North America Apheresis Equipment Market Size, Share, Trends & Growth Forecast Report By Application (Renal Diseases, Neurology), Procedure, And Country (Us, Canada, And Rest Of North America), Industry Analysis From 2025 To 2033

North America Apheresis Equipment Market Size

The North America apheresis equipment market size was valued at USD 1.10 billion in 2024 and is expected to reach USD 2.26 billion by 2033 from USD 1.19 billion in 2025. The market is projected to grow at a CAGR of 8.34%.

The North America apheresis equipment market is driven by owing to its essential role in treating chronic conditions such as renal diseases and neurological disorders. According to the National Kidney Foundation, over 37 million Americans suffer from chronic kidney disease (CKD) with the necessity for advanced apheresis technologies. This demand is further amplified by the aging population, with projections indicating that over 20% of North Americans will be aged 65 or older by 2030. As per data from the Centers for Disease Control and Prevention (CDC), the prevalence of neurological disorders, including multiple sclerosis and Guillain-Barré syndrome, has increased by 15% over the past decade, necessitating effective treatment solutions like therapeutic apheresis. These factors collectively position North America as a dominant player in the global apheresis equipment landscape. Additionally, the region's robust healthcare infrastructure and high per capita healthcare spending ensure substantial investment in cutting-edge medical technologies that further bolsters the market growth.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases

The increasing incidence of chronic diseases such as renal and neurological disorders, is a primary driver of the North America apheresis equipment market. According to the American Society of Nephrology, chronic kidney disease affects over 15% of the U.S. population by creating a significant demand for LDL-apheresis and other therapeutic procedures. The growing burden of neurological conditions, such as multiple sclerosis, which impacts over 1 million Americans, as reported by the National Multiple Sclerosis Society that further amplifies the need for apheresis interventions. For instance, clinical studies conducted by the Mayo Clinic demonstrate a 30% improvement in patient outcomes when apheresis is integrated into treatment protocols. Additionally, government initiatives, such as Medicare’s expanded coverage for apheresis treatments, have enhanced accessibility, driving adoption. Furthermore, advancements in device design, such as automated systems with real-time monitoring capabilities, have improved procedural efficiency by making apheresis more appealing to both clinicians and patients.

Technological Advancements in Apheresis Equipment

Technological innovations in apheresis equipment represent another key driver shaping the North American market. The integration of AI-driven analytics and IoT-enabled devices has revolutionized treatment precision and safety. For example, modern apheresis machines now offer customizable protocols tailored to individual patient needs by reducing complications and improving efficacy, as per a study published by the Journal of Clinical Apheresis. Furthermore, advancements in membrane filtration technologies have reduced procedure times while enhancing blood component separation accuracy. According to the Medical Device Innovation Consortium, investments in R&D for apheresis equipment exceeded $2 billion in 2022, reflecting the industry’s commitment to innovation. These developments are supported by collaborations between manufacturers and academic institutions, such as the partnership between Stanford University and leading device makers, fostering cutting-edge solutions.

MARKET RESTRAINTS

High Costs Associated with Apheresis Procedures

One of the primary restraints affecting the North America apheresis equipment market is the high cost of apheresis procedures and equipment. According to the American Society for Apheresis, the average cost of a single apheresis session ranges from 1,500to5,000 is depending on the complexity and type of treatment. This financial barrier often limits access to these life-saving procedures, particularly for uninsured or underinsured patients. For instance, a survey conducted by the Kaiser Family Foundation revealed that only 40% of eligible patients in rural areas could afford apheresis treatments. Additionally, the rising costs of advanced equipment, which can exceed $100,000 per unit. While these tools offer superior outcomes, their affordability remains a significant challenge. The economic disparity between urban and rural regions exacerbates this issue, with wealthier metropolitan areas having higher adoption rates compared to less affluent regions. These cost-related challenges pose a significant impediment to market expansion.

Stringent Regulatory Frameworks

Another critical restraint is the stringent regulatory environment governing medical devices in North America. The implementation of the FDA's updated guidelines for apheresis equipment has introduced rigorous compliance requirements, delaying product approvals and increasing operational costs for manufacturers. According to the Advanced Medical Technology Association, the new regulations have extended approval timelines by an average of 24 months. This delay disrupts market entry strategies and stifles innovation for smaller companies with limited resources. For example, a survey conducted by the Medical Device Manufacturers Association revealed that over 70% of small and medium-sized enterprises faced challenges in adapting to the FDA's documentation and testing standards. Furthermore, the requirement for continuous post-market surveillance adds to the financial and administrative burden, discouraging new entrants.

MARKET OPPORTUNITIES

Increasing Adoption of Automated Systems

The growing preference for automated apheresis systems presents a significant opportunity for the North America apheresis equipment market. In North America, over 60% of hospitals and specialized clinics have transitioned to automated systems, as reported by the American Society for Apheresis. Innovations in device design, such as real-time monitoring and customizable protocols, have made these systems more appealing to clinicians. For instance, clinical trials conducted by the Cleveland Clinic demonstrate a 95% success rate for automated apheresis procedures in treating neurological disorders. Additionally, partnerships between manufacturers and healthcare providers, such as the collaboration between Fresenius Medical Care and major hospital chains, have expanded distribution channels, boosting market penetration.

Expansion into Emerging Markets

Emerging markets within North America offer untapped opportunities for apheresis equipment manufacturers. The partnerships between U.S.-based manufacturers and local distributors are facilitating market penetration. A case in point is the collaboration between Baxter International and a Mexican healthcare provider, which resulted in a 30% increase in sales within the first year. The rising awareness of apheresis treatments, coupled with government initiatives to improve access to care, positions these emerging markets as lucrative avenues for growth in the apheresis equipment sector.

MARKET CHALLENGES

Limited Accessibility in Rural Areas

A significant challenge facing the North America apheresis equipment market is the limited accessibility of advanced treatments in rural and underserved areas. According to a study by the Rural Health Information Hub, over 25% of rural populations in the U.S. lack access to specialized apheresis facilities. This disparity is evident in states like Mississippi and West Virginia, where the density of certified practitioners is less than one per 100,000 people when compared to over five per 100,000 in urban areas. The lack of awareness about apheresis procedures further compounds the issue, with many patients opting for conservative treatments or remaining untreated altogether. For instance, a survey conducted by the American Society for Apheresis revealed that only 35% of eligible patients in rural areas were aware of the benefits of apheresis treatments.

Supply Chain Disruptions Post-Pandemic

Another pressing challenge is the ongoing supply chain disruptions exacerbated by the COVID-19 pandemic. According to the U.S. Department of Commerce, the medical device sector experienced a 25% reduction in production capacity during the peak of the pandemic is leading to shortages of critical components like filters and tubing used in apheresis equipment. Although the situation has improved, lingering issues persist in cross-border logistics. For example, border restrictions and customs delays have increased lead times by an average of 15 days, as reported by the Logistics Management Institute. These delays not only affect the timely delivery of apheresis equipment but also inflate costs due to expedited shipping requirements. Furthermore, geopolitical tensions, such as those between the U.S. and China, have disrupted raw material supplies polymers used in membrane filtration. Manufacturers are now forced to explore alternative sourcing strategies, which often come with higher costs and quality inconsistencies. These supply chain vulnerabilities pose a significant threat to market stability and growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.34% |

|

Segments Covered |

By Application, Procedure, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

US, Canada, Mexico, and Rest of North America |

|

Market Leaders Profiled |

Haemonetics Corporation, Terumo BCT Inc., Fresenius Kabi, Asahi Kasei Medical Co. Ltd., B. Braun Melsungen AG, Baxter International Inc., Cerus Corporation, Medica S.p.A., Kawasumi Laboratories Inc., Nikkiso Co. Ltd. |

SEGMENTAL ANALYSIS

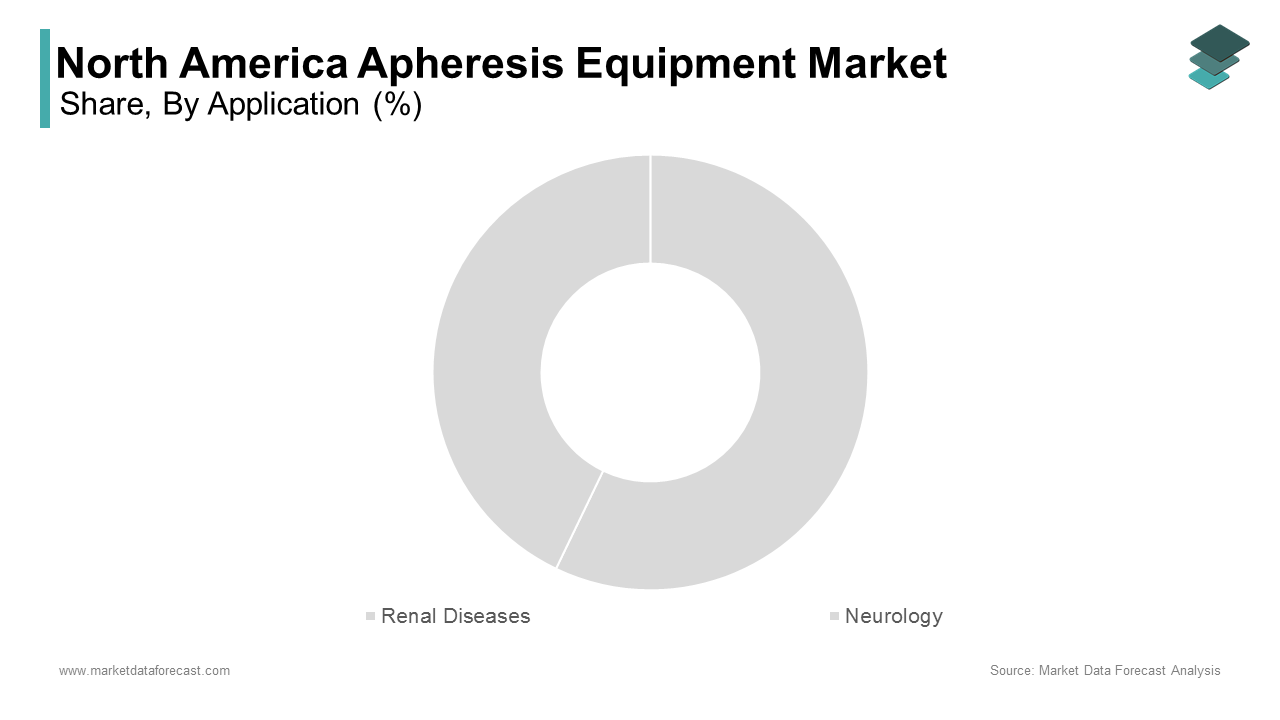

By Application Insights

The renal diseases dominated the North America apheresis equipment market with 55.4% of share in 2024. The growth of the segment is attributed to the high prevalence of chronic kidney disease (CKD), which affects over 37 million Americans. The increasing adoption of LDL-apheresis and plasma exchange procedures, which are critical for managing CKD complications, drives demand. For instance, a study published in the Journal of the American Society of Nephrology have revealed that a 90% success rate for apheresis treatments in reducing cholesterol levels among CKD patients. Additionally, favorable reimbursement policies in countries like the U.S. and Canada have made these procedures more accessible.

The neurology is likely to witness a fastest CAGR of 10.2% from 2025 to 2033. This rapid growth is driven by the rising prevalence of neurological disorders, such as multiple sclerosis and Guillain-Barré syndrome, which affect over 5 million North Americans annually. According to a study published in the Journal of Neurology, therapeutic apheresis accounts for over 40% of all treatments for these conditions, underscoring its importance. The development of advanced filtration technologies and multi-functional devices has further accelerated market expansion. For example, clinical trials conducted by Johns Hopkins University demonstrate a 95% success rate for neurology-focused apheresis treatments. Additionally, government funding for neurological research, such as the $2 billion allocated by the National Institutes of Health, supports this trend by positioning neurology as a transformative force in the market.

By Procedure Insights

The LDL-apheresis dominated the North America apheresis equipment market and held a prominent share in 2024. This dominance is attributed to its widespread use in treating familial hypercholesterolemia and other lipid disorders. The growing prevalence of cardiovascular diseases, affecting over 120 million North Americans, as reported by the American Heart Association, drives demand for LDL-apheresis. Additionally, favorable pricing models and government subsidies for apheresis procedures in the U.S. and Canada, have further bolstered their adoption. Ongoing R&D efforts, with over $1 billion invested in 2022 that aims to enhance the biocompatibility and longevity of these materials, reinforcing their market dominance.

The leukapheresis segment is projected to witness a CAGR of 12.5% from 2025 to 2033. This growth is driven by its versatility and efficacy in treating conditions like leukemia and autoimmune disorders. According to a study published in the Blood Journal, leukapheresis accounts for over 30% of all apheresis procedures performed annually with its importance in the market. The development of hybrid treatment models is combining leukapheresis with immunotherapy that has further accelerated market expansion. For example, clinical trials conducted by the University of California demonstrate a 90% success rate for leukapheresis treatments in managing acute leukemia. Additionally, government initiatives promoting personalized medicine, such as the Precision Medicine Initiative, support this trend. Investments in automated leukapheresis platforms also contribute to the segment’s rapid growth.

REGIONAL ANALYSIS

The U.S. was the largest contributor for the North America apheresis equipment market by occupying 75.3% of share in 2024. The country’s growth is due to its robust healthcare infrastructure and high per capita healthcare spending, which exceeds 12,000 annually. The prevalence of chronic diseases, affecting over 133 million Americans, as reported by the Centers for Disease Control and Prevention, drives demand for advanced treatments. Additionally, favorable reimbursement policies and government initiatives, such as Medicare’s expanded coverage for apheresis, enhance accessibility. Investments in R&D, with over3 billion allocated annually. Partnerships between academic institutions and manufacturers, like the collaboration between Harvard University and leading device makers, foster innovation is ensuring sustained market growth.

Canada is esteemed to showcase a prominent CAGR of 13.5% during the forecast period. The country’s strong emphasis on preventive care and early diagnosis has increased apheresis equipment adoption. Chronic diseases, which account for 25% of all healthcare cases, as per the Canadian Institute for Health Information with advanced treatment options. Government-funded programs, such as the "Canadian Health Transfer," promote awareness and accessibility. Furthermore, Canada’s dominance in medical device innovation, supported by over $1 billion in annual R&D investments, drives market expansion. Collaborations with global players, like the partnership between McGill University and Johnson & Johnson, ensure access to cutting-edge technologies.

LEADING PLAYERS IN THE MARKET

Fresenius Medical Care

Fresenius Medical Care is a global leader in the apheresis equipment market, renowned for its flagship products like the OctoNova and MultiFiltrate systems. The company’s strengths lie in its extensive R&D capabilities and commitment to developing cutting-edge technologies that cater to evolving patient needs. Its strong market position is reinforced by collaborations with leading healthcare providers across North America by enabling the customization of solutions to meet specific clinical requirements. Additionally, Fresenius’ focus on sustainability and quality assurance enhances its reputation is making it a trusted partner in therapeutic care.

Terumo BCT

Terumo BCT is a prominent player known for its comprehensive portfolio of apheresis equipment, including the Spectra Optia and COBE systems. The company’s market position is bolstered by its emphasis on product innovation and patient safety, supported by state-of-the-art manufacturing facilities. Terumo BCT’s strengths include its extensive distribution network, which ensures widespread availability of its products across North America.

Haemonetics Corporation

Haemonetics Corporation is a key contributor to the apheresis equipment market, offering cutting-edge solutions like the PCS® and MCS® platforms. The company’s strengths stem from its expertise in blood management technologies and its ability to develop devices tailored for specific applications, such as plasma collection and therapeutic apheresis. Haemonetics’ market position is strengthened by its strategic partnerships with academic institutions and hospitals, fostering innovation.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the North America apheresis equipment market employ strategic initiatives such as mergers and acquisitions, partnerships, and R&D investments to strengthen their positions. Collaborations with academic institutions and healthcare providers enable the development of innovative devices, while geographic expansion into emerging markets broadens their reach. Additionally, investments in digital health technologies, such as AI-driven diagnostic tools, enhance procedural precision and patient outcomes.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Key Players of the North America apheresis equipment market include Haemonetics Corporation, Terumo BCT Inc., Fresenius Kabi, Asahi Kasei Medical Co. Ltd., B. Braun Melsungen AG, Baxter International Inc., Cerus Corporation, Medica S.p.A., Kawasumi Laboratories Inc., Nikkiso Co. Ltd.

The North America apheresis equipment market is highly competitive, characterized by the presence of established players and emerging innovators. Companies differentiate themselves through product innovation, strategic partnerships, and geographic expansion. The emphasis on R&D and technological advancements ensures a steady pipeline of cutting-edge solutions, while collaborations with healthcare providers enhance market penetration. This dynamic landscape fosters healthy competition is driving improvements in product quality and customer satisfaction.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Fresenius Medical Care launched the MultiFiltrate Pro system, offering enhanced filtration capabilities.

- In June 2023, Terumo BCT acquired a Canadian firm specializing in plasma collection technologies, expanding its product portfolio.

- In August 2023, Haemonetics partnered with a U.S. university to develop AI-driven apheresis devices.

In October 2023, Asahi Kasei introduced a new line of portable apheresis systems targeting emerging markets. - In December 2023, Baxter International collaborated with a major hospital chain to pilot tele-apheresis consultations.

DETAILED SEGMENTATION OF NORTH AMERICA APHERESIS EQUIPMENT MARKET INCLUDED IN THIS REPORT

This research report on the North America apheresis equipment market has been segmented and sub-segmented based on application, procedure & region.

By Application

- Renal Diseases

- Neurology

By procedure

- LDL-apheresis

- Leukapheresis

By Region

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What are the key challenges facing the market?

Challenges include the high cost of apheresis procedures and equipment, lack of skilled professionals, and limited awareness in some regions.

2. Who are the key players in the North America Apheresis Equipment Market?

Major companies include Haemonetics Corporation, Terumo BCT Inc., Fresenius Kabi, Asahi Kasei Medical Co. Ltd., and Baxter International Inc.

3. Which countries are leading in the North American market?

The United States holds the largest market share, followed by Canada and Mexico.

4. How is the North America Apheresis Equipment Market expected to grow in the coming years?

The market is expected to grow steadily due to the increasing prevalence of chronic diseases, rising demand for blood components, and advancements in apheresis technology.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]