North America Metal Fabrication Market Size, Share, Trends & Growth Forecast Report By Process (Welding, Machining, Forming, Shearing, Cutting, Folding, Rolling, Stamping, Punching), Raw Material, End-User and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Metal Fabrication Market Size

The North America metal fabrication market was worth USD 4.85 billion in 2024. The North American market is estimated to grow at a CAGR of 5.75% from 2025 to 2033 and be valued at USD 8.02 billion by the end of 2033 from USD 5.13 billion in 2025.

The North America Metal Fabrication Market involves shaping, cutting, welding, and assembling metal parts to create products used in industries like automotive, aerospace, construction, and energy. These industries rely heavily on high-quality, custom-made metal components. In recent years, the market has grown due to advancements in technology, such as automation, robotics, and computer-aided design (CAD). These tools have made production faster, more accurate, and cost-effective. At the same time, there is a growing focus on sustainability, with companies using greener materials and methods to reduce their environmental impact. The United States and Canada are the biggest players in this market because of their strong industrial sectors and demand for specialized metal products.

The metal fabrication industry reflects wider economic trends. For example, the U.S. Bureau of Labor Statistics reports that manufacturing, which includes metal fabrication, provides jobs for about 8.4% of the U.S. workforce. The National Association of Manufacturers also notes that manufacturing adds over $2 trillion to the U.S. economy every year. On the environmental side, the Environmental Protection Agency mentions that industries like metal fabrication contribute nearly 23% of greenhouse gas emissions in the U.S. This shows the importance of adopting cleaner technologies. These figures show how the metal fabrication market is connected to both the economy and environmental challenges, making it an important area to watch.

MARKET DRIVERS

Increasing Adoption of Additive Manufacturing

Additive manufacturing, also known as 3D printing, is emerging as a transformative force in the metal fabrication industry. Unlike traditional subtractive methods, additive manufacturing builds components layer by layer, reducing material waste and enabling intricate designs. In North America, industries like aerospace and healthcare are leveraging this technology to produce lightweight, high-strength components with precision. For instance, the National Institute of Standards and Technology draws attention on the fact that additive manufacturing can reduce production time by up to 50% for complex parts. This innovation not only enhances efficiency but also opens new revenue streams for fabricators willing to invest in this cutting-edge technology, positioning them at the forefront of industrial evolution.

Rising Demand for Customized Fabrication Solutions

Customization is becoming a key driver in the metal fabrication market which is fueled by the increasing need for tailored solutions across industries. The construction sector, for example, requires unique metal structures for modern architectural designs, while the energy sector demands specialized components for renewable energy projects. A study by McKinsey & Company reveals that companies offering customized products experience a 10% to 15% higher customer retention rate compared to those offering standardized solutions. Additionally, the growing trend of "mass customization" allows fabricators to meet specific client needs without compromising on scalability. The U.S. Department of Commerce notes that small-scale custom fabricators have seen a 7% annual growth in orders since 2020. This demand for bespoke solutions is reshaping the market, encouraging fabricators to adopt flexible manufacturing processes and advanced software tools to stay competitive.

MARKET RESTRAINTS

Skilled Labor Shortages

One of the significant restraints facing the North America Metal Fabrication Market is the shortage of skilled labor. Despite the industry's growth, there is a widening gap between the demand for skilled workers and the available workforce. The Manufacturing Institute reports that the U.S. manufacturing sector could face a shortfall of 2.1 million skilled workers by 2030. This issue is particularly acute in metal fabrication, where tasks like welding and machining require specialized training. The Bureau of Labor Statistics states that employment in metal fabrication occupations is expected to grow by only 2% annually, slower than other industries, due to the difficulty in attracting new talent. The lack of skilled labour not only delays project timelines but also increases operational costs, as companies must invest in training or outsource work which is impacting overall profitability.

Trade Policies and Tariffs

Trade policies and tariffs remain a critical restraint for the North America Metal Fabrication Market, affecting the cost and availability of raw materials. The United States-Mexico-Canada Agreement (USMCA) has introduced stricter rules of origin for steel and aluminum, requiring that 70% of these materials be sourced from North America to qualify for tariff exemptions. While this policy aims to boost domestic production, it has led to increased costs for fabricators reliant on imported materials. The Peterson Institute for International Economics estimates that steel tariffs alone have added approximately $500 million annually to manufacturing costs in the U.S. These trade barriers create uncertainty for fabricators, especially smaller firms with limited bargaining power.

MARKET OPPORTUNITIES

Emerging Role in Modular Construction

Modular construction is gaining traction across North America, creating a significant opportunity for the metal fabrication industry. This construction method relies heavily on prefabricated metal components, such as steel frames and modular panels, which are fabricated off-site and assembled on-site. The U.S. Census Bureau highlights that non-residential construction spending reached $850 billion in 2022, with modular solutions accounting for an increasing share. Metal fabricators can capitalize on this trend by producing standardized yet customizable components that align with modular designs. This shift not only diversifies their client base but also positions them as key enablers of sustainable and efficient construction practices.

Growing Demand for Smart Manufacturing Solutions

The integration of smart manufacturing technologies presents a transformative opportunity for the metal fabrication market. Technologies like the Internet of Things (IoT), artificial intelligence (AI), and predictive maintenance are reshaping production processes. A report by PwC states that manufacturers adopting IoT solutions can achieve up to a 12% reduction in operational costs and a 10% increase in productivity. For instance, IoT-enabled sensors can monitor equipment performance in real-time, reducing downtime by 20%, according to the National Institute of Standards and Technology. Additionally, AI-driven analytics can optimize material usage, minimizing waste and enhancing sustainability.

MARKET CHALLENGES

Cybersecurity Risks in Connected Systems

As metal fabricators adopt advanced technologies like IoT and connected machinery, they face growing cybersecurity risks, which pose a significant challenge. Cyberattacks on industrial systems have surged in recent years, with IBM reporting a 30% increase in manufacturing-related breaches in 2022. These attacks can disrupt operations, compromise sensitive data, and lead to costly downtime. The U.S. Department of Homeland Security notes that small and medium-sized fabricators are particularly vulnerable due to limited IT resources and outdated security protocols. Furthermore, a study by Deloitte focuses that 48% of manufacturers lack comprehensive cybersecurity strategies, leaving them exposed to threats. Addressing these risks requires substantial investment in cybersecurity infrastructure and employee training, which can strain budgets and divert focus from core operations.

Environmental Compliance Costs

While sustainability is a growing priority, the costs associated with environmental compliance present a significant challenge for the metal fabrication market. The Environmental Protection Agency mandates strict emissions standards, requiring fabricators to invest in cleaner technologies and waste management systems. A report by the National Association of Manufacturers estimates that compliance costs for environmental regulations can reach up to $19,564 per employee annually. Additionally, the transition to low-carbon energy sources, such as electric furnaces, involves upfront investments of over $1 million per facility, according to the Edison Electric Institute. Smaller fabricators often struggle to meet these financial demands, risking non-compliance penalties or reduced competitiveness. Balancing regulatory adherence with profitability remains a persistent challenge in an era of increasing environmental scrutiny.

SEGMENTAL ANALYSIS

By Process Insights

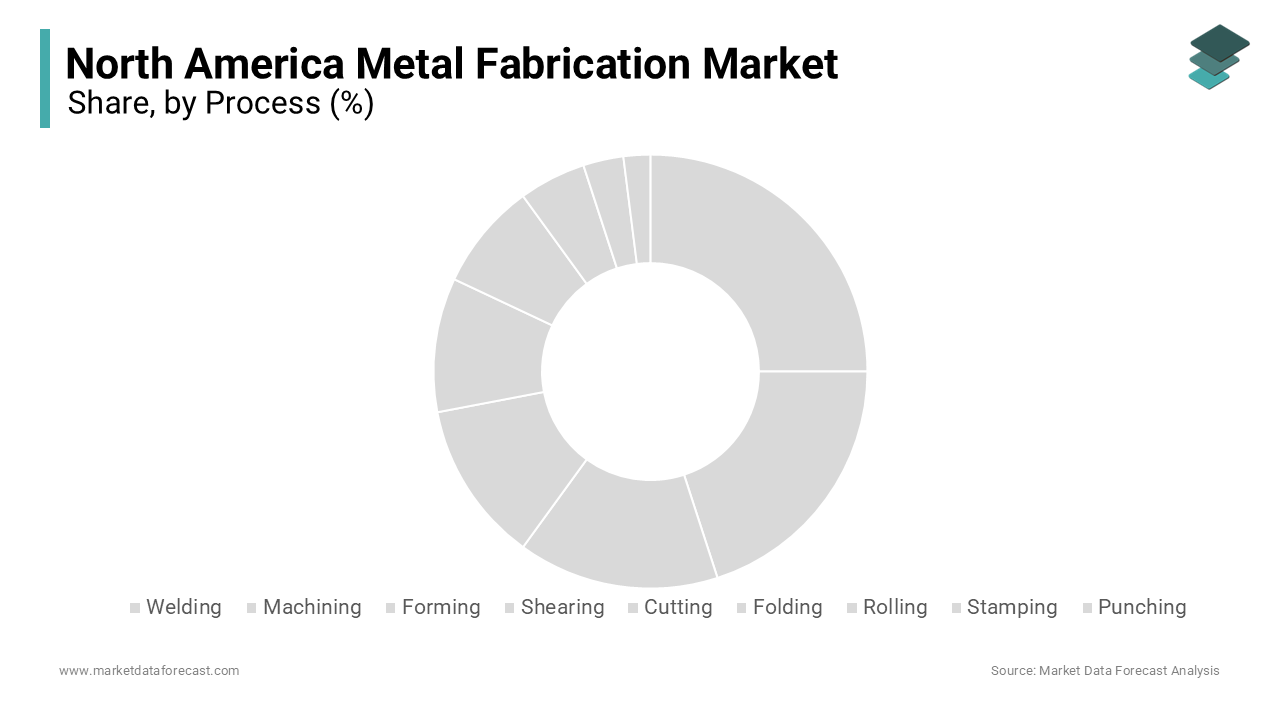

The Welding segment gained popularity as the largest segment in the North America Metal Fabrication Market by holding a market share of 25.3% in 2024. This significance is due to its widespread use across industries like automotive, construction, and aerospace. The U.S. Bureau of Labor Statistics reports that welding-related jobs account for over 400,000 positions in the manufacturing sector alone. Welding's importance lies in its ability to join metals with high strength and precision, making it indispensable for structural applications. For example, the American Welding Society states that over 50% of U.S. GDP is influenced by welding-dependent industries. Its versatility and reliability ensure it remains a critical process in metal fabrication.

The cutting segment is the fastest-growing in the North America Metal Fabrication Market, with a CAGR of 6.8% from 2025 to 2033. This growth is driven by advancements in laser and plasma cutting technologies, which offer higher precision and faster production speeds. According to the National Institute of Standards and Technology, laser cutting systems can reduce material wastage by up to 15%, making them cost-effective. Additionally, the rise of custom fabrication projects has increased demand for precise cutting techniques. A report by the U.S. Department of Commerce highlights that industries like aerospace and automotive are adopting advanced cutting tools, boosting segment growth. These innovations make cutting vital for meeting modern manufacturing needs efficiently.

By Raw Material Insights

The steel segment was the biggest category in the North America Metal Fabrication Market and captured a market share of 65% during the forecast period. Steel commanced due to its strength, durability, and versatility, making it essential for industries like construction, automotive, and energy. The U.S. Geological Survey reported that steel production in North America exceeded 100 million metric tons in 2023, highlighting its widespread use. Steel’s importance also stemmed from its cost-effectiveness compared to other materials. The Environmental Protection Agency noted that recyclable steel accounted for over 80% of the material used in fabrication, supporting sustainability efforts. Its ability to meet diverse industrial needs ensured its leadership position in the market.

The Aluminum segment is predicted to be the fastest-growing segment in the North America Metal Fabrication Market, with a CAGR of 7.5% from 2025 to 2033. This development will be propelled by increasing demand for lightweight materials in the automotive and aerospace industries. The Aluminum Association predicts that aluminum usage in vehicles will rise by 30% by 2030, as automakers aim to improve fuel efficiency. Additionally, Boeing’s market outlook estimates that over 43,000 new aircraft will be built by 2040, many requiring aluminum components. The U.S. Department of Energy states that using aluminum can reduce vehicle weight by up to 40%, lowering emissions. These trends will make aluminum vital for meeting future manufacturing and environmental goals.

By End-use Insights

The construction sector was the largest end-use segment in the North America Metal Fabrication Market and controlled a market share of 35.3%. This progress was caused by the high demand for metal components like steel beams, aluminum frames, and fabricated structures in residential and commercial projects. The U.S. Census Bureau reported that construction spending exceeded $1.8 trillion in 2023, with metals playing a critical role in modern infrastructure. The National Association of Home Builders showcased that over 60% of new homes required custom metal parts for durability and design flexibility. Construction’s importance stemmed from its ability to drive economic growth while supporting urbanization and sustainable building practices.

The energy and power segment is projected to be the rapidly rising end-use segment in the North America Metal Fabrication Market, with a CAGR of 8.2% during the forecast period. This growth will be fueled by the rising adoption of renewable energy projects, such as wind turbines and solar panel installations. The U.S. Department of Energy predicts that solar energy capacity will grow by 324 gigawatts by 2030, requiring significant metal components like turbine towers and mounting structures. Additionally, the American Wind Energy Association estimates that wind energy projects will account for over 20% of U.S. electricity generation by 2030.

REGIONAL ANALYSIS

The United States was the major contributor to the North America Metal Fabrication Market and possessed a market share of 85.2%. This dominance was driven by its robust industrial base and high demand for fabricated metals in sectors like automotive, aerospace, and construction. The U.S. Bureau of Economic Analysis reported that manufacturing contributed over $2.5 trillion to the U.S. GDP in 2023, with metal fabrication playing a key role. Additionally, the National Association of Manufacturers spotlighted that the U.S. accounted for nearly 12% of global manufacturing output. The country’s position is due to its advanced infrastructure, skilled workforce, and technological innovation, making it a central hub for metal fabrication.

Canada is likely to be the fastest-growing market in the North America Metal Fabrication Market, with a CAGR of 6.3% from 2025 to 2033. This rise will be fueled by increased investments in renewable energy projects and infrastructure development. Natural Resources Canada predicts that wind and solar energy capacity will grow by 50% by 2030, requiring significant metal components. Additionally, the Canadian government announced plans to invest $180 billion in infrastructure projects over the next decade, boosting demand for fabricated metals. Canada’s focus on sustainable practices and its abundant raw material resources, such as aluminum, will further drive its growth. These factors will make Canada a key player in the region’s metal fabrication future.

Top 3 Players in the market

O’Neal Manufacturing Services

O’Neal Manufacturing Services holds a dominant position in the North America metal fabrication market, capitalizing on the growing demand for customized and large-scale metal components. As industries such as heavy equipment, transportation, and energy push for more integrated manufacturing partners, O’Neal has expanded its footprint by offering end-to-end fabrication services that include machining, welding, assembly, and finishing. Its strategic emphasis on supply chain integration and lean manufacturing allows it to meet evolving customer expectations for faster turnaround times and high-quality outputs. O’Neal’s contribution to the market is substantial, as it acts as a key enabler of efficiency and cost optimization for OEMs navigating a highly competitive and time-sensitive manufacturing landscape.

BTD Manufacturing

BTD Manufacturing has cemented its leadership in the North America metal fabrication space by embracing automation and digital manufacturing trends. The rising adoption of robotics and smart factory solutions has provided BTD with a competitive edge, particularly as customers increasingly prioritize precision, scalability, and shorter product cycles. The company’s proficiency in value-added services such as laser cutting, robotic welding, and advanced machining has allowed it to serve critical industries like agriculture, construction, and industrial machinery more effectively. BTD’s contribution to the market is marked by its ability to deliver tailored, technology-driven solutions that enhance product innovation and operational agility for its clients, supporting broader trends of modernization within the metal fabrication sector.

Mayville Engineering Company (MEC)

Mayville Engineering Company (MEC) maintains a strong market presence through its diversified capabilities and commitment to expanding its contract manufacturing services. As trends like reshoring and nearshoring gain momentum in North America, MEC’s ability to offer localized, vertically integrated solutions has strengthened its value proposition to clients across military, power sports, commercial vehicles, and other industrial sectors. The company’s growth strategy, supported by acquisitions and continuous investments in automation and lean processes, has positioned it to capitalize on the increasing need for flexible, high-volume production capabilities. MEC’s contribution to the metal fabrication market lies in its role as a full-service partner, helping customers improve supply chain resilience and achieve faster time-to-market in an environment where supply chain disruptions and labor shortages are shaping competitive dynamics.

Top strategies used by the key market participants

Sustainability and Green Manufacturing

Sustainability has become a core focus for key players as industries across North America push for eco-friendly practices and carbon reduction. Leading metal fabrication companies are adopting green manufacturing strategies, which include investing in energy-efficient equipment, minimizing material waste through lean manufacturing principles, and incorporating recycled metals into their supply chains. Many are also aligning with environmental certifications and implementing closed-loop production systems to further reduce their environmental footprint. This commitment to sustainability not only meets growing regulatory and customer expectations but also serves as a competitive differentiator, helping these companies attract clients who prioritize responsible sourcing and sustainable production processes.

Reshoring and Localization

The reshoring trend has gained momentum as companies seek to mitigate supply chain disruptions and reduce reliance on overseas manufacturing. In response, major players in the North America metal fabrication market are investing in expanding and modernizing domestic facilities to better serve local and regional clients. This localization strategy improves lead times, enhances supply chain resilience, and enables closer collaboration with customers. By bringing production closer to end markets, these companies can offer more responsive and flexible services while supporting the broader economic trend of revitalizing North American manufacturing. Reshoring also aligns with the strategic push for national security and self-sufficiency in critical sectors such as defense, infrastructure, and heavy industry.

Customization and Value-Added Services

To differentiate themselves from competitors, market leaders are focusing on delivering highly customized solutions and value-added services tailored to the unique requirements of each client. This strategy includes offering services like engineering support, prototyping, assembly, and even logistics assistance. By becoming more than just component suppliers and acting as full-service partners, these companies foster long-term relationships with customers who increasingly seek flexibility and specialized expertise. Customization enhances customer satisfaction, improves project outcomes, and builds brand loyalty in a market where precision and responsiveness are critical.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Helander, O’Neal Manufacturing Services, BTD Manufacturing Inc, Kapco Metal Stamping, Canadian Metal Fabricators Ltd., Ballman Metals, Schaumberg Specialties LLC, Mayville Engineering Company Inc., Miro Manufacturing Inc, Matcor-Matsu Group Inc, Standard Iron & Wire Works Inc, IronForm.

The North America metal fabrication market is highly competitive, with many companies striving to meet the growing demand for customized and high-quality metal products. Metal fabrication involves cutting, shaping, and assembling metals to create parts or structures used in industries like automotive, construction, aerospace, and energy. In this market, competition is driven by factors such as innovation, cost-efficiency, and the ability to deliver precise solutions.

Large companies often dominate due to their advanced technology and strong supply chains. For example, firms like Precision Castparts Corp. and Reliance Steel & Aluminum Co. lead by offering a wide range of services and maintaining partnerships with key industries. These companies invest heavily in automation and robotics to improve efficiency and reduce costs, giving them an edge over smaller players.

However, smaller businesses also compete by focusing on niche markets and providing specialized services. They often cater to local customers who need quick turnaround times or custom designs. This creates a balanced mix of big and small players in the market.

The competitive landscape is further shaped by rising demand for lightweight materials, especially in the automotive and aerospace sectors. According to the U.S. Department of Commerce, the use of advanced materials like aluminum and titanium has grown significantly, pushing fabricators to adapt.

To stay ahead, companies emphasize sustainability and eco-friendly practices. Recycling scrap metal and reducing energy consumption are becoming key strategies. Overall, the North America metal fabrication market thrives on innovation, customer needs, and adapting to industry trends, making it a dynamic and challenging space for all players.

RECENT MARKET DEVELOPMENTS

- In March 2025, the American President Donald Trump implemented a 25% tariff on all steel and aluminum imports. This move aims to boost domestic production and stabilize the supply chain in North America, with significant implications for businesses and consumers reliant on imported metals.

- In February 2025, Australia launched a $636 million (A$1 billion) fund to support the production and supply chains of green iron. An initial A$500 million was allocated to rescue the Whyalla steelworks in South Australia, which had faced financial challenges. This investment is part of a broader A$1.9 billion package aimed at revitalizing the steel industry and aligning with the nation's clean energy transition goals.

- In December 2024, ArcelorMittal, a leading global steel manufacturer, announced the delay of its planned investments in greener steelmaking technologies in Europe. The company cited policy uncertainties within the European Union, including concerns over the proposed carbon border tax and competition from low-cost Chinese steel imports, as reasons for postponing projects aimed at reducing carbon emissions.

MARKET SEGMENTATION

This research report on the north america metal fabrication market is segmented and sub-segmented based on categories.

By Process

- Welding

- Machining

- Forming

- Shearing

- Cutting

- Folding

- Rolling

- Stamping

- Punching

By Raw Material

- Steel

- Aluminum

- Others

By End-use

- Construction

- Automotive

- Manufacturing

- Energy & Power

- Electronics

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What are the current trends in the North America metal fabrication market?

Key trends include the adoption of automation and robotics for increased efficiency, a focus on sustainability and energy-efficient processes, and the increasing use of 3D printing for metal components and custom fabrication.

What challenges does the North America metal fabrication market face?

Challenges include the rising costs of raw materials, labor shortages in skilled trades, and the need to meet environmental regulations related to emissions and waste management.

What is the future outlook for the North America metal fabrication market?

The market is expected to grow due to continued demand in key sectors like construction, automotive, and aerospace, with an increasing emphasis on advanced fabrication techniques, sustainability, and customized metal solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com