North America Mechanical Ventilators Market Research Report - Segmented By Product Type (Critical Care, Portable ventilators) , Mode (Invasive ventilatorsNon-invasive ventilators), End User (Hospitals,Home Healthcare) & Country (U.S, Canada & Rest of North America) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts (2025 to 2033)

North America Mechanical Ventilators Market Size

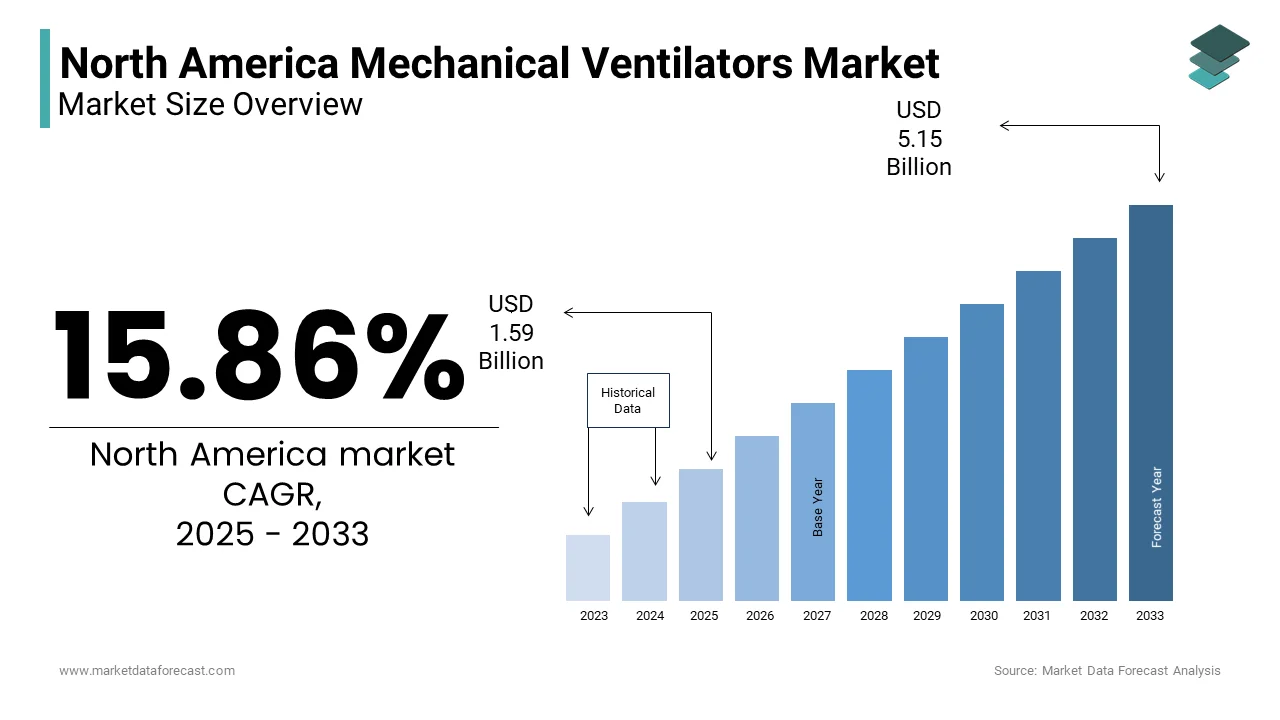

The North America Mechanical Ventilators Market Size was valued at USD 1.37 billion in 2024. The North America Mechanical Ventilators Market size is expected to have 15.86% CAGR from 2025 to 2033 and be worth USD 5.15 billion by 2033 from USD 1.59 billion in 2025.

The North America mechanical ventilators market is a component of the region's healthcare infrastructure in light of recent global health crises. The Centers for Disease Control and Prevention (CDC) estimates that over 25 million Americans suffer from asthma, while chronic obstructive pulmonary disease (COPD) affects nearly 16 million individuals with the demand for ventilator technologies. Canada, with its publicly funded healthcare system has seen steady growth in ventilator adoption, supported by government initiatives to enhance critical care infrastructure. As per Deloitte, hospitals in North America are increasingly investing in state-of-the-art ventilator systems to meet rising patient volumes and improve outcomes.

MARKET DRIVERS

Rising Prevalence of Chronic Respiratory Diseases

The escalating incidence of chronic respiratory diseases is a primary driver propelling the North America mechanical ventilators market forward. According to the American Lung Association, respiratory conditions such as COPD and asthma account for over 10 million hospitalizations annually in the U.S. alone. These conditions require advanced ventilator support, particularly during acute exacerbations, driving demand for critical care and portable ventilators. Furthermore, as per a study by the National Institutes of Health (NIH), the prevalence of respiratory illnesses is expected to increase by 15% over the next decade due to environmental factors such as air pollution and smoking. This trend is compounded by the aging population, with the U.S. Census Bureau projecting that individuals aged 65 and above will constitute 22% of the population by 2030. Older adults are disproportionately affected by respiratory conditions, necessitating robust ventilator infrastructure.

Technological Advancements in Ventilator Design

Technological advancements in ventilator design represent another significant driver shaping the North America mechanical ventilators market. Innovations such as non-invasive ventilation (NIV) and AI-integrated monitoring systems have revolutionized patient care, enhancing both safety and efficiency. According to a report by Frost & Sullivan, the adoption of NIV systems has reduced hospital readmission rates by 20%, as these devices minimize complications associated with invasive procedures. Additionally, as per a study by PwC, AI-powered ventilators can predict patient deterioration up to 48 hours in advance, enabling proactive interventions. Portable ventilators, equipped with wireless connectivity, have also gained traction, particularly in home healthcare settings. Over 60% of patients prefer portable ventilators for their convenience and ease of use. These technological breakthroughs not only improve patient outcomes but also expand the addressable market is driving widespread adoption across healthcare facilities.

MARKET RESTRAINTS

High Costs of Advanced Ventilators

The substantial costs associated with advanced mechanical ventilators pose a significant barrier to market growth, particularly for smaller healthcare providers. The financial burden often deters rural hospitals and clinics from upgrading their equipment that is limiting access to cutting-edge technologies. Furthermore, as per a report by the Healthcare Financial Management Association (HFMA), ongoing maintenance and calibration expenses can add an additional 15-20% to the total cost of ownership. These expenditures are particularly challenging for facilities operating on tight budgets, where allocating resources for capital investments is a constant struggle.

Stringent Regulatory Requirements

Stringent regulatory requirements governing the approval and usage of mechanical ventilators present another major restraint impacting the market. The U.S. Food and Drug Administration (FDA) mandates rigorous testing and compliance with safety standards, which can delay product launches and increase development costs. According to a study by Ernst & Young, the average time required to bring a new ventilator model to market is approximately 3-5 years is significantly longer than other medical devices. Additionally, as per a report by Deloitte, manufacturers must adhere to evolving guidelines, such as those outlined in ISO 13485, to ensure quality management systems are in place. These regulatory hurdles often deter smaller companies from entering the market, consolidating dominance among established players. Furthermore, the complexity of navigating international standards, such as those set by Health Canada, adds another layer of difficulty for manufacturers seeking to expand their reach.

MARKET OPPORTUNITIES

Expansion of Home Healthcare Services

The growing emphasis on home healthcare services presents a transformative opportunity for the North America mechanical ventilators market. Portable ventilators are gaining traction in this segment due to their compact design and ease of use. Furthermore, advancements in telehealth technologies have enabled remote monitoring of ventilator-dependent patients by enhancing safety and compliance. According to a study by McKinsey, integrating AI-driven analytics into home ventilators can reduce emergency interventions by 25%, lowering overall healthcare costs.

Integration with Smart Healthcare Systems

The integration of mechanical ventilators with smart healthcare systems offers a lucrative opportunity for the North America market. Connected ventilators, equipped with IoT sensors and real-time data analytics that enable seamless communication between devices and healthcare providers. According to a report by Gartner, over 60% of hospitals plan to adopt smart healthcare solutions by 2025 by creating a strong demand for interoperable ventilator systems. These technologies facilitate predictive maintenance thereby reducing downtime and ensuring optimal performance. Additionally, as per a study by PwC, AI-driven ventilators can analyze patient data to optimize ventilation parameters by improving clinical outcomes. The shift towards value-based care models further amplifies the need for integrated systems that align financial incentives with patient outcomes.

MARKET CHALLENGES

Limited Skilled Workforce

A limited skilled workforce capable of operating advanced mechanical ventilators poses a significant challenge to the North America market. According to a study by the American Association of Critical-Care Nurses (AACN), there is a projected shortage of over 100,000 registered nurses specializing in critical care by 2025. This shortage is exacerbated by the complexity of modern ventilators, which require specialized training to operate effectively. Furthermore, as per a report by the Joint Commission, inadequate training leads to a 30% increase in ventilator-associated complications by undermining patient safety and operational efficiency. Rural areas, in particular, face difficulties in recruiting qualified personnel that further widening the gap in access to advanced respiratory care.

Supply Chain Disruptions

Supply chain disruptions have emerged as a critical challenge for the North America mechanical ventilators market in the wake of global health crises. According to a report by McKinsey, over 70% of ventilator components are sourced internationally by making the supply chain vulnerable to geopolitical tensions and logistical bottlenecks. The COVID-19 pandemic due to these vulnerabilities, with manufacturers experiencing delays of up to six months in securing essential parts. Furthermore, as per a study by Deloitte, fluctuations in raw material prices have increased production costs by 25% is impacting profitability. These disruptions not only hinder timely delivery of ventilators but also limit the ability to scale production during periods of high demand. Strengthening domestic manufacturing capabilities and diversifying supplier networks are essential to mitigate these risks.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

15.86 % |

|

Segments Covered |

By Product, Mode , End User and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

The U.S., Canada and Rest of North America |

|

Market Leader Profiled |

Dragerwerk AG & Co. KGaA, ResMed, Philips Healthcare, Medtronic Plc, GE Healthcare |

SEGMENTAL ANALYSIS

By Product Type Insights

The critical care ventilators segment dominated the North America mechanical ventilators market with 55.1% of share in 2024. The segment’s growth is driven by their widespread use in intensive care units (ICUs) to manage severe respiratory conditions. According to the Center for Disease and Control Prevention, over 4.5 million patients are admitted to ICUs annually in the U.S., with respiratory failure being a leading cause. The precision and reliability of critical care ventilators make them indispensable in managing complex cases during pandemics. The advancements in ventilator design, such as adaptive modes and real-time monitoring, have enhanced their appeal. Hospitals are increasingly investing in these systems to ensure compliance with stringent regulatory standards and improve patient outcomes.

The portable ventilators segment is projected to witness a CAGR of 10.5% from 2025 to 2033. This rapid growth is fueled by the increasing demand for mobility and flexibility in patient care. A study by Frost & Sullivan reveals that portable ventilators reduce hospital readmissions by 20% by making them particularly appealing for home healthcare settings. Additionally, as per a report by PwC, advancements in battery technology and wireless connectivity have expanded their usability, enabling remote monitoring and real-time data transmission. The growing emphasis on patient-centric care has further accelerated adoption, with over 50% of providers exploring portable solutions.

By Mode Insights

The invasive ventilators segment was accounted in holding a dominant share of the North America mechanical ventilators market in 2024 owing to the managing severe respiratory conditions that require intubation. According to the NIH, invasive ventilation is utilized in over 70% of ICU admissions for respiratory failure with its importance in critical care. The precision and control offered by invasive ventilators make them indispensable in high-stakes scenarios during pandemic. Furthermore, as per a study by Deloitte, advancements in ventilator design, such as synchronized intermittent mandatory ventilation (SIMV), have enhanced their efficacy.

The non-invasive ventilators segment is lucratively growing with a projected CAGR of 11.2% from 2025 to 2033. This growth is driven by their ability to minimize complications associated with invasive procedures, making them ideal for mild to moderate respiratory conditions. According to a study by PwC, non-invasive ventilation reduces hospital readmissions by 25% by attracting widespread adoption. Additionally, as per a report by Frost & Sullivan, advancements in mask design and pressure regulation have improved patient comfort and compliance. The growing emphasis on preventive care has further accelerated adoption, with over 60% of providers exploring non-invasive solutions. These dynamics position non-invasive ventilators as the fastest-growing segment in the market.

By End User Insights

The hospitals segment was the largest by capturing a significant share of the North America mechanical ventilators market in 2024 owing to the critical role ventilators play in managing severe respiratory conditions in intensive care units (ICUs). The precision and reliability of hospital-grade ventilators make them indispensable in managing complex cases, particularly during pandemics. The advancements in ventilator design, such as adaptive modes and real-time monitoring, have enhanced their appeal. Hospitals are increasingly investing in these systems to ensure compliance with stringent regulatory standards and improve patient outcomes by reinforcing their prominence as the largest segment.

The home healthcare segment is likely to grow lucratively with a CAGR of 9.8% from 2025 to 2033. This growth is driven by the increasing preference for personalized and cost-effective care, particularly among patients requiring long-term ventilation. As per a study by Accenture, over 40% of patients prefer home-based solutions is citing improved quality of life and reduced hospital stays. Additionally, as per a report by McKinsey, advancements in telehealth technologies have enabled remote monitoring of ventilator-dependent patients by enhancing safety and compliance. The growing emphasis on patient-centric care has further accelerated adoption, with over 50% of providers exploring home healthcare solutions.

Country Level Analysis

The U.S. led the North America mechanical ventilators market with an estimated share of 85.4% in 2024. The growth of the market in this country is driven by the advanced healthcare system and high prevalence of chronic respiratory conditions. The aging population, projected to reach 22% by 2030 that further amplifies this need. Investments in smart healthcare systems and AI-driven ventilators are gaining traction, with over 60% of hospitals adopting these technologies.

Canada mechanical ventilators market is esteemed to showcase a CAGR of 13.4% during the forecast period. The country’s publicly funded healthcare system presents unique challenges, including limited budgets and slower adoption rates of advanced technologies. Government initiatives to enhance critical care infrastructure have spurred adoption, with over 50% of hospitals upgrading their equipment. According to a study by Frost & Sullivan, portable ventilators are gaining popularity, driven by their cost-effectiveness and scalability.

Top 3 Players in the Market

Medtronic plc

Medtronic plc is a prominent player in the North America mechanical ventilators market, renowned for its innovative and reliable products that cater to diverse patient needs. The company’s strengths lie in its ability to deliver cutting-edge technologies, such as AI-integrated ventilators, which enhance patient safety and operational efficiency. Medtronic’s commitment to innovation is evident in its strategic partnerships with research institutions to develop next-generation ventilator systems.

GE Healthcare

GE Healthcare is a key contributor to the North America mechanical ventilators market, offering a comprehensive range of products tailored to the needs of hospitals and trauma centers. The company’s strengths include its scalable solutions and robust customer support services. GE Healthcare’s focus on interoperability ensures seamless integration with existing healthcare IT systems, enhancing operational efficiency. Its strategic investments in smart healthcare technologies have enabled the development of connected ventilators by positioning it as a trusted partner for healthcare organizations.

Philips Healthcare

Philips Healthcare is a leading player in the North America mechanical ventilators market, known for its user-friendly platforms and advanced service offerings. The company’s strengths lie in its ability to deliver customizable solutions that cater to the unique needs of healthcare providers. Philips’ emphasis on patient-centric care has resulted in the development of ventilators that prioritize comfort and compliance. Its strategic collaborations with telehealth providers have expanded its reach by enabling it to address the growing demand for remote respiratory care solutions.

Top strategies used by the key market participants

Key players in the North America mechanical ventilators market employ several strategies to maintain their competitive edge. Strategic acquisitions are a common approach, allowing companies to expand their product portfolios and enter new markets. Partnerships with technology firms, particularly those specializing in AI and IoT, are also prevalent, enabling the development of advanced ventilator systems. Additionally, investments in research and development drive innovation, ensuring compliance with evolving regulatory standards. Companies also focus on enhancing customer engagement through training programs and support services. These strategies collectively strengthen their market position and drive growth.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a dominant role in the North America Mechanical Ventilators Market profiled in this report are Dragerwerk AG & Co. KGaA, ResMed, Philips Healthcare, Medtronic Plc, GE Healthcare, Getinge Group, Smiths Medical, Fisher and Paykel Healthcare Limited, Dickinson and Company, Becton, and Hamilton Medical AG.

The North America mechanical ventilators market is characterized by intense competition, with numerous players vying for market share. Established companies leverage their extensive networks and technological expertise to maintain dominance, while emerging players focus on niche markets to differentiate themselves. The market is witnessing a wave of consolidation, with mergers and acquisitions becoming increasingly common. Additionally, the growing emphasis on digital transformation has intensified competition, as companies strive to offer innovative solutions that meet the evolving needs of healthcare providers.

RECENT HAPPENINGS IN THE MARKET

In April 2024, Medtronic plc launched a new AI-driven ventilator model, enhancing predictive monitoring capabilities and improving patient outcomes.

In June 2023, GE Healthcare partnered with a telehealth provider to integrate remote monitoring features into its ventilator systems by expanding its service offerings.

In January 2024, Philips Healthcare introduced a portable ventilator designed for home healthcare settings by addressing the growing demand for mobility and flexibility.

In September 2023, ResMed acquired a startup specializing in IoT-enabled ventilators, by strengthening its position in the smart healthcare segment.

In November 2023, Hamilton Medical collaborated with a research institution to develop next-generation ventilator technologies by focusing on energy efficiency and sustainability.

MARKET SEGMENTATION

This research report on the North America Mechanical Ventilators Market has been segmented and sub-segmented into the following.

By Product Type

- Critical Care

- Portable ventilators

By Mode

- Invasive ventilators

- Non-invasive ventilators

By End User

- Hospitals

- Home Healthcare

By Country

- U.S

- Canada

- Rest of North America

Frequently Asked Questions

What factors are contributing to the growth of the mechanical ventilators market in North America?

Factors such as an aging population, rising prevalence of respiratory diseases, advancements in technology leading to improved ventilator designs, and increased awareness about critical care are driving the growth of the mechanical ventilators market in North America.

Which countries in North America are major contributors to this market?

The United States and Canada are the primary contributors to the mechanical ventilators market in North America due to their robust healthcare infrastructure and high healthcare spending.

What are some technological trends influencing the market?

Trends include the integration of artificial intelligence for improved patient-ventilator synchronization, portable and compact ventilators for enhanced mobility, and the development of smart ventilators with remote monitoring capabilities

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com