Middle East And Africa Feed Additives Market Size, Share, Trends & Growth Forecast Report By Type, Livestock, and Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Rest of Middle East and Africa), Industry Analysis From 2025 To 2033

Middle East and Africa Feed Additives Market Size

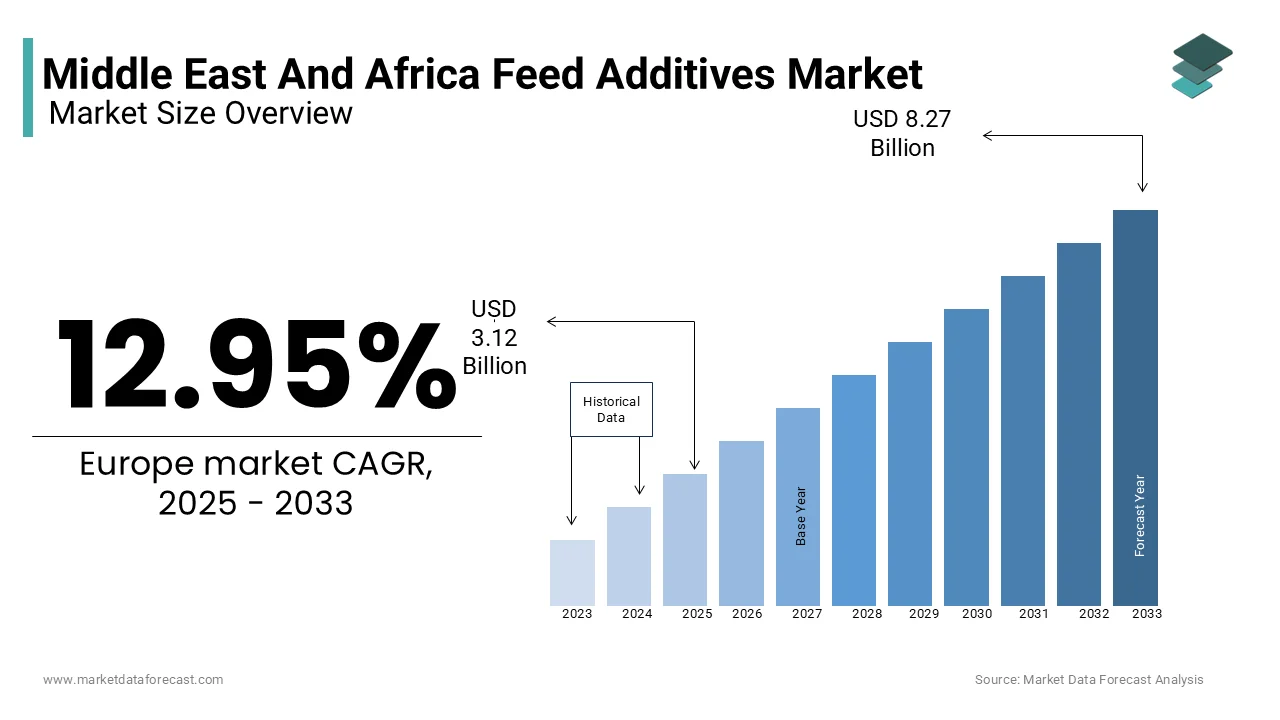

The feed additives market size in the Middle East and Africa was valued at USD 2.43 billion in 2024 and is anticipated to reach USD 2.53 billion in 2025 from USD 3.49 billion by 2033, growing at a compound annual growth rate (CAGR) of 4.1% from 2025 to 2033.

Feed additives include vitamins, amino acids, enzymes, and probiotics, are essential for optimizing animal performance, reducing disease risks, and meeting nutritional requirements. As per the Middle East Feed Manufacturers Association, feed additives are majorly utilized in poultry and ruminant diets, underscoring their importance in promoting sustainable livestock production. Additionally, advancements in biotechnology have improved product efficacy, reducing costs by 15%, as highlighted by the Egyptian Ministry of Agriculture. With increasing emphasis on reducing feed waste and greenhouse gas emissions, the market is evolving into a highly specialized sector, addressing both economic and ecological challenges while meeting the rising standards of modern agriculture.

MARKET DRIVERS

Rising Demand for High-Quality Animal Protein in Middle East and Africa

The growth of the Middle East and Africa feed additives market is primarily driven by the escalating demand for high-quality animal protein due to the population growth, urbanization, and changing dietary preferences. According to the Food and Agriculture Organization (FAO), the demand for meat, dairy, and eggs in the region is projected to grow by 30% by 2030 owing to the increasing disposable incomes and urban lifestyles. This trend is particularly evident in countries like Saudi Arabia and South Africa, where poultry farming accounts for over 40% of total livestock production, as reported by the Saudi Ministry of Environment, Water, and Agriculture. For instance, as per a study by the Egyptian National Research Centre, feed additive usage in poultry diets increased by 25% in 2022, driven by their ability to enhance nutrient absorption and reduce feed costs. Additionally, partnerships between feed manufacturers and biotech companies have reduced production costs by 20%, making these products more accessible. By ensuring consistent quality and enhancing productivity, feed additives have become indispensable for modern livestock farming, driving market growth across the region.

Stringent Regulations on Antibiotic Use in Livestock

The implementation of stringent regulations banning the use of antibiotics as growth promoters is further fuelling the growth of the Middle East and Africa feed additives market. According to the World Health Organization (WHO), over 60% of livestock farms in the region have transitioned to antibiotic-free solutions, driven by consumer demand for chemical-free meat and dairy products. This trend is particularly pronounced in Israel and Kenya, where government mandates have reduced antibiotic usage by 20%, as noted by the Israeli Ministry of Agriculture. As per a report by the South African Agricultural Research Council, feed additive sales surged by 18% in 2022 owing to the investments in high-efficiency formulations. Additionally, advancements in enzyme technologies have enhanced scalability, making them ideal for diverse applications. By addressing regulatory pressures and fostering ecological balance, feed additives are unlocking immense growth potential in this sector.

MARKET RESTRAINTS

High Costs of Production and Application

The high cost associated with production and application is a major restraint to the Middle East and Africa feed additives market. According to the Egyptian Ministry of Agriculture, the average cost of producing feed additives exceeds $300 per ton, creating financial barriers for rural producers. This issue is particularly pronounced in Sub-Saharan Africa, where over 60% of farmers lack access to advanced additive technologies, as reported by the Kenyan Ministry of Agriculture. As per a study by the South African Agricultural Research Council, only 35% of surveyed farms in rural areas have adopted feed additives, citing affordability as a major obstacle. Additionally, the absence of standardized pricing models exacerbates the problem, leaving many consumers uncertain about the value proposition of these products. Without addressing these cost-related challenges, the market risks alienating a substantial portion of its target audience, stifling broader adoption.

Limited Awareness Among Small-Scale Farmers

The limited awareness among small-scale farmers regarding the benefits and proper usage of feed additives is another significant restraint to the regional market expansion. According to the Ethiopian Ministry of Agriculture, over 50% of small-scale livestock farmers in East Africa lack technical knowledge about additive formulation and application techniques, leading to suboptimal outcomes despite investing in premium products. This issue is compounded by generational disparities, as highlighted by the Kenyan Ministry of Livestock Development, which reports that farmers aged 55 and above are 40% less likely to adopt new technologies compared to younger counterparts. Furthermore, a study by the University of Pretoria demonstrates that improper usage and maintenance practices can reduce feed additive efficacy by up to 30%, undermining their potential benefits. Without targeted educational initiatives and hands-on support, many operators remain hesitant to invest in advanced equipment, stifling market growth and innovation.

MARKET OPPORTUNITIES

Expansion into Aquaculture and Poultry Farming

The expansion into aquaculture and poultry farming that offer stable solutions for enhancing animal health and productivity in this region is a major opportunity for the Middle East and Africa feed additives market. According to the African Union’s Department of Fisheries, aquaculture production in Africa grew by 20% in 2022, with feed additives accounting for over 40% of nutritional supplements used in fish diets. This trend is particularly evident in Egypt and Nigeria, where tilapia and catfish farming dominate the industry, as noted by the Egyptian Ministry of Agriculture. For instance, a study by the South African Agricultural Research Council highlights that feed additive usage in aquaculture grew by 25% in recent years, driven by their ability to enhance protein digestibility and reduce feed costs. Additionally, partnerships between farmers and biotech companies have reduced production costs by 15%, making these products more accessible. By ensuring animal health and enhancing biodiversity, feed additives have become indispensable for modern aquaculture, driving market growth across the region.

Increasing Focus on Reducing Greenhouse Gas Emissions

The growing emphasis on reducing greenhouse gas emissions from livestock farming is another promising opportunity for the Middle East and Africa feed additives market. According to the United Nations Framework Convention on Climate Change, over 60% of livestock farms in the Middle East and Africa are exploring additive-based solutions to reduce methane emissions, driven by government incentives for green practices. A study by the Ethiopian Ministry of Environment highlights that the adoption of feed additives in ruminant diets achieved a 30% reduction in methane emissions in 2022, addressing environmental concerns. This trend is further bolstered by consumer preferences for environmentally responsible products, as noted by the South African Agricultural Research Council. Additionally, advancements in additive formulations enhance scalability, making them ideal for diverse applications. By leveraging these opportunities, companies can capitalize on the growing demand for sustainable solutions, solidifying their position in the market.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Shortages

The ongoing supply chain disruptions and raw material shortages is a major challenge to the Middle East and Africa feed additives market. According to the Middle East Feed Manufacturers Association, global shortages of key raw materials, such as amino acids and microbial strains, led to a 15% decline in feed additive production capacity in 2022, affecting manufacturers across the region. This issue is particularly pronounced in Saudi Arabia, where over 60% of production plants experienced delays due to logistical bottlenecks, as reported by the Saudi Ministry of Industry and Mineral Resources. A study by the South African Agricultural Research Council highlights that 40% of surveyed businesses faced extended lead times for new inventory orders, undermining their ability to meet rising consumer demand. Additionally, the rising costs of raw materials, such as bio-based feedstocks, have increased production expenses by 25%, further straining profitability. Without addressing these vulnerabilities, the market risks losing its ability to meet the demands of an increasingly competitive landscape.

Limited Infrastructure for Large-Scale Production

The limited availability of robust infrastructure required for large-scale production and distribution of feed additives is another major challenge to the regional market growth. According to the African Union’s Department of Agriculture, less than 10% of African feed additive plants are equipped to handle biological inputs, primarily due to inconsistent investment in biotech facilities. This issue is compounded by the absence of standardized production protocols, as highlighted by the Kenyan Ministry of Livestock Development, which notes that improper handling often results in material losses of up to 40%. Furthermore, a report by the Ethiopian Ministry of Agriculture underscores that inadequate investments in processing technologies have left many facilities ill-equipped to handle large volumes. For instance, the South African Agricultural Research Council estimates that only 25% of fermentation plants are capable of producing high-quality feed additives efficiently. Without scaling up infrastructure capabilities, the market risks exacerbating environmental concerns and missing opportunities to recover valuable resources.

SEGMENTAL ANALYSIS

Middle East and Africa Feed Additives Market by Livestock

The poultry segment had the leading share of 45.4% of the Middle East and Africa feed additives market in 2024. The domination of poultry segment in the Middle East and African market is driven by the widespread consumption of poultry products, particularly chicken meat and eggs, which are affordable and culturally preferred protein sources across the region. The Food and Agriculture Organization (FAO) reports that poultry accounts for over 60% of total meat production in countries like Egypt and South Africa, creating significant demand for feed additives to enhance productivity. A study published in Poultry Science highlights that feed additives improve feed conversion ratios by up to 20%, reducing production costs for farmers. Additionally, the growing trend of large-scale poultry farming is also fuelling the additive usage to ensure rapid growth and high-quality meat. For instance, companies like DSM Nutritional Products have developed specialized vitamin and mineral formulations tailored for broiler chickens, ensuring optimal health and performance. With the region prioritizing affordable protein sources, poultry remains central to the feed additives market.

The aquatic animals segment is growing rapidly and is expected to witness a CAGR of 10.88% over the forecast period due to the increasing demand for fish and seafood, particularly in coastal regions like Morocco and Kenya. A report by the African Development Bank states that aquaculture production has grown by 15% annually, driven by urbanization and rising consumer incomes. Feed additives play a critical role in improving growth rates and immunity in farmed fish, with studies showing a 30% reduction in mortality rates, as noted in Aquaculture Economics & Management . For example, brands like BASF incorporate amino acids and enzymes to enhance nutrient absorption in tilapia and catfish. Additionally, the push for sustainable aquaculture practices has fuelled the demand for eco-friendly additives. As the region accelerates its transition to sustainable food systems, aquatic animals emerge as a transformative segment driving innovation in feed additive applications.

Middle East and Africa Feed Additives Market by Type

The vitamins and minerals segment held the leading share of 36.3% of the Middle East and African market share in 2024. The essential role that vitamins and minerals play in maintaining animal health and productivity, particularly in regions with nutrient-deficient soils is driving the domination of the segment in this regional market. The International Feed Industry Federation (IFIF) highlights that vitamins and minerals account for over 40% of all feed additive usage, ensuring balanced nutrition for livestock. A study in Animal Nutrition notes that vitamin supplementation improves immune response by up to 25%, reducing disease outbreaks in poultry and ruminants. Additionally, the rising cost of raw materials is fuelling the demand for synthetic vitamins like A, D3, and E. For instance, companies like Evonik Industries optimize mineral formulations to meet the specific needs of dairy cattle, enhancing milk yield by up to 15%. With governments prioritizing food security and livestock health, vitamins and minerals remain pivotal in fostering efficient and resilient agricultural systems.

The enzymes segment is the fastest growing segment in the Middle East and Africa feed additives market and is predicted to grow at a CAGR of 13.1% over the forecast period. The ability of enzymes to enhance nutrient digestibility and reduce feed costs, particularly in poultry and aquaculture is propelling the growth of the enzymes segment in this regional market. A report by the African Union’s Department of Agriculture states that enzyme usage has surged by 20% annually, driven by the adoption of non-conventional feed ingredients like maize and cassava. For example, brands like Novozymes utilize carbohydrase and protease to break down complex nutrients, improving feed efficiency by up to 30%. Additionally, the rise of precision feeding is increasing the demand for tailored enzyme solutions. A study in Aquaculture Research highlights that enzymes reduce phosphorus excretion by 40%, aligning with sustainability goals. As the region intensifies efforts to combat food insecurity under initiatives like CAADP, enzymes emerge as a transformative solution for sustainable animal nutrition.

Middle East and Africa Feed Additives Market by Form

The dry feed additives segment led the market by holding the leading share of the Middle East and African market in 2024. The long shelf life and ease of storage of dry feed additives is making them ideal for large-scale agricultural operations in hot and arid climates, which is one of the key factors driving the segmental growth in this regional market. The African Feed Manufacturers Association (AFMA) highlights that dry additives account for over 70% of all feed supplement usage due to their stability during transportation and storage. A study published in Journal of Applied Animal Research notes that dry forms retain their efficacy for up to two years, ensuring consistent performance in feed formulations. Additionally, the growing trend of small-scale farming has increased demand for standardized and accessible additives. For instance, companies like Adisseo optimize dry vitamin and mineral blends to meet the nutritional needs of diverse livestock species. With the region prioritizing scalable and efficient feed solutions, dry additives remain central to the market landscape.

The liquid feed additives segment is estimated to register the fastest CAGR of 9.7% over the forecast period. The rapid absorption and ease of application, particularly in intensive farming systems like poultry and swine is primarily boosting the growth of the liquid segment in the Middle East and African market. A report by the International Livestock Research Institute (ILRI) states that liquid additives improve nutrient bioavailability by up to 40%, making them ideal for high-value livestock. For example, brands like Alltech utilize liquid acidifiers to enhance gut health and reduce pathogen colonization in broiler chickens. Additionally, the rise of automated feeding systems is increasing the demand for liquid additives that integrate seamlessly with modern equipment. A study in Livestock Science highlights that liquid forms reduce feed wastage by 15%, appealing to cost-conscious farmers. As the region embraces technological advancements in agriculture, liquid additives emerge as a key enabler of efficient and precise animal nutrition.

Middle East and Africa Feed Additives Market by Source

The synthetic feed additives segment accounted for the major share of the Middle East and African market in 2024 due to their cost-effectiveness and consistency, making them ideal for large-scale industrial farming operations. The European Chemical Industry Council (CEFIC) highlights that synthetic additives account for over 70% of all feed supplements used in livestock farming, ensuring uniform nutrient delivery. A study published in Industrial Biotechnology notes that synthetic vitamins and amino acids reduce production costs by up to 30%, making them accessible for budget-constrained farmers. Additionally, the growing trend of precision agriculture is promoting the demand for standardized synthetic formulations. For instance, companies like BASF produce synthetic methionine, which enhances growth rates in poultry by up to 20%. With the region prioritizing affordable and scalable feed solutions, synthetic additives remain pivotal in fostering efficient livestock systems.

The natural feed additives segment is predicted to grow at a CAGR of 11.7% over the forecast period in this regional market. The growing demand for organic and antibiotic-free animal products, particularly in urban markets is majorly boosting the growth of the natural segment in this regional market. A report by the African Organic Agriculture Network states that natural additives, such as plant extracts and probiotics, reduce dependency on synthetic chemicals by up to 25%, aligning with consumer preferences for eco-friendly farming practices. For example, brands like Chr. Hansen utilize natural probiotics to improve gut health and immunity in livestock, reducing mortality rates by 15%. A study in Sustainable Agriculture Research highlights that natural additives improve soil health by reducing chemical runoff by 40%. As the region intensifies efforts to combat climate change, natural additives emerge as a transformative solution for sustainable animal nutrition.

COUNTRY ANALYSIS

Top 5 Leading Countries in the Middle East and Africa Feed Additives Market

Saudi Arabia is a dominant player in the Middle East and Africa feed additive market. The significant investment in its agricultural sector of Saudi Arabia that is driven by Vision 2030, aims to enhance food security and reduce dependency on imports. According to the Saudi Ministry of Environment, Water, and Agriculture, the livestock sector is projected to grow at a CAGR of 5.5% from 2021 to 2025, highlighting the increasing demand for high-quality feed additives. The rise in poultry production, which reached over 1.2 million tons in 2020, further fuels the need for feed additives that improve growth rates and feed efficiency. Additionally, the government's initiatives to promote sustainable farming practices and animal welfare standards are expected to drive the adoption of innovative feed solutions, positioning KSA as a leader in the region.

The UAE holds a significant share of the Middle East and Africa feed additive market. The strategic location of the UAE as a trade hub and its growing population have led to increased demand for livestock products, particularly poultry and dairy. The UAE's Ministry of Climate Change and Environment reported that the livestock sector is expected to grow by 4% annually, emphasizing the need for efficient feed solutions. The rising trend of urban farming and the government's support for sustainable agricultural practices have further propelled the use of feed additives. Additionally, the UAE's focus on food security, especially in light of the COVID-19 pandemic, has led to increased investments in the agricultural sector. The presence of key players like Al Ain Farms and Emirates Feed Factory enhances competition and innovation, driving the market forward.

South Africa is also a key player in the feed additive market in this region. The country's well-established livestock industry, particularly in poultry and beef production, is a major driver of demand for feed additives. According to the South African Poultry Association, the poultry sector alone contributes over R50 billion to the economy, highlighting its significance. The increasing focus on improving feed efficiency and animal health has led to a growing adoption of feed additives, which are essential for enhancing productivity. Furthermore, South Africa's diverse agricultural landscape and favorable climate conditions support the growth of the livestock sector. The presence of major companies like Afgri and Cargill in the market fosters innovation and the development of tailored feed solutions, further driving market growth.

Egypt holds a notable share of the Middle East and Africa feed additive market, driven by its large population and growing demand for animal protein. The Egyptian Ministry of Agriculture reported that the livestock sector is a vital component of the national economy, contributing around EGP 100 billion annually. The increasing focus on food security and self-sufficiency has led to a surge in poultry and dairy production, necessitating the use of high-quality feed additives. Additionally, the government's initiatives to modernize the agricultural sector and improve livestock health standards are expected to drive the adoption of innovative feed solutions. The presence of local companies like El-Wahy and international players such as Alltech enhances competition and innovation in the market, positioning Egypt as a significant contributor to the regional feed additive landscape.

Kenya is predicted to grow at a steady CAGR in the feed additive market in the Middle East and Africa, with a rapidly growing livestock sector that includes cattle, poultry, and goats. The Kenya National Bureau of Statistics reported that the agricultural sector contributes about 33% of the country's GDP, with livestock playing a crucial role. The increasing demand for meat and dairy products, driven by a growing middle class, has led to a heightened focus on improving feed quality and animal health. The adoption of feed additives is seen as a key strategy to enhance productivity and profitability in the livestock sector. Furthermore, the government's support for sustainable agricultural practices and initiatives to improve food security are expected to drive further growth in the feed additive market. The presence of local companies and international players fosters competition and innovation, positioning Kenya as an emerging leader in the region.

KEY MARKET PLAYERS

Some of the key players in the Middle East and Africa Feed Additives market are Adisseo Asia-Pacific Pte Ltd, Cargill Asia-Pacific Holdings Pte Limited, DuPont Asia-Pacific, Ltd., Novozymes (China) Investment Co., Ltd., Evonik (SEA) Pte. Ltd., BASF Asia-Pacific, DSM Dyneema, Lonza Biologics Tuas Pte Ltd, ADM (Shanghai) Management Company, Chr. Hansen (Beijing) Trading Co., Ltd.

MARKET SEGMENTATION

This market research report on the Middle East and Africa feed additives market is segmented and sub-segmented into the following categories.

By Livestock

- Ruminants

- Dairy

- Beef

- Calf

- Goats

- Sheep

- Poultry

- Broilers

- Layers and breeders

- Swine

- Aquatic animal

- Others, such as equine and pets

By Type

- Vitamins and minerals

- Acidifiers

- Amino acids

- Phosphates

- Carotenoids

- Enzymes

- Mycotoxin detoxifiers

- Flavors & sweeteners

- Antioxidants

- Others

By Form

- Dry

- Liquid

By Source

- Natural

- Synthetic

By Country

- KSA

- UAE

- Israel

- rest of GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA

Frequently Asked Questions

What Is The Expected Growth Rate of The MEA Feed Additives Market?

The Middle East and Africa feed additives market is expected to reach at a compound annual growth rate (CAGR) of 5.2% during the forecast period from 2025 to 2033.

What Are The Dominating Factors In MEA Feed Additives Market?

The vitamins and minerals segment holds the major share of the market in terms of volume, as they are essential for sustaining and improving the health of livestock.

What Are The Key Market Players Involved In MEA Feed Additives Market?

Some of the key players in the Middle East and Africa Feed Additives market are Adisseo Asia-Pacific Pte Ltd, Cargill Asia-Pacific Holdings Pte Limited, DuPont Asia-Pacific, Ltd., Novozymes (China) Investment Co., Ltd., Evonik (SEA) Pte. Ltd., BASF Asia-Pacific, DSM Dyneema, Lonza Biologics Tuas Pte Ltd, ADM (Shanghai) Management Company, Chr. Hansen (Beijing) Trading Co., Ltd. They are playing a dominant role in the Middle East and Africa feed additives market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]