North America Dental Equipment Market Research Report - Segmented By Product Type ( Dental Radiology Equipment,Systems and Parts) End User( Hospitals and Clinics,Dental Laboratories ) and Country (U.S., Canada & Rest of North America) - Industry Size, Share, Growth, Trends & Forecast (2025 to 2033)

North America Dental Equipment Market Size

The North America Dental Equipment Market was valued at USD 1.83 billion in 2024. The North America Dental Equipment Market is expected to have a 5.3 % CAGR from 2025 to 2033 and be worth USD 2.91 billion by 2033 from USD 1.93 billion in 2025.

The dental equipment is integral to the broader healthcare ecosystem, as it facilitates advancements in oral health management while addressing evolving patient needs and technological innovations. The region has witnessed significant growth due to increasing awareness of oral hygiene, rising incidences of dental disorders, and an aging population that demands specialized dental care. According to the Centers for Disease Control and Prevention, nearly half of all adults in the United States have some form of periodontal disease with an advanced dental equipment to manage these conditions effectively.

Technological progress has been pivotal in shaping this market, with innovations such as digital imaging systems, laser dentistry tools, and CAD/CAM technologies revolutionizing traditional practices. Additionally, the American Dental Association reports that approximately 75% of dentists in the U.S. now utilize digital radiography by reflecting a steady adoption curve for cutting-edge solutions. Another key factor driving demand is the growing preference for minimally invasive procedures among patients, which aligns with the capabilities offered by modern dental equipment.

Furthermore, socioeconomic trends play a role with data from the U.S. Census Bureau indicates that disposable income levels have risen steadily over the past decade, enabling more individuals to invest in elective dental treatments. These dynamics collectively contribute to a robust environment where dental equipment manufacturers can thrive by ensuring continued innovation and accessibility across North America's diverse healthcare landscape.

MARKET DRIVERS

Increasing Prevalence of Dental Disorders

The rising incidence of dental disorders in North America serves as a significant driver for the dental equipment market. According to the National Institute of Dental and Craniofacial Research, over 90% of adults in the United States have experienced dental caries at some point in their lives, while approximately 26% suffer from untreated tooth decay. These alarming figures amplifies the urgent need for advanced diagnostic and treatment tools to manage widespread oral health issues. According to the Centers for Disease Control and Prevention, oral cancers account for nearly 3% of all new cancer cases annually in the U.S., necessitating specialized equipment for early detection and intervention. The dental practitioners are investing in state-of-the-art devices such as intraoral cameras and 3D imaging systems to enhance patient outcomes, thereby fueling market growth.

Growing Geriatric Population and Associated Oral Health Needs

The expanding geriatric population in North America is another critical factor propelling the demand for dental equipment. The U.S. Census Bureau projects that by 2034, older adults will outnumber children for the first time in U.S. history, with individuals aged 65 and above comprising over 20% of the population. This demographic shift brings increased instances of age-related dental issues, such as tooth loss and periodontal diseases, which require specialized care. The National Center for Health Statistics reveals that nearly one in five adults aged 65 and older have lost all their teeth, driving the adoption of restorative dental technologies like implants and prosthetics. Accoridng to the Administration on Aging, elderly patients are more likely to seek regular dental check-ups by boosting the utilization of advanced equipment tailored to their unique needs.

MARKET RESTRAINTS

High Costs Associated with Advanced Dental Equipment

The substantial costs of cutting-edge dental equipment pose a significant restraint to the North America Dental Equipment Market. According to the Bureau of Labor Statistics, the average annual salary of a dentist in the U.S. is approximately $164,000, yet many practitioners face financial constraints when purchasing high-end tools such as CAD/CAM systems or 3D printers, which can cost upwards of $50,000. According to the National Health Expenditure Accounts, dental care spending constitutes about 4% of total healthcare expenditures by leaving limited room for additional investments in expensive technologies. Smaller clinics, particularly those in rural areas, often struggle to afford these innovations by leading to slower adoption rates. This financial barrier limits access to advanced care for certain populations and hinders the overall growth of the market, as manufacturers must balance innovation with affordability to cater to diverse practice sizes.

Limited Reimbursement Coverage for Advanced Dental Procedures

Inadequate reimbursement policies for advanced dental treatments further restrain the growth of the dental equipment market in North America. The Centers for Medicare & Medicaid Services states that dental services are generally excluded from Medicare coverage, except in rare cases like oral surgeries linked to other medical conditions. Similarly, Medicaid offers limited dental benefits, with only about 50% of adults eligible for any form of dental care under the program, as per the Kaiser Family Foundation. This lack of financial support discourages patients from opting for procedures requiring sophisticated equipment, such as laser treatments or digital imaging. Consequently, dental practices face reduced demand for advanced technologies, impacting their willingness to invest in new devices. The absence of comprehensive insurance coverage for innovative treatments creates a bottleneck in the widespread adoption of modern dental equipment across the region.

MARKET OPPORTUNITIES

Rising Adoption of Teledentistry and Digital Solutions

The growing integration of teledentistry and digital solutions presents a significant opportunity for the North America Dental Equipment Market. According to the Federal Communications Commission, over 93% of Americans have access to high-speed internet by enabling seamless adoption of virtual consultations and remote diagnostics. This trend has been further accelerated by the COVID-19 pandemic, with the Centers for Disease Control and Prevention emphasizing the role of telehealth in maintaining continuity of care. Accoridng to the American Teledentistry Association, teledentistry can reduce patient wait times by up to 25%, encouraging practices to invest in compatible equipment such as intraoral scanners and portable imaging devices. As more states adopt policies supporting telehealth reimbursement, the demand for equipment facilitating remote care is expected to surge. This shift not only enhances accessibility but also drives innovation in portable and user-friendly dental technologies.

Increasing Focus on Preventive Dental Care Initiatives

Government-led initiatives promoting preventive dental care create a favorable environment for market expansion. The U.S. Department of Health and Human Services reports that every dollar spent on preventive dental care saves approximately $50 in restorative and emergency treatments. Programs like the National Oral Health Surveillance System aim to improve oral health literacy, reaching millions of individuals annually. Additionally, the Centers for Disease Control and Prevention notes that community water fluoridation, one of the most cost-effective preventive measures, benefits nearly 200 million Americans. These efforts increase awareness about early diagnosis and regular check-ups by driving demand for diagnostic tools such as digital X-rays and caries detection devices. Both public health agencies and private practices are fostering a culture of proactive care by creating opportunities for manufacturers to develop affordable, efficient, and innovative dental equipment tailored to preventive needs.

MARKET CHALLENGES

Regulatory Hurdles and Compliance Requirements

The stringent regulatory standards for dental equipment pose a significant challenge to market growth in North America. The U.S. Food and Drug Administration mandates rigorous testing and approval processes for medical devices by including dental equipment, which can take an average of 3 to 7 years, as stated by the Government Accountability Office. These regulations ensure safety and efficacy but also increase development costs and delay product launches. Additionally, the Environmental Protection Agency enforces strict guidelines on the disposal of dental materials for those containing mercury or other hazardous substances that further complicates the operational workflows for practitioners. According to the Occupational Safety and Health Administration, non-compliance with these regulations can result in fines exceeding $13,000 per violation by creating financial and administrative burdens for manufacturers and clinics alike. Navigating this complex regulatory landscape remains a persistent challenge for the market key players.

Workforce Shortages in Dental Care Delivery

A growing shortage of dental professionals in North America threatens the effective utilization of advanced dental equipment. According to the Health Resources and Services Administration, over 60 million Americans live in areas designated as having a shortage of dental health professionals. Furthermore, the American Dental Association notes that nearly one-third of practicing dentists are aged 55 or older by signaling an impending wave of retirements that could exacerbate the workforce gap. This shortage limits the ability of clinics to maximize the potential of sophisticated tools like robotic-assisted systems or laser dentistry equipment, as proper training and expertise are essential for their operation. The Bureau of Labor Statistics projects that while employment in dental occupations will grow by 6% through 2031, this growth may not be sufficient to meet rising patient demand by hindering the widespread adoption of cutting-edge technologies in underserved regions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.3 % |

|

Segments Covered |

By Product Type , End-User and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

The U.S., Canada and Rest of North America |

|

Market Leader Profiled |

3M, Carestream Health Inc., Danaher Corporation, Dentsply Sirona, and GC Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

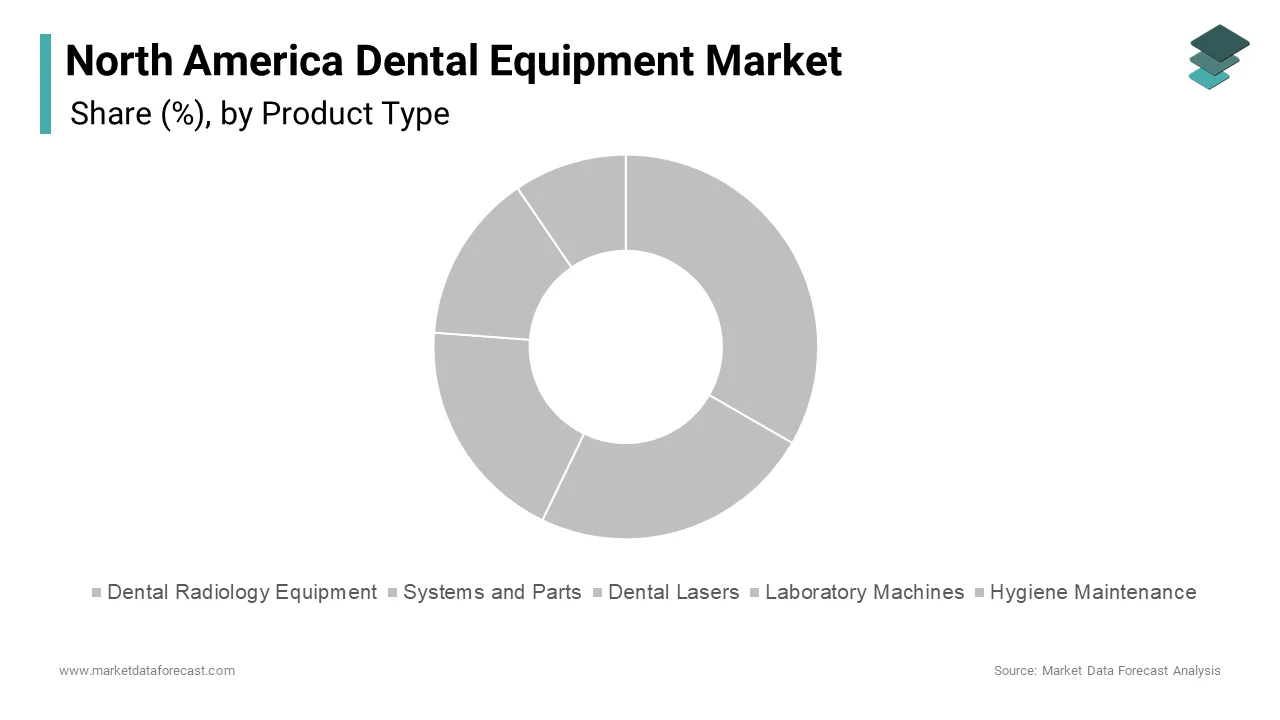

The dental radiology equipment segment was the largest in the North America dental equipment market and held a dominant share of 35.4% in 2024. This dominance is driven by its critical role in modern dental diagnostics and treatment planning. According to the Centers for Disease Control and Prevention, over 60% of adults in the U.S. visit the dentist annually, with diagnostic imaging being a cornerstone of these visits. Dental radiology equipment, including digital X-rays, panoramic systems, and cone beam computed tomography (CBCT), is indispensable for detecting cavities, periodontal diseases, oral cancers, and other dental abnormalities. According to the American Dental Association, nearly 75% of dental practices have transitioned to digital radiography, which reduces radiation exposure by up to 80% compared to traditional film-based methods. This shift not only enhances diagnostic accuracy but also aligns with growing patient demand for safer and more efficient care. The widespread adoption of dental radiology equipment escalates its importance in enabling early detection, precise treatment planning, and improved patient outcomes by making it a vital component of contemporary dental practices.

The dental lasers segment is likely to experience a significant CGAR of 11.5% during the forecast period. This growth is fueled by the increasing preference for minimally invasive procedures, which offer reduced pain, faster recovery times, and enhanced precision. The National Institute of Dental and Craniofacial Research emphasizes that patients are increasingly seeking advanced treatment options that minimize discomfort and improve overall experience. Dental lasers, approved by the Food and Drug Administration for applications such as gum disease treatment, cavity preparation, and soft tissue surgeries, exemplify this trend. According to the American Academy of Periodontology, laser treatments reduce bleeding and postoperative pain by enhancing patient comfort and satisfaction. Additionally, the rising awareness of cosmetic dentistry, coupled with higher disposable incomes, has further propelled the adoption of dental lasers. The Bureau of Labor Statistics reports that employment in dental occupations is projected to grow by 6% through 2031 by reflecting increased demand for advanced dental care. The dental lasers are emerging as a transformative force in the industry by driving innovation and expanding the scope of modern dentistry.

By End User Insights

The hospitals and clinics segment was the largest in the North America Dental Equipment Market by occupying a dominant share in 2024. This dominance is primarily due to their ability to offer a broad spectrum of dental services under one roof, ranging from routine check-ups to complex surgical procedures. These facilities are equipped with state-of-the-art technologies such as cone-beam computed tomography (CBCT) scanners, intraoral cameras, and laser dentistry tools, enabling comprehensive care. According to the Centers for Medicare & Medicaid Services, hospitals account for nearly 30% of all healthcare spending in the U.S. by reflecting their significant financial capacity to invest in advanced dental equipment. Furthermore, hospitals and clinics serve as primary access points for dental care, particularly for underserved populations by ensuring widespread utilization of these technologies.

The dental laboratories segment is swiftly emerging with a CAGR of 8.5% during the forecast period. This rapid expansion is driven by increasing demand for customized dental prosthetics, including crowns, bridges, veneers, and implants. The National Institute of Dental and Craniofacial Research reports that over 120 million Americans are missing at least one tooth, while 36 million are entirely edentulous that is fueling the need for laboratory-based restorative solutions. Technological advancements have further accelerated this growth, with innovations like Computer-Aided Design/Computer-Aided Manufacturing (CAD/CAM) systems enhancing precision and reducing production time. These systems enable dental labs to fabricate prosthetics with exceptional accuracy by meeting the rising patient expectations for aesthetic and functional outcomes. Additionally, the aging population, coupled with growing awareness of oral health, has created a surge in demand for high-quality, personalized dental solutions. Dental laboratories play an indispensable role in bridging the gap between dental practitioners and patients by ensuring timely delivery of tailored treatments that align with modern clinical standards.

Country Level Analysis

The United States Dental Equipment Market held the dominant share of 86.4% in 2024 owing to its vast population, advanced healthcare infrastructure, and high awareness of oral health. According to the Centers for Disease Control and Prevention, nearly 47% of adults in the U.S. suffer from some form of periodontal disease by creating a substantial demand for cutting-edge diagnostic and treatment tools. Additionally, the American Dental Association notes that there are over 200,000 actively practicing dentists in the country by ensuring widespread adoption of advanced equipment such as digital imaging systems, intraoral scanners, and laser dentistry tools. The presence of leading manufacturers and robust investments in R&D further cements the U.S.'s position as a global hub for dental innovation by making it a critical driver of growth in the region.

Canada dental Equipment Market is projected to register a CAGR of 7.2% during the forecast period. This rapid expansion is driven by increasing adoption of minimally invasive dental procedures, rising healthcare expenditures, and a growing aging population. According to the Canadian Institute for Health Information, oral health spending accounts for about 6% of total healthcare expenditures by reflecting a strong emphasis on advanced dental care. Furthermore, projections indicate that seniors will constitute 23% of Canada’s population by 2030 is driving demand for restorative solutions like implants and prosthetics. The integration of digital technologies, such as teledentistry and AI-driven diagnostics, is gaining momentum, supported by government initiatives to modernize healthcare infrastructure. These factors position Canada as a key player in fostering innovation and expanding access to advanced dental equipment across the region.

Top 3 Players in the market

3M

3M is a global leader in the North America Dental Equipment Market, renowned for its innovative solutions and extensive product portfolio. The company specializes in advanced dental technologies, including restorative materials, digital imaging systems, and infection prevention products. 3M’s contributions to the market are marked by its commitment to enhancing patient outcomes through cutting-edge research and development. Its proprietary technologies, such as nanotechnology-based composites and advanced adhesives, have set industry benchmarks for durability and aesthetics. Additionally, 3M’s focus on sustainability and eco-friendly solutions has positioned it as a preferred choice among dental practitioners.

Danaher Corporation

Danaher Corporation is another key player in the North America Dental Equipment Market, primarily through its subsidiary, KaVo Kerr, which is a cornerstone of its dental segment. Danaher’s influence stems from its comprehensive range of products, including imaging systems, treatment units, and consumables. The company is known for integrating advanced digital technologies into its offerings, such as intraoral scanners and CAD/CAM systems, enabling precise diagnostics and restorative care. Danaher’s strategic acquisitions and emphasis on operational excellence have allowed it to expand its footprint globally while maintaining a strong presence in North America.

Dentsply Sirona

Dentsply Sirona stands out as one of the most influential players in the North America Dental Equipment Market, often referred to as "The Dental Solutions Company." It offers an expansive portfolio that spans preventive, restorative, and diagnostic equipment, including digital imaging systems, treatment chairs, and endodontic tools. Dentsply Sirona’s contributions are escalating by its focus on digital dentistry, leveraging AI and automation to enhance precision and efficiency in dental procedures. The company’s commitment to education and training further strengthens its market position, as it actively supports dental professionals in adopting new technologies.

Top strategies used by the key market participants

Strategic Acquisitions and Collaborations

Key players in the North America Dental Equipment Market have consistently leveraged acquisitions and collaborations to expand their product portfolios and enhance market presence. For instance, companies like Danaher Corporation have acquired innovative firms to integrate cutting-edge technologies into their offerings, ensuring they remain at the forefront of industry advancements. Collaborations with research institutions and technology providers also enable these companies to co-develop solutions that address emerging dental care needs. Such strategic partnerships not only strengthen their competitive edge but also allow them to tap into new customer segments and geographies by fostering long-term growth.

Focus on Research and Development (R&D)

Investment in R&D is a cornerstone strategy for leading players such as 3M and Dentsply Sirona. These companies prioritize innovation by developing advanced materials, digital tools, and equipment that cater to evolving clinical demands. For example, the development of nanotechnology-based restorative materials and AI-driven diagnostic systems has redefined treatment precision and efficiency. By continuously pushing the boundaries of dental science, these organizations ensure their products remain relevant and superior in a highly competitive market.

Expansion of Digital Dentistry Solutions

The shift toward digital dentistry has prompted key players to focus on expanding their digital product lines. Companies are investing in technologies such as CAD/CAM systems, intraoral scanners, and teledentistry platforms to meet the growing demand for minimally invasive and patient-centric solutions. By offering integrated digital workflows, these players streamline clinical processes, improve accuracy, and reduce treatment times. This emphasis on digital transformation aligns with the broader trend of modernizing dental practices, enabling companies to capture a larger share of the market while addressing the needs of tech-savvy practitioners.

Emphasis on Training and Education

Leading companies recognize the importance of educating dental professionals about the benefits and applications of advanced equipment. To this end, they offer extensive training programs, workshops, and online resources to familiarize practitioners with new technologies. For example, Dentsply Sirona has established dedicated training centers to support the adoption of its digital solutions.

Sustainability and Eco-Friendly Initiatives

In response to growing environmental concerns, major players are incorporating sustainability into their strategies. Companies like 3M are developing eco-friendly products, such as biodegradable materials and energy-efficient equipment, to align with global sustainability goals. By prioritizing environmentally responsible practices, these organizations appeal to environmentally conscious consumers and regulatory bodies, enhancing their brand image and market positioning. This forward-thinking approach ensures compliance with evolving regulations while meeting the expectations of modern stakeholders.

Geographic Expansion and Market Penetration

To strengthen their foothold in North America, key players are focusing on geographic expansion and deeper market penetration. They are targeting underserved regions by establishing distribution networks, service centers, and partnerships with local clinics and hospitals. This strategy not only broadens their reach but also ensures timely delivery of products and services, fostering trust and reliability among customers.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

The North American dental equipment market is somewhat competitive, with players like 3M, Carestream Health Inc., Danaher Corporation, Dentsply Sirona, and GC Corporation are the major shareholders. The intense competition poses a severe threat to small businesses in this region.

The North America Dental Equipment Market is characterized by intense competition, driven by the presence of established global players and innovative startups vying for market share. Key companies such as Dentsply Sirona, Danaher Corporation, and 3M dominate the landscape, leveraging their extensive product portfolios, advanced technologies, and strong distribution networks to maintain its dominance. These industry giants consistently invest in research and development to introduce cutting-edge solutions like digital imaging systems, CAD/CAM technologies, and AI-driven diagnostic tools by ensuring they stay ahead of evolving clinical demands.

In addition to these leaders, smaller firms and regional players contribute to the competitive dynamics by offering niche products tailored to specific customer needs. This has led to a fragmented yet dynamic market where innovation is a key differentiator. Strategic initiatives such as mergers, acquisitions, and collaborations are frequently employed to expand technological capabilities and geographic reach. For instance, partnerships with dental laboratories and educational institutions help companies enhance adoption rates and build brand loyalty.

The competitive environment is further intensified by the growing emphasis on digital dentistry, which has prompted companies to adopt aggressive marketing strategies and focus on customer education. Additionally, regulatory compliance and sustainability efforts play a crucial role in shaping competition, as companies strive to align with healthcare standards and environmental goals. Overall, the interplay of innovation, strategic expansion, and customer-centric approaches defines the highly competitive yet collaborative nature of the North America Dental Equipment Market by fostering continuous advancements in dental care delivery.

RECENT HAPPENINGS IN THE MARKET

- In July 2023, 3M announced its decision to spin off its healthcare division, including its dental segment, to form a separate company by the end of the year. This move was intended to enhance the focus on healthcare innovations and streamline operations.

- In July 2023, Carestream Dental established a partnership with ArchformByte, allowing dental professionals utilizing the CS 3500 and CS 3600 intraoral scanners to transmit precise images for the fabrication of C-Thru aligners. This collaboration aimed to enhance Carestream's digital dentistry solutions in North America.

- In August 2023, 3M completed the sale of certain dental local anesthetic assets to Pierrel S.p.A. for $70 million. This transaction was part of 3M’s strategy to optimize its dental product offerings and focus on key growth areas.

- In December 2023, Young Innovations acquired Salvin Dental Specialties, a company known for its expertise in surgical dental equipment for implantology. This acquisition aimed to enhance Young Innovations’ presence in the North American dental equipment market.

- In January 2024, Align Technology Inc. introduced the iTero Lumina intraoral scanner, featuring an expanded capture field and a more compact, lightweight design. This innovation aimed to improve scanning speed and accuracy for dental professionals across North America.

- In February 2024, Dentsply Sirona broadened its partnership with A-dec by integrating advanced scanning technology into A-dec’s dental delivery systems. This expansion was designed to enhance digital workflows for dental practitioners.

- In April 2024, Medit launched the i900 intraoral scanner, incorporating touchpad and touch band functionality. This advanced system was developed to provide North American dental professionals with more efficient and user-friendly scanning capabilities.

- In July 2024, Danaher introduced two new laboratories certified by the Clinical Laboratory Improvement Amendments (CLIA) and the College of American Pathologists (CAP) to accelerate the development of precision diagnostic tools, reinforcing its presence in the North American market.

- In September 2024, RPA Dental unveiled an online store, providing dental professionals with easy access to spare parts, accessories, and essential dental equipment. This initiative aimed to improve service availability and customer convenience.

- In September 2024, NSK acquired DCI International, a manufacturer of dental components and equipment. This acquisition was intended to combine the expertise of both companies and strengthen their presence in the North American dental equipment sector.

MARKET SEGMENTATION

This research report on the America Dental Equipment Market has been segmented and sub-segmented into the following categories.

By Product Type

- Dental Radiology Equipment

- Intraoral

- Digital sensors

- Digital X-Ray units

- Extraoral

- Analog

- Digital

- Intraoral

- Systems and Parts

- Cast Machine

- Instrument Delivery Systems

- Vacuums & Compressors

- Cone Beam CT Systems

- Furnace and Ovens

- CAD/CAM

- Electrosurgical Equipment

- Dental Lasers

- Diode Lasers

- Vertical Cavity Surface Emitting Lasers

- Quantum Well Lasers

- Vertical External Cavity Surface Emitting Lasers

- Heterostructure Lasers

- Distributed Feedback Lasers

- Quantum Cascade Lasers

- Separate Confinement Heterostructure Lasers

- Carbon dioxide Lasers

- Diode Lasers

- Laboratory Machines

- Micro Motor

- Ceramic Furnaces

- Electronic Waxer

- Hydraulic Press

- Suction Unit

- Hygiene Maintenance

- Air Purification & Filters

- Hypodermic Needle Incinerator

- Sterilizers

By End User

- Hospitals and Clinics

- Dental Laboratories

- Others

By Country

- The U.S.

- Canada

- Rest of North America.

Frequently Asked Questions

What are the major types of dental equipment?

Diagnostic, therapeutic, hygiene maintenance, and laboratory equipment.

How does the aging population affect the market?

Growing elderly populations increase demand for restorative and prosthetic dentistry.

What is the North America Dental Equipment Market?

It refers to the industry producing tools and devices used in dental care across North America.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]