North America Energy Drinks Market Research Report - Segmented Based on Type, Ingredient Type, Packaging, and Country (The U.S., Canada and Rest of North America) – Analysis on Size, Share, Trends, & Growth Forecast (2026 to 2034)

North America Energy Drinks Market Report Summary

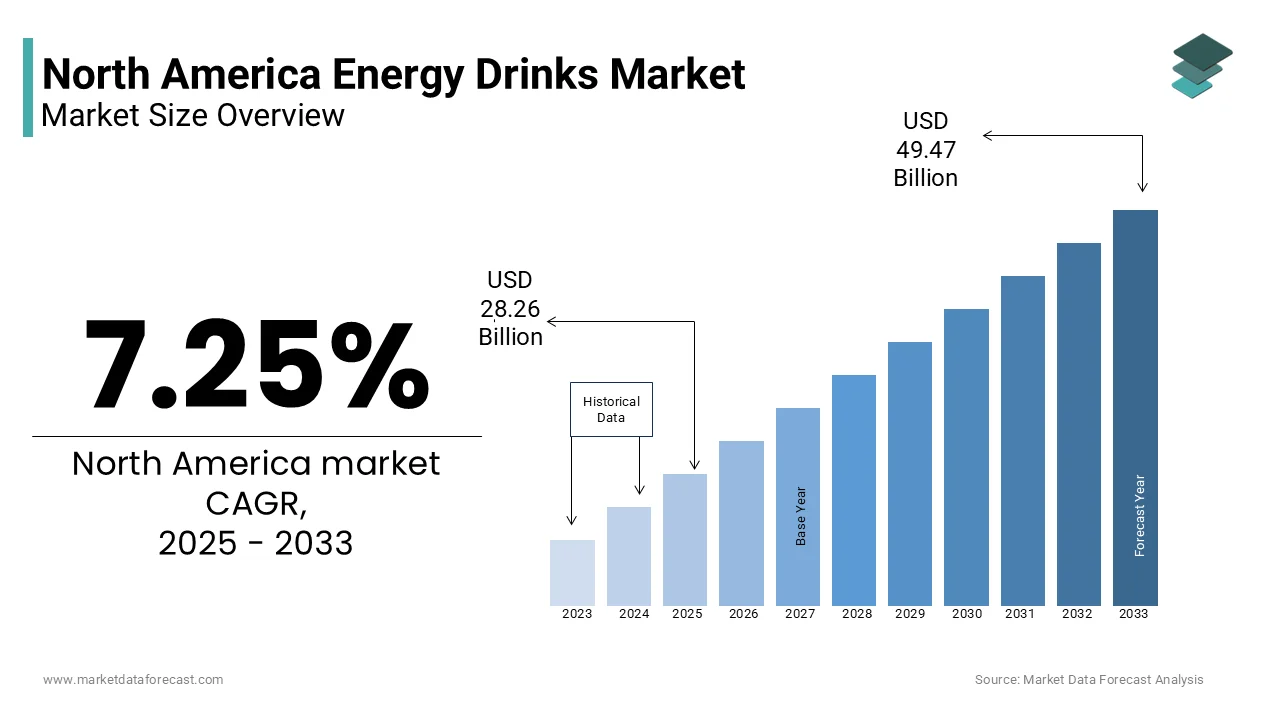

The North America energy drinks market was valued at USD 28.32 billion in 2025, is estimated to reach USD 30.37 billion in 2026, and is projected to reach USD 53.16 billion by 2034, growing at a CAGR of 7.25% during the forecast period. Market growth is driven by increasing consumer demand for functional beverages, rising need for instant energy and performance enhancement, and growing popularity among young adults and working professionals. The expansion of fitness culture, along with increasing product innovation in flavors and formulations, is further supporting market growth. In addition, strong marketing strategies and brand positioning are contributing to sustained demand across North America.

Key Market Trends

- Rising demand for functional and performance enhancing beverages is driving market growth.

- Increasing consumption among young adults and fitness enthusiasts is boosting demand.

- Growing innovation in flavors, ingredients, and formulations is supporting market expansion.

- Expansion of retail and e commerce channels is improving product availability.

- Rising focus on low sugar and health conscious formulations is influencing product development.

Segmental Insights

- Based on type, the hypertonic segment was the largest and held 53.5% of the North America energy drinks market share in 2025. This dominance is attributed to its high energy content and effectiveness in rapid energy replenishment.

- Based on ingredient type, the sweeteners segment accounted for 36.7% of the North America energy drinks market share in 2025. The segment’s growth is driven by the need to enhance taste and consumer appeal.

- Based on packaging, the cans segment dominated with 74.1% of the North America energy drinks market share in 2025, supported by convenience, portability, and strong branding opportunities.

Regional Insights

- The North America energy drinks market is experiencing strong growth across the region, supported by high consumption and product innovation.

- The United States was the largest contributor, accounting for 78.7% of the North America energy drinks market share in 2025, driven by strong consumer demand, extensive distribution networks, and presence of leading brands.

Competitive Landscape

The North America energy drinks market is highly competitive, with major players focusing on product innovation, marketing strategies, and expansion of distribution channels to strengthen their market position. Companies are investing in new product launches, healthier formulations, and brand collaborations. Prominent players in the North America energy drinks market include Red Bull, Monster Beverage Corporation, Rockstar Inc, Coca Cola, PepsiCo, Arizona Beverage Company, National Beverage Corp, Dr Pepper Snapple Group, Living Essentials, and Cloud 9.

North America Energy Drinks Market Size

The North American energy drinks market size was valued at USD 28.32 billion in 2025, and the market size is expected to reach USD 30.37 billion in 2026, to reach USD 53.16 billion by 2034, and is estimated to be growing at a CAGR of 7.25% from 2026 to 2034

The North America energy drinks market has evolved from a niche category targeting extreme sports enthusiasts to a mainstream staple consumed by students, professionals and athletes across the United States, Canada and Mexico. The market definition now extends beyond traditional carbonated formats to include functional shots, ready to drink coffee hybrids and natural energy alternatives derived from guarana or yerba mate. According to the Centers for Disease Control and Prevention, approximately 21% of 12th graders in the United States used energy drinks in the past year, highlighting their integration into daily dietary habits. The Food and Drug Administration mandates strict labeling requirements for caffeine content, which typically ranges from 80 to 300 milligrams per serving, influencing consumer choices and regulatory compliance. As per Statistics Canada, the prevalence of energy drink consumption among teenagers has risen significantly, prompting public health discussions regarding safety and moderation. The industry is characterized by intense innovation, with manufacturers focusing on sugar free variants and clean label ingredients to address health concerns. Consumer preferences are shifting towards products that offer sustained energy without the subsequent crash, driving demand for natural sweeteners and adaptogens. The market operates within a complex regulatory environment where health claims are scrutinized, ensuring that product formulations align with evolving nutritional guidelines and consumer expectations for transparency and efficacy.

MARKET DRIVERS

Pervasive Culture of High Performance and Extended Work Hours

The demanding nature of modern professional and academic environments in North America is majorly driving the growth of the North American energy drinks market. The prevalence of long working hours and the gig economy has created a workforce that frequently relies on chemical stimulation to maintain productivity and focus. According to the Bureau of Labor Statistics, the average private sector employee in the United States works approximately 34.2 hours per week, with many professionals exceeding this duration due to remote work boundaries and increased connectivity. This culture of constant availability drives the need for convenient and rapid sources of energy that can be consumed on the go. Energy drinks offer a portable solution that fits seamlessly into busy schedules, providing an immediate cognitive boost without the preparation time required for coffee. As per the National Sleep Foundation, nearly 44% of children across all age groups do not consistently get the amount of sleep recommended for their age, further exacerbating the reliance on stimulants to function effectively during the day. Students also contribute significantly to this demand, with the College Health Association noting that approximately 90% of university students in certain surveyed populations consume energy drinks to cope with academic pressure and late night study sessions. The psychological association between energy drinks and enhanced performance reinforces their utility in competitive environments. As the boundary between work and personal life continues to blur, the dependency on functional beverages to sustain energy levels throughout extended periods of activity remains a robust driver of market growth.

Expansion of Gaming, Esports and Digital Entertainment Industries

The rapid growth of the gaming and esports sectors in North America has emerged as a significant driver for the energy drinks market, which is also creating a symbiotic relationship between brands and digital communities. Professional gamers and streamers require sustained concentration and quick reflexes, making energy drinks an essential component of their routine. According to Newzoo, the PC and console games market in 2025 saw its first notable revenue growth since the pandemic, increasing 7% year over year with millions of engaged viewers who emulate the habits of their favorite players. Major energy drink companies have capitalized on this trend by sponsoring tournaments, teams and individual influencers, thereby embedding their products into the gaming culture. The International Esports Federation highlights that the average gaming session can last several hours, necessitating beverages that combat fatigue and maintain alertness. This demographic, particularly males aged 18 to 34, represents a highly loyal consumer base that values brand authenticity and community engagement. Marketing strategies often involve interactive digital campaigns and limited edition packaging featuring popular game franchises, which resonate strongly with this audience. The integration of energy drinks into gaming setups as a standard accessory has normalized their consumption beyond athletic contexts. As the esports industry continues to expand with increasing mainstream recognition, the demand for performance enhancing beverages among gamers and enthusiasts is expected to rise steadily. This cultural shift ensures a dedicated and growing segment of consumers who view energy drinks as integral to their digital lifestyle.

MARKET RESTRAINTS

Stringent Regulatory Scrutiny and Health Safety Concerns

Increasing regulatory scrutiny and rising awareness of potential health risks associated with excessive caffeine consumption are primarily impeding the expansion of the North American energy drinks market. Health authorities and consumer advocacy groups have raised alarms regarding the adverse effects of high stimulant intake, particularly among children and adolescents. According to the American Academy of Pediatrics, caffeine and other energy drink ingredients should not be consumed by children or adolescents due to potential impacts on developing cardiovascular and nervous systems. The Food and Drug Administration has issued warnings to manufacturers regarding unsafe additive levels and misleading health claims, leading to stricter compliance requirements. Several states and municipalities in the United States have proposed or enacted bans on the sale of energy drinks to minors, reflecting growing public concern. As per the Centers for Disease Control and Prevention, thousands of emergency room visits annually are related to energy drink consumption, often involving heart palpitations, anxiety and insomnia. These negative health associations damage brand reputation and deter cautious consumers from purchasing these products. Retailers face pressure to restrict sales or remove products from shelves to avoid liability issues. The threat of additional legislation, such as mandatory warning labels or taxation similar to sugary beverages, creates uncertainty for manufacturers. This regulatory environment forces companies to reformulate products and invest in extensive safety testing, increasing operational costs. Consequently, the market faces headwinds as public perception shifts towards viewing energy drinks as potentially hazardous rather than beneficial.

Consumer Shift Towards Natural and Clean Label Alternatives

The growing consumer preference for natural and clean label beverages is another substantial restraint to the North American energy drinks market, which is often perceived as artificial and overly processed. Modern shoppers are increasingly scrutinizing ingredient lists and avoiding synthetic additives, high fructose corn syrup and artificial colors commonly found in conventional energy drinks. According to the International Food Information Council, a significant portion of consumers actively try to limit or avoid sugars in their diet, driving demand for healthier alternatives. This trend has led to a surge in the popularity of natural energy sources such as green tea, matcha, yerba mate and coconut water, which are perceived as safer and more wholesome. The Hartman Group notes that transparency in sourcing and production is a key factor influencing purchase decisions, with consumers favoring brands that prioritize organic and non genetically modified ingredients. Traditional energy drink manufacturers struggle to shed their image of being unhealthy despite introducing sugar free variants. The perception that natural ingredients provide sustained energy without the jittery side effects of synthetic caffeine further erodes the appeal of conventional products. Retailers are allocating more shelf space to functional beverages that align with wellness trends, leaving less room for traditional energy drinks. This shift in consumer behavior forces established brands to compete with niche players who have built their identity around purity and health. Without significant reformulation and rebranding efforts, the traditional segment risks losing market relevance to these emerging natural alternatives.

MARKET OPPORTUNITIES

Innovation in Sugar Free and Keto Friendly Formulations

The rising prevalence of health conscious diets such as ketogenic, paleo and low carbohydrate regimes is a lucrative opportunity for the North America energy drinks market through the development of sugar free and keto friendly products. Consumers are actively seeking beverages that provide energy without spiking blood sugar levels or contributing to weight gain. According to the International Ketogenic Society, North America is expected to lead the keto diet products market, capturing a 38% share in 2026, driven by strong health and wellness trends and widespread adoption of the ketogenic diet. Energy drink manufacturers can capitalize on this trend by utilizing natural zero calorie sweeteners such as stevia, monk fruit and erythritol to create products that align with these dietary preferences. The success of brands that have pioneered sugar free variants demonstrates the strong demand for healthier options that do not compromise on taste or efficacy. Additionally, the inclusion of exogenous ketones or medium chain triglyceride oil in energy drinks can enhance their appeal to keto dieters by providing an alternative fuel source for the brain. Marketing these products as compatible with specific lifestyles allows companies to target niche but highly engaged consumer segments. Retailers are increasingly stocking these specialized products in health food sections, attracting shoppers who prioritize metabolic health. By expanding their portfolios to include clean label sugar free options, manufacturers can attract a broader demographic including fitness enthusiasts and diabetics. This strategic pivot not only mitigates health concerns but also opens new revenue streams in the growing wellness beverage sector.

Expansion into Functional Wellness and Adaptogenic Blends

The integration of functional ingredients such as adaptogens, nootropics and vitamins into energy drinks offers a significant opportunity for the North American energy drinks market. Consumers are increasingly looking for beverages that provide holistic health benefits beyond simple stimulation, such as stress reduction, improved focus and immune support. According to the Global Wellness Institute, the global wellness economy was valued at $5.6 trillion in 2022, with consumers willing to pay a premium for products that support mental and physical well being. Ingredients like ashwagandha, rhodiola rosea and L theanine are gaining popularity for their ability to modulate stress and enhance cognitive function without the jitteriness associated with high caffeine doses. Energy drink brands can leverage these trends by creating formulations that cater to specific needs, such as relaxation, clarity or immunity. The National Institutes of Health recognizes the potential of certain adaptogens in helping the body resist stressors, validating their inclusion in functional beverages. Collaborations with nutritionists and health experts can enhance credibility and educate consumers on the benefits of these advanced formulations. Retailers are eager to stock innovative products that stand out in crowded aisles, driving foot traffic and sales. This evolution transforms energy drinks from mere stimulants into comprehensive wellness tools appealing to a broader and more health conscious audience. By embracing functional innovation, manufacturers can command higher price points and foster brand loyalty among consumers seeking multifaceted health solutions.

MARKET CHALLENGES

Intense Market Saturation and Brand Differentiation Difficulties

The intense saturation with numerous established giants and emerging startups competing for shelf space and consumer attention is one of the notable challenges to the expansion of the North American energy drinks market. This overcrowded landscape makes it difficult for new entrants to gain visibility and for existing brands to maintain distinct identities. According to NielsenIQ, thousands of new beverage products are launched annually in the United States with a high failure rate due to lack of differentiation. Consumers are overwhelmed by choices, leading to brand switching behavior based on price, promotions or novelty rather than loyalty. Major players dominate distribution channels, making it challenging for smaller brands to secure retail placement without significant marketing investments. The similarity in product formulations and packaging designs further complicates differentiation, forcing companies to spend heavily on advertising and sponsorships. As per the Beverage Marketing Corporation, the volume growth of the energy drink category is slowing in mature markets, indicating saturation. This stagnation forces brands to engage in price wars, which erode profit margins and sustainability. Innovations are quickly copied by competitors, reducing the window of exclusivity for new products. The constant need to refresh branding and launch limited editions strains resources and can dilute brand equity. Navigating this crowded field requires strategic precision and substantial financial backing, which poses a significant barrier to growth and profitability for many participants in the market.

Volatility in Raw Material Costs and Supply Chain Disruptions

The energy drinks market in North America is vulnerable to fluctuations in the costs of key raw materials such as caffeine, sugar, aluminum and natural extracts, which pose a significant challenge to the regional market growth. Global supply chain disruptions, exacerbated by geopolitical tensions and climate change, have led to unpredictable pricing and availability of these inputs. According to the World Bank, the LME Aluminium cash price rose 12.3% to a multi-year high of $3,600 per tonne in April 2026, affecting production costs for beverage manufacturers. Aluminum tariffs and trade policies specifically impact the cost of cans, which are the primary packaging format for energy drinks. The Aluminum Association notes that price swings in metal markets directly influence manufacturing expenses, forcing companies to adjust pricing strategies or absorb costs. Additionally, the sourcing of natural ingredients like guarana and ginseng is subject to agricultural risks including weather events and crop failures. These supply side uncertainties complicate inventory management and financial planning for manufacturers. Passing increased costs to consumers is risky in a competitive market where price sensitivity is high. Companies must invest in diversified supply chains and hedging strategies to mitigate these risks, which require capital and expertise. Smaller players are particularly vulnerable to these shocks as they lack the bargaining power of larger corporations. Ensuring consistent product quality and availability amidst these challenges remains a persistent operational hurdle that threatens margin stability and market competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.25% |

| Segments Covered | By Type, Ingredient Type, Packaging, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The U.S., Canada and Rest of North America |

| Market Leaders Profiled | Red Bull, Monster Beverage Corporation, Rockstar Inc, Coca-Cola, PepsiCo, Arizona Beverage Company, National Beverage Corp, Dr.Pepper Snapple Group, Living Essentials and Cloud 9 |

SEGMENTAL ANALYSIS

By Type Insights

The hypertonic segment dominated the market by holding 53.5% of the global market share in 2025. The dominating spot of hypertonic segment in this market is primarily driven by the high concentration of carbohydrates and stimulants, which provide a rapid and substantial energy boost required for intense physical exertion and prolonged mental focus. Hypertonic drinks typically contain higher levels of sugar and caffeine compared to isotonic or hypotonic variants, making them the preferred choice for consumers seeking immediate performance enhancement. According to the American College of Sports Medicine, athletes often utilize hypertonic solutions before or during high intensity activities to maximize glycogen stores and sustain energy levels. The prevalence of competitive sports and rigorous fitness regimes in North America fuels the demand for these potent formulations. As per the National Sporting Goods Association, millions of Americans participate in high intensity training programs that necessitate significant caloric and stimulant intake. The psychological association between sweetness and energy further reinforces consumer preference for hypertonic options. Manufacturers formulate these drinks with complex carbohydrate blends and elevated caffeine levels to deliver instant alertness and stamina. Retailers prioritize these products due to their strong correlation with athletic performance and lifestyle branding. The effectiveness of hypertonic drinks in combating severe fatigue makes them indispensable for students, professionals and athletes alike. This functional efficacy ensures that the hypertonic segment remains the cornerstone of the energy drink industry in North America.

On the other hand, the hypotonic segment is estimated to showcase a CAGR of 9.2% over the forecast period in the North American market owing to the increasing consumer demand for lightweight hydration solutions that provide mild stimulation without the heaviness or caloric load of traditional energy drinks. Hypotonic drinks have lower concentrations of solutes than body fluids, allowing for faster absorption and rehydration, which appeals to health conscious consumers and endurance athletes. According to the International Society of Sports Nutrition, rapid fluid replacement is critical for maintaining performance and preventing dehydration during prolonged activity. The rise of wellness trends emphasizing clean hydration and minimal sugar intake has shifted preference towards hypotonic formulations. As per the Centers for Disease Control and Prevention, a high percentage of adults are trying to lose weight or maintain a healthy weight, driving demand for low calorie beverage options. Hypotonic energy drinks often utilize natural electrolytes and moderate caffeine levels to offer a balanced boost that supports both hydration and alertness. This dual benefit makes them attractive for daily consumption rather than just occasional use. Brands are innovating with added vitamins and minerals to enhance the functional profile of these lighter drinks. The versatility of hypotonic drinks for various activities from yoga to office work broadens their appeal. This alignment with holistic health and hydration needs ensures sustained growth for the segment.

By Ingredient Type Insights

The sweeteners segment led the market with 36.7% of the North American market share in 2025. The growth of the sweeteners segment in this regional market is attributed to the critical role sweeteners play in masking the bitter taste of caffeine and other functional ingredients while providing the necessary calories for immediate energy. Sugar and high intensity sweeteners are essential for creating the appealing flavor profiles that drive repeat purchases among consumers. According to the United States Department of Agriculture, sugarconsumption remains a significant part of the American diet, although trends are shifting towards reduced intake. Traditional energy drinks rely heavily on sucrose and high fructose corn syrup to deliver quick glucose spikes that complement the stimulant effect of caffeine. The sensory experience of sweetness is deeply ingrained in consumer preferences for beverages, making it a non negotiable component for mass market appeal. As per the International Food Information Council, taste remains the primary factor influencing food and beverage choices for over 80% of consumers. Even in sugar free variants, artificial and natural sweeteners such as sucralose, stevia and erythritol are crucial for maintaining palatability without adding calories. The formulation expertise required to balance sweetness with functionality gives this ingredient category strategic importance. Manufacturers invest heavily in sweetener technology to improve taste and reduce aftertastes. The ubiquity of sweeteners in both regular and diet formulations ensures their continued dominance in the market composition.

However, the water and additives segment is estimated to showcase a promising CAGR of 10.5% over the forecast period in the North American market owing to the increasing incorporation of functional additives such as electrolytes, amino acids, vitamins and nootropics into energy drink formulations. Consumers are seeking beverages that offer multifaceted health benefits beyond simple stimulation, leading to the rise of enhanced water based energy drinks. According to the Global Wellness Institute, the wellness economy is expanding rapidly with consumers prioritizing products that support hydration, immunity and cognitive function. Additives like taurine, L carnitine and B vitamins are being added in higher concentrations to differentiate products and justify premium pricing. The trend towards clean label products has also increased the use of natural additives derived from fruits and herbs. As per the Natural Products Association, sales of natural and organic products continue to grow, reflecting consumer demand for transparency and purity. Water serves as the base for these innovative formulations, allowing for the seamless integration of diverse functional ingredients. Manufacturers are leveraging advanced extraction technologies to preserve the efficacy of these additives. The ability to customize energy drinks for specific needs such as focus, recovery or relaxation drives innovation in this segment. This evolution from basic stimulants to comprehensive functional beverages ensures robust growth for water and additives.

By Packaging Insights

The cans segment led the market by capturing 74.1% of the regional market share in 2025. The growth of the cans segment in this regional market is attributed to the superior convenience, portability and protective qualities of aluminum cans, which are ideal for on the go consumption. Cans provide an effective barrier against light and oxygen that preserve the freshness and potency of energy drinks. According to the Aluminum Association, approximately 95% of the primary aluminum produced in the Middle East is exported, which underscores the global dependence on this material for packaging like beverage cans. The sleek and vibrant design possibilities of cans allow brands to create striking visual identities that stand out on retail shelves. Major energy drink companies leverage can packaging for limited edition releases and collaborations, enhancing brand engagement. As per the Beverage Marketing Corporation, single serve cans account for the majority of energy drink sales due to their suitability for impulse purchases. The lightweight nature of cans reduces transportation costs and carbon footprint compared to glass bottles. Retailers prefer cans for their stackability and efficient use of shelf space. The tactile experience of opening a cold can is also associated with refreshment and energy boosting rituals. This combination of functional benefits and marketing versatility ensures that cans remain the preferred packaging format for energy drinks in North America.

However, the bottles segment is predicted to witness a healthy CAGR of 8.2% over the forecast period in this regional market owing to the rising demand for premium and larger volume energy drinks that offer resealability and extended consumption opportunities. Plastic and glass bottles are increasingly used for high end energy beverages and hybrid products such as energy coffee blends. According to the Plastics Industry Association, the global recycled aluminum cans market is forecasted to grow from $4.09 billion in 2026 to $6.18 billion by 2035, reflecting a significant trend in sustainable packaging that includes bottled beverage materials. Resealable bottles allow consumers to pace their intake, which is appealing for longer work sessions or workouts. The transparency of bottles showcases the color and clarity of the liquid, enhancing perceived quality and naturalness. As per NielsenIQ, premium beverage sales have outpaced standard categories as consumers trade up for higher quality experiences. Bottles enable differentiated branding through unique shapes and labels that convey sophistication. The ability to include larger volumes such as 16 ounce or 20 ounce sizes caters to heavy users seeking value. Retailers are expanding their bottled energy drink sections to accommodate this growing segment. The versatility of bottles for both cold and ambient storage further supports their adoption. This shift towards premium and functional packaging formats ensures sustained growth for the bottle segment.

REGIONAL ANALYSIS

United States Energy Drinks Market Analysis

The United States dominated the energy drinks market in North America in 2025 with 78.7% of the regional market share. The dominance of the U.S. in the North American market can be credited to high consumption rates driven by a culture of productivity and fitness. According to the Centers for Disease Control and Prevention, energy drink consumption is prevalent among young adults who seek enhanced focus and energy. The presence of major global brands and numerous local startups creates a highly competitive landscape fostering continuous innovation. The trend towards sugar free and natural ingredients is reshaping product portfolios as health consciousness rises. Regulatory scrutiny regarding caffeine content and labeling is stringent, influencing formulation strategies. The robust retail infrastructure, including convenience stores, supermarkets and vending machines, ensures wide availability. E commerce platforms are also gaining traction, offering subscription models and exclusive products. The United States leads in marketing spend and sponsorships, particularly in esports and extreme sports. This dynamic environment supports steady market growth despite saturation in traditional segments. Innovation in functional ingredients and packaging continues to drive consumer interest. The market serves as a trendsetter for the rest of North America and globally.

Canada Energy Drinks Market Analysis

Canada occupied a significant position in the North America energy drinks market in 2025. The Canadian market status is mature, with a strong emphasis on health and safety regulations. According to Statistics Canada, participation in sports and physical activities is high, leading to consistent demand for energy and hydration products. Health Canada imposes strict limits on caffeine content and requires warning labels on high caffeine beverages, which influences consumer choices and product formulation. Consumers are increasingly opting for natural and organic energy drinks, reflecting a broader trend towards clean eating. The retail sector is dominated by major grocery chains and convenience stores that offer a wide variety of brands. Urban centers like Toronto and Vancouver are hubs for innovation and new product launches. The influence of American trends is significant but adapted to local preferences and regulatory requirements. Sustainability is a key concern, with consumers preferring recyclable packaging and eco friendly brands. The market is stable, with steady growth driven by health conscious innovations. Local brands are gaining traction by emphasizing transparency and quality. Canada remains a key market for premium and natural energy drink segments.

COMPETITIVE LANDSCAPE

The competition in the North America Energy Drinks Market is intense and characterized by the dominance of a few major players alongside numerous emerging niche brands. Large corporations leverage their extensive distribution networks and substantial marketing budgets to maintain market leadership. They compete on brand recognition product innovation and strategic partnerships with retailers. Smaller independent brands differentiate themselves through unique flavor profiles organic ingredients and targeted marketing to specific lifestyle communities. The market sees frequent product launches featuring functional benefits such as improved focus or relaxation. Price competition is prevalent particularly in the mass market segment prompting companies to offer value packs and promotions. Regulatory pressures regarding health claims and caffeine content influence competitive dynamics requiring strict compliance. Digital marketing and social media engagement are critical for building brand awareness and connecting with younger consumers. The rise of private label energy drinks from major retailers adds further pressure on established brands. Innovation in packaging sustainability and clean label formulations serves as a key differentiator. This dynamic environment requires continuous adaptation and strategic agility to sustain growth and profitability.

KEY MARKET PLAYERS

Some of the major players in the North American energy drinks market are

- Red Bull

- Monster Beverage Corporation

- Rockstar Inc

- Coca-Cola

- PepsiCo

- Arizona Beverage Company

- National Beverage Corp

- Dr Pepper Snapple Group

- Living Essentials

- Cloud 9

Top Players in the Market

- Monster Beverage Corporation is a dominant force in the North America Energy Drinks Market known for its extensive portfolio of high performance energy beverages. The company leverages strong brand recognition and aggressive marketing strategies to maintain its competitive edge. Recent actions include expanding its product line with zero sugar variants and functional energy drinks infused with vitamins and nootropics. Monster actively partners with major esports organizations and extreme sports events to engage with its core demographic. The company continues to invest in sustainable packaging initiatives such as increasing recycled content in cans. By focusing on innovation and strategic distribution alliances Monster strengthens its market position. Its ability to adapt to changing consumer preferences for healthier options ensures sustained relevance. The corporation also expands its global footprint through international partnerships reinforcing its status as a key industry leader driving growth and setting trends in the dynamic energy beverage sector.

- Red Bull GmbH is a pioneering brand in the energy drink sector with a significant presence in North America. The company is renowned for its unique marketing approach that associates the brand with high energy activities and extreme sports. Red Bull recently intensified its focus on organic and natural ingredient formulations to cater to health conscious consumers. The company invests heavily in event sponsorships including music festivals and athletic competitions to build brand loyalty. Red Bull also enhances its digital engagement through interactive content and social media campaigns. By maintaining premium pricing and exclusive distribution channels the company preserves its luxury image. Recent innovations include limited edition flavors and collaborations with artists. These strategies help Red Bull retain its leadership position despite intense competition. The brand's commitment to quality and lifestyle marketing continues to resonate with diverse consumer groups ensuring robust market performance and enduring influence in the North American beverage landscape.

- The Coca Cola Company plays a crucial role in the North America Energy Drinks Market through its diverse portfolio including Monster Energy and proprietary brands. The company leverages its unparalleled distribution network to ensure widespread availability of energy products across retail channels. Recent actions involve launching new caffeine infused beverages under established brands like Coca Cola Energy. The company focuses on sustainability by investing in recycling infrastructure and reducing plastic waste. Coca Cola also utilizes data analytics to understand consumer trends and tailor marketing efforts effectively. Strategic acquisitions and partnerships allow the company to innovate rapidly and respond to market demands. By integrating energy drinks into its broader beverage strategy Coca Cola captures various consumer segments. The company emphasizes convenience and accessibility making its products available in vending machines and convenience stores. This comprehensive approach strengthens its competitive position and drives continuous growth in the evolving energy drink category.

Top Strategies Used by the Key Market Participants

Key players in the North America Energy Drinks Market primarily focus on product diversification by introducing sugar free and natural ingredient variants to meet evolving health preferences. Companies invest heavily in experiential marketing and sponsorships of esports and extreme sports to build strong brand loyalty among younger demographics. Strategic partnerships with retail giants ensure prominent shelf placement and wide distribution coverage across urban and rural areas. Brands leverage digital platforms for direct consumer engagement and personalized marketing campaigns. Innovation in functional ingredients such as adaptogens and nootropics helps differentiate products in a saturated market. Sustainability initiatives including recyclable packaging and carbon neutral goals enhance corporate image and appeal to eco conscious consumers. Mergers and acquisitions allow larger corporations to expand portfolios and eliminate competition. These strategies collectively enable participants to navigate regulatory challenges and maintain competitiveness in a dynamic industry.

MARKET SEGMENTATION

This research report on the North American energy drinks market has been segmented and sub-segmented into the following categories.

By Type

- Isotonic

- Hypotonic

- Hypertonic

By Ingredient Type

- Water And Additives

- Sweeteners

- Flavors

- Acidulants

By Packaging

- Bottles

- Cans

By Country

- The United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What are energy drinks and how are they consumed in North America?

Energy drinks are functional beverages consumed to boost energy, alertness, and physical performance.

2. What factors are driving the North America energy drinks market growth?

Growth is driven by busy lifestyles, rising sports participation, and demand for convenient energy boosting drinks.

3. Which countries dominate the North America energy drinks market?

The United States leads the market, followed by Canada and Mexico with growing consumption.

4. What are the key ingredients in energy drinks?

Common ingredients include caffeine, taurine, B vitamins, guarana, and herbal extracts.

5. Which consumer groups drive demand for energy drinks?

Young adults, athletes, gamers, and working professionals are major consumer groups.

6. What distribution channels are important in the North America energy drinks market?

Convenience stores, supermarkets, online retail, and vending machines are key channels.

7. Is demand for sugar free energy drinks increasing?

Yes, sugar free and low calorie energy drinks are gaining popularity due to health concerns.

8. What role does branding play in the energy drinks market?

Strong branding, sponsorships, and influencer marketing significantly impact consumer choice.

9. Are natural and clean label energy drinks gaining traction?

Yes, demand for natural ingredients and clean label formulations is increasing.

10. What challenges does the North America energy drinks market face?

Health concerns, regulatory scrutiny, and intense market competition are key challenges.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com