North America Dietary Supplements Market Size, Share, Trends & Growth Forecast Report By Ingredient (Vitamins, Botanicals, Minerals, Proteins & Amino Acids, Fibers & Specialty Carbohydrates, Omega Fatty Acids, Others), Form, Application, End-User, Distribution Channel and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Dietary Supplements Market Size

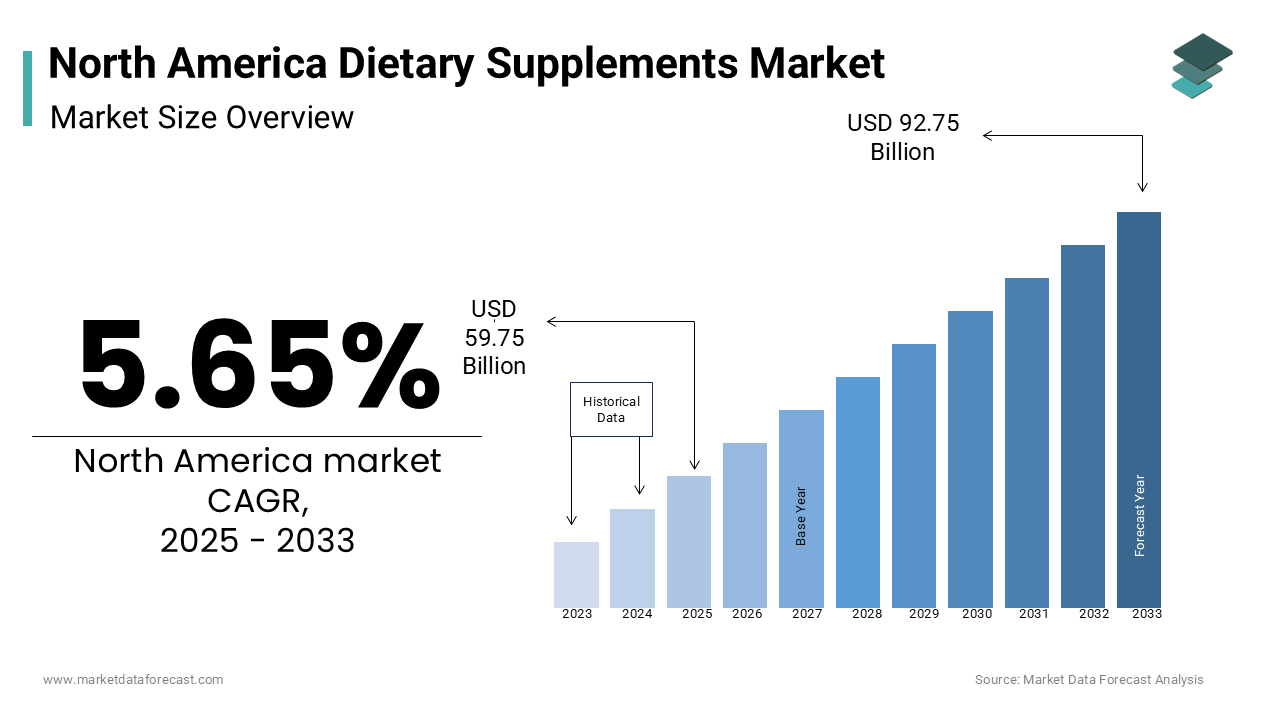

The North America dietary supplements market was worth USD 56.55 billion in 2024. The North American market is estimated to grow at a CAGR of 5.65% from 2025 to 2033 and be valued at USD 92.75 billion by the end of 2033 from USD 59.75 billion in 2025.

The North American dietary supplements market is expanding as more consumers prioritize health and wellness. With a growing focus on preventive healthcare, individuals are incorporating vitamins, minerals, and herbal supplements into their daily routines. According to the Council for Responsible Nutrition, nearly 80% of American adults reported using dietary supplements in 2023, highlighting their widespread acceptance.

Dietary supplements include a wide range of products such as vitamins, minerals, herbal extracts, amino acids, and probiotics. These are designed to enhance overall health or address specific nutritional needs. While traditional multivitamins once dominated the industry, there is now a shift toward functional and specialized supplements, including plant-based formulations and personalized nutrition solutions.

Beyond market trends, the broader health landscape underscores the importance of dietary supplementation. The Centers for Disease Control and Prevention (CDC) states that nearly 10% of the U.S. population is deficient in essential nutrients like vitamin D and iron, reinforcing the demand for dietary supplements. The World Health Organization notes that poor nutrition contributes to nearly 20% of all global deaths, emphasizing the role of proper supplementation in maintaining long-term well-being.

With an aging population and evolving consumer preferences, the North American dietary supplements market will remain a key player in the global nutrition industry. It continues to address both lifestyle-driven and medical nutritional needs.

MARKET DRIVERS

Integration of Personalized Nutrition Solutions

Personalized nutrition is revolutionizing the dietary supplements industry by offering customized health solutions based on individual needs. Advances in genetic testing, gut microbiome analysis, and artificial intelligence-driven recommendations have made it possible to tailor supplement regimens for optimal health. Research from the National Institutes of Health shows that genetic variations can influence how the body absorbs and metabolizes nutrients, making standardized supplementation less effective for some individuals. For example, people with variations in the MTHFR gene may have difficulty processing folic acid, requiring methylated forms of B vitamins for proper absorption. Beyond genetics, lifestyle factors such as diet, sleep patterns, and stress levels also play a crucial role in nutritional needs. The American Psychological Association reports that 77% of adults experience stress that affects their health, increasing the demand for supplements targeting stress relief and cognitive support. The popularity of DNA-based supplement services and personalized vitamin subscriptions has surged, with companies using AI algorithms to analyze biomarkers and recommend precise formulations. This shift toward tailored supplementation is empowering consumers to take a more targeted approach to their health rather than relying on generic multivitamins.

Expansion of Plant-Based and Functional Ingredients

The growing preference for plant-based diets has significantly influenced the types of supplements consumers seek. As more individuals move away from synthetic ingredients, botanical extracts and functional supplements have gained traction. The Plant Based Foods Association states that over 35% of Americans are actively reducing their meat consumption, leading to a higher demand for plant-derived nutrients such as pea protein, algae-based omega-3s, and herbal adaptogens. Herbal supplements like turmeric, ashwagandha, and elderberry are particularly popular due to their scientifically studied health benefits. The National Center for Complementary and Integrative Health shows that turmeric contains curcumin, a compound with strong anti-inflammatory properties that may help with joint health and chronic conditions. Similarly, ashwagandha has been shown to support stress reduction by lowering cortisol levels, as confirmed by studies published in the Journal of Alternative and Complementary Medicine. Functional probiotics are also gaining widespread use, as Harvard Medical School emphasizes the crucial role of gut microbiota in digestion, immune function, and mental well-being.

MARKET RESTRAINTS

Regulatory Evolution and Compliance Challenges

As awareness of supplement safety grows, regulatory scrutiny is increasing. The U.S. Food and Drug Administration (FDA) reports that nearly 50% of recalled supplements in recent years contained unapproved ingredients or misleading claims. The Council for Responsible Nutrition has emphasized the importance of better enforcement to protect consumers, especially as an estimated 23,000 emergency room visits annually in the U.S. are linked to supplement-related adverse effects, according to the Centers for Disease Control and Prevention.

Consumer Skepticism Due to Lack of Standardization

The dietary supplements industry faces challenges due to inconsistent product quality and misleading health claims. A study by the Journal of the American Medical Association found that nearly 20% of supplements tested did not contain the labeled ingredients in the correct amounts. Additionally, the Federal Trade Commission has taken action against companies making false claims, emphasizing the need for standardized regulations. The widespread presence of misinformation on social media also contributes to consumer skepticism, with the Pew Research Center reporting that nearly 64% of Americans encounter health-related misinformation online.

MARKET OPPORTUNITIES

Growing Awareness of Gut Health and the Microbiome

Scientific advancements in gut health research are increasing consumer interest in probiotics, prebiotics, and digestive health supplements. The National Institutes of Health states that nearly 70% of the immune system resides in the gut, making digestive health crucial for overall well-being. The Human Microbiome Project has revealed that gut bacteria influence not just digestion but also mental health, metabolism, and immune function. Studies published in Nature indicate that dietary habits and lifestyle factors can significantly impact gut microbiota composition, prompting a surge in demand for microbiome-friendly foods and supplements. With nearly 62 million Americans diagnosed with digestive disorders, as reported by the National Institute of Diabetes and Digestive and Kidney Diseases, probiotics and fiber supplements offer an opportunity for brands to cater to consumers seeking better digestive health.

Aging Population and Increased Focus on Longevity

As life expectancy rises, older adults are prioritizing health and wellness, leading to increased demand for age-specific supplements. According to the U.S. Census Bureau, the number of Americans aged 65 and older is projected to nearly double by 2060, reaching 94.7 million. Research from Harvard Medical School notes that aging affects nutrient absorption, leading to deficiencies in key vitamins such as B12, D, and calcium. Additionally, the National Osteoporosis Foundation reports that half of all adults over 50 are at risk of bone fractures due to declining bone density. Supplements targeting joint health, cognitive function, and cardiovascular support are gaining popularity as seniors seek ways to maintain mobility and mental sharpness. This shift presents a significant opportunity for the development of formulations tailored to healthy aging.

MARKET CHALLENGES

Sustainability and Ethical Sourcing Issues

Sustainability concerns related to supplement production are becoming more prominent as consumers demand ethically sourced ingredients and environmentally friendly packaging. The Environmental Protection Agency (EPA) reports that plastic packaging accounts for over 30% of landfill waste is prompting companies to shift toward biodegradable or recyclable alternatives. Also, the sourcing of raw materials, such as omega-3 from fish oil or herbal extracts from wild plants, raises concerns about overfishing and deforestation. The World Wildlife Fund warns that unsustainable harvesting practices threaten biodiversity and ecosystem balance. As a result, supplement brands must invest in sustainable sourcing, fair trade ingredients, and eco-friendly packaging to align with consumer expectations while managing cost implications.

Rising Ingredient Costs and Supply Chain Disruptions

Fluctuations in raw material prices and supply chain disruptions pose a significant challenge to supplement manufacturers. The U.S. Department of Agriculture notes that extreme weather conditions and geopolitical factors have impacted the availability of key ingredients such as plant-based proteins, omega-3s, and herbal extracts. The COVID-19 pandemic also exposed vulnerabilities in global supply chains, leading to delays and increased production costs. According to the U.S. Bureau of Labor Statistics, transportation and logistics costs have surged in recent years, further driving up supplement prices. To remain competitive, companies must find ways to optimize sourcing strategies and manage supply chain risks while maintaining product affordability for consumers.

SEGMENTAL ANALYSIS

By Ingredient Insights

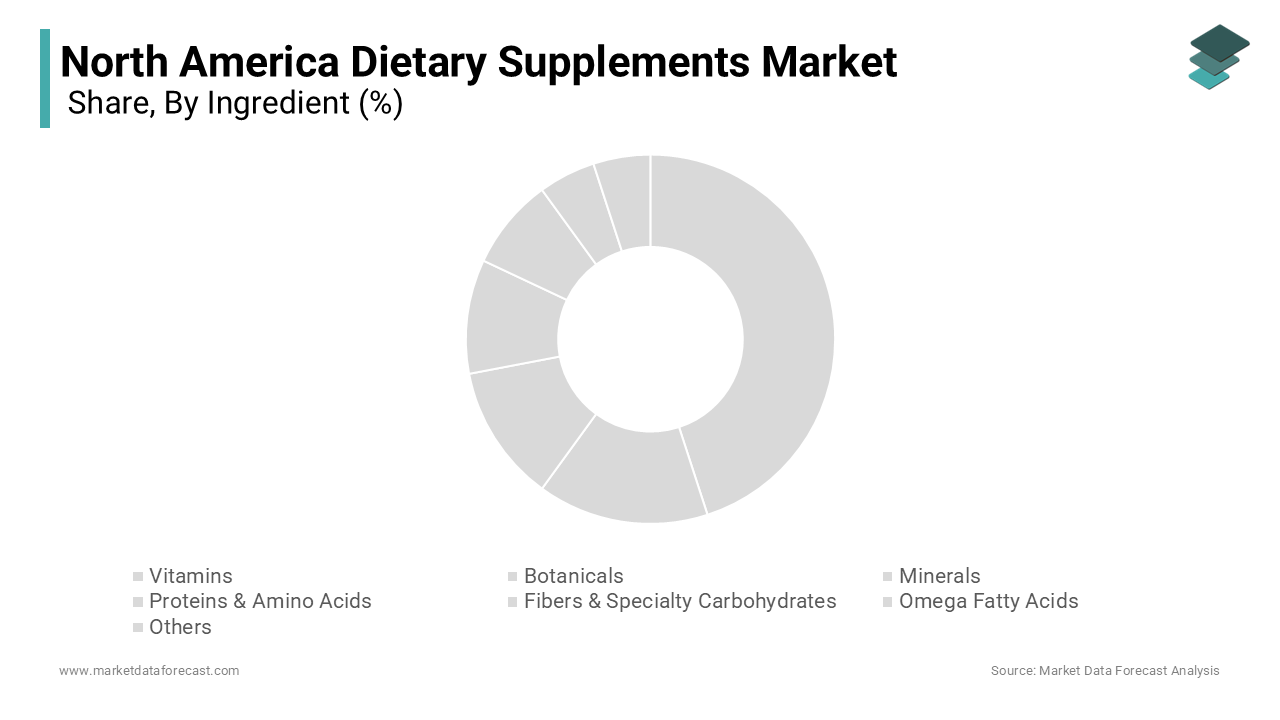

In 2024, vitamins were the largest segment in the North America dietary supplements market, holding a market share of 34.5%. The high demand was driven by rising awareness of immune health and overall well-being. According to the National Institutes of Health, nearly 90% of Americans did not get enough vitamin D from their diet, making supplements essential for bone health and immune function. The CDC also reported that 40% of the U.S. population had inadequate vitamin C intake, further boosting demand. The growing aging population, which relies on vitamins for bone strength and energy, also contributed to the segment’s dominance.

Omega fatty acids will grow at the fastest rate in the coming years, with a projected CAGR of 9.8%. Increased awareness of heart health and cognitive function will drive this demand. The American Heart Association states that heart disease causes nearly 697,000 deaths per year in the U.S., making omega-3 supplements crucial for cardiovascular support. Additionally, the Alzheimer’s Association states that 6.9 million Americans aged 65 and older are living with Alzheimer’s disease, pushing demand for brain-supporting supplements. As more consumers seek natural solutions for heart and brain health, omega fatty acids will gain popularity. The segment’s expansion will also be fueled by plant-based omega alternatives for vegetarian and vegan consumers.

By Form Insights

In 2024, tablets held the largest share of the North American dietary supplements market, contributing 41.2% of total sales. Their popularity was driven by affordability, extended shelf life, and the ability to deliver high doses of nutrients in a compact form. The National Institutes of Health stressed that over half of U.S. adults consumed at least one dietary supplement daily, with multivitamins in tablet form being the most widely used. Consumers also preferred tablets because they offered precise dosage control and required minimal preservatives. Pharmacies, supermarkets, and online platforms stocked a vast range of tablet-based supplements, ensuring their widespread accessibility.

Gummies are projected to be the fastest-growing segment, with an anticipated CAGR of 10.5%. This growth will be fueled by rising consumer demand for chewable, easy-to-consume supplements, particularly among children and adults with difficulty swallowing pills. The CDC noted that 30% of U.S. adults struggle with pill swallowing, increasing the preference for alternative formats like gummies. Additionally, concerns over sugar content in supplements have led to innovations in sugar-free and vitamin-rich gummy formulations. As companies introduce functional gummies enriched with probiotics, collagen, and omega fatty acids, this segment will gain traction. The expansion of plant-based and allergen-free gummy options will further drive adoption across diverse consumer groups.

By Application Insights

In 2024, general health supplements dominated the North American dietary supplements market, accounting for 38.6% of total sales. This category led due to its broad consumer appeal, covering multivitamins, minerals, and essential nutrients that support overall well-being. The National Center for Health Statistics reported that 57.6% of U.S. adults used dietary supplements regularly, with multivitamins being the most consumed. As chronic diseases like obesity and diabetes became more prevalent, consumers turned to supplements for preventive health measures. The growing awareness of micronutrient deficiencies and the convenience of daily multivitamin use further solidified this segment’s leadership in the market.

Immunity supplements are projected to grow at the fastest rate, with an estimated CAGR of 9.2%. The rising focus on immune health, particularly after the COVID-19 pandemic, has significantly increased consumer demand. The CDC noted that influenza affects between 9 and 41 million Americans annually, reinforcing the importance of immune-boosting nutrients like vitamin C, zinc, and probiotics. Additionally, the National Institutes of Health stated that nearly one-third of the U.S. population had low vitamin D levels, a key factor in immune function. As more consumers prioritize preventive healthcare and natural solutions to strengthen immunity, the demand for vitamin-rich supplements, herbal blends, and probiotics will continue to surge.

By End-user Insights

In 2024, adults represented the largest end-user segment in the North America dietary supplements market, holding 62.3% of the total market share. The widespread use of supplements among adults was driven by growing concerns about nutritional gaps, stress management, and lifestyle-related health issues. According to the National Health and Nutrition Examination Survey, nearly 58% of U.S. adults regularly consumed dietary supplements, with multivitamins, omega fatty acids, and probiotics being the most common choices. Rising work-related stress, sleep disturbances, and digestive issues also contributed to the demand for supplements supporting mental well-being and gut health. As more individuals sought preventive healthcare solutions, the adoption of dietary supplements continued to expand.

The geriatric population is expected to be the fastest-growing end-user segment, with a projected CAGR of 8.7% in the coming years. The U.S. Census Bureau estimates that by 2030, one in five Americans will be aged 65 or older, significantly increasing the need for supplements targeting bone health, cognitive function, and cardiovascular support. The National Osteoporosis Foundation reported that 10 million Americans aged 50 and older have osteoporosis, making calcium and vitamin D supplements essential for aging populations. Additionally, the prevalence of age-related cognitive decline is driving demand for brain-boosting supplements containing omega-3 fatty acids and antioxidants. As life expectancy rises, the focus on healthy aging and disease prevention will continue to accelerate growth in this segment.

By Distribution Channel Insights

In 2024, the offline distribution channel held the majority share of 68.5% in the North America dietary supplements market. Pharmacies were the dominant sub-segment, as consumers preferred purchasing supplements with guidance from pharmacists and healthcare professionals. According to the National Community Pharmacists Association, over 90% of Americans live within five miles of a pharmacy, making them easily accessible for purchasing health-related products. Supermarkets and hypermarkets also contributed significantly, with large retail chains expanding their supplement sections. Consumers valued the ability to physically inspect products and access promotions, leading to sustained demand for brick-and-mortar shopping despite the rise of e-commerce.

The online distribution channel is expected to experience the fastest growth, with a projected CAGR of 10.2% over the next few years. The U.S. Census Bureau reported that e-commerce sales increased by 7.6% in 2024 is reflecting a shift in consumer shopping habits. The rise of direct-to-consumer (DTC) brands and subscription-based supplement services has fueled online sales. Additionally, the convenience of doorstep delivery and access to a wider range of products has encouraged more consumers to purchase supplements online. The U.S. Food and Drug Administration has emphasized stricter regulations on online supplement sales, ensuring greater product transparency and safety, further boosting consumer trust in digital purchasing channels.

REGIONAL ANALYSIS

In 2024, the United States led the North American dietary supplements industry, holding a 78.9% market share with revenues reaching USD 121.56 billion. This dominance stemmed from a strong emphasis on preventive healthcare and an aging population. The U.S. Census Bureau reported that the median age reached 38.9 years in 2022, reflecting a demographic increasingly reliant on supplements for wellness. Moreover, rising obesity and cardiovascular disease rates fueled demand for nutritional products. A growing focus on fitness and immunity also contributed to higher consumption, solidifying the country’s position as the region’s largest market.

Canada's dietary supplements market is projected to experience a compound annual growth rate (CAGR) of 6.37% from 2024 to 2032, positioning it as the fastest-growing market in North America. This growth is attributed to increasing health consciousness among Canadians and a shift towards preventive healthcare. The Canadian Community Health Survey indicated that a significant portion of the population is actively seeking ways to improve their health through nutrition and supplementation. Furthermore, the rising aging population in Canada, as reported by Statistics Canada, is contributing to the increased demand for dietary supplements aimed at addressing age-related health concerns. The government's initiatives to promote healthy living and the availability of a wide range of products are also expected to support this upward trend.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Amway Corp. (US), Glanbia PLC (Ireland), Abbott (US), Bayer AG (Germany), Pfizer Inc. (US), ADM (US), Nu Skin Enterprises, Inc. (US), GlaxoSmithKline plc (UK), Bionova (Mexico), Herbalife International of America, Inc. (US), Nature’s Sunshine Products, Inc. (US), and NutraBlend Foods (Canada) are some of the prominent key market players in the North America Dietary Supplements Market.

The North America dietary supplements market is evolving rapidly, leading to intense competition among established companies and emerging brands. The industry has expanded beyond vitamins and minerals into specialized segments such as gut health, cognitive function, and plant-based wellness. This diversification has created a fragmented competitive landscape where companies must innovate constantly to keep consumer interest.

Pharmaceutical and biotech companies are now entering the supplement space, leveraging their expertise in clinical research and precision health. These firms develop evidence-backed formulations that challenge traditional supplement brands relying on herbal and natural ingredients. As a result, established players must invest more in scientific validation and product transparency to maintain consumer trust.

Competition is also increasing from private-label brands launched by major retailers. Grocery stores, pharmacies, and online marketplaces now offer their own supplement lines at lower prices, making affordability a key factor in consumer choices. To stay competitive, leading brands focus on premium formulations, sustainability initiatives, and partnerships with healthcare professionals.

Another emerging trend is the rise of artificial intelligence in personalized nutrition. AI-driven health assessments and tailored supplement subscriptions are reshaping competition by offering hyper-personalized solutions, making it harder for one-size-fits-all brands to stay dominant.

Top Players in the market

Amway

Amway has established itself as a leading provider of dietary supplements, leveraging its direct-selling model and extensive product portfolio. The company focuses on high-quality, plant-based ingredients sourced from its certified organic farms, ensuring transparency and sustainability. Its Nutrilite brand is particularly well-known for offering vitamins, minerals, and herbal supplements catering to diverse health needs. Amway continuously invests in research and development to enhance product efficacy and innovation. Strong customer loyalty, personalized health solutions, and digital engagement strategies have further strengthened its market position, making it a dominant force in North America's dietary supplements industry.

Herbalife Nutrition

Herbalife Nutrition has built a strong presence in the dietary supplements market through its extensive network of independent distributors. The company's focus on weight management, sports nutrition, and general wellness has enabled it to cater to a wide consumer base. With a commitment to scientific research, Herbalife Nutrition develops formulations that support various health goals, from energy and immunity to digestive wellness. It also places significant emphasis on personalized nutrition and coaching, creating a more interactive consumer experience. Its strategic marketing efforts, combined with product expansion and global reach, have solidified its position as a key player in the industry.

Nature’s Bounty (Nestlé Health Science)

Nature’s Bounty, now part of Nestlé Health Science, has been a trusted name in dietary supplements, offering a broad range of vitamins, herbal products, and specialty formulations. The company is known for its focus on quality assurance and rigorous testing, ensuring product safety and effectiveness. With an emphasis on innovation, Nature’s Bounty continues to develop new formulations that align with evolving health trends. Its strong retail presence, e-commerce expansion, and commitment to scientific advancements have contributed to its widespread consumer trust. By integrating wellness solutions with cutting-edge research, the company remains a significant player in North America’s dietary supplements market.

Top strategies used by the key market participants

Functional Ingredient Integration

Top companies are incorporating multifunctional ingredients into their products to cater to consumers seeking comprehensive health solutions. Instead of single-nutrient formulations, they develop blends that support multiple aspects of wellness, such as combining probiotics with vitamins for gut and immune health or integrating adaptogens with minerals for stress management. This approach not only enhances product effectiveness but also appeals to consumers looking for convenience in their supplementation routines.

Clinical Trials and Regulatory Compliance Focus

To build credibility and differentiate from competitors, leading brands are increasingly conducting clinical trials to validate the efficacy of their products. By securing scientific backing and aligning with stringent regulatory standards, they enhance consumer confidence and gain approval from healthcare professionals. Compliance with evolving FDA guidelines, third-party testing certifications, and transparency in labeling further strengthens their market position, allowing them to stand out in a sector often scrutinized for unverified claims.

Subscription-Based Wellness Programs

Companies are shifting toward subscription-based models that provide ongoing, customized supplement regimens. These programs use consumer health assessments to recommend personalized products, ensuring consistent engagement and brand loyalty. Subscription services also integrate wellness coaching, digital tracking tools, and periodic health evaluations, creating a more interactive and long-term relationship between brands and consumers.

RECENT MARKET DEVELOPMENTS

- In March 2025, NotCo announced its plan to launch a botanical GLP-1 booster designed to be added to any food, aiding in appetite control and weight loss. This product aims to naturally stimulate the body's GLP-1 hormone production, promoting a feeling of fullness.

- In January 2025, Clinique La Prairie introduced a €100 million Longevity Fund to invest in early-stage and Series B startups focused on medical, nutrition, wellness, and movement technologies. The fund aims to scale companies bridging science and longevity, with future closings targeting €300 million.

MARKET SEGMENTATION

This research report on the North American dietary supplements market is segmented and sub-segmented based on categories.

By Ingredient

- Vitamins

- Botanicals

- Minerals

- Proteins & Amino Acids

- Fibers & Specialty Carbohydrates

- Omega Fatty Acids

- Others

By Form

- Tablets

- Capsules

- Soft gels

- Powders

- Gummies

- Liquids

- Others

By Application

- Energy & Weight Management

- General Health

- Bone & Joint Health

- Gastrointestinal Health

- Immunity

- Cardiac Health

- Diabetes

- Anti-cancer

- Lungs Detox/Cleanse

- Others

By End-user

- Adults

- Geriatric

- Pregnant Women

- Children

- Infants

By Distribution Channel

- Offline

- Pharmacy

- Supermarket/Hypermarkets

- Others

- Online

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What are the key factors driving the growth of the North America Dietary Supplements Market?

Key factors driving the North America Dietary Supplements Market include increasing health consciousness, rising lifestyle diseases, and growing demand for sports nutrition. Additionally, advancements in supplement formulations and the preference for clean-label products contribute to market expansion.

What are the latest trends in the North America Dietary Supplements Market?

Key trends in the North America Dietary Supplements Market include personalized nutrition, clean-label and organic supplements, plant-based products, and CBD-infused supplements. Subscription-based services and AI-driven nutrition solutions are also gaining popularity.

What is the future outlook for the North America Dietary Supplements Market?

The North America Dietary Supplements Market is expected to grow steadily due to increasing demand for preventive healthcare and personalized supplements. AI-driven formulations and digital health integrations will further shape the industry's future.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]