North America Activated Aluma Market Research Report – Segmented By End-Use ( Water Treatment, Healthcare ) Application ( Catalyst, Bio Ceramics ) and Country (The U.S., Canada and Rest of North America) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts 2025 to 2033.

North America Activated Aluma Market Size

The North America Activated Aluma Market Size was valued at USD 0.42 billion in 2024. The North America Activated Aluma Market size is expected to have 5.87 % CAGR from 2025 to 2033 and be worth USD 0.71 billion by 2033 from USD 0.45 billion in 2025.

The North American activated alumina market has established a robust presence owing to its critical applications across diverse industrial sectors. This steady expansion is primarily driven by the material's indispensable role in water treatment, catalysts, and desiccants. Also, the region benefits from stringent environmental regulations, which mandate advanced water purification methods, thereby boosting demand for activated alumina. According to the U.S. Environmental Protection Agency, approximately 90% of public water systems in the United States utilize some form of advanced filtration technology, with activated alumina playing a pivotal role. Additionally, the oil and gas sector’s reliance on activated alumina for removing impurities during refining processes contributes significantly to market stability. Canada, with its abundant natural resources, also supports regional growth through increased industrial activities. So, the market conditions can be described by regulatory compliance, technological advancements, and industrial expansion, creating a conducive environment for sustained demand.

MARKET DRIVERS

Rising Demand for Water Purification Solutions

Water purification stands as a cornerstone driver for the activated alumina market in North America. With increasing concerns about water contamination, activated alumina is widely used to remove fluoride, arsenic, and other impurities. According to the World Health Organization, nearly 200 million people globally are exposed to high fluoride levels in drinking water, with significant cases reported in North America. Activated alumina's efficiency in adsorbing contaminants makes it indispensable. The U.S. Geological Survey emphasizes that groundwater contamination affects approximately 43 million Americans annually. Furthermore, government initiatives, such as the Clean Water Act, have mandated stringent water quality standards, propelling demand. Investments in municipal water treatment infrastructure further amplify this trend.

Expanding Oil and Gas Industry

The oil and gas sector serves as another major driver for the market by leveraging activated alumina for purifying gases and liquids during refining processes. As per the U.S. Energy Information Administration, North America accounts for a significant portion of global oil production, with refining activities concentrated in the Gulf Coast region. Activated alumina's ability to adsorb moisture and sulfur compounds enhances operational efficiency and product quality. A study by the American Petroleum Institute notes that refining costs can increase by up to 15% without proper desiccant usage, emphasizing the material's importance. Additionally, the shale gas boom has spurred investments in natural gas processing plants, where activated alumina is extensively used.

MARKET RESTRAINTS

High Production Costs

One significant restraint impacting the activated alumina market in North America is the high cost associated with its production. The manufacturing process involves multiple stages, including bauxite calcination and activation, which require substantial energy inputs and specialized equipment. According to the U.S. Department of Energy, industrial energy costs in the region make up a significant portion total production expenses, placing financial pressure on manufacturers. Besides, raw material price volatility exacerbates the challenge. These cost fluctuations limit profit margins and hinder smaller players from entering the market. Larger companies, however, absorb these costs by passing them onto consumers, leading to higher product prices. This pricing barrier restricts widespread adoption, particularly in cost-sensitive industries like construction and small-scale manufacturing, ultimately constraining market growth.

Stringent Environmental Regulations

Environmental regulations pose another major challenge to the activated alumina market. The production process generates significant carbon emissions and waste byproducts, attracting scrutiny from regulatory bodies. Like, industrial emissions from alumina production contribute notably to the total greenhouse gas emissions in the U.S. To comply with regulations, manufacturers must invest in cleaner technologies, which often require substantial capital outlays. Furthermore, stricter waste disposal norms impose additional operational burdens, limiting production scalability. This regulatory landscape creates a challenging environment for stakeholders aiming to scale their operations efficiently

MARKET OPPORTUNITIES

Growing Adoption in Bio Ceramics

The bio ceramics segment presents a lucrative opportunity for the activated alumina market in North America. Activated alumina's biocompatibility and mechanical strength make it ideal for medical implants, dental prosthetics, and tissue engineering scaffolds. Moreover, advances in healthcare technologies, coupled with an aging population, are driving demand for innovative biomaterials. Additionally, research into nanostructured activated alumina for drug delivery systems is gaining traction. A study published in the Journal of Biomedical Materials Research notes a 25% increase in R&D funding for bio ceramics in 2022.

Expansion in Renewable Energy Applications

Activated alumina's role in renewable energy applications offers another promising avenue for market growth. It is increasingly utilized in hydrogen purification and fuel cell technologies due to its excellent adsorption properties. According to the Hydrogen Council, the global hydrogen economy is expected to generate $2.5 trillion in revenue by 2050, with North America emerging as a key player. Also, the U.S. Department of Energy reports that hydrogen fuel cells could power over 10 million vehicles by 2030, necessitating efficient purification systems. Activated alumina's ability to remove impurities like water vapor and carbon dioxide ensures high-purity hydrogen production, making it indispensable. Furthermore, solar energy storage systems utilizing phase-change materials benefit from activated alumina's thermal stability. A report by the National Renewable Energy Laboratory notes a significant increase in solar energy adoption in North America since 2020. These developments emphasize the material's transformative potential in advancing clean energy technologies, creating vast opportunities for market expansion.

MARKET CHALLENGES

Limited Awareness Among End-Users

A significant challenge facing the activated alumina market in North America is the limited awareness among end-users regarding its multifaceted applications. Despite its proven efficacy in industries like water treatment and healthcare, many small and medium enterprises remain unaware of its benefits. This knowledge gap restricts broader adoption, particularly in emerging sectors like bio ceramics and renewable energy. Apart from these, misconceptions about high costs deter potential users, even though long-term savings outweigh initial investments. a study by the Manufacturing Institute, in partnership with Deloitte, highlights that lack of technical expertise and training is a significant contributor to the skills gap in manufacturing, leaving businesses unprepared to integrate advanced materials into their processes.

Intense Competition from Substitute Materials

Another pressing challenge is the intense competition from substitute materials, which threatens market share for activated alumina. Alternatives like silica gel and molecular sieves offer similar functionalities at competitive prices, creating a fragmented competitive landscape. These materials are often perceived as more cost-effective, particularly in low-end applications like packaging and electronics. Moreover, advancements in polymer-based adsorbents are further intensifying rivalry. A report by the American Chemical Society notes that polymer alternatives exhibit superior performance in specific applications, such as humidity control in pharmaceutical packaging. This growing preference for substitutes erodes activated alumina's market dominance, forcing manufacturers to innovate and differentiate their offerings to maintain relevance.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.87 % |

|

Segments Covered |

By End-Use, Application and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

The U.S., Canada and Rest of North America |

|

Market Leader Profiled |

BASF SE, Honeywell International Inc., Sumitomo Chemical Co., Ltd., Axens, AGC CHEMICALS PVT. LTD. |

SEGMENTAL ANALYSIS

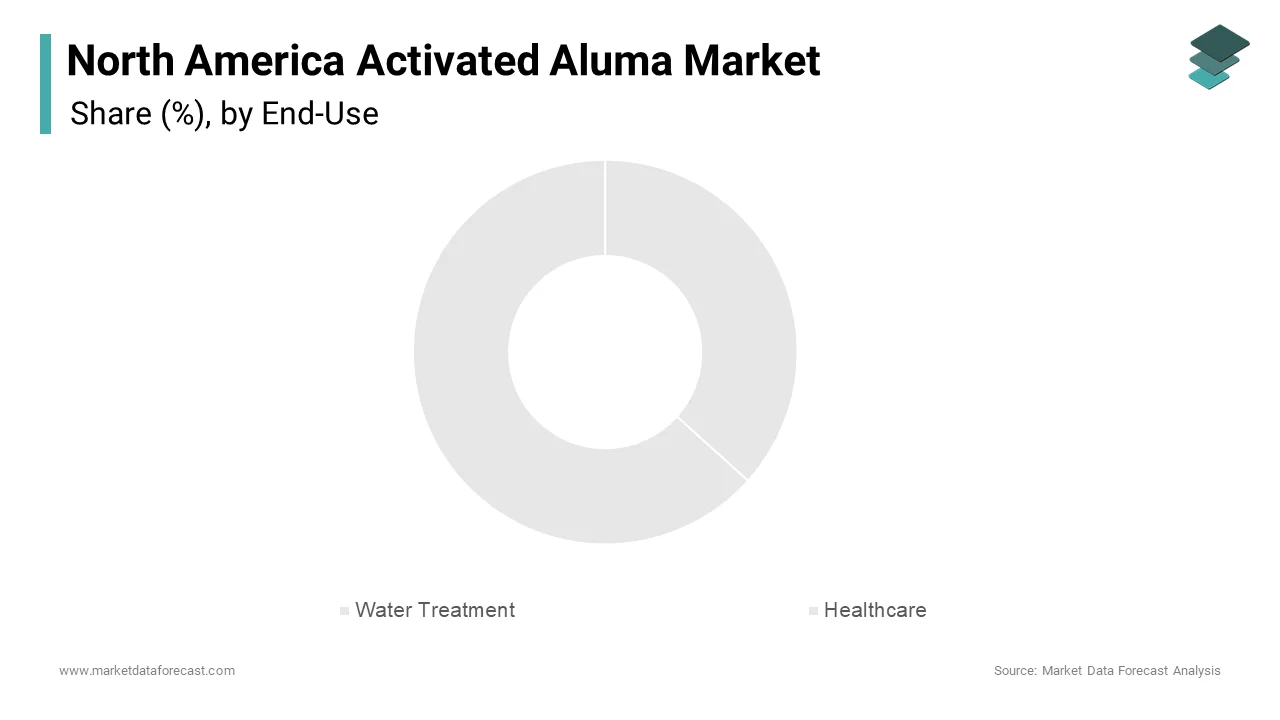

By End-Use Insights

The water treatment segment dominated the North American activated alumina market by holding a share of 35.2% in 2024. This growth of the segment is due to the material's unparalleled ability to remove contaminants like fluoride and arsenic, addressing critical water quality issues. Many community water systems in the U.S. utilize advanced filtration technologies, with activated alumina being a preferred choice. Regulatory frameworks, such as the Safe Drinking Water Act, mandate the removal of harmful impurities, further solidifying its position. Additionally, the rise in industrial wastewater treatment initiatives contributes significantly. The U.S. Environmental Protection Agency estimates that industrial facilities discharge 300 million gallons of contaminated water daily, necessitating robust purification solutions.

The healthcare segment is the fastest-growing, with a projected CAGR of 7.5% from 2025 to 2033. This rapid growth is fueled by activated alumina's applications in bio ceramics, drug delivery systems, and medical devices. it is expected that the proportion of the North American population aged 65 and over will increase, and by 2030, roughly one in five Americans will be 65 or older, drives demand for orthopedic implants and dental prosthetics. Furthermore, advancements in nanotechnology have expanded its use in targeted drug delivery, enhancing therapeutic efficacy. A study in the Journal of Controlled Release reports a 30% increase in R&D funding for nanostructured materials in healthcare. These innovations when coupled with rising healthcare expenditures position the segment as a key growth driver, reflecting the material's transformative impact on modern medicine.

By Application Insights

The catalyst application segment led the North American activated alumina market by commanding a share of 40.6% in 2024. This influence of the segment is attributed to its widespread use in petrochemical refining and chemical synthesis processes. Activated alumina's high surface area and thermal stability make it an ideal choice for cracking, reforming, and dehydration processes. Additionally, the growing demand for cleaner fuels aligns with its role in sulfur removal, as noted by the U.S. Energy Information Administration.

The bio ceramics segment is the quickest expanding, with a CAGR of 8.2% in the coming years. This progress is propelled by activated alumina's biocompatibility and mechanical strength, making it suitable for medical implants and tissue engineering. The aging population in North America, projected to reach 22% by 2030, drives demand for orthopedic and dental applications. Apart from these, advancements in nanostructured materials for drug delivery systems are gaining traction. A study in the Journal of Biomedical Materials Research notes a 25% increase in R&D funding for bio ceramics in 2022.

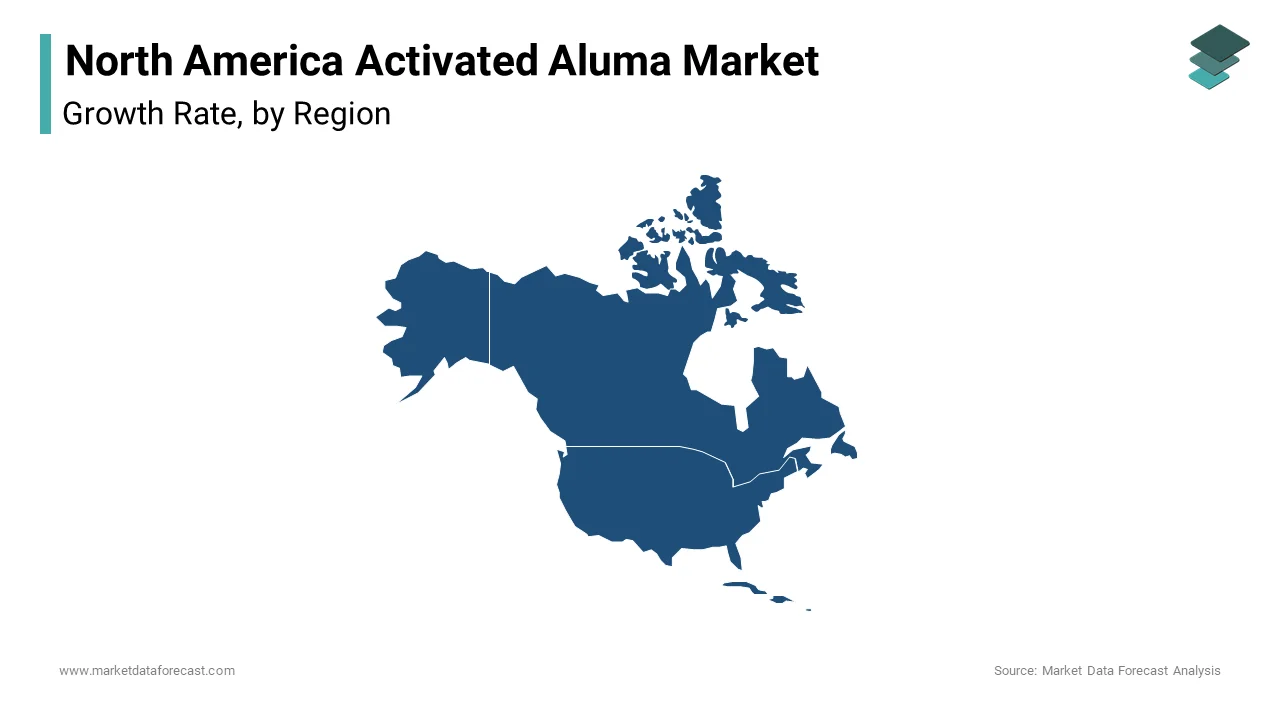

COUNTRY LEVEL ANALYSIS

The United States stood as the epicenter of the North American activated alumina market by commanding a 65.8% share in 2024. This is because of its advanced industrial infrastructure, stringent environmental regulations, and robust demand across multiple sectors. The Clean Water Act has been a cornerstone in driving the adoption of activated alumina for water treatment applications, particularly for removing contaminants like fluoride and arsenic. A report by the Environmental Protection Agency emphasizes that a significant portion of public water systems in the U.S. utilize advanced filtration technologies, with activated alumina playing a pivotal role. Additionally, the country's oil and gas industry, concentrated in regions like the Gulf Coast, heavily relies on activated alumina for refining processes. According to the U.S. Energy Information Administration, the nation accounts for approximately 20% of global oil production, underscoring its reliance on this material for sulfur removal and gas purification. Furthermore, the healthcare sector's rapid growth, driven by an aging population and advancements in bio ceramics, further amplifies demand.

Canada holds a significant share of the North American activated alumina market. It is bolstered by its abundant natural resources and expanding industrial activities. The Canadian Environmental Protection Act mandates stringent water quality standards, driving demand for activated alumina in municipal water treatment systems. According to Natural Resources Canada, the mining and oil sands industries are among the primary consumers of activated alumina, utilizing it extensively for gas purification and desiccant applications. The Alberta oil sands, one of the world’s largest oil reserves, rely heavily on activated alumina to remove impurities during refining, creating a steady demand stream. Moreover, Canada's focus on sustainability and clean energy initiatives has spurred investments in renewable energy projects, where activated alumina is used for hydrogen purification and fuel cell technologies. The country's strategic emphasis on eco-friendly solutions aligns with global trends, positioning it as a key player in the regional market.

Mexico is key player in the North American activated alumina market and is driven by rapid industrialization, urbanization, and infrastructural development. Activated alumina's role in purifying water and removing harmful impurities has become indispensable, especially in regions with high groundwater contamination. Additionally, the automotive manufacturing sector, one of Mexico's fastest-growing industries, utilizes activated alumina as a desiccant in air conditioning systems and vehicle components. According to the International Trade Administration, Mexico is the seventh-largest vehicle producer globally, creating a substantial demand for high-performance materials. The country's strategic geographic location also positions it as a gateway for exports to both North and South America, enhancing its market significance.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the North America Activated Aluma Marketc are BASF SE, Honeywell International Inc., Sumitomo Chemical Co., Ltd., Axens, AGC CHEMICALS PVT. LTD., Sorbead India, Shandong Zhongxin New Material Technology Co., Ltd., Luoyang Xinghua Chemical Co., Ltd., Sialca Industries, Shayan Corporation, BeeChems, Hengye Inc., Huber Engineered Materials.

The North American activated alumina market is characterized by intense competition, driven by the presence of established giants and emerging players striving to carve out their niche. Albemarle Corporation, BASF SE, and Honeywell International Inc. dominate the landscape, leveraging their extensive R&D capabilities, global supply chains, and brand recognition. However, the market is also witnessing fragmentation, with smaller firms introducing cost-effective alternatives and niche products. This has intensified rivalry, particularly in segments like desiccants and bio ceramics, where polymer-based substitutes pose a significant threat. To differentiate themselves, key players focus on innovation, sustainability, and customer-centric solutions. Regulatory compliance and environmental standards further add complexity, compelling manufacturers to invest in cleaner technologies. Additionally, the rise of e-commerce platforms has lowered barriers to entry, enabling smaller firms to compete effectively. This dynamic interplay of factors creates a fiercely competitive environment, pushing companies to continuously innovate and adapt to changing market conditions.

Top Players in the Market

The North American activated alumina market is dominated by three major players: Albemarle Corporation, BASF SE, and Honeywell International Inc., each contributing significantly to the global market through innovation, sustainability, and strategic expansions. Albemarle Corporation, headquartered in Charlotte, North Carolina, is a global leader in specialty chemicals. The company excels in producing high-performance catalysts and adsorbents, leveraging its expertise in refining technologies. Its commitment to research and development has enabled it to introduce cutting-edge products tailored for the oil and gas and healthcare sectors. BASF SE, based in Germany but with a strong foothold in North America. The company focuses on sustainable solutions, offering eco-friendly activated alumina products that align with global environmental standards. Its innovations in bio ceramics and desiccants have positioned it as a key player in emerging applications. Honeywell International Inc. is a U.S.-based conglomerate. Its advanced materials division caters to diverse industries, including aerospace, automotive, and pharmaceuticals. Together, these companies account for a major share of the global activated alumina market, driving advancements and setting benchmarks for quality, efficiency, and sustainability.

Top Strategies Used by Key Players

Key players in the North American activated alumina market employ a range of strategies to maintain their competitive edge and drive growth. Mergers and acquisitions (M&A) are a prominent strategy, enabling companies to expand their product portfolios and enter new markets. For instance, Albemarle Corporation has actively pursued acquisitions of smaller firms specializing in nanostructured materials and advanced adsorbents, enhancing its capabilities in emerging applications like bio ceramics. Strategic partnerships and collaborations are another critical approach, with BASF SE forging alliances with renewable energy firms to develop innovative solutions for hydrogen purification and fuel cell technologies. These partnerships not only broaden their market reach but also align with global sustainability goals. Research and development (R&D) remains a cornerstone strategy, with Honeywell International Inc. investing heavily in digital technologies to optimize production processes and enhance product performance. The company’s focus on developing eco-friendly desiccants underscores its commitment to meeting evolving consumer demands. Additionally, companies emphasize branding and market education, launching campaigns to raise awareness about activated alumina's multifaceted applications. These strategies collectively ensure market leadership, foster innovation, and address challenges posed by substitutes and regulatory pressures.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, Albemarle Corporation acquired NanoPur Technologies, a startup specializing in nanostructured activated alumina, enhancing its portfolio for bio ceramics and drug delivery systems.

- In June 2024, BASF SE launched EcoSorb, a line of sustainable desiccants designed to meet stringent environmental regulations, targeting eco-conscious industries like packaging and pharmaceuticals.

- In August 2024, Honeywell International Inc. partnered with HydroGen Solutions, a renewable energy firm, to develop advanced hydrogen purification systems using activated alumina, aligning with global clean energy initiatives.

- In October 2024, Porocel invested $50 million in a state-of-the-art production facility in Texas to meet rising demand from the oil and gas sector, particularly for catalyst applications.

- In December 2024, Sorbead India expanded its distribution network across North America by establishing partnerships with local distributors, strengthening its market presence and accessibility.

MARKET SEGMENTATION

This research report on the north america activated alumina market has been segmented and sub-segmented into the following.

By End-Use

- Water Treatment

- Healthcare

By Application

- Catalyst

- Bio Ceramics

By Country

- The U.S.

- Canada

- Rest of North America.

Frequently Asked Questions

What are the primary applications of activated alumina in North America?

Activated alumina is widely used in North America for water treatment, air purification, drying gases, and removing fluoride and arsenic from drinking water. It is also used in catalysts and adsorbents in chemical processes.

What is driving the growth of the activated alumina market in North America?

The growing demand for clean drinking water, environmental regulations requiring air and water purification, and the expanding oil and gas sector are key factors driving the growth of the activated alumina market in North America.

What are the key challenges faced by the activated alumina market in North America?

Some challenges include high production costs, competition from alternative materials (such as synthetic zeolites), and fluctuations in raw material prices.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]