power tools are extensively used in construction, automotive, aerospace, and shipbuilding sectors.

What is the impact of technological advancements on the power tools market?

Advancements like battery-powered and cordless tools have enhanced portability and efficiency, boosting market growth.

What challenges does the power tools market face in North America?

Challenges include high maintenance costs and fluctuations in raw material prices.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]