Middle East Real Estate Market Size, Share, Trends, Forecast, Research Report By Property Type, Transaction Type, and Region (Brazil, Mexico, Argentina, Chile & Rest of Latin America) – Regional Industry 2026 to 2034

Middle East Real Estate Market Size

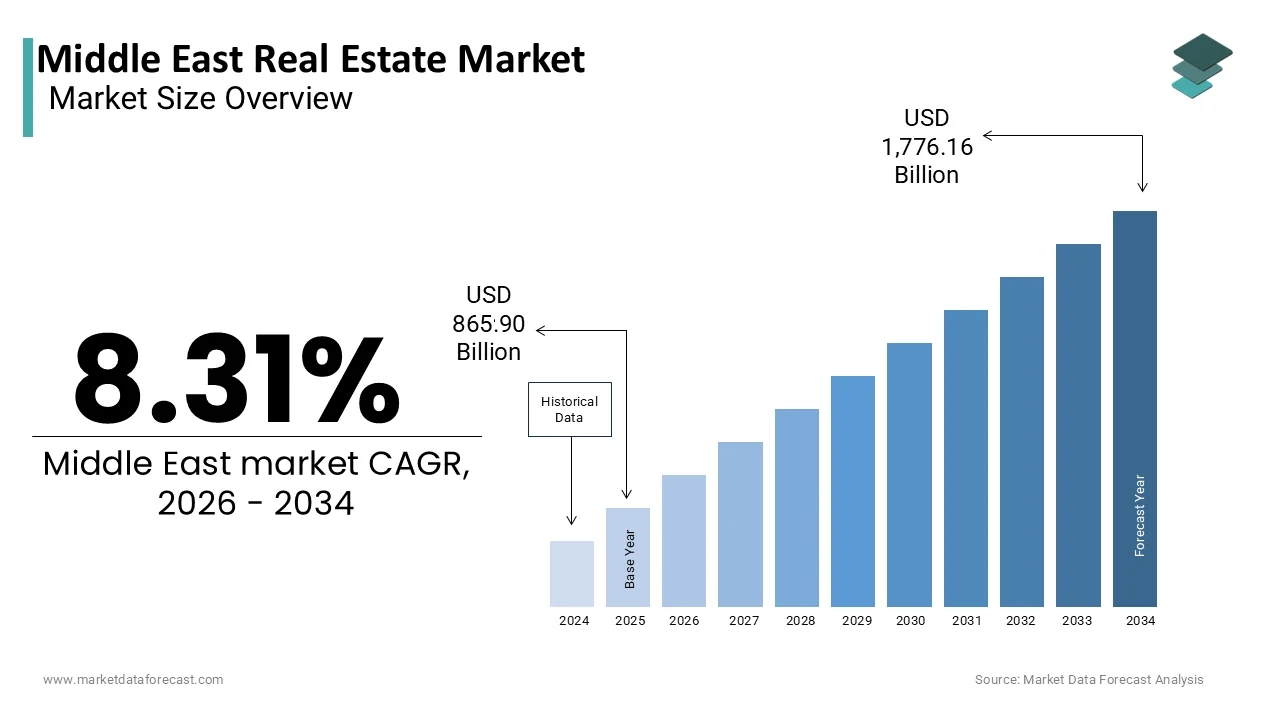

The Middle East real estate market was valued at USD 865.90 billion in 2025, is estimated to reach USD 937.85 billion in 2026, and is projected to reach USD 1,776.16 billion by 2034, growing at a CAGR of 8.31% from 2026 to 2034.

The real estate is a blend of luxury developments, smart city projects, and affordable housing initiatives. The region’s real estate landscape is being reshaped by government policies, urbanization trends, and foreign investment inflows. Countries like the United Arab Emirates, Saudi Arabia, and Qatar are leading this shift, leveraging Vision 2030-style strategies to attract both domestic and international capital. According to BMI Research (Fitch Solutions), real estate has become a cornerstone of economic diversification efforts across the Gulf Cooperation Council (GCC), with governments allocating substantial budgets toward infrastructure, mixed-use developments, and digital urban planning. The rise of mega-projects such as NEOM, Riyadh Season, and Expo City Dubai has further reinforced investor confidence, positioning the region as a global hub for commercial and residential real estate. Additionally, regulatory reforms, including long-term residency visas, property ownership rights for expatriates, and streamlined transaction processes,s have enhanced market accessibility.

MARKET DRIVERS

Government-Led Urbanization and Mega-Projects

The extensive pipeline of government-backed urban development and mega-infrastructure projects igeareded to drive the growth of the Middle East real estate market. These initiatives aim to accommodate rapid population growth, support economic diversification, and enhance living standards through modern, sustainable cities. In Saudi Arabia, Vision 2030 has spurred the creation of futuristic developments such as NEOM, Qiddiya, and the Red Sea Project, all of which require massive investments in residential, commercial, and hospitality real estate. According to the Saudi Ministry of Housing, over 700,000 housing units were either completed or under construction in 2023, which ireflectsthe scale of activity. Similarly, in the UAE, the Centennial 2071 strategy has led to major expansions in Dubai’s skyline and Abu Dhabi’s industrial zones, attracting both institutional and retail investors.

Rising Foreign Investment and Expatriate Demand

Foreign investment is also greatly influencing the growth of the real estate market in the Middle East. Governments have introduced favorable policies such as long-term residency visas, full ownership rights for non-nationals, and tax-free environments to attract overseas buyers. In 2023, the UAE launched the Golden Visa program by offering renewable ten-year residency permits to property investors who purchase properties valued at AED 2 million or more, as outlined by the General Directorate of Residency and Foreigners Affairs (GDRFA). This policy has significantly boosted demand from high-net-worth individuals from Europe, India, and China. According to Property Finder Middle East, over 18,000 expatriates purchased property in Dubai in 2023, which is marking a year-on-year increase of 35%.

MARKET RESTRAINTS

High Entry Barriers and Affordability Challenges

Property prices in these cities have risen sharply due to speculative investment, limited land availability, and high construction costs. According to Knight Frank’s Wealth Report 2023, Dubai ranks among the top 20 most expensive cities globally for prime residential property, with average prices reaching AED 2,800 per square foot. While government-led affordable housing programs have been introduced, such as the Saudi Ministry of Housing’s “Sakani” initiative, supply often fails to meet demand, especially for middle-income earners. In 2023, the Central Department of Statistics and Information (CDSI) in Saudi Arabia reported that nearly 60% of young adults under 35 were unable to afford homeownership without financial assistance. Additionally, financing constraints, including high down payment requirements and stringent mortgage eligibility criteria, further limit access to the market.

Regulatory Complexity and Policy Uncertainty

The inconsistency in legal frameworks and land registration procedures across different jurisdictions is also slowing down the growth of the Middle East real estate market. While some countries have made considerable progress in digitizing property transactions and streamlining ownership laws, others still grapple with bureaucratic inefficiencies, unclear title documentation, and overlapping jurisdictional responsibilities. According to the World Bank’s Doing Business Report 2023, several Middle Eastern economies rank below global averages in terms of ease of registering property, with lengthy approval times and complex legal hurdles discouraging both local and foreign investors. In Egypt, for instance, disputes over land ownership and unclear zoning regulations have delayed numerous large-scale developments.

MARKET OPPORTUNITIES

Smart Cities and Digital Infrastructure Integration

The rise of smart cities with technological innovation and government-backed digital transformation agendas is solely to create huge opportunities for the growth of the Middle East real estate market. Countries such as the UAE, Saudi Arabia, and Bahrain are investing heavily in intelligent urban ecosystems equipped with AI-powered traffic management, IoT-enabled buildings, and automated utilities. Projects like Dubai’s Smart City, Riyadh’s Smart District, and NEOM’s THE LINE are setting new benchmarks for sustainable, tech-integrated living environments.

Growth of Co-Living and Flexible Housing Models

The emergence of co-living spaces and flexible housing solutions is also expected to boost the growth of the Middle East real estate market in the coming years. Developers in the UAE, Qatar, and Saudi Arabia have begun introducing fully furnished, service-based residential complexes that offer shared amenities, short-term contracts, and community-driven experiences. According to Colliers International’s 2023 Middle East Residential Outlook, co-living occupancy rates in Dubai reached 92% in 2023, outperforming conventional apartments due to their convenience and affordability. In Riyadh, the launch of co-living towers near university campuses and business districts reflects a broader trend toward adaptable housing models. Additionally, the post-pandemic rise in remote work has fueled demand for hybrid living and working environments, which is prompting developers to incorporate flexible layouts and high-speed connectivity into new projects.

MARKET CHALLENGES

Environmental Constraints and Climate Adaptation Pressures

Environmental challenges pose a growing concern for the Middle East real estate market in relation to water scarcity, extreme heat, and desertification. The region’s arid climate necessitates high energy consumption for cooling and desalination, making sustainable building practices essential for long-term viability. According to the Arab Center for Research and Policy Studies, temperatures in parts of the Gulf have exceeded 50°C (122°F) in recent summers, placing additional strain on infrastructure and increasing operational costs for residential and commercial buildings. However, compliance with green building standards such as LEED and Estidama often results in higher upfront costs, potentially deterring smaller developers. In response, larger firms are investing in research and development to integrate climate-resilient technologies, including reflective surfaces, solar panels, and advanced insulation.

Overreliance on Speculative Investment and Market Volatility

The vulnerability to fluctuations with speculative investment rather than fundamental demand is posing risks to long-term stability, which additionally hinders the growth of the Middle East real estate market. In cities like Dubai and Riyadh, a significant portion of property purchases are made by investors seeking capital appreciation rather than end-users, creating potential bubbles if demand does not keep pace with supply. According to Knight Frank’s Prime Global Index 2023, Dubai’s prime property prices surged by 27% in 2023, outpacing income growth and raising concerns about affordability. Similarly, secondary markets in Saudi Arabia have seen rapid price increases following deregulation and marketing campaigns aimed at attracting foreign buyers. This speculative behavior can lead to imbalances in inventory levels, with completed but unsold units accumulating in certain areas.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Property Type, Transaction Type, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, Rethe restf GCC countries, andthe restt of the Middle East. |

| Market Leaders Profiled | Emaar Properties, United Development Company, Zara Investment Holdings, Taller Moustafa Group and several others, and others. |

SEGMENTAL ANALYSIS

By Property Type Insights

The residential real estate segment accounted in holding 45.3% of the Middle East real estate market share in 2025, owing to the rapid urbanization, population growth, and increasing demand for affordable and luxury housing across major cities like Dubai, Riyadh, and Doha. Governments have actively supported this sector through national housing strategies aimed at improving homeownership rates and reducing reliance on rental accommodations. In Saudi Arabia, the Ministry of Housing reported that over 700,000 new housing units were either completed or under construction in 2023, as part of Vision 2030's goal to increase homeownership from 47% to 70% by 2030. The UAE introduced long-term residency visas for property investors, encouraging foreign buyers to enter the market. The rise in remote work has also spurred demand for larger living spaces and suburban developments, which is further boosting residential real estate activity.

The industrial real estate segment is projected to expand with a CAGR of 9.6% in the coming years, with the region’s strategic shift toward economic diversification, particularly in logistics, manufacturing, and e-commerce. Countries such as the UAE and Saudi Arabia are investing heavily in industrial parks, free zones, and smart warehouses to support supply chain resilience and attract global businesses. For instance, the UAE’s National Strategy for Industry and Advanced Technology aims to increase the contribution of the industrial sector to GDP from 13% to 20% by 2031, as outlined by the Ministry of Industry and Advanced Technology. The expansion of ports, including Jebel Ali and Ras Al-Khair, has further stimulated demand for logistics facilities and cold storage units. Additionally, the growth of e-commerce platforms like Noon and Amazon's increased presence in the region has led to a surge in warehouse leasing, with vacancy rates dropping below 5% in key industrial hubs, according to JLL Middle East.

By Transaction Type Insights

The sales segment accounted in holding 58.2% of the Middle East real estate market share in 2025. This preference for outright property ownership is largely influenced by cultural attitudes toward asset accumulation, combined with favorable financing options and government-backed mortgage programs. In the UAE, the introduction of the Golden Visa scheme, which grants long-term residency to property buyers, has significantly boosted investor interest.

The lease segment is anticipated to grow with a CAGR of 11.2% in the coming years. Unlike traditional rentals, leasing arrangements in commercial and industrial properties are gaining traction due to their flexibility, tax advantages, and suitability for corporate tenants. In the UAE, the expansion of free zone entities and multinational corporations has led to a sharp increase in demand for long-term leased office spaces and retail units. The Dubai Multi Commodities Centre (DMCC) reported that over 5,000 new companies registered in 2023, many of which opted for flexible leasing models rather than purchasing premises outright.

REGIONAL ANALYSIS

Kingdom of Saudi Arabia (KSA)

Saudi Arabia was the largest contributor in the Middle East real estate market by holding 34.3% of the share in 2025. Vision 2030 has catalyzed the creation of futuristic cities such as NEOM, Qiddiya, and the Red Sea Project, all of which require massive investments in residential, commercial, and hospitality real estate. The Ministry of Housing reported that over 700,000 housing units were either completed or under construction in 2023, reflecting the scale of activity. Additionally, regulatory reforms such as the Privileged Residence Program and expanded mortgage financing have made property ownership more accessible to both citizens and expatriates. The government's emphasis on public-private partnerships has also encouraged private sector participation in large-scale developments.

United Arab Emirates (UAE)

The UAE was positioned second with 27.5% of the Middle East real estate market share in 2025. The country's real estate industry is anchored by Dubai and Abu Dhabi, which serve as global hubs for luxury property, commercial leasing, and mixed-use developments. The launch of the Golden Visa program, offering renewable ten-year residency permits to property investors who purchase properties valued at AED 2 million or more, has significantly boosted foreign buyer interest. In addition, Expo City Dubai, Meydan One Mall, and Palm Jebel Ali have reinforced the emirate’s reputation as a premier destination for high-end residential and commercial real estate. Meanwhile, Abu Dhabi has focused on expanding industrial zones and logistics hubs, attracting multinational corporations seeking strategic footholds in the region.

Egypt

Egypt's real estate market is expected to grow with a prominent CAGR during the forecast period. The country's real estate sector benefits from a rapidly growing population, rising urbanization rates, and government-led housing programs. The Ministry of Housing announced that over 700,000 affordable housing units were delivered in 2023, which is significantly boosting demand for residential properties. The Suez Canal Economic Zone (SCZone) and New Administrative Capital (NAC) projects are also driving commercial and industrial real estate development, attracting foreign direct investment from Chinese, Emirati, and European firms. According to JLL Middle East, Egyptian developers have increasingly adopted international design and sustainability standards, enhancing the competitiveness of new projects.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Emaar Properties, United Development Company, Zara Investment Holdings, Taller Moustafa Group, and several others are playinga dominantg role in the Middle East real estate market.

The Middle East real estate market is characterized by intense competition driven by a mix of government-backed entities, private developers, and international investors. While state-owned enterprises dominate large-scale infrastructure and housing initiatives, private developers are increasingly capturing niche segments such as luxury residences, co-living spaces, and industrial parks. The entry of global real estate giants into the region has further intensified rivalry, particularly in high-end markets like Dubai and Riyadh. Developers are differentiating themselves through design innovation, technological integration, and superior customer experience. Additionally, regulatory reforms allowing greater foreign ownership have diversified the investor base by encouraging more agile and dynamic market participation. The rise of fintech-enabled real estate platforms and digital property transactions has also disrupted traditional sales and leasing models, which is pushing companies to adopt digital-first strategies.

TOP PLAYERS IN THE MARKET

Emaar Properties (UAE)

Emaar Properties is a leading name in the Middle East real estate sector, known for developing iconic projects such as Burj Khalifa, Dubai Mall, and Downtown Dubai. The company has played a pivotal role in shaping modern urban landscapes across the UAE and beyond. Globally, Emaar is recognized for its integrated lifestyle developments that combine residential, retail, hospitality, and entertainment components. Its strategic partnerships with international architects, retailers, and technology firms have elevated the standard of luxury real estate not only in the region but also in global markets like Turkey, Egypt, and India.

ROSHN Group (Saudi Arabia)

ROSZN Group is one of the fastest-growing real estate developers in Saudi Arabia, playing a central role in the Kingdom’s Vision 2030 initiative to increase homeownership rates. The company focuses on large-scale residential communities that integrate smart living solutions, sustainability, and community-based amenities. It collaborates with international consultants and technology providers to enhance operational efficiency and improve housing affordability, positioning itself as a model for sustainable urban development in emerging markets.

Majid Al Futtaim (UAE)

While primarily known for its retail and shopping mall developments, Majid Al Futtaim is a major force in mixed-use real estate through projects like City Centre malls, Carillion residential communities, and hotel ventures. The company integrates retail, leisure, and residential spaces into cohesive urban environments that enhance lifestyle experiences. Globally, Majid Al Futtaim has expanded its footprint into Egypt, Oman, and Georgia, bringing its expertise in experiential real estate to new markets. Its focus on sustainability and customer-centric design has made it a benchmark for integrated real estate development worldwide.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Adoption of Smart and Sustainable Development Models

Leading real estate developers are increasingly integrating smart technologies and green building standards into their projects. This includes AI-driven property management systems, energy-efficient infrastructure, and water conservation mechanisms. These strategies align with regional sustainability goals and attract environmentally conscious buyers and investors.

Expansion into Mixed-Use and Integrated Communities

Developers are shifting from standalone buildings to fully integrated communities that combine residential, commercial, retail, and recreational elements. These ecosystems offer convenience, reduce commute times, and create long-term value, making them highly appealing to both residents and businesses seeking holistic living and working environments.

Strategic Partnerships and International Collaborations

Major players are forming alliances with global architecture firms, technology providers, and financial institutions to enhance project delivery, access cutting-edge innovations, and expand their market reach. These collaborations support knowledge transfer, risk mitigation, and brand elevation in competitive regional and international markets.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, Emaar Properties announced a partnership with a global architectural firm to develop a new line of AI-integrated residential towers in Dubai, aiming to redefine smart living standards and reinforce its dominance in tech-driven real estate.

- In July 2023, ROSZN Group launched a new housing initiative focused on expanding affordable family communities in Riyadh and Jeddah, which incorporates eco-friendly materials and renewable energy sources to align with national sustainability goals.

- In January 2025, Majid Al Futtaim unveiled a redevelopment plan for an existing retail hub in Abu Dhabi by transforming it into a mixed-use destination featuring residential units, wellness centers, and immersive entertainment zones to enhance consumer engagement.

- In October 2023, Dar Al Arkan, a leading Saudi developer, introduced a blockchain-based property management system for its premium villa communities, which is improving transparency and security for owners and tenants alike.

- In May 2025, Nakheel, a major Dubai-based developer, signed a strategic agreement with an international logistics provider to establish a dedicated distribution center within its upcoming Palm Jebel Ali residential complex by enhancing last-mile delivery capabilities for residents.

MARKET SEGMENTATION

This research report on the Middle East real estate market is segmented and sub-segmented into the following categories.

By Property Type

- Residential

- Commercial

- Industrial

- Land

- Others

By Transaction Type

- Sales

- Rental

- Lease

By Country

- KSA

- UAE

- Israel

- The rest of GCC countries and the rest of the Middle East

Frequently Asked Questions

1. What is driving the rapid expansion of the real estate sector in the Middle East?

Key drivers include population growth, urbanization, government infrastructure projects, and foreign investment inflows.

2. Which segments are witnessing the fastest growth in the Middle East real estate market?

Residential, commercial, and tourism-related real estate are experiencing robust growth, especially in smart cities and mixed-use developments.

3. What are the latest trends shaping the Middle East real estate sector?

Trends include smart buildings, sustainable construction, real estate digitization, and branded residential living.

4. Which countries are leading the real estate boom in the Middle East?

The UAE and Saudi Arabia are leading, driven by Vision 2030, mega projects, and regulatory reforms encouraging investment.

5. How is tourism contributing to real estate development in the region?

High tourist influx is boosting demand for hotels, resorts, vacation rentals, and retail complexes across major cities and heritage zones.

6. What investment opportunities are emerging in the Middle East real estate market?

Opportunities exist in luxury residences, logistics hubs, smart industrial parks, and green-certified developments.

7. How is technology influencing the real estate market in the Middle East?

Proptech adoption, digital property platforms, AI-driven valuations, and virtual tours are transforming the property buying experience.

8. What is the long-term outlook for the Middle East real estate market?

With favorable demographics, infrastructure investments, and smart city initiatives, the region's real estate market is poised for sustained growth through 2033.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com