North America Painting Tools Market Size, Share, Trends & Growth Forecast, Segmented By Product, Pricing, Application, Distribution Channel, And By Country (The USA, Canada, Mexico and Rest of North America), Industry Analysis From 2025 to 2033

North America Painting Tools Market Size

The North America Painting tools market size was valued at USD 3.79 billion in 2024 and is anticipated to reach USD 3.95 billion in 2025 from USD 5.50 billion by 2033, growing at a CAGR of 4.23% during the forecast period from 2025 to 2033.

MARKET DRIVERS

Rising Demand for Residential Renovations

A primary driver propelling the North America painting tools market is the escalating demand for residential renovations, which is fueled by a surge in home ownership and remodeling activities. Like, homeownership rates reached 65.8% in 2022, the highest in over a decade, creating a fertile ground for painting tool sales. Additionally, a significant portion of homeowners undertaking renovations prioritize aesthetic upgrades, including painting, to enhance property value. This trend is particularly pronounced among millennials, who represent a notable share of first-time buyers and are more inclined toward frequent updates. Professional painters catering to this demographic often invest in premium tools like high-density rollers and precision brushes, driving demand across product categories. Moreover, the proliferation of DIY culture, amplified by platforms like Pinterest and YouTube, has empowered amateur painters to undertake projects independently. Also, DIY paint supplies accounted for a considerable share of total retail sales, underscoring the dual influence of professional and amateur users.

Advancements in Tool Technology

Another pivotal driver is the continuous advancement in painting tool technology, which enhances efficiency and user experience. Innovations such as ergonomic handles, anti-drip designs, and self-cleaning mechanisms have transformed traditional tools into high-performance instruments. Similarly, manufacturers like Purdy have developed synthetic brushes with superior bristle retention, reducing material waste and improving finish quality. These technological leaps not only cater to the growing emphasis on precision but also align with sustainability goals by minimizing resource consumption. Furthermore, industry reports reveal that eco-friendly tools designed for low-VOC paints are gaining traction, with an estimated rise in adoption rates.

MARKET RESTRAINTS

High Costs of Premium Tools

A significant restraint hindering the broader adoption of painting tools in North America is the high cost associated with premium models, which often integrate advanced features or specialized materials. Consequently, affordability remains a critical challenge impeding broader market penetration across socio-economic demographics.

Environmental Regulations on Paints

Another restraint stems from stringent environmental regulations governing paint formulations, which indirectly impact tool compatibility and performance. Governments across North America have mandated reductions in volatile organic compounds (VOCs) to mitigate air pollution, compelling manufacturers to reformulate paints with water-based or low-VOC alternatives. However, these eco-friendly formulations often require specialized tools for optimal application, increasing complexity for users accustomed to traditional solvent-based products. For example, low-VOC paints necessitate fine-tipped brushes and high-pressure spray systems to achieve desired finishes, driving up initial investment costs. Misinformation about tool adaptability further compounds the issue, with a major percentage of surveyed contractors reporting dissatisfaction due to mismatched equipment. While regulatory compliance safeguards environmental health, it simultaneously imposes operational hurdles that hinder seamless adoption of modern painting tools, creating friction within the market ecosystem.

MARKET OPPORTUNITIES

Growing Commercial Construction Sector

A promising opportunity for the North American painting tools market lies in the burgeoning commercial construction sector, which increasingly demands high-performance tools to meet project specifications. These projects often require durable finishes and precise application techniques, prompting contractors to adopt advanced tools like air-assisted spray guns and extension poles. Similarly, the use of industrial-grade rollers reduced labor hours during large-scale refurbishments, emphasizing their economic value. Furthermore, partnerships between construction firms and tool manufacturers facilitate bulk procurement, ensuring the timely deployment of cutting-edge technologies.

Surge in Smart Home Integration

Another lucrative avenue is the integration of smart technologies into painting tools, aligning with the broader trend of connected living spaces. Smart painting tools, equipped with IoT sensors and app-based controls, offer unprecedented convenience and precision, appealing to tech-savvy consumers. For instance, Graco’s SmartControl sprayers enable users to adjust pressure settings remotely, enhancing workflow efficiency. Additionally, voice-activated masking tapes and automated tray dispensers simplify complex tasks, fostering greater inclusivity among amateur users. These innovations not only differentiate brands in a crowded marketplace but also cater to evolving lifestyle preferences, prioritizing automation and ease of use.

MARKET CHALLENGES

Intense Market Competition

The North American painting tools market faces significant challenges stemming from intense competition among key players vying for dominance. This saturation complicates efforts to differentiate products based solely on functionality, pushing companies to invest heavily in marketing and R&D initiatives. However, aggressive pricing strategies adopted by competitors frequently erode profit margins, particularly for mid-tier manufacturers struggling to match promotional budgets. Furthermore, counterfeit products flooding online retail platforms pose additional threats, undermining brand credibility and consumer trust. Such illicit activities distort market dynamics, forcing legitimate businesses to allocate resources toward anti-counterfeiting measures. Navigating this fiercely contested landscape requires innovative approaches, yet achieving sustainable profitability remains a daunting task amid mounting operational pressures.

Skill Gaps Among Users

Another formidable challenge is the persistent skill gap among end-users, particularly DIY enthusiasts and novice contractors, which impedes optimal utilization of advanced painting tools. Despite the widespread availability of tutorials and guides, a significant portion of amateur painters struggle with achieving professional-grade finishes due to improper technique or inadequate knowledge of tool functionality. This disconnect not only diminishes customer satisfaction but also tarnishes brand reputation when tools fail to deliver expected results. Additionally, training programs offered by manufacturers often lack accessibility, especially in remote regions, leaving many users ill-equipped to leverage sophisticated features. While industry leaders advocate for hands-on workshops and virtual demonstrations, scaling these initiatives poses logistical challenges.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

4.23% |

|

Segments Covered |

By Product, Pricing, Application, Distribution Channel, and Country |

|

Various Analyses Covered |

Global, Regional, and country-level analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country's Covered |

The United States, Canada, and the Rest of North America |

|

Market Leaders Profiled |

Allway Tool, Anderson Products, Asian Paints, Braun Brush Co., Durapaints, EPOS Egypt, Gordon Brush Mfg. Co., Inc., Harbor Freight Tools, JAT Transforming Spaces, MAAN, Milton Brushware, Nespoli Group, NOUR Trading House Inc., PETA Decorating, Purdy, Richard Tools, S. R. Bristle Products, TechnoChem Industries, The Mill-Rose Company, Vishwakarma Impex. |

SEGMENTAL ANALYSIS

By Product Insights

The Brushes segment dominated the North America painting tools market by commanding a 40.7% share in 2024. Their versatility and precision make them indispensable across residential, commercial, and industrial applications. Professional painters rely on high-quality brushes for intricate detailing, while DIY enthusiasts appreciate their ease of use for smaller projects. According to a study by the Paint Quality Institute, synthetic brushes exhibit superior durability compared to natural variants, contributing to an increase in sales in the past few years. Additionally, innovations such as angled tips and ergonomic handles enhance user comfort, driving preference among diverse demographics. Manufacturers capitalize on this demand by launching customizable options tailored to specific substrates, further solidifying brushes’ leadership position while addressing evolving consumer expectations.

On the other hand, the spray guns segment emerges as the fastest-growing segment, boasting a CAGR of 7.2% from 2025 to 2033. This rapid expansion is fueled by their unparalleled efficiency in covering large surface areas with minimal effort. Industries such as automotive refinishing and furniture manufacturing extensively utilize spray guns to achieve uniform coatings. Technological breakthroughs enabling variable pressure adjustments and multi-pattern spraying broaden applicability across diverse sectors. Moreover, partnerships with distributors streamline accessibility, ensuring the timely deployment of cutting-edge technologies. As industries embrace automation and digitization, the imperative for seamless environmental controls grows, positioning this segment as a transformative force within the market.

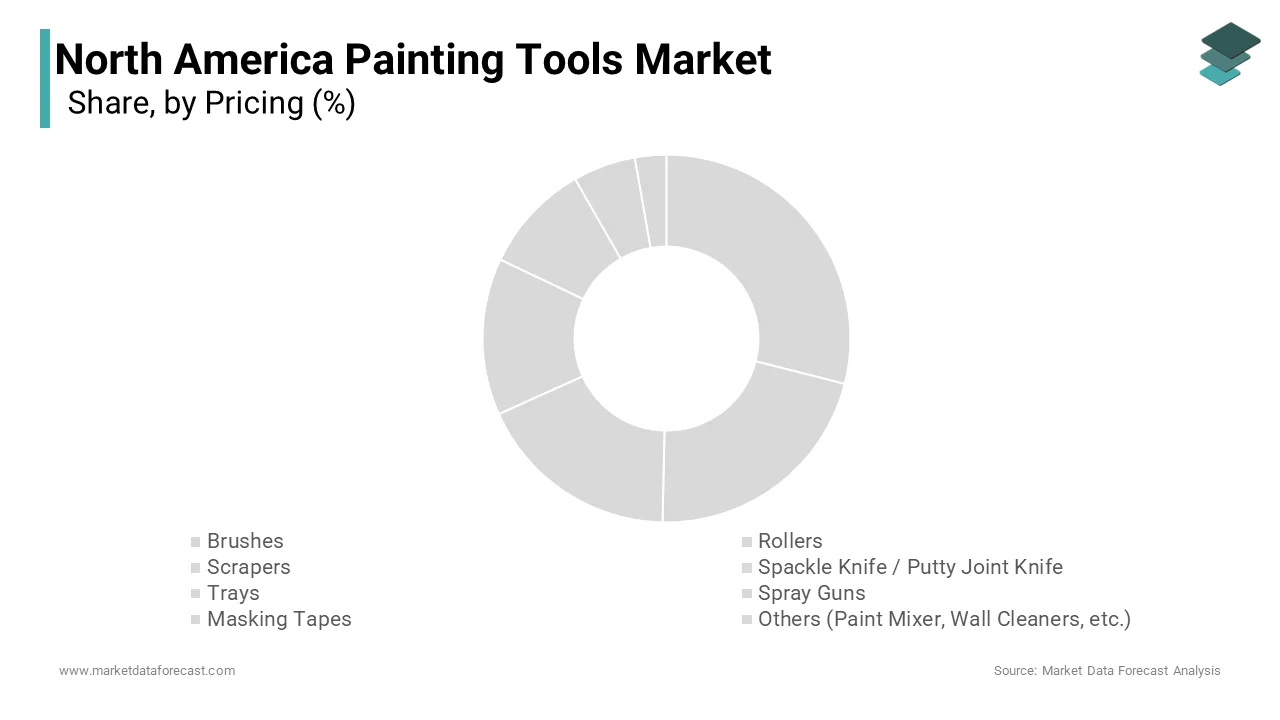

By Pricing Insights

The segment of medium-priced tools led the North American painting tools market by capturing 55.9% of total revenue in 2024. This growth arises from their ability to strike a balance between affordability and functionality, appealing to both professional contractors and DIY enthusiasts. Similarly, medium-priced rollers and brushes are preferred for a notable share of residential renovation projects, owing to their reliability and versatility. Furthermore, innovations such as anti-drip designs and ergonomic handles enhance user experience without inflating costs, driving preference among budget-conscious consumers. Strategic collaborations between manufacturers and suppliers ensure widespread distribution, fostering accessibility across urban and suburban markets.

The High-priced tools category represents the rapidly expanding segment, registering a CAGR of 9.8%. This surge is credited to the indispensable role of advanced tools in achieving precision and durability, particularly in commercial and industrial applications. For instance, airless spray guns capable of handling viscous coatings are essential for large-scale infrastructure projects. Additionally, stringent occupational health regulations mandate comfortable working conditions, driving factories to upgrade outdated systems with energy-efficient alternatives. Technological breakthroughs, such as IoT-enabled monitoring, further bolster efficiency, allowing real-time adjustments tailored to specific production needs.

COUNTRY LEVEL ANALYSIS

The United States commands the largest share of the North American painting tools market by accounting for 85.8% of regional revenue in 2024. This leading position is due to the pervasive urbanization trends and escalating demand for home improvement projects. Metropolitan areas like New York and Los Angeles exhibit exceptionally high adoption rates, with a large number of households utilizing advanced tools during peak renovation seasons. Furthermore, the nation’s robust e-commerce infrastructure facilitates easy access to affordable models is fostering widespread accessibility. Government initiatives promoting green technologies also incentivize manufacturers to develop energy-efficient variants, aligning with federal sustainability objectives.

Canada is moving ahead at a notable pace in the market. Harsh winters spanning several provinces necessitate effective painting solutions to combat moisture damage, driving consistent demand nationwide. Ontario and Quebec, home to dense urban populations, collectively account for a considerable share of domestic sales. Public health advisories issued by provincial authorities emphasize the importance of maintaining adequate humidity levels to mitigate respiratory ailments, further boosting consumer confidence in these products. Additionally, stringent environmental policies incentivize eco-friendly designs, prompting local manufacturers to innovate sustainable offerings. Cross-border trade agreements facilitate seamless import-export activities, enabling Canadian firms to leverage U.S.-based R&D expertise.

Mexico constitutes a key share of the North American painting tools market. Despite its smaller footprint, the country demonstrates considerable growth potential fueled by rapid urbanization and rising disposable incomes. Also, affordable pricing strategies adopted by domestic manufacturers make painting tools accessible to broader demographics, offsetting economic disparities prevalent in rural regions. Collaborations with international brands introduce advanced technologies previously unavailable locally, accelerating market evolution. Moreover, government-led housing programs incorporating climate control provisions enhance long-term prospects, embedding painting tools into mainstream construction practices.

The Rest of North America encompasses smaller economies such as Puerto Rico and the Caribbean islands, collectively representing a nascent yet promising segment. In addition, this region benefits from unique climatic conditions requiring tailored painting solutions. Although constrained by geographic isolation and logistical complexities, this segment’s untapped potential offers fertile ground for expansion, provided stakeholders address existing barriers through targeted interventions and collaborative efforts.

KEY MARKET PLAYERS

Allway Tool, Anderson Products, Asian Paints, Braun Brush Co., Durapaints, EPOS Egypt, Gordon Brush Mfg. Co., Inc., Harbor Freight Tools, JAT Transforming Spaces, MAAN, Milton Brushware, Nespoli Group, NOUR Trading House Inc., PETA Decorating, Purdy, Richard Tools, S. R. Bristle Products, TechnoChem Industries, The Mill-Rose Company, and Vishwakarma Impex are the market players that are dominating the North America painting tools market.

Top Players in the Market

Sherwin-Williams

Sherwin-Williams stands out as a leading player in the North American painting tools market, leveraging its reputation for innovation and reliability. Renowned for producing advanced models like the Purdy Clearcut Glide Angular Brush, Sherwin-Williams addresses key consumer pain points such as bristle shedding and uneven coverage. Strategic partnerships with major retailers like Lowe’s and Home Depot ensure widespread distribution, while investments in R&D yield cutting-edge features like tapered edges and extended handles. Its commitment to sustainability is evident in eco-friendly offerings, appealing to environmentally conscious buyers.

Benjamin Moore

Benjamin Moore occupies a prominent position, credited with revolutionizing the market through sleek, high-performance tools integrated with precision engineering. Its emphasis on aesthetics and functionality resonates with design-oriented consumers, bolstered by aggressive digital marketing campaigns. Furthermore, Benjamin Moore’s global supply chain network enables efficient scaling, reinforcing its competitive edge.

Wagner SprayTech

Wagner SprayTech rounds out the top three, specializing in affordable yet stylish tools catering to budget-conscious households. Known for its Control Spray Max HVLP System popular among DIY enthusiasts. Its focus on durability and ease of use fosters brand loyalty, particularly in suburban communities. Collaborations with online platforms like Amazon enhance visibility, while periodic discounts drive impulse purchases. Wagner’s adaptability to shifting consumer preferences ensures sustained relevance amidst fierce competition.

Top Strategies Used By Key Market Participants

Key players in the North American painting tools market employ diverse strategies to consolidate their positions and stimulate growth. Product differentiation emerges as a cornerstone tactic, with companies like Sherwin-Williams and Benjamin Moore investing heavily in R&D to introduce multifunctional devices combining precision with durability. Strategic alliances with e-commerce giants such as Amazon and Walmart facilitate extensive reach, enabling brands to tap into burgeoning online sales channels. Pricing strategies also play a pivotal role; premium manufacturers like Benjamin Moore adopt skimming models targeting affluent demographics, whereas Wagner SprayTech focuses on penetration pricing to attract budget-conscious buyers. Additionally, sustainability initiatives, including eco-friendly coatings and recyclable materials, resonate with environmentally aware consumers. Marketing campaigns emphasizing health benefits further amplify demand, particularly during peak seasons like winter.

COMPETITION OVERVIEW

The North American painting tools market is characterized by intense competition, marked by a delicate balance between established giants and emerging challengers. Market leaders like Sherwin-Williams and Benjamin Moore dominate through relentless innovation, consistently unveiling technologically advanced products that set industry benchmarks. Meanwhile, smaller firms like Wagner SprayTech capitalize on affordability and niche appeal, carving out loyal customer bases. The competitive landscape is further complicated by the influx of counterfeit products, which distort pricing structures and erode brand equity. Simultaneously, regulatory compliance serves as both a barrier and an opportunity, with companies investing in safer, greener designs to align with evolving standards.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Sherwin-Williams launched the Purdy Clearcut Glide Angular Brush, featuring advanced bristle retention technology. This move strengthened its portfolio of precision-focused products.

- In June 2023, Benjamin Moore unveiled the Ultra/Spec XP Sprayer, introducing adjustable flow control capabilities alongside high-pressure delivery. This reinforced its reputation for multifunctional innovation.

- In August 2023, Wagner SprayTech partnered with AmazonBasics to offer exclusive bundles, enhancing affordability and accessibility for budget-conscious consumers.

- In October 2023, Graco introduced the Xtreme Duty Airless Sprayer, combining high-viscosity handling with IoT-enabled monitoring. This addressed diverse consumer preferences effectively.

- In December 2023, Purdy collaborated with Home Depot to launch a DIY workshop series, educating amateur painters on advanced techniques, appealing to tech-savvy users.

MARKET SEGMENTATION

This research report on the North American painting tools market is segmented and sub-segmented into the following categories.

By Product

- Brushes

- Rollers

- Scrapers

- Spackle Knife / Putty Joint Knife

- Trays

- Spray Guns

- Masking Tapes

- Others (Paint Mixer, Wall Cleaners, etc.)

By Pricing

- Low

- Medium

- High

By Application

- Fine art & decorative painting

- Construction

- Residential

- Commercial

- Automotive

- Appliances

- Furniture

- Industrial machinery & equipment

- Others (utilities, government marking, restoration & conversion, etc.)

By Distribution Channel

- Online

- Company Website

- E-Commerce Site

- Offline

- Specialty Stores

- Mega Retail Stores

- Others

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What is driving growth in the North America painting tools market?

The market is expanding due to rising home renovations, increased demand for DIY tools, and booming construction in residential and commercial sectors across the U.S. and Canada.

What types of painting tools are most popular in North America?

Rollers, paint brushes, spray guns, and paint trays lead the market, with roller systems gaining popularity for their efficiency and ease of use in large surface applications.

Which end-user segments contribute most to the demand for painting tools?

The residential sector dominates due to constant remodeling and DIY trends, while professional contractors and commercial real estate projects also maintain steady demand.

What challenges does the North American painting tools industry face?

Challenges include price sensitivity in DIY segments, competition from low-cost imports, and environmental concerns related to disposable or plastic-based tool components.

What trends are shaping the future of painting tools in North America?

The market is shifting toward ergonomic designs, sustainable materials, multi-surface tools, and smart painting accessories that align with both professional and DIY needs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]