Global Micro Data Center Market Size, Share, Trends, & Growth Forecast Report – Segmented By Application (Instant Data Center, Remote Office, And Branch Office And Edge Computing), Rack Unit (Up To 20 RU, 20 RU To 40 RU And Above 40 RU), Organization Size (Small And Medium-Sized Enterprises And Large Enterprises), Verticals (IT And Telecommunication, BFSI, Media And Entertainment, Healthcare, Government And Defence, Retail, Manufacturing, And Others) and Regional - (2024 to 2032)

Global Micro Data Center Market Size (2024 to 2032)

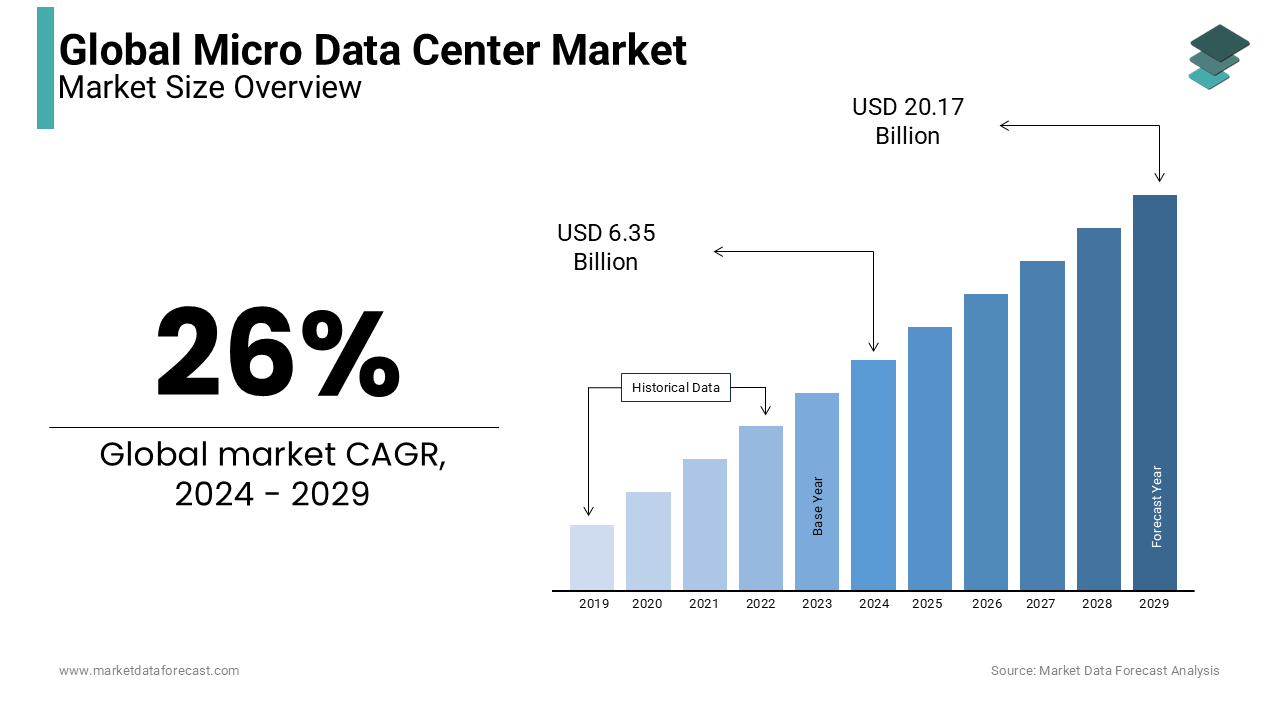

The global micro data center market was worth USD 5.04 billion in 2023. The global market is predicted to reach USD 6.35 billion in 2024 and USD 40.34 billion by 2032, growing at a CAGR of 26% during the forecast period.

The micro data center is nothing but a self-contained infrastructural design that was achieved by integrating the storage, processing, and networking modules that are required to run indoor as well as outdoor applications in a secure computing environment, whereas these micro data centers are available in standardized prefabricated sizes that enable the data center owners to save their capital investment and the time needed in building those data centers by the traditional approach in which the size and flexibility features of the micro data centers make them ideal for use in some of the applications such as instant data centers, remote office and branch office and also edge computing.

MARKET DRIVERS

The growing demand for high-performing, energy-efficient, cost-effective data center solutions is expected to play an essential role in the growth of the micro data center market across the globe.

Another factor is the growing demand for edge micro data centers in several industry verticals, which influence the growth of the Micro Data Center market during the forecast period. Deployment and commercialization of 5g network connectivity in the Europe region and North America and the rise in the number of SMEs in the Asia Pacific region are some of the major driving factors that promote the growth of the revenue rate of the Micro Data Center market during the forecast period. Furthermore, the flourishing telecommunication sector in South America and the rise in urbanization and digitalization in MEA are other major growth-supporting factors in the Micro Data Center market.

MARKET RESTRAINTS

Lack of awareness is one of the important barriers to market growth. Challenges in implementing high-performance computing act as an important deterrent to the growth of the Micro Data Center market. Monitoring and management challenges at remote locations are also major restraints that hinder the growth of the microdata center market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024 to 2032 |

|

CAGR |

26% |

|

Segments Covered |

By Application, Rack Unit, Organization Size, Verticals, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Eaton Corporation, Hewlett Packard Enterprise, Huawei Technologies Limited, IBM Corporation, Edgemicro, EdgePresence, NVIDIA Corporation, Smart Edge Data Centers Limited, Panduit Corporation, Rittal GmbH & Co. Kg, Schneider Electric SE, Vertiv Co., Attom Technology, and Others. |

SEGMENTAL ANALYSIS

Global Micro Data Center Market Analysis By Application

The Micro Data Center Market is divided into the instant data centers, remote offices, and branch offices, and edge computing. The edge computing segment held the prominent share and is predicted to remain at the forefront throughout the forecast period due to the accelerated demand for instantaneous. Access to data anytime and anywhere, these edge computing and micro data centers are becoming more abundant and also increasingly vulnerable. This application also has the potential to prevent such issues from arising as the physical infrastructure, which is located to the source data.

Global Micro Data Center Market Analysis By Rack Unit

The Micro Data Center Market is divided into up to 20 RU, 20 RU to 40 RU, and above 40 RU. The 20 RU to 40 RU segment holds the major share of the market, and this segment is expected to hold dominance during the forecast period.

Global Micro Data Center Market Analysis By Organization Size

The Micro Data Center Market is divided into small and medium-sized enterprises and large enterprises. Among these segments, the large-sized enterprises segment held the prominent share, and it is predicted to remain at the forefront in the upcoming years since these enterprises face various issues related to higher power consumption and higher carbon footprint.

Global Micro Data Center Market Analysis By Verticals

The Micro Data Center Market is divided into IT and telecommunication, BFSI, media and entertainment, healthcare, government and defense, retail, manufacturing, and other verticals such as energy, education, transportation, and logistics. The BFSI segment holds the major share of the market and is expected to hold the dominance during the forecast period.

REGIONAL ANALYSIS

The Asia Pacific region holds a prominent share of the market due to factors such as the rising adoption of advanced technologies such as the Internet of Things and edge computing. The region is expected to hold the dominance during the forecast period. North America is also expected to increase market growth due to the growing demand for edge micro data centers in several industry verticals. Europe is also expected to increase its market value in the upcoming years, followed by the Asia Pacific region and North America region. Latin America is likely to have steady growth opportunities in the foreseen years. The Middle East and Africa are projected to have a slow growth rate during the forecast period.

KEY PARTICIPANTS IN THE GLOBAL MICRO DATA CENTER MARKET

The major companies operating in the global micro data center market include Eaton Corporation, Hewlett Packard Enterprise, Huawei Technologies Limited, IBM Corporation, Edgemicro, EdgePresence, NVIDIA Corporation, Smart Edge Data Centers Limited, Panduit Corporation, Rittal GmbH & Co. Kg, Schneider Electric SE, Vertiv Co., and Attom Technology.

RECENT HAPPENINGS IN THE GLOBAL MICRO DATA CENTER MARKET

-

Schneider Electric launched a cooling solution for edge and micro data centers in March 2020. This new solution aims to make cooling more efficient and ultimately reduce operational costs.

-

Vertiv company has introduced a new software named Vertiv Environet Alert, which brings enterprise-level infrastructure monitoring and management capabilities to micro data centers and edge facilities.

DETAILED SEGMENTATION OF THE GLOBAL MICRO DATA CENTER MARKET INCLUDED IN THIS REPORT

This research report on the global micro data center market is segmented and sub-segmented based on application, rack unit, organization size, verticals, and region.

By Application

-

Instant Data Center

-

Remote Office And Branch Office

-

Edge Computing

By Rack Unit

-

Up to 20 RU

-

20 RU to 40 RU

-

Above 40 RU

By Organization Size

-

Small And Medium-Sized Enterprises

-

Large Enterprises

By Verticals

-

IT and Telecommunication

-

BFSI

-

Media And Entertainment

-

Healthcare

-

Government And Defense

-

Retail

-

Manufacturing

-

Others

By Region

-

North America

-

The United States

-

Canada

-

Rest of North America

-

-

Europe

-

The United Kingdom

-

Spain

-

Germany

-

Italy

-

France

-

Rest of Europe

-

-

The Asia Pacific

-

India

-

Japan

-

China

-

Australia

-

Singapore

-

Malaysia

-

South Korea

-

New Zealand

-

Southeast Asia

-

-

Latin America

-

Brazil

-

Argentina

-

Mexico

-

Rest of LATAM

-

-

The Middle East and Africa

-

Saudi Arabia

-

UAE

-

Lebanon

-

Jordan

-

Cyprus

-

Frequently Asked Questions

How does the adoption of edge computing impact the Micro Data Center market?

The adoption of edge computing, which involves processing data closer to the source of generation, is driving the demand for Micro Data Centers. These facilities enable organizations to deploy computing resources at the edge of the network, reducing latency and improving the performance of applications and services.

What role do modular Micro Data Center solutions play in the market?

Modular Micro Data Center solutions offer scalability and flexibility, allowing organizations to expand their computing infrastructure as needed. These pre-engineered units can be quickly deployed in remote or temporary locations, making them ideal for edge computing applications and rapid deployment scenarios.

What are the sustainability implications of Micro Data Centers?

Micro Data Centers can contribute to sustainability efforts by optimizing energy efficiency and reducing carbon emissions. By deploying energy-efficient hardware, implementing advanced cooling techniques, and leveraging renewable energy sources, organizations can minimize their environmental footprint while supporting their computing needs.

How do regional regulations and compliance requirements affect the deployment of Micro Data Centers?

Regional regulations and compliance requirements vary across different geographies, impacting the design, deployment, and operation of Micro Data Centers. Organizations must ensure that their infrastructure meets local data protection laws, industry standards, and regulatory mandates to avoid legal and financial risks.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]