North America Heat Meters Market Size, Share, Trends & Growth Forecast Report Segmented By Equipment Type, Pipe Size, Functionality, Technology, Application, And By Country (US, Canada, Mexico, and Brazil), Industry Analysis From 2025 to 2033

North America Heat Meters Market Size

The North America heat meters market was valued at USD 0.61 billion in 2024 and is anticipated to reach USD 0.65 billion in 2025 from USD 1.14 billion by 2033, growing at a CAGR of 7.26%, during the forecast period from 2025 to 2033.

Current Scenario Of The North America Heat Meters Market

The North America heat meters market covers devices designed to measure the amount of thermal energy consumed in heating systems, primarily for residential, commercial, and industrial applications. These meters are essential for accurately billing customers based on their actual energy usage, thereby promoting energy efficiency and conservation. Heat meters operate by measuring the flow of water or steam in heating systems and calculating the energy consumed based on temperature differentials.

The growth of this market is driven by increasing energy costs and a growing emphasis on energy efficiency. As consumers and businesses seek to reduce their energy expenditures, the demand for accurate measurement and monitoring solutions has intensified. Additionally, regulatory frameworks promoting energy conservation and sustainability are further propelling the adoption of heat meters. The integration of smart technologies, such as IoT-enabled heat meters, is also enhancing the market landscape by providing real-time data and analytics for better energy management.

MARKET DRIVERS

The increasing focus on energy efficiency and sustainability is a primary driver of the North America heat meters market. As energy costs continue to rise, both consumers and businesses are becoming more conscious of their energy consumption patterns. Heat meters play a crucial role in this context by providing accurate measurements of thermal energy usage, enabling users to monitor and optimize their heating systems. According to the U.S. Energy Information Administration, residential heating costs are projected to increase by 30% in the upcoming winter season, underscoring the need for effective energy management solutions.

Moreover, regulatory initiatives aimed at promoting energy conservation are further driving the demand for heat meters. Governments across North America are implementing policies that encourage the adoption of energy-efficient technologies, including heat meters, to reduce greenhouse gas emissions and enhance energy security. The U.S. Department of Energy has set ambitious targets for energy efficiency improvements, which are expected to drive investments in heat metering technologies. As industries and consumers increasingly prioritize energy efficiency, the North America heat meters market is set to benefit from this growing trend.

The rise of smart technologies and the Internet of Things (IoT) is another significant driver of the North America heat meters market. The integration of IoT capabilities into heat meters allows for real-time monitoring and data analytics, enabling users to make informed decisions about their energy consumption. As indicated in a report, the global IoT sphere is projected to reach a major share with a substantial portion of this growth driven by the need for advanced sensing technologies in energy management.

Furthermore, the increasing adoption of smart home technologies is contributing to the demand for IoT-enabled heat meters. As consumers seek greater control over their energy usage, the ability to remotely monitor and manage heating systems becomes increasingly appealing. This trend is particularly relevant in the context of rising energy prices and growing environmental awareness. As smart technologies continue to evolve and gain traction, the North America heat meters market is expected to experience significant growth, driven by the demand for innovative and efficient energy management solutions.

MARKET RESTRAINTS

Among the key restraints affecting the North America heat meters market is the high initial investment required for advanced metering technologies. While heat meters are essential for accurate energy measurement and billing, the cost of purchasing and installing these devices can be substantial, particularly for small and medium-sized enterprises. As per a survey conducted by the National Association of Manufacturers, 60% of manufacturers cited high equipment costs as a significant barrier to adopting new technologies. This reluctance to invest in heat metering solutions can hinder market growth, as companies may opt for less accurate or outdated measurement methods to manage their heating systems.

Additionally, the complexity of integrating heat meters into existing heating systems can pose challenges for manufacturers and end-users. Many heat metering solutions require specialized knowledge and expertise for installation and calibration, which can lead to increased operational costs and longer implementation times. The industry experts stress that the learning curve associated with mastering heat metering technologies can be steep, particularly for companies with limited experience in this area. Consequently, the high costs and integration complexities associated with heat meters may restrict their widespread adoption and is ultimately impacting the growth of the North America heat meters market.

Another significant restraint is the regulatory environment surrounding energy measurement and billing practices. As governments implement stricter regulations aimed at ensuring accurate billing and promoting energy efficiency, heat meter manufacturers must ensure that their products comply with these evolving standards. This can lead to increased costs associated with research and development, testing, and certification processes. According to the National Electrical Manufacturers Association, compliance with regulatory requirements can add up to 20% to the overall cost of product development. Thus, navigating the complex regulatory landscape can pose a significant challenge for heat meter manufacturers, potentially impacting their ability to bring new products to market efficiently.

MARKET OPPORTUNITIES

The increasing focus on renewable energy sources presents a significant opportunity for the North America heat meters market. As governments and industries strive to reduce carbon emissions and transition to cleaner energy solutions, the demand for heat meters that can effectively monitor and manage renewable heating systems is expected to rise. Heat meters are essential for optimizing the performance of systems such as solar thermal heating and biomass heating, ensuring efficient energy conversion and integration into the grid. The U.S. Energy Information Administration states that renewable energy is projected to account for 42% of total U.S. electricity generation by 2050 which is showcasing the growing importance of advanced metering solutions in this sector.

Moreover, the rise of smart grid technologies offers substantial opportunities for the North America heat meters market. Smart grids leverage advanced sensing and communication technologies to enhance the efficiency and reliability of electricity distribution systems. Heat meters are integral to smart grid applications, providing real-time data for monitoring energy consumption, detecting faults, and optimizing grid performance. According to a report by the U.S. Department of Energy, investments in smart grid technologies are expected to exceed $100 billion by 2030, creating a favorable environment for heat meter manufacturers. As utilities and energy providers increasingly adopt smart grid solutions, the demand for heat meters is likely to grow, positioning the North America heat meters market for significant expansion.

The expansion of district heating systems also presents a promising opportunity for the heat meters market. District heating involves the centralized production of heat, which is then distributed to multiple buildings through a network of insulated pipes. As urban areas continue to grow, the demand for efficient heating solutions is increasing, driving the need for accurate heat measurement in district heating applications. According to the International Energy Agency, district heating systems are expected to expand significantly in North America, further driving the demand for heat meters. As cities increasingly adopt district heating solutions to enhance energy efficiency and reduce emissions, the North America heat meters market is well-positioned to capitalize on this trend.

MARKET CHALLENGES

One of the foremost challenges for the North America heat meters market is the increasing competition from alternative measurement technologies. As the market evolves, new methods such as infrared thermography and wireless temperature sensors are gaining traction, offering unique advantages over traditional heat metering solutions. These alternatives can provide enhanced accuracy, flexibility, and ease of installation, which may attract customers away from conventional heat meters. This competitive landscape necessitates that heat meter manufacturers continuously innovate and improve their products to maintain market share.

Another significant challenge is the regulatory environment surrounding energy measurement and billing practices. As governments implement stricter regulations aimed at ensuring accurate billing and promoting energy efficiency, heat meter manufacturers must ensure that their products comply with these evolving standards. This can lead to increased costs associated with research and development, testing, and certification processes. As per the National Electrical Manufacturers Association, compliance with regulatory requirements can add up to 20% to the overall cost of product development. As a result, navigating the complex regulatory landscape can pose a significant challenge for heat meter manufacturers, potentially impacting their ability to bring new products to market efficiently.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024 to 2032 |

|

CAGR |

7.26% |

|

Segments Covered |

By Equipment Type, Pipe Size, Functionality, Technology, Application and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Danfoss (Denmark), Diehl Stiftung & Co. KG (Germany), Engelmann (Germany), Huizhong Instrumentation Co., Ltd. (China), ista International GmbH (Germany), Itron, Inc. (U.S.), Kamstrup A/S (Denmark), Landis+Gyr AG (Switzerland), Premier Control Technologies Ltd (Norfolk), QUNDIS GmbH (Germany), Siemens AG (Germany), Solenvis Flowmeters (U.K.), Sontex SA (Switzerland), Suntront Technology Co., Ltd. (China), TEKSAN (Turkey), Trend Control Systems Limited (U.K), VERAUT GmbH (Austria), Vital Energi Ltd. (U.K), We can Precision Instruments (China), WEIHAI PLOUMETER CO., LTD (China), ZENNER International GmbH & Co. KG. (Germany). |

SEGMENTAL ANALYSIS

By Equipment Type Insights

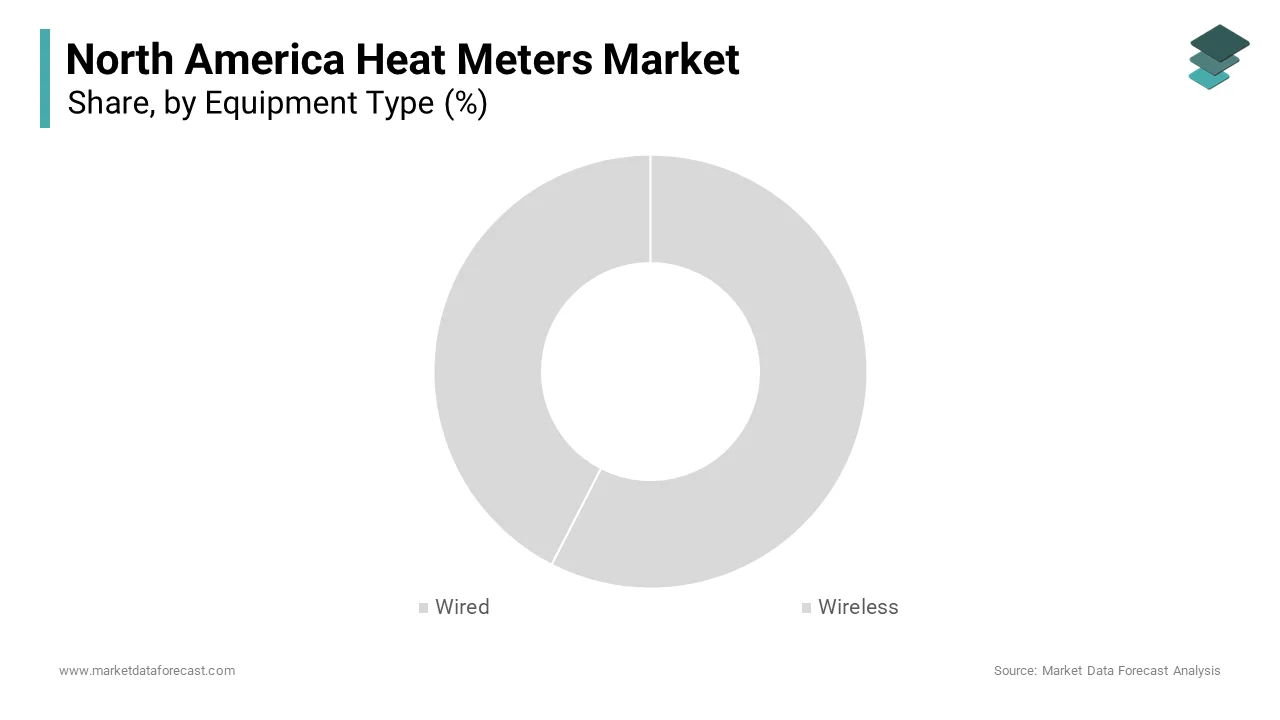

The wired segment held the largest market share 60.3% of the total market in 2024. This control over the market can be due to the broad application of wired heat meters in various applications, including residential, commercial, and industrial heating systems. Wired heat meters are known for their reliability, accuracy, and ease of integration into existing infrastructure, making them a preferred choice for many users. The industry estimates indicate that the demand for wired heat meters is expected to grow as manufacturers increasingly prioritize efficiency and performance in their heating systems. In addition, the ability of wired heat meters to provide continuous and real-time data is particularly appealing for applications requiring high precision and reliability. Additionally, the growing emphasis on energy efficiency and sustainability is driving the adoption of wired heat meters, as they enable better monitoring and control of heating systems.

In contrast, the fastest-growing segment in the North America heat meters market is the wireless category, projected to grow at a CAGR of 9.1% in the future. This progression can be influenced by the increasing demand for flexible and easy-to-install heat metering solutions that offer enhanced connectivity and data accessibility. Wireless heat meters utilize advanced communication technologies to transmit data, allowing for remote monitoring and management of heating systems. Furthermore, the rise of smart home technologies and IoT applications is driving the adoption of wireless heat meters. These meters can be easily integrated into existing systems, providing real-time data for monitoring and control without the need for extensive modifications.

By Pipe Size Insights

The 15 mm – 40 mm pipe size segment was the largest category by accounting for 52.1% of the total market share in 2024 owing to the prevalent use of heat meters in residential and small commercial applications, where heating systems typically utilize smaller pipe sizes. According to industry estimates, the demand for heat meters in this pipe size range is expected to grow as the focus on energy efficiency and accurate billing continues to rise among consumers and businesses alike. Moreover, the potential of heat meters in the 15 mm – 40 mm range to provide precise measurements for smaller heating systems is particularly appealing for applications requiring high accuracy and reliability. Additionally, the growing emphasis on energy conservation and sustainability is driving the adoption of heat meters in this segment, as they enable better monitoring and control of heating systems.

The swiftly advancing segment in the North America heat meters market is the 40 mm – 80 mm pipe size category which is believed to grow at a CAGR of 8.2% because of the increasing demand for heat meters in larger residential and commercial heating systems, where pipe sizes in this range are commonly used. Furthermore, the rise of district heating systems, which often utilize larger pipe sizes, is driving the adoption of heat meters in this segment. These systems require accurate measurement and monitoring to ensure efficient operation and billing, making heat meters in the 40 mm – 80 mm range increasingly attractive to manufacturers and end-users.

By Functionality Insights

The in-line segment prevailed in the North America heat meters market by commanding a substantial portion of the market share. This authority can be attributed to the far-reaching use of in-line heat meters in various applications, including residential, commercial, and industrial heating systems. In-line heat meters are known for their reliability, accuracy, and ease of integration into existing infrastructure, making them a preferred choice for many users. The industry estimates reveal that the demand for in-line heat meters is expected to grow as manufacturers increasingly prioritize efficiency and performance in their heating systems. The feature of in-line heat meters to provide continuous and real-time data is particularly appealing for applications requiring high precision and reliability. Besides these, the growing emphasis on energy efficiency and sustainability is driving the adoption of in-line heat meters as they enable better monitoring and control of heating systems.

The rapidly expanding segment in the North America heat meters market is the insertion category and is estimated to advance at a CAGR of 9.3% throughout the coming years. This rise can be associated with the increasing demand for flexible and easy-to-install heat metering solutions that offer enhanced connectivity and data accessibility. Insertion heat meters utilize advanced communication technologies to provide accurate measurements without the need for extensive modifications to existing piping systems. The rise of smart technologies and the Internet of Things (IoT) is driving the adoption of insertion heat meters. These meters can be easily integrated into existing systems, providing real-time data for monitoring and control, which is particularly beneficial for retrofitting older heating systems.

By Technology Insights

The mechanical technology segment popularised as the top performer in the North America heat meters market and possessed 56.3% of the total market share in 2024. This position can be caused by the long-standing reliability and simplicity of mechanical heat meters, which have been widely used in residential and commercial applications for decades. Mechanical heat meters operate based on the flow of water through a turbine or impeller, providing accurate measurements of thermal energy consumption. According to industry estimates, the demand for mechanical heat meters is expected to remain strong as they continue to be a cost-effective solution for many users. The ability of mechanical heat meters to provide consistent and reliable measurements is particularly appealing for applications requiring straightforward installation and maintenance. Apart from this, the growing emphasis on energy efficiency and sustainability is driving the adoption of mechanical heat meters, as they enable better monitoring and control of heating systems.

The swiftly accelerating category in the North America heat meters market is the ultrasonic technology segment and is estimated to advance at a CAGR of 10.4% in the coming years. This escalating in performance can be attributed to the increasing demand for high-precision heat measurement solutions that offer enhanced performance and reliability. Ultrasonic heat meters utilize sound waves to measure the flow of water and temperature differentials, providing highly accurate readings without moving parts. Furthermore, the rise of smart technologies and IoT applications is driving the adoption of ultrasonic heat meters. These meters can provide real-time data for monitoring and control, enabling enhanced energy management and operational efficiency.

By Application Insights

The household application segment retained the dominant position in the North America heat meters market by contributing 43.7% of the total market share in 2024 owing to the ubiquitous use of heat meters in residential heating systems where accurate measurement of thermal energy consumption is essential for billing and energy management. The U.S. Energy Information Administration emphasizes that residential heating costs are projected to increase significantly, underscoring the need for effective measurement solutions. The demand for heat meters in households is expected to grow as consumers become more conscious of their energy usage and seek to optimize their heating systems. The potential to provide precise measurements for household heating systems is particularly appealing for applications requiring high accuracy and reliability. In addition, the growing emphasis on energy efficiency and sustainability is driving the adoption of heat meters in residential applications, as they enable better monitoring and control of heating systems.

The quickly progressing segment is the industrial application category which is calculated to advance at a CAGR of 8.4% over the years. This development can be linked to the increasing demand for heat meters in industrial heating systems, where precise measurement and monitoring are critical for optimizing energy consumption and ensuring operational efficiency. Also, the rise of smart manufacturing and Industry 4.0 initiatives is driving the adoption of heat meters in industrial applications. These meters can provide real-time data for monitoring and control, enabling enhanced energy management and operational efficiency.

COUNTRY ANALYSIS

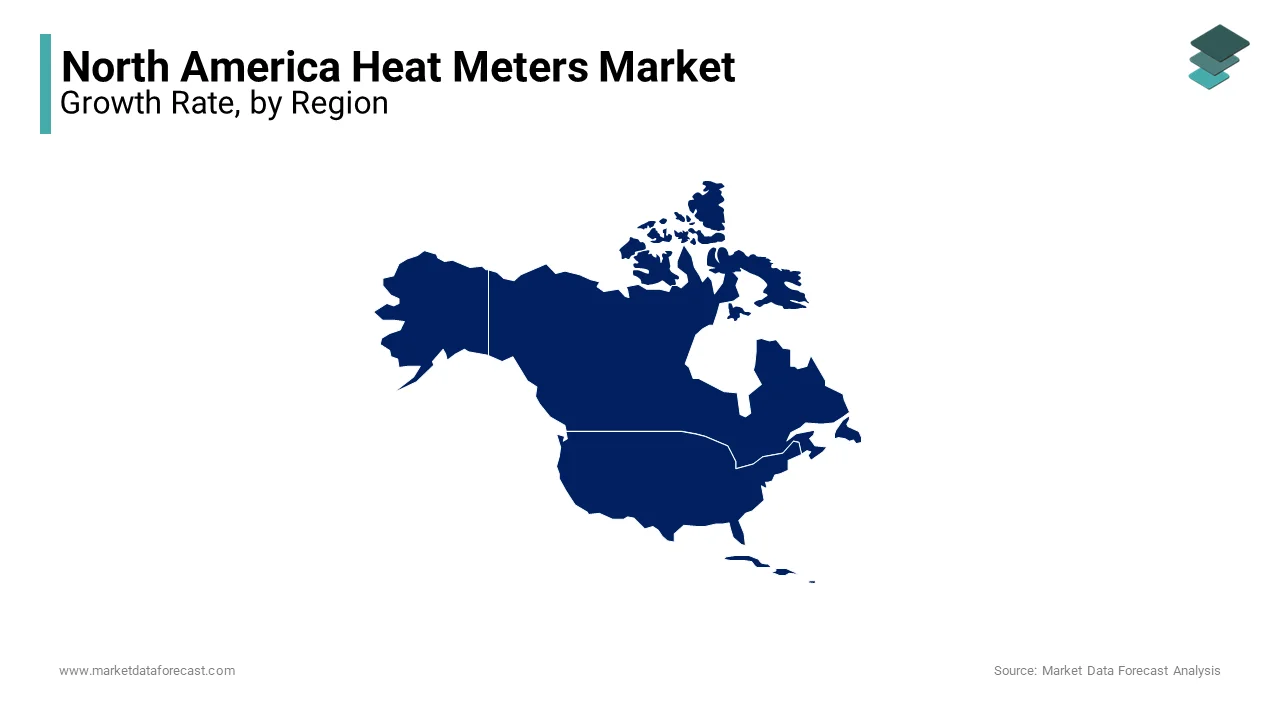

The United States held a dominant position in the North America heat meters market by accounting for 74.9% of the total market share in 2024. The U.S. market is defined by a robust demand for heat metering solutions across various sectors, including residential, commercial, and industrial applications. As per the U.S. Department of Energy, the increasing focus on energy efficiency and sustainability is driving investments in heat metering technologies, further bolstering the market. The rapid adoption of smart technologies and the push for renewable energy solutions are also contributing to the growth of the heat meters market in the U.S., as these applications require accurate measurement and monitoring. Moreover, the presence of key players and a well-established manufacturing base in the United States enhances the market's competitive landscape. Major companies such as Landis+Gyr, Itron, and Kamstrup are actively involved in developing innovative heat metering solutions, driving technological advancements in the industry.

Canada continues to develop steadily in the market for heat meters in North America which is supported by the adoption of renewable energy-based heating networks, particularly in colder provinces, and ongoing governmental support for carbon-neutral building initiatives. The Canadian market is driven by a growing interest in energy efficiency and sustainability, as the government emphasizes the importance of reducing greenhouse gas emissions. The Natural Resources Canada states that the country aims to achieve a 30% reduction in greenhouse gas emissions by 2030, which is expected to drive investments in heat metering technologies for residential and commercial applications. The surging adoption of smart technologies and the expansion of district heating systems are also contributing to the demand for heat meters in Canada.

The Rest of North America is charting the highest trajectory in the regional heat meters market and is reflected in a CAGR of 6.8% in the future. This is propelled by expanding urbanization, rising investments in sustainable heating solutions, and growing awareness around precise thermal energy management across commercial and industrial facilities. The Mexican market is characterized by a growing demand for heat metering solutions in residential and industrial applications. According to the Mexican Association of Manufacturers of Electrical Equipment, the market for electrical equipment, including heat meters, is expected to grow significantly as industries modernize and adopt advanced technologies.

Top Players in the Global North America Heat Meters Market

In the North America heat meters market, several key players have established themselves as leaders, contributing significantly to the overall market dynamics.

Landis+Gyr is one of the foremost manufacturers, renowned for its high-quality heat metering solutions that cater to various applications, including residential, commercial, and industrial heating systems. By consistently pushing technological boundaries and offering a diverse range of products, the company has secured a leadership role, prioritizing innovative metering solutions that boost both reliability and efficiency.

Another major player is Itron, a well-known name in the metering industry. Itron offers a diverse range of heat metering solutions, including both mechanical and electronic meters, which are widely used in various applications. Through strategic investments in R&D, the firm has unveiled ground-breaking solutions tailored to shifting customer demands, strengthening its competitive edge within the North America heat meters industry.

Kamstrup is also a prominent player in the heat meters market, recognized for its innovative metering solutions and commitment to sustainability. Kamstrup's heat meters are widely used in district heating systems and residential applications, making them integral to the transition towards cleaner and more efficient energy solutions. Catering to eco-aware consumers, the company’s drive to create energy-saving, high-performance meters has elevated its brand image, earning it recognition as a reliable name across the regional market.

Major Strategies Used By Key Players in the North America Heat Meters Market

Key players in the North America heat meters market employ a variety of strategies to strengthen their market position and enhance competitiveness. One prominent strategy is the focus on innovation and technological advancement. Companies like Landis+Gyr and Itron invest heavily in research and development to create cutting-edge heat metering technologies that improve performance, accuracy, and energy efficiency.

Another significant strategy is the expansion of product portfolios to cater to diverse consumer needs. Manufacturers are increasingly offering a wide range of heat metering solutions, including mechanical, ultrasonic, and smart meters, to appeal to various applications. For instance, Kamstrup has introduced a range of smart heat meters specifically designed for district heating systems, addressing the growing demand for advanced metering solutions.

Strategic partnerships and collaborations also play a crucial role in enhancing market presence. Companies often collaborate with utilities and energy providers to expand their reach and improve distribution channels. For example, partnerships with municipalities enable heat meter producers to integrate their technologies into a wider array of applications, thereby increasing sales and market penetration.

Competition in the North America Heat Meters Market

The competition in the North America heat meters market is characterized by a mix of established players and emerging manufacturers, all vying for market share in a rapidly evolving landscape. Major companies such as Landis+Gyr, Itron, and Kamstrup dominate the market, leveraging their strong brand recognition, extensive distribution networks, and commitment to innovation. These industry leaders continuously invest in research and development to enhance metering performance, accuracy, and compliance with stringent environmental regulations, thereby maintaining their competitive advantage.

Emerging players are also entering the market, often focusing on niche segments or innovative technologies, such as smart metering solutions and IoT-enabled devices. This influx of new entrants intensifies competition, as they seek to capture market share by offering unique value propositions and addressing the growing demand for sustainable solutions. Additionally, the increasing consumer preference for eco-friendly products is prompting established manufacturers to adapt their offerings and invest in cleaner technologies, further heightening competition.

Price competition is another significant factor influencing the market dynamics. As manufacturers strive to attract price-sensitive consumers, they may engage in competitive pricing strategies, which can impact profit margins. However, companies that prioritize quality, performance, and customer service are likely to differentiate themselves and build brand loyalty, allowing them to navigate the competitive landscape effectively.

Major Actions Taken by Key Companies in the North America Heat Meters Market

- In March 2023, Landis+Gyr launched a new line of advanced heat meters designed for district heating applications, reinforcing its commitment to innovation and market leadership.

- In January 2023, Itron introduced a new series of smart heat meters aimed at residential applications, catering to the growing demand for energy-efficient solutions.

- In February 2023, Kamstrup expanded its product portfolio by launching a new range of ultrasonic heat meters specifically designed for commercial buildings, addressing the increasing demand for accurate measurement.

- In April 2023, Honeywell partnered with a leading energy provider to integrate its heat metering solutions into a new line of smart home technologies, enhancing its market presence.

- In May 2023, Siemens acquired a small heat metering technology firm to strengthen its capabilities in the market and expand its product offerings.

- In June 2023, Schneider Electric announced a strategic collaboration with a major utility company to develop smart grid solutions that incorporate advanced heat metering technologies.

- In July 2023, Sensus launched a new series of heat meters designed for industrial applications, reflecting its commitment to innovation and addressing the growing demand for advanced solutions.

- In August 2023, Elster Group introduced a new line of mechanical heat meters aimed at the residential market, targeting the increasing demand for cost-effective solutions.

- In September 2023, Aclara expanded its distribution network by partnering with major retailers to increase the availability of its heat metering equipment across North America.

- In October 2023, Badger Meter unveiled a new series of smart heat meters designed for the commercial sector, aiming to capture a larger share of the market.

KEY MAKRET PLAYERS

Danfoss (Denmark), Diehl Stiftung & Co. KG (Germany), Engelmann (Germany), Huizhong Instrumentation Co., Ltd. (China), ista International GmbH (Germany), Itron, Inc. (U.S.), Kamstrup A/S (Denmark), Landis+Gyr AG (Switzerland), Premier Control Technologies Ltd (Norfolk), QUNDIS GmbH (Germany), Siemens AG (Germany), Solenvis Flowmeters (U.K.), Sontex SA (Switzerland), Suntront Technology Co., Ltd. (China), TEKSAN (Turkey), Trend Control Systems Limited (U.K), VERAUT GmbH (Austria), Vital Energi Ltd. (U.K), We can Precision Instruments (China), WEIHAI PLOUMETER CO., LTD (China), ZENNER International GmbH & Co. KG. (Germany). are the market players that are dominating the North America heat meters market.

MARKET SEGMENTATION

This research report on the North America heat meters market is segmented and sub-segmented into the following categories.

By Equipment Type

- Wired

- Wireless

By Pipe Size

- 15 mm – 40 mm

- 40 mm – 80 mm

By Functionality

- Insertion

- In-line

By Technology

- Mechanical

- Ultrasonic

- Others

By Application

- Household

- Commercial

- Industrial

By Country

- U.S

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What is the role of heat meters in energy management?

Heat meters measure thermal energy consumption in heating and cooling systems, helping optimize energy efficiency and reduce costs.

Why is the demand for heat meters growing in North America?

Increasing focus on energy conservation, government regulations on energy efficiency, and the rise of district heating and cooling systems are driving demand.

Which sectors rely heavily on heat meters?

Commercial buildings, residential complexes, industrial plants, and district heating networks use heat meters to monitor and manage energy usage.

Which countries in North America lead in heat meter adoption?

The United States and Canada are major markets, with growing adoption in smart grid infrastructure and renewable heating solutions.

Which companies dominate the North American heat meters market?

Leading players include Kamstrup, Siemens, Diehl Metering, Landis+Gyr, and Itron, offering advanced metering solutions for precise energy measurement.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]