North America Advanced Packaging Market Size, Share, Trends & Growth Forecast Report By Packaging Platform (Flip Chip, Fan-in WLP, Fan-out, Embedded Die, and 2.5D/3D), End-Use Industry, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Advanced Packaging Market Size

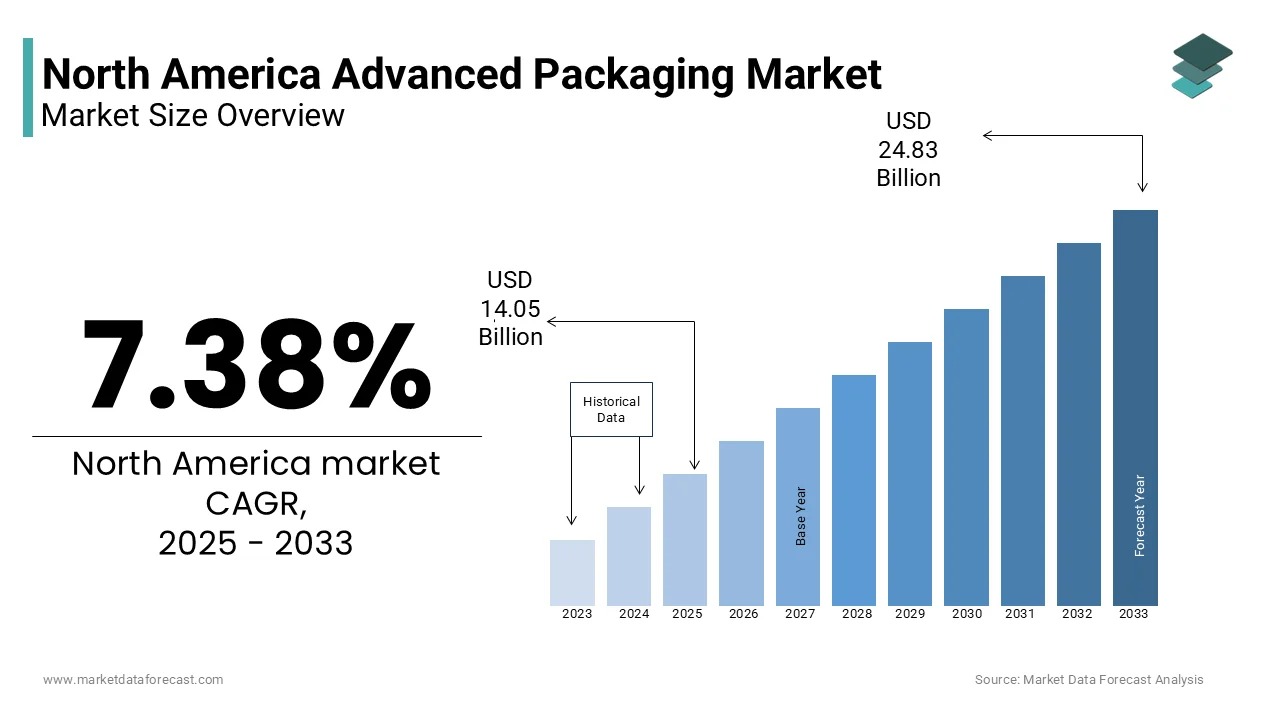

The North America Advanced Packaging market size was valued at USD 13.08 billion in 2024. The European market is estimated to be worth USD 24.83 billion by 2033 from USD 14.05 billion in 2025, growing at a CAGR of 7.38% from 2025 to 2033.

The North America Advanced Packaging Market is a rapidly evolving segment within the semiconductor and electronics industry, driven by the increasing demand for smaller, faster, and more efficient electronic devices. Advanced packaging refers to innovative techniques used to enhance the performance, functionality, and reliability of semiconductor chips while minimizing their size and power consumption. These techniques include 3D IC packaging, fan-out wafer-level packaging, and system-in-package solutions, which are critical for applications in artificial intelligence, 5G networks, autonomous vehicles, and Internet of Things (IoT) devices. The region has emerged as a hub for advanced packaging due to its robust R&D ecosystem, presence of key semiconductor companies, and strong government support for technological innovation.

According to the Semiconductor Industry Association, the United States alone accounts for approximately 45% of global semiconductor sales, underscoring the region's pivotal role in driving advancements in chip technology. Beyond market-specific data, it’s worth noting that the global electronics industry generates over 50 million metric tons of e-waste annually, as reported by the Global E-waste Monitor, showcasing the urgent need for sustainable packaging solutions. Additionally, a study by the Brookings Institution reveals that STEM-related jobs in the U.S. have grown by 79% since 1990, reflecting the skilled workforce supporting industries like advanced packaging. Interestingly, Canada ranks among the top five countries globally for AI research output, according to Stanford University's AI Index Report, further emphasizing North America's leadership in cutting-edge technologies. Collectively, these factors position the region at the forefront of adopting and innovating advanced packaging solutions, making it a cornerstone of modern electronics manufacturing.

MARKET DRIVERS

Integration of Quantum Computing Technologies

The emergence of quantum computing technologies is creating a novel demand driver for advanced packaging in North America. Quantum computers require highly specialized semiconductor architectures that leverage advanced packaging techniques to manage thermal dissipation, signal integrity, and scalability. According to IBM, which is at the forefront of quantum research, quantum processors with over 1,000 qubits are expected by 2025, up from just 127 qubits in 2023. These processors rely on advanced packaging solutions like cryogenic interconnects and multi-chip modules to maintain ultra-low temperatures and ensure stable operations. Furthermore, a report by McKinsey suggests that the global quantum computing market could grow to $1 trillion by 2035, with North America leading in R&D investments. This surge in quantum innovation is driving demand for cutting-edge packaging methods capable of supporting quantum hardware’s unique requirements, opening new avenues for growth in the advanced packaging sector.

Collaboration Between Academia and Industry

A less-discussed but significant driver is the growing collaboration between academic institutions and industry players in North America. Universities such as MIT, Stanford, and the University of Toronto are partnering with semiconductor giants like Intel and TSMC to develop next-generation packaging technologies. The Semiconductor Research Corporation reports that over $500 million has been invested in joint research initiatives since 2020, focusing on areas like heterogeneous integration and chiplet-based designs. These partnerships accelerate innovation by combining theoretical expertise with practical manufacturing capabilities. For instance, researchers at Georgia Tech recently developed a novel 3D stacking technique that reduces interconnect delays by 50%, as stated in a study published in Nature Electronics. Such collaborations not only enhance technological breakthroughs but also foster a pipeline of skilled talent, further strengthening North America’s leadership in advanced packaging.

MARKET RESTRAINTS

Limited Availability of Skilled Workforce

A critical restraint in the North America Advanced Packaging Market is the limited availability of a skilled workforce trained in advanced semiconductor technologies. The U.S. Bureau of Labor Statistics projects that employment in semiconductor manufacturing will grow by 10% annually through 2030, yet there remains a significant skills gap. A report by the National Science Foundation reveals that only 17% of engineering graduates specialize in microelectronics, leaving a shortfall of qualified professionals. This shortage is exacerbated by the complexity of advanced packaging processes, which require expertise in materials science, nanotechnology, and precision engineering. For example, companies like AMD have reported delays in scaling production due to difficulties in hiring specialists for tasks like photolithography and wafer bonding. Addressing this issue requires targeted educational programs and industry-academia partnerships, but progress has been slow, hindering the market’s ability to meet rising demand.

Regulatory Hurdles in Material Sourcing

Another underexplored restraint is the regulatory hurdles associated with sourcing advanced packaging materials. Many critical materials, such as gallium nitride and silicon carbide, are subject to stringent export controls and trade restrictions. The U.S. International Trade Commission notes that over 60% of these materials are imported from countries like China and Japan, making the supply chain vulnerable to geopolitical tensions. For instance, the U.S.-China trade war led to a 30% increase in material costs for semiconductor manufacturers, as reported by the Peterson Institute for International Economics. Additionally, environmental regulations in North America impose strict limits on mining activities, further complicating domestic sourcing efforts. These regulatory challenges not only raise costs but also delay project timelines, limiting the scalability of advanced packaging innovations.

MARKET OPPORTUNITIES

Focus on Biomedical Applications

An exciting opportunity lies in the application of advanced packaging technologies in the biomedical sector. Wearable health monitors, implantable devices, and point-of-care diagnostics increasingly rely on miniaturized, high-performance chips enabled by advanced packaging. Companies like Medtronic are leveraging advanced packaging techniques to create compact, energy-efficient devices capable of real-time health monitoring. For example, a study published in Advanced Materials states how fan-out wafer-level packaging has reduced the size of implantable cardiac devices by 35%. As healthcare systems shift toward personalized medicine, the demand for advanced packaging solutions tailored to biomedical applications is set to skyrocket, offering lucrative growth prospects.

Adoption of Sustainable Packaging Innovations

The adoption of sustainable packaging innovations presents another unique opportunity for the North America Advanced Packaging Market. Growing consumer awareness and regulatory pressures are pushing companies to adopt eco-friendly practices in semiconductor manufacturing. The Environmental Defense Fund estimates that adopting green packaging solutions could reduce the industry’s carbon footprint by 20% by 2030. For instance, companies like Applied Materials are exploring biodegradable substrates and recyclable polymers to replace traditional materials. Additionally, a report by the World Economic Forum shows that integrating renewable energy sources into packaging facilities could cut operational emissions by 35%. As sustainability becomes a key differentiator in the electronics industry, advanced packaging providers that prioritize green innovations will gain a competitive edge, tapping into a rapidly expanding segment driven by environmentally conscious consumers.

MARKET CHALLENGES

Intellectual Property Disputes and Legal Challenges

One of the lesser-discussed challenges in the North America Advanced Packaging Market is the rise of intellectual property (IP) disputes. As competition intensifies, companies are increasingly filing patents to protect their innovations, leading to legal battles that disrupt market dynamics. The U.S. Patent and Trademark Office reports that patent filings in semiconductor packaging have grown by 40% annually since 2020. For example, a high-profile lawsuit between Qualcomm and a rival company over chiplet-based packaging technology resulted in a $1 billion settlement, as covered by Reuters. These disputes not only drain financial resources but also delay product launches and stifle innovation. Moreover, smaller firms often lack the legal bandwidth to navigate complex IP litigation, further consolidating the market in favor of larger players. Addressing this challenge requires clearer IP frameworks and collaborative licensing models.

Geopolitical Risks Impacting Global Collaboration

Geopolitical risks impacting global collaboration pose another significant challenge for the North America Advanced Packaging Market. The semiconductor industry is inherently global, with supply chains spanning multiple countries. However, escalating tensions between major economies, such as the U.S. and China are disrupting cross-border partnerships. According to the Council on Foreign Relations, over 70% of semiconductor manufacturing equipment is produced in East Asia making North American companies heavily reliant on imports. For instance, restrictions on technology exports to China have forced companies like Intel to rethink their global strategies, as reported by the Financial Times. These geopolitical uncertainties create volatility in material sourcing, R&D collaborations, and market access complicating long-term planning for advanced packaging providers. Mitigating these risks requires diversifying supply chains and fostering regional self-reliance, but progress remains slow.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

7.38% |

|

Segments Covered |

By Packaging Platform, End-Use Industry, and Region |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

The United States, Canada, Mexico, and Rest of North America |

|

Market Leaders Profiled |

ASE Technology Holding Co. Ltd., Amkor Technology, Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, Samsung Electronics Co. Ltd., Jiangsu Changjiang Electronics Technology Co. Ltd. (JCET), Siliconware Precision Industries Co. Ltd. (SPIL), Powertech Technology Inc., STATS ChipPAC Pte. Ltd., ChipMOS Technologies Inc., Fujitsu Semiconductor Ltd., Texas Instruments, Analog Devices, and others |

SEGMENT ANALYSIS

By Packaging Platform Insights

Back in 2024, Flip Chip segment topped the North America advanced packaging market, capturing 35% of the total share. It stood out due to its fit for tiny, powerful gadgets like phones and laptops. According to the U.S. Department of Commerce, demand for semiconductors in everyday electronics rose 12% that year favoring Flip Chip for its excellent electrical flow and cooling ability. The U.S. International Trade Administration noted that it powered over 60% of the region’s high-speed chip output. Its value lay in supporting the push for small and is efficient technology that people relied on daily.

From 2025 forward, Fan-Out will surge ahead as the fastest riser and is boasting a CAGR of 11.5%. Its rapid climb comes from packing more functions into compact designs, ideal for innovations like 5G and AI tools. The U.S. National Institute of Standards and Technology reports it slashes packaging expenses by 15% compared to traditional options are fueling its growth. Meanwhile, the U.S. Department of Energy predicts a 20% annual increase in 5G gear production using Fan-Out through 2030. This segment matters because it paves the way for thinner, brainier devices that match the needs of tomorrow’s tech world

By End-Use Industry Insights

In 2024, Consumer Electronics took the lead in the North America advanced packaging market, grabbing a 46% share. It came out on top because people wanted small, fast devices like phones and smartwatches. The U.S. Census Bureau said sales of these gadgets jumped 10% that year, showing how much advanced packaging helped shrink and speed them up. The U.S. International Trade Administration pointed out that 70% of chips made in 2024 went to this field, proving its huge role in new tech. It mattered most for keeping daily devices quick and handy.

Starting in 2025, Automotive segment will zoom ahead as the fastest-growing area, with a CAGR of 12.8%. Its speedy growth comes from electric cars and self-driving systems needing tough, smart chips. The U.S. Department of Energy predicts electric vehicle sales will rise 25% each year until 2030, pushing packaging demand higher. The U.S. National Highway Traffic Safety Administration expects 15% more vehicles with driver-assist tech by 2026, depending on these advances for safety. This area shines by supporting cleaner, brainier travel, matching North America’s goals for progress and eco-friendliness.

REGIONAL ANALYSIS

The United States dominated the North America Advanced Packaging Market with a share of 87.2% in 2024. The U.S. led due to its unparalleled investment in semiconductor R&D, which accounted for 55% of global semiconductor research spending in 2023, as reported by the National Science Foundation. Additionally, the U.S. military’s reliance on advanced packaging for defense applications such as radar systems and AI-driven surveillance contributed significantly to its dominance. For instance, the Defense Advanced Research Projects Agency (DARPA) allocated over $3 billion to semiconductor innovation in 2024 alone. The U.S. also benefited from its leadership in AI hardware, with NVIDIA and AMD controlling 65% of the global GPU market, as per Gartner. These factors solidified the U.S.’s role as the backbone of advanced packaging innovation in North America.

Canada is expected to grow at the fastest CAGR of 13.7% and is driven by its strategic focus on sustainable technologies and clean energy integration. According to Natural Resources Canada, over CAD 2 billion was invested in green semiconductor initiatives in 2024, with advanced packaging playing a pivotal role in reducing power consumption in IoT devices and renewable energy systems. Canada’s expertise in quantum computing also positioned it as a growth leader, Quantum Valley Investments reported that Canadian quantum startups raised CAD 1.2 billion in venture capital in 2024. Furthermore, Canada’s proximity to U.S. tech hubs enabled seamless collaboration, with companies like Teledyne DALSA expanding their operations by 25% annually . The rise of autonomous vehicles in Canada, projected to reach 15% adoption by 2030 and will further drive demand for advanced packaging solutions tailored to AI and sensor fusion technologies.

TOP PLAYERS IN THIS MARKET

Intel Corporation

Intel Corporation has been a cornerstone of innovation in the North America Advanced Packaging Market, leveraging its decades-long expertise in semiconductor manufacturing. The company has pioneered advanced packaging technologies such as Embedded Multi-Die Interconnect Bridge (EMIB) and Foveros 3D stacking, which have set new benchmarks for performance and efficiency. Intel’s focus on integrating multiple chips into a single package has addressed critical challenges in miniaturization and power consumption, making its solutions indispensable for industries like AI, cloud computing, and automotive electronics. By collaborating with academic institutions and industry partners, Intel has not only strengthened its technological leadership but also fostered an ecosystem that accelerates the adoption of advanced packaging techniques across North America. Its commitment to pushing the boundaries of chip design has positioned it as a key enabler of next-generation electronic devices.

Taiwan Semiconductor Manufacturing Company (TSMC)

Taiwan Semiconductor Manufacturing Company (TSMC) has played a transformative role in shaping the North America Advanced Packaging Market through its cutting-edge technologies and global influence. As a leader in semiconductor foundry services, TSMC has introduced innovative solutions like Integrated Fan-Out (InFO) and Chip-on-Wafer-on-Substrate (CoWoS), which cater to high-performance applications such as 5G networks and data centers. In North America, TSMC has expanded its footprint by establishing advanced packaging facilities and forming strategic partnerships with leading tech companies. Its ability to deliver highly reliable and scalable packaging solutions has made it a preferred partner for firms seeking to integrate complex functionalities into compact designs. TSMC’s contributions have not only enhanced the region’s manufacturing capabilities but also reinforced North America’s position as a hub for semiconductor innovation.

Advanced Micro Devices (AMD)

Advanced Micro Devices (AMD) has emerged as a dynamic player in the North America Advanced Packaging Market, driven by its relentless pursuit of performance and efficiency in semiconductor design. The company has leveraged advanced packaging techniques to create powerful processors that cater to gaming, AI, and enterprise applications. AMD’s focus on heterogeneous integration has allowed it to combine CPUs, GPUs, and other components into unified systems, enabling seamless multitasking and superior computational power. By prioritizing customer-centric innovations, AMD has consistently delivered solutions that meet the evolving demands of modern electronics. Its efforts to enhance energy efficiency and reduce latency have set new standards in the industry, inspiring widespread adoption of advanced packaging technologies across North America. Through its visionary approach, AMD continues to shape the future of semiconductor packaging.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Investment in Research and Development

One of the most critical strategies adopted by key players in the North America Advanced Packaging Market is a strong focus on research and development. By channeling significant resources into R&D, companies are able to explore new materials, techniques, and designs that enhance the performance and efficiency of advanced packaging solutions. This strategy has allowed them to stay ahead of technological trends and address emerging challenges in industries like AI, 5G, and automotive electronics. The emphasis on innovation not only strengthens their competitive edge but also positions them as leaders in developing next-generation semiconductor technologies. Through continuous experimentation and refinement, these companies ensure that their solutions remain at the forefront of the rapidly evolving market landscape.

Strategic Partnerships and Collaborations

Another major strategy involves forming strategic partnerships and collaborations with other industry players, academic institutions, and government bodies. By working together, companies can pool expertise, share resources, and accelerate the development of advanced packaging technologies. These partnerships often lead to breakthroughs that would be difficult to achieve independently, enabling faster adoption of cutting-edge solutions. Collaborations also help companies expand their reach and influence by tapping into new markets or addressing complex challenges through joint efforts. This approach fosters an ecosystem of innovation, where knowledge exchange and co-development drive the industry forward while strengthening the position of the participating organizations.

Expansion of Manufacturing Facilities

Key players in the North America Advanced Packaging Market have also focused on expanding their manufacturing facilities to meet growing demand and improve supply chain resilience. By establishing new production sites or upgrading existing ones, companies aim to enhance their capacity to deliver advanced packaging solutions at scale. This strategy not only allows them to cater to diverse customer needs but also reduces dependency on external suppliers, ensuring greater control over quality and timelines. Additionally, localized manufacturing helps companies respond more effectively to regional requirements, fostering stronger relationships with clients. By investing in robust infrastructure, these players reinforce their ability to maintain a steady supply of innovative products while adapting to dynamic market conditions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

ASE Technology Holding Co. Ltd., Amkor Technology, Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, Samsung Electronics Co. Ltd., Jiangsu Changjiang Electronics Technology Co. Ltd. (JCET), Siliconware Precision Industries Co. Ltd. (SPIL), Powertech Technology Inc., STATS ChipPAC Pte. Ltd., ChipMOS Technologies Inc., Fujitsu Semiconductor Ltd., Texas Instruments, and Analog Devices are playing dominating role in the North America Advanced Packaging Market.

The competition in the North America Advanced Packaging Market is intense, as many big companies are working hard to lead the industry. This market is very important because it helps make electronic devices smaller, faster, and more powerful. Companies like Intel, TSMC, and AMD are some of the top players, and they are all trying to create better packaging technologies to meet the growing demand for advanced electronics. These companies compete by investing in new ideas, improving their products, and working with other businesses or universities to stay ahead.

One reason for the tough competition is that the market is growing quickly. More people want smart devices, electric cars, and faster internet, which means there is a bigger need for advanced packaging solutions. To win, companies try to offer unique features, such as making chips use less energy or work better in extreme conditions. They also focus on keeping their prices reasonable while delivering high-quality products.

Another part of the competition is about teamwork. Many companies partner with others to share knowledge and resources. This helps them solve problems faster and create new technologies. At the same time, they also compete to build factories closer to customers in North America, so they can deliver products quickly and avoid delays.

RECENT HAPPENINGS IN THE MARKET

- In October 2024, ProAmpac, a leader in flexible packaging, unveiled several sustainable packaging solutions at PACK EXPO 2024 in Chicago. These innovations, including the FiberSculpt and FiberCool bags, are expected to significantly advance eco-friendly packaging options and improve product shelf life.

- In January 2025, the U.S. Department of Commerce announced $1.4 billion in funding for semiconductor advanced packaging. This investment is aimed at boosting U.S. leadership in semiconductor manufacturing and packaging, ensuring a robust domestic industry.

- In October 2024, TSMC and Amkor Technology signed a memorandum of understanding to provide advanced packaging and testing services from a new facility in Peoria, Arizona. This partnership, supported by the U.S. government’s CHIPS and Science Act, is set to strengthen the U.S. semiconductor packaging industry.

- In January 2025, the CHIPS National Advanced Packaging Manufacturing Program (NAPMP) finalized $1.4 billion in funding awards to promote the growth of the U.S. semiconductor advanced packaging sector. This initiative is expected to foster innovation and create new opportunities in the field.

- In October 2024, ProAmpac showcased its 2024 packaging innovations, including the ProActive Intelligent Moisture Protect MP-1000 platform, at PACK EXPO. These new technologies are anticipated to improve packaging sustainability and enhance product shelf life without using desiccant sachets.

MARKET SEGMENTATION

This research report on the North America advanced packaging market is segmented and sub-segmented into the following categories.

By Packaging Platform

- Flip Chip

- Fan-in WLP

- Fan-out

- Embedded Die

- 2.5D/3D

By End-Use Industry

- Consumer Electronics

- Automotive

- Telecommunications

- Healthcare

- Industrial

- Others

By Country

- The United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What is the projected North America Advanced Packaging market size by 2033?

The North America Advanced Packaging market is estimated to reach USD 24.83 billion by 2033.

2. What factors are driving the growth of the advanced packaging market?

Growth drivers include increasing demand for miniaturized electronics, advancements in semiconductor technology, and rising adoption of IoT-connected devices, such as wearables and electric vehicles.

3. What trends are shaping the future of advanced packaging in North America?

Emerging trends include copper hybrid bonding, wafer-level packaging innovations, and increased focus on sustainable packaging solutions for IoT devices and electric vehicles.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]