North America Pet Food Packaging Market Research Report – Segmented By End-Use (dry food packaging segment,treats packaging segment ) Material Type ( plastic segment, paper segment ) Closure Type ( zip lock closures segment, press-latch closure segment ) Distribution Channel ( supermarkets and hypermarkets segment , online stores segment ) and Country (The U.S., Canada and Rest of North America) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts 2025 to 2033.

North America Pet Food Packaging Market Size

The North America Pet Food Packaging Market Size was valued at USD 26.2 billion in 2024. The North America Pet Food Packaging Market size is expected to have 6.12 % CAGR from 2025 to 2033 and be worth USD 44.72 billion by 2033 from USD 27.80 billion in 2025.

Pet food packaging involves in a variety of materials and formats, including bags, pouches, cans, and containers that is designed to meet the specific needs of pet owners and manufacturers alike. This growth is driven by the rising pet ownership rates with the increasing focus on premium and organic pet food products, and the demand for sustainable packaging solutions. The North America pet food packaging market is poised for continued expansion, with manufacturers focusing on product innovation, convenience, and sustainability to meet evolving consumer preferences. The market is also benefiting from the growing trend of e-commerce, as more consumers turn to online shopping for pet food by necessitating packaging that is both functional and visually appealing.

MARKET DRIVERS

Increasing Pet Ownership and Spending on Pet Care

The North America pet food packaging market is significantly driven by the increasing pet ownership and the corresponding rise in spending on pet care. The demand for high-quality pet food products has surged as more households adopt pets, particularly dogs and cats. According to the American Pet Products Association, approximately 67% of U.S. households, or about 85 million families, own a pet by reflecting a steady increase in pet ownership over the past decade. This trend has led to a substantial rise in the pet food market, which is projected to reach $95 billion by 2025. There is a growing demand for premium and specialized pet food products as pet owners become more discerning about the quality and nutritional value of the food they provide. This, in turn, drives the need for innovative packaging solutions that not only preserve the freshness and quality of the food but also communicate the product's benefits effectively.

Growth in E-commerce and Online Pet Food Sales

Another significant driver of the North America pet food packaging market is the growth in e-commerce and online pet food sales. The shift towards online shopping has transformed the way consumers purchase pet food, with many opting for the convenience of home delivery. According to a report by Packaged Facts, online pet food sales in the U.S. are expected to reach $30 billion by 2025. This trend is prompting manufacturers to develop packaging solutions that are not only functional but also visually appealing to attract consumers browsing online. Packaging that is easy to open, resealable, and designed for safe transport is becoming increasingly important in the e-commerce landscape. Additionally, the rise of subscription services for pet food has further fueled the demand for packaging that can accommodate various portion sizes and maintain product freshness over time.

MARKET RESTRAINTS

Regulatory Compliance and Quality Standards

One of the primary restraints affecting the North America pet food packaging market is the stringent regulatory compliance and quality standards imposed by government agencies. The production and sale of pet food packaging are subject to rigorous regulations regarding safety, labeling, and quality assurance. According to the U.S. Food and Drug Administration, manufacturers must adhere to specific guidelines to ensure the safety and efficacy of packaging materials used for pet food. This regulatory landscape can pose challenges for packaging producers, particularly smaller companies that may lack the resources to navigate complex compliance requirements. Additionally, the lack of standardized definitions for terms such as "natural" or "organic" can create confusion among consumers and complicate marketing efforts. Companies must invest time and resources to ensure compliance with regulations while effectively communicating their product benefits to consumers. Failure to meet regulatory standards can result in product recalls, legal issues, and damage to brand reputation. The manufacturers must remain vigilant in navigating these regulatory challenges to maintain consumer trust and market competitiveness as the pet food packaging market continues to evolve.

Price Volatility of Raw Materials

Another significant restraint in the North America pet food packaging market is the price volatility of raw materials used in packaging production. The healthcare packaging industry relies on various materials, including plastics, metals, and paper, which can be subject to price fluctuations due to factors such as supply chain disruptions, geopolitical tensions, and changes in demand. Fluctuations in the prices of raw materials can significantly impact the overall cost of pet food packaging by leading to increased production costs for manufacturers. This situation can pose challenges for companies that must balance the need to maintain competitive pricing with the rising costs of materials. Additionally, the reliance on a limited number of suppliers for high-quality raw materials can create supply chain vulnerabilities. To mitigate these challenges, manufacturers may need to explore alternative sourcing strategies or invest in long-term contracts with suppliers. Addressing the issue of raw material price volatility will be crucial for maintaining stability and competitiveness in the pet food packaging market.

MARKET OPPORTUNITIES

Expansion of Sustainable Packaging Solutions

The North America pet food packaging market presents significant opportunities for growth through the expansion of sustainable packaging solutions. There is a growing demand for packaging materials that are eco-friendly and recyclable as consumers and regulatory bodies increasingly prioritize environmental sustainability. This trend is driving manufacturers to innovate and develop sustainable packaging solutions that minimize environmental impact while maintaining product safety and efficacy. The versatility of sustainable packaging materials, such as biodegradable plastics and recycled paper, allows them to be used in various pet food applications, including bags, pouches, and containers. The companies can position themselves to meet the increasing demand for eco-friendly packaging solutions and expand their market presence. This emphasis on sustainable packaging is expected to significantly contribute to the growth of the pet food packaging market in North America.

Rising Demand for Premium Pet Food Products

Another major opportunity in the North America pet food packaging market lies in the rising demand for premium pet food products. There is a growing interest in high-quality, nutritious, and specialized pet food options as pet owners increasingly view their pets as family member. According to the American Pet Products Association, the U.S. pet food market is projected to reach $95 billion by 2025 with premium pet food products accounting for a significant portion of this growth. This trend is driving manufacturers to develop packaging solutions that reflect the quality and premium nature of their products, including visually appealing designs and informative labeling. The versatility of packaging materials allows for the incorporation of features such as resealable closures and transparent windows, enhancing the consumer experience.

MARKET CHALLENGES

Supply Chain Disruptions

One of the significant challenges facing the North America pet food packaging market is the potential for supply chain disruptions. The production of pet food packaging relies on key materials such as plastics, metals, and paper, which can be affected by fluctuations in supply and demand. Additionally, the sourcing of packaging materials can be impacted by ethical and sustainability concerns, leading some consumers to seek alternatives. Manufacturers may face challenges in sourcing suitable substitutes that meet consumer expectations for quality and performance as the market shifts towards sustainable and health-conscious options. Addressing these supply chain challenges will be crucial for maintaining product availability and quality in the pet food packaging market.

Competition from Alternative Packaging Solutions

Another challenge in the North America pet food packaging market is the increasing competition from alternative packaging solutions. The rise of health-conscious consumers has led to a surge in demand for various natural and plant-based alternatives, such as biodegradable and compostable packaging, which can pose a challenge to traditional pet food packaging materials. This trend is particularly pronounced among environmentally conscious consumers who are increasingly seeking packaging that aligns with their values. The pet food packaging manufacturers must compete not only with other traditional packaging brands but also with a wide array of alternative packaging solutions that cater to evolving consumer preferences.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.12 % |

|

Segments Covered |

By End-Use,Material Type, Closure Type,Distribution Channel and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

The U.S., Canada and Rest of North America |

|

Market Leader Profiled |

Cargill,Merrick Pet Care,General Mills,Nestle Purina PetCare,Mars Petcare,Blue Buffalo |

SEGMENTAL ANALYSIS

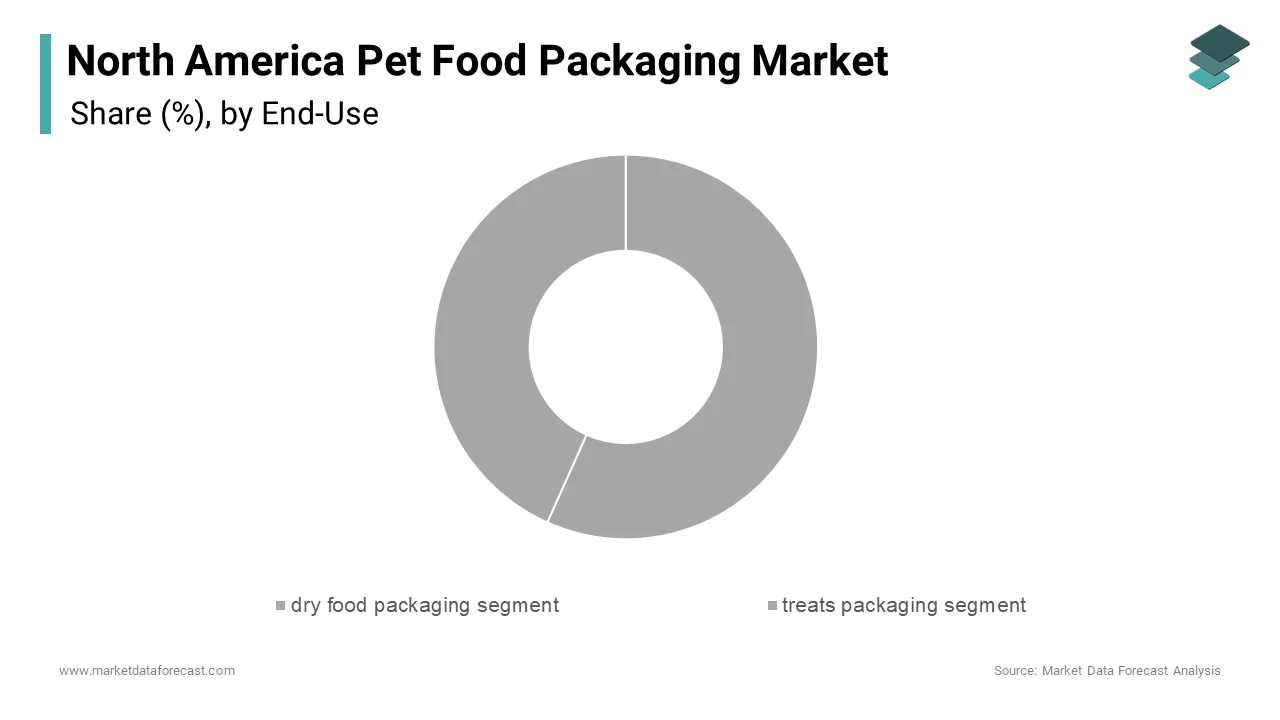

By End-Use Insights

The dry food packaging segment was the largest and held 55.3% of the North America pet food packaging market share in 2024. This dominance can be attributed to the widespread consumption of dry pet food, which is favored for its convenience, shelf stability, and cost-effectiveness. The versatility of dry food packaging allows it to be designed in various formats, including bags, pouches, and containers by catering to a wide range of pet food products. Additionally, the growing trend of premiumization in the pet food market has further propelled the demand for innovative packaging solutions that enhance the appeal and functionality of dry pet food products. The dry food packaging segment is expected to maintain its leading position in the North America pet food packaging market as the demand for high-quality dry pet food continues to rise.

The treats packaging segment is anticipated to witness a significant CAGR of 6.4% during the forecast period. This segment's growth can be attributed to the increasing popularity of pet treats among pet owners, who are increasingly seeking products that enhance their pets' well-being and provide positive reinforcement. Treats packaging is designed to preserve freshness and maintain product integrity, making it a critical component of the pet treats market. Additionally, the rise of e-commerce and online pet food sales has further propelled the demand for treats packaging, as these products are often marketed as convenient and indulgent options for pet owners. The treats packaging segment is poised for significant growth by providing an additional avenue for innovation and development in the coming years.

By Material Type Insights

The plastic segment dominated the market by accounting for 63.2% of the North America pet food packaging market share in 2024. This dominance can be attributed to the versatility, lightweight nature, and cost-effectiveness of plastic materials, which make them ideal for a wide range of pet food applications. The adaptability of plastic allows it to be molded into various shapes and sizes is catering to diverse product requirements, from bags and pouches to containers and tubs. Additionally, the growing trend of sustainability has prompted manufacturers to explore biodegradable and recyclable plastic options, further enhancing the appeal of plastic packaging in the pet food sector. The plastic segment is expected to maintain its leading position in the North America pet food packaging market as the demand for innovative and efficient packaging solutions continues to rise.

The paper segment is likely to experience a projected CAGR of 6.5% in the next coming years. This segment's growth can be attributed to the increasing preference for sustainable packaging solutions among environmentally conscious consumers. Paper packaging is often perceived as a more eco-friendly option compared to plastic, as it is biodegradable and recyclable. The versatility of paper allows it to be used in various applications, including bags, boxes, and pouches by appealing to a wide range of pet food products. Additionally, the rise of premium pet food brands that emphasize natural ingredients and sustainable practices has further propelled the demand for paper packaging solutions. The paper segment is poised for significant growth by providing an additional avenue for innovation and development in the coming years.

By Closure Type Insights

The zip lock closures segment was accounted in capturing a 40.3% of the North America pet food packaging market share in 2024. This dominance can be attributed to the convenience and functionality that zip lock closures offer by allowing pet owners to easily open and reseal packaging to maintain freshness. The versatility of zip lock closures allows them to be used in various packaging formats, including bags and pouches, catering to a wide range of pet food products. Additionally, the growing trend of health-conscious pet ownership has further propelled the demand for packaging that preserves the quality and freshness of pet food.

The press-latch closure segment is experiencing rapid growth with a projected CAGR of 6.4% during the forecast period. This segment's growth can be attributed to the increasing preference for secure and tamper-evident packaging solutions among consumers. Press-latch closures provide an added layer of safety and convenience by ensuring that pet food remains sealed and protected from contamination. The demand for press-latch closures in the pet food market is on the rise which was driven by the growing trend of premium pet food products that emphasize quality and safety. The ease of use and reliability of press-latch closures make them an attractive option for pet owners who prioritize product integrity. Additionally, the rise of e-commerce and online pet food sales has further propelled the demand for press-latch closures, as these packaging solutions are well-suited for shipping and handling. The press-latch segment is poised for significant growth by providing an additional avenue for innovation and development in the coming years.

Country Level Analysis

The United States was the top performer in the North American pet food packaging market with an estimated share of 80.9% in 2024. The U.S. market is characterized by a robust demand for pet food packaging solutions owing to the increasing prevalence of pet ownership and the growing focus on premium pet food products. This trend is prompting manufacturers to develop innovative packaging solutions that cater to the needs of health-conscious pet owners. The U.S. market benefits from a well-established retail infrastructure, with a wide range of pet food packaging products available in supermarkets, specialty stores, and online platforms. Additionally, the growing interest in sustainable packaging solutions has led to increased innovation among manufacturers that further drives the market growth. The popularity of pet food packaging in seasonal events, such as holidays and pet-related promotions, also contributes to its sustained demand. Manufacturers are focusing on clean-label formulations as consumer awareness of product quality and ingredient transparency continues to rise which is expected to enhance the market's growth trajectory in the coming years.

Canada pet food packaging market is anticipated to witness a CAGR of 25.4% during the forecast period. The Canadian market is experiencing a similar trend to that of the U.S., with an increasing number of consumers seeking innovative packaging solutions for pet food products. The Canadian market is also witnessing a growing interest in sustainable packaging solutions, reflecting the broader trend towards environmentally friendly practices in the pet food sector. The manufacturers are responding by introducing innovative products that cater to these demands as consumers become more aware of the importance of packaging in ensuring product safety and quality. The expansion of retail channels, including online shopping, is further enhancing the accessibility of pet food packaging products across Canada. The Canadian pet food packaging market is expected to grow steadily owing to the increasing consumer awareness and demand for high-quality with sustainable packaging solutions.

Top strategies used by the key market participants

The North America pet food packaging market is characterized by the presence of several key players who dominate the landscape. Notable companies include Amcor, which is recognized for its extensive range of packaging solutions, and Sealed Air Corporation, a leading provider of packaging materials that has established a strong foothold in the pet food segment. These companies leverage their extensive distribution networks and brand recognition to capture a significant share of the market. Additionally, smaller, niche players are emerging, focusing on innovative formulations and health-oriented products, such as sustainable and smart packaging solutions. The competitive landscape is further intensified by the growing trend of e-commerce, as brands increasingly adopt online sales strategies to reach a broader audience. The key players are investing in product innovation, marketing strategies, and sustainability initiatives to strengthen their market position and appeal to health-conscious consumers.

Key players in the North America pet food packaging market employ various strategies to strengthen their market position and enhance competitiveness. One prominent strategy is product innovation, where companies continuously develop new formulations and applications for pet food packaging to cater to changing consumer preferences. For instance, introducing sustainable and smart packaging solutions has become a popular tactic to attract environmentally conscious consumers. Additionally, many manufacturers are focusing on sustainability initiatives, such as reducing packaging waste and sourcing materials responsibly, to appeal to environmentally aware consumers.

Another strategy involves expanding distribution channels, particularly through e-commerce platforms, to enhance product accessibility. Companies are increasingly partnering with online retailers to reach a wider audience and capitalize on the growing trend of online shopping. Furthermore, marketing campaigns that emphasize the nutritional benefits and versatility of pet food packaging in various applications are being utilized to engage consumers and drive brand loyalty. Collaborations with pet influencers and social media promotions are also becoming common practices to create buzz around new product launches.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the North America pet food packaging market are Cargill,Merrick Pet Care,General Mills,Nestle Purina PetCare,Mars Petcare,Blue Buffalo,American Kennel Club,Diamond Pet Foods,WellPet,PetSmart,Tuffy's Pet Foods.

The North America pet food packaging market is characterized by a competitive landscape that includes both established brands and emerging players. Major companies such as Amcor, Sealed Air Corporation, and Berry Global dominate the market by leveraging their extensive distribution networks and brand recognition to capture significant market shares. These companies invest heavily in product innovation by focusing on new formulations and applications to meet the evolving preferences of health-conscious consumers. Additionally, the rise of niche brands specializing in sustainable and smart packaging solutions has intensified competition, as these companies cater to a growing demographic seeking environmentally friendly alternatives. The increasing trend of e-commerce has further transformed the competitive landscape, with brands adopting online sales strategies to reach a broader audience. The competition is expected to intensify is prompting manufacturers to differentiate themselves through quality, safety, and innovative marketing strategies.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Amcor launched a new line of sustainable pet food packaging solutions, expanding its product portfolio to cater to the growing demand for eco-friendly options. This initiative aims to enhance consumer accessibility to clean-label products.

- In March 2023, Sealed Air Corporation introduced a fortified pet food packaging product line, targeting the increasing interest in nutritional supplements among consumers.

- In May 2023, Berry Global announced a partnership with a popular pet influencer to promote its pet food packaging products through social media campaigns, aimed at increasing brand awareness and consumer engagement.

- In July 2023, Amcor expanded its distribution network by partnering with major pet food manufacturers across North America, enhancing the availability of its packaging solutions to a wider audience.

- In September 2023, Sealed Air Corporation launched a marketing campaign focused on educating consumers about the versatility of pet food packaging in ensuring product safety and freshness, aiming to increase brand loyalty and consumer engagement.

- In November 2023, Berry Global participated in a major pet expo, showcasing its packaging solutions and engaging with pet owners to promote brand awareness.

- In January 2024, Amcor introduced a new line of flavored pet food packaging options, capitalizing on the growing trend of gourmet products among consumers.

- In March 2024, Sealed Air Corporation announced the launch of a pet food packaging subscription service, allowing consumers to receive regular shipments of their favorite products, thereby enhancing customer convenience and loyalty.

- In April 2024, Berry Global collaborated with a renowned veterinarian to create a series of educational materials on the importance of packaging in pet food safety, leveraging social media to reach a broader audience.

- In June 2024, Amcor launched a limited-edition seasonal packaging design for pet food products, aiming to attract consumers looking for unique and festive options during the holiday season.

- These strategic actions reflect the dynamic nature of the North America pet food packaging market, as companies continuously adapt to consumer trends and preferences to strengthen their market presence.

MARKET SEGMENTATION

This research report on the North America Pet Food Packaging Market has been segmented and sub-segmented into the following categories.

By End-Use

- dry food packaging segment

- treats packaging segment

By Material Type

- plastic segment

- paper segment

By Closure Type

- zip lock closures segment

- press-latch closure segment

By Distribution Channel

- supermarkets and hypermarkets segment

- online stores segment

By Country

- The U.S.

- Canada

- Rest of North America.

Frequently Asked Questions

What is the North America Pet Food Packaging Market?

It refers to the industry focused on packaging solutions for pet food products in North America.

What are the key materials used in pet food packaging?

Common materials include plastic, paper & paperboard, metal, and biodegradable materials.

What are the latest trends in pet food packaging?

Sustainable packaging, resealable closures, and smart packaging technologies.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]