North America Polyisoprene Market Research Report – Segmented By Application ( tires & related products, footwear ) and Country (The U.S., Canada and Rest of North America) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts 2025 to 2033.

North America Polyisoprene Market Size

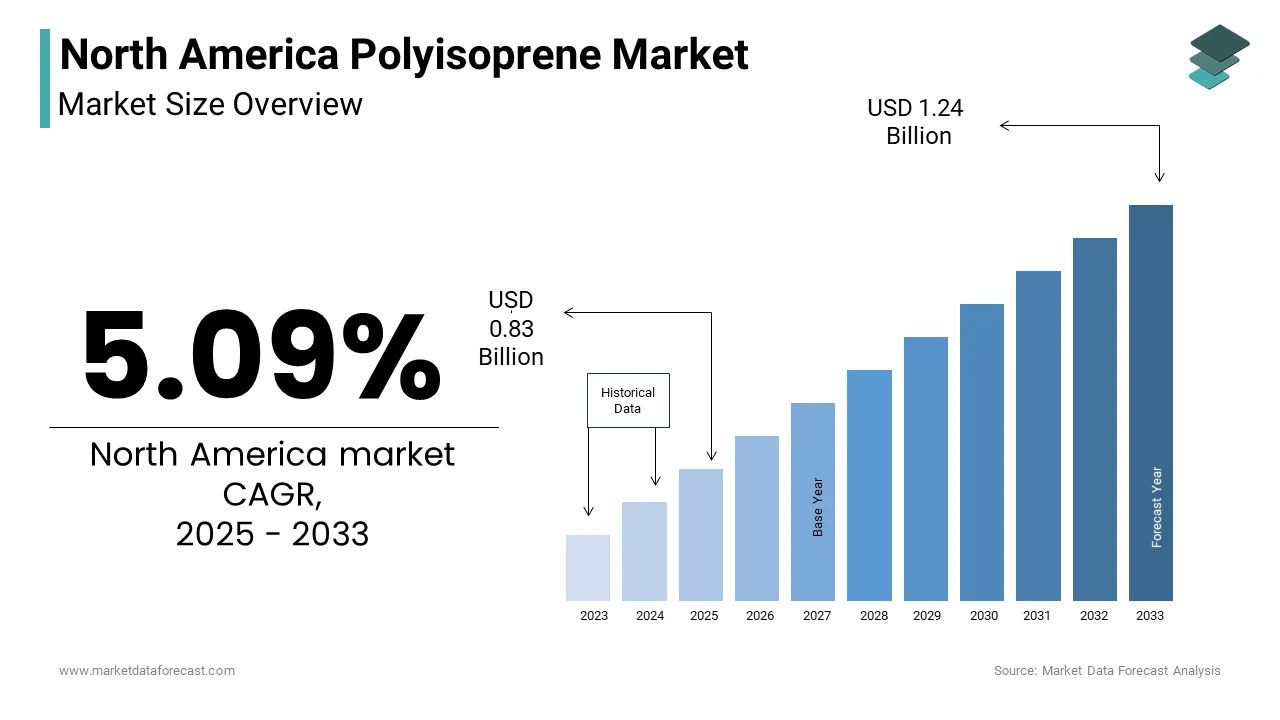

The North America Polyisoprene Market Size was valued at USD 0.79 billion in 2024. The North America Polyisoprene Market size is expected to have 5.09 % CAGR from 2025 to 2033 and be worth USD 1.24 billion by 2033 from USD 0.83 billion in 2025.

MARKET DRIVERS

Rising Demand in the Automotive Sector

The automotive industry is a primary driver of the North America polyisoprene market. Polyisoprene is widely used in tire manufacturing due to its exceptional elasticity, tear resistance, and durability. The growing emphasis on fuel-efficient vehicles has spurred demand for lightweight tires, with a notable increase in eco-friendly tire production. Additionally, the rise in electric vehicle (EV) adoption has further amplified polyisoprene usage, as EVs require specialized tires to handle increased torque and weight. According to the International Energy Agency, EV sales in North America surged considerably in recent years, creating sustained demand for advanced tire materials.

Expansion in Medical and Healthcare Applications

Polyisoprene’s biocompatibility and hypoallergenic properties make it a preferred material for medical gloves and devices. The healthcare sector accounts for a key share of polyisoprene demand. The COVID-19 pandemic accelerated this trend, with medical glove production rapidly increasing globally in 2020. Furthermore, the aging population in North America, projected to grow significantly by 2030, according to the U.S. Census Bureau, is expected to drive demand for medical-grade polyisoprene products. These factors show the material's critical role in meeting healthcare needs and expanding its application scope.

MARKET RESTRAINTS

High Production Costs

High production costs pose a significant challenge to the North America polyisoprene market, primarily due to the expensive polymerization process required to synthesize polyisoprene. This cost disparity often forces manufacturers to absorb thinner profit margins or pass expenses onto consumers and is thereby limiting market penetration. Additionally, fluctuations in raw material prices, particularly isoprene monomers, exacerbate cost volatility. Like, isoprene prices rose in 2022, further straining producers. Such economic pressures hinder the competitiveness of polyisoprene against cheaper alternatives.

Environmental Concerns and Regulatory Pressures

Environmental concerns and stringent regulations present another major restraint for the polyisoprene market. The production process generates significant greenhouse gas emissions are prompting regulatory bodies like the Environmental Protection Agency to impose strict emission limits. Similarly, compliance costs for manufacturers surged in recent years, impacting operational efficiency. Furthermore, public scrutiny over non-biodegradable synthetic materials has led to calls for greener alternatives, reducing polyisoprene’s appeal in certain applications. These regulatory and environmental challenges necessitate innovation in sustainable production methods to ensure long-term viability.

MARKET OPPORTUNITIES

Growth in Green Tire Technology

Green tire technology represents a significant opportunity for the North America polyisoprene market, driven by increasing demand for fuel-efficient and eco-friendly tires. Also, green tires account for a considerable percentage of the tire market, with projections indicating an annual growth rate in the coming years. Polyisoprene’s superior elasticity and low rolling resistance make it an ideal material for these tires, enabling improvement in fuel efficiency. The shift toward sustainability aligns with consumer preferences and regulatory mandates, creating a lucrative niche for polyisoprene producers.

Advancements in Biobased Polyisoprene

Biobased polyisoprene production is emerging as a transformative opportunity. It is driven by the need for renewable alternatives. Companies like Genomatica have developed bio-based isoprene derived from plant sugars, achieving a key reduction in carbon emissions. By adopting biobased technologies, polyisoprene manufacturers can cater to environmentally conscious consumers while complying with stringent environmental norms. This shift not only enhances brand reputation but also positions companies as leaders in the circular economy.

MARKET CHALLENGES

Competition from Natural Rubber

Competition from natural rubber remains a persistent challenge for the North America polyisoprene market. Natural rubber is significantly cheaper and widely available, representing a significant portion of global rubber consumption. In 2023, natural rubber prices dropped, making it an attractive alternative for cost-sensitive industries. Additionally, the perception of natural rubber as a more sustainable option further erodes polyisoprene’s market share. So, overcoming this challenge requires innovation in performance-enhancing additives and strategic pricing models to differentiate synthetic polyisoprene.

Supply Chain Vulnerabilities

Supply chain vulnerabilities pose another significant challenge, particularly concerning raw material availability. Isoprene monomers is a key feedstock for polyisoprene and are derived from petroleum is making the market susceptible to crude oil price fluctuations. Geopolitical tensions and trade restrictions further exacerbate supply disruptions, forcing manufacturers to operate below capacity. Addressing these logistical complexities requires investments in localized sourcing and diversified supply chain strategies to ensure market stability.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.09 % |

|

Segments Covered |

By Application and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

The U.S., Canada and Rest of North America |

|

Market Leader Profiled |

Zeon Corp, JSR Corp, Goodyear Tire & Rubber Co, Kuraray Co Ltd |

SEGMENTAL ANALYSIS

By Application Insights

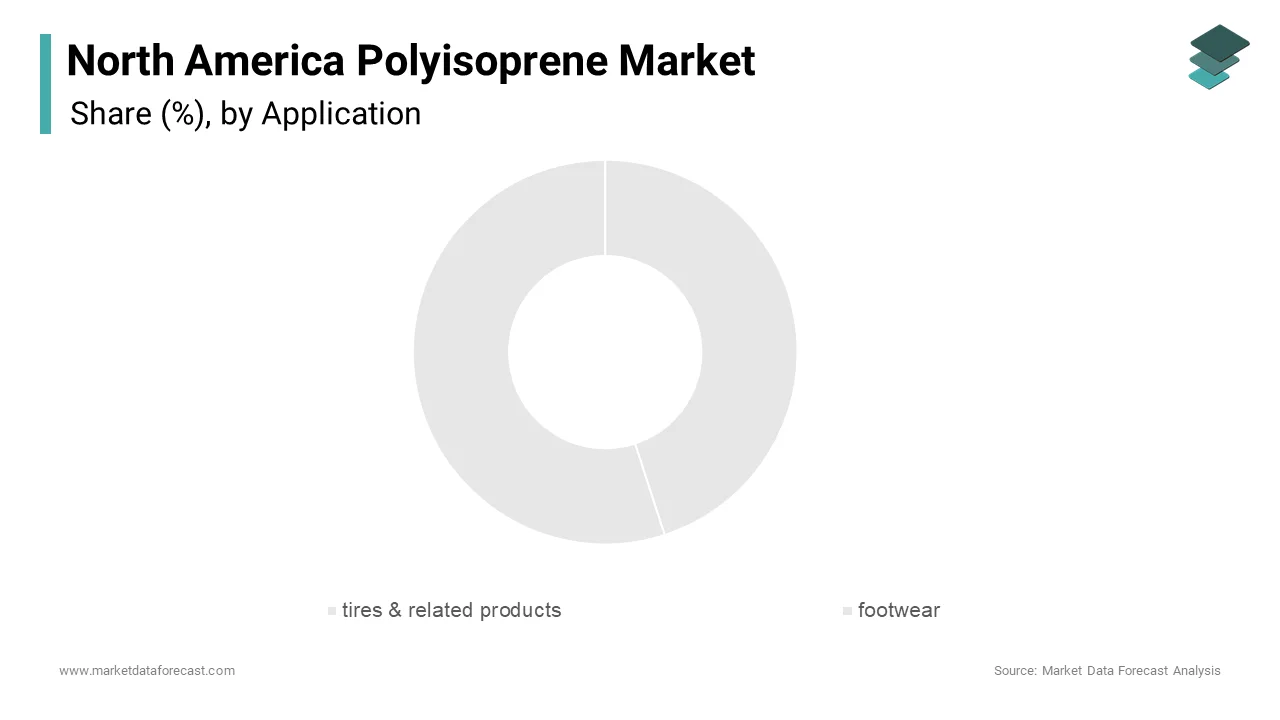

The tires & related products segment dominated the North America polyisoprene market and accounted for 45.5% of total consumption in 2024. This rise of the segment is credited to the material’s exceptional elasticity and durability, which are critical for high-performance tires. Also, the automotive sector’s shift toward fuel-efficient and electric vehicles (EVs) has further amplified demand, with EV tire production projected to grow considerably in the next few years. Apart from these, the rise in green tire technology, which reduces rolling resistance and improves fuel efficiency, has created a niche for polyisoprene. These factors reinforce the segment’s position as the market leader, supported by its versatility and widespread applications.

On the other hand, the footwear segment is the fastest-growing, registering a CAGR of 7.2% from 2025 to 2033. This acceleration is fueled by rising demand for comfortable and durable athletic shoes, which account for key share of footwear applications. Like, the global athletic footwear landscape is projected to expand in the coming years. Polyisoprene’s flexibility and shock-absorbing properties make it ideal for shoe soles, enhancing comfort and performance. Additionally, the growing popularity of sustainable footwear, incorporating biobased polyisoprene, has expanded its application scope, driving rapid market expansion.

COUNTRY LEVEL ANALYSIS

The United States was the cornerstone of the North America polyisoprene market with a 70.6% share in 2024. This leading position is caused by the country’s advanced industrial infrastructure, robust automotive sector, and growing healthcare industry. The U.S. automotive sector, which accounts for a significant portion of polyisoprene consumption, has been a primary driver of demand. For instance, the shift toward fuel-efficient and electric vehicles (EVs) has amplified the need for high-performance tires, with EV tire production projected to grow considerably. Additionally, the healthcare sector’s reliance on polyisoprene for medical gloves and devices has surged due to the ongoing emphasis on hygiene and safety. Furthermore, federal initiatives like the Infrastructure Investment and Jobs Act have indirectly bolstered demand for polyisoprene in construction-related applications such as seals and gaskets.

Canada is moving forward by leveraging its focus on sustainable materials and renewable feedstocks to carve out a niche in the industry. Like, Canada ranks among the top five global producers of biobased isoprene, with investments surging in the recent years. This strategic emphasis on green chemistry aligns with global sustainability goals and positions Canada as a leader in eco-friendly polyisoprene production. The construction and industrial sectors, which consume key share of polyisoprene in Canada, have benefited from federal infrastructure spending. Similarly, public infrastructure projects have driven a key annual increase in polyisoprene demand in the past few years. Moreover, Canada’s participation in trade agreements, such as the United States-Mexico-Canada Agreement (USMCA), enhances its access to broader North American markets, enabling manufacturers to scale operations efficiently.

Mexico accounts for smaller share of the North America polyisoprene market. This is driven by its rapidly expanding manufacturing base and favorable trade policies. The transition to lightweight materials in vehicle manufacturing has significantly boosted the use of polyisoprene in tires, seals, and hoses. Additionally, Mexico’s participation in free trade agreements, such as the USMCA, facilitates seamless access to North American markets, enabling manufacturers to meet rising demand efficiently. In addition, Mexico’s footwear industry, which consumes a notable portion of polyisoprene, is also experiencing growth due to increasing exports to the U.S. and Europe. This strategic geographic location, coupled with cost-effective labor and raw material availability, solidifies Mexico’s position as a vital contributor to the regional polyisoprene market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the North America Polyisoprene Market are Zeon Corp, JSR Corp, Goodyear Tire & Rubber Co, Kuraray Co Ltd.

The North America polyisoprene market is characterized by intense competition, with established players and new entrants vying for market share. Established companies like ExxonMobil Chemical, Goodyear Tire & Rubber Company, and Zeon Corporation dominate the landscape, leveraging their scale, technological expertise, and brand reputation to maintain leadership. However, the entry of smaller firms specializing in biobased polyisoprene introduces fresh competition, particularly in eco-conscious segments. Price wars often arise due to the influx of low-cost imports from Asia, forcing companies to adopt cost-saving measures or differentiate their offerings. Additionally, stringent environmental regulations and the need for sustainable practices add complexity, compelling firms to innovate continuously. Despite these challenges, the market remains resilient, driven by strategic investments and a focus on meeting diverse industrial needs.

Top Players in the Market

ExxonMobil Chemical

ExxonMobil Chemical is a global leader in the polyisoprene market, contributing majorly to North America’s production capacity. The company operates state-of-the-art integrated manufacturing facilities, ensuring cost efficiency and supply chain resilience. Its strong R&D capabilities and partnerships with industries like automotive and healthcare enable ExxonMobil to maintain its leadership position.

Goodyear Tire & Rubber Company

Goodyear specializes in high-performance polyisoprene tailored for tire applications. The company’s strategic collaborations with leading automotive manufacturers. Additionally, Goodyear invests heavily in research to enhance product quality and expand its application scope. Its focus on customer-centric solutions and operational excellence ensures sustained growth in a competitive market.

Zeon Corporation

Zeon Corporation is leveraging its expertise in biobased polyisoprene to align with global sustainability goals. The company’s strategic partnerships with downstream industries ensure a steady demand pipeline, while its global presence enhances market reach. Zeon’s emphasis on innovation and sustainability positions it as a key player in the evolving polyisoprene landscape.

Top Strategies Used by Key Players

Key players in the North America polyisoprene market employ a range of strategies to maintain their competitive edge and drive growth. One prominent approach is vertical integration, which allows companies to streamline operations and reduce dependency on external suppliers. For instance, ExxonMobil Chemical operates integrated isoprene-to-polyisoprene production facilities, minimizing costs and enhancing supply chain reliability. Another critical strategy is investing in research and development (R&D) to innovate sustainable products. Goodyear Tire & Rubber Company, for example, collaborates with automotive giants to develop lightweight materials, addressing the growing demand for fuel-efficient vehicles. Sustainability initiatives are also a focal point, with Zeon Corporation spearheading biobased polyisoprene projects to meet regulatory requirements and consumer preferences. Strategic partnerships and acquisitions further strengthen market positions, enabling companies to expand their portfolios and tap into new application areas.

RECENT HAPPENINGS IN THE MARKET

- In June 2023 , ExxonMobil Chemical launched a biobased polyisoprene pilot plant, marking a significant step toward sustainable production and enhancing its portfolio of eco-friendly products.

- In March 2023 , Goodyear Tire & Rubber Company partnered with Tesla to co-develop lightweight tires using advanced polyisoprene formulations, addressing the automotive industry’s demand for fuel-efficient materials.

- In January 2023 , Zeon Corporation announced a $600 million investment in renewable feedstock research, aiming to produce biobased polyisoprene and align with global sustainability goals.

- In October 2022 , Bridgestone acquired a polyisoprene facility in Texas, expanding its production capacity and strengthening its position in the North American market.

- In July 2022 , Michelin introduced a low-emission polyisoprene derivative designed for eco-conscious consumers, targeting applications in green construction and sustainable packaging.

MARKET SEGMENTATION

This research report on the north america polyisoprene market has been segmented and sub-segmented into the following.

By Application

- tires & related products

- footwear

By Country

- The U.S.

- Canada

- Rest of North America.

Frequently Asked Questions

What is Polyisoprene and how is it used in North America?

Polyisoprene is a synthetic elastomer with properties similar to natural rubber. In North America, it's widely used in medical devices (e.g., gloves, catheters), automotive parts, footwear, and adhesives.

What is driving the growth of the North American Polyisoprene market?

Key drivers include rising demand for medical-grade materials, increased automotive production, and a shift toward synthetic alternatives due to latex allergies from natural rubber.

Which countries dominate the Polyisoprene market in North America?

The United States holds the largest share due to its advanced manufacturing sector, strong healthcare infrastructure, and significant R&D investments.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]