Global Medical Foods Market Size, Share, Trends & Growth Forecast Report By Route of Administration, Product, Application, Sales Channel and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Medical Foods Market Size

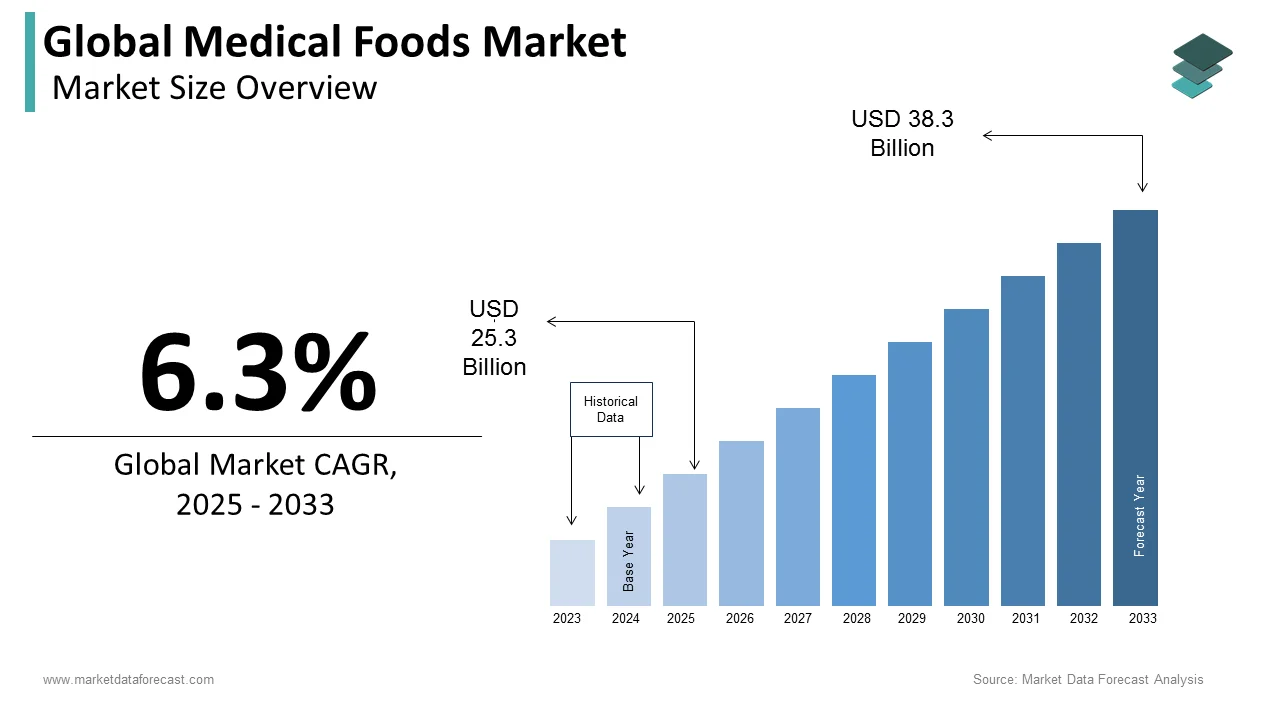

The global medical foods market was worth US$ 21.1 billion in 2024 and is anticipated to reach a valuation of US$ 38.3 billion by 2033 from US$ 23.5 billion in 2025, and it is predicted to register a CAGR of 6.3% during the forecast period 2025-2033.

MARKET DRIVERS

The growing patient population suffering from chronic diseases primarily propels the growth of the medical foods market.

The incidence of various chronic diseases worldwide, such as diabetes, cardiovascular disease, cancer, and Alzheimer's disease, is on the rise. According to the World Health Organization (WHO), 71% of deaths worldwide were due to chronic diseases in 2019. CDC says 6 out of 10 U.S. adults have at least one chronic disease. People who are suffering from chronic diseases must undergo a multifaceted approach, including lifestyle changes, medication, and nutritional therapy. Medical foods are foods that are specifically designed to provide nutrition support to patients and these foods are primarily used to satisfy the unique nutritional needs of patients suffering from chronic diseases. For example, medical foods for diabetic patients contain certain nutrients that help regulate their blood sugar levels. Likewise, the growing prevalence of chronic diseases is anticipated to result in the increasing demand for medical foods and contribute to market growth.

The rising awareness among people regarding the importance of nutrition contributes to the growth of the medical foods market.

In recent years, the understanding of people regarding the importance of nutrition in overall health has improved significantly and people have widely adopted various nutritional products to balance their specific nutritional needs. Medical foods provide the required nutritional support and are designed to address the specific needs of people. Due to the recent COVID-19 pandemic, people have started putting emphasis on their health conditions and consuming more nutritious foods to meet their nutritional needs. Such actions from people are expected to fuel the demand levels for medical foods and boost market growth in the coming years.

The growing aging population worldwide contributes to the growth of the medical foods market.

Aged people are likely to diagnose with various diseases such as Alzheimer's disease and osteoporosis and need strong nutritional support to manage the conditions effectively, which is fuelling the demand for medical foods and contributing to the market growth. The increasing number of advancements in medical research and rising R&D efforts by the market participants to develop new and effective medical food products further fuel the growth rate of the market.

Furthermore, the growing healthcare costs, regulatory support from the governments for medical foods, rising interest in personalized nutrition and personalized healthcare, increasing availability of medical foods through various distribution channels such as e-commerce and retail stores and growing trend of self-care support the medical foods market growth. The development of new formulations and delivery systems for medical foods, increasing investments in research and development by manufacturers and academic institutions for the R&D of medical foods and rising demand for natural and organic products favor the medical foods market growth.

MARKET RESTRAINTS

The high costs associated with medical foods are one of the key factors hampering the market growth. Poor awareness among healthcare professionals regarding the potential benefits of medical foods is another major roadblock to the growth rate of the medical foods market. Stringent regulatory frameworks and limited reimbursement policies for medical foods further impede market growth. The competition from alternative therapies such as pharmaceuticals and dietary supplements and limited research on the efficacy and safety of medical foods hinder market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.3% |

|

Segments Covered |

By Product, Application, Route of Administration, Sales Channel, and Region. |

|

Various Analyses Covered |

Global, Regional, and country-level analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Fresenius Kabi AG, Danone, Targeted Medical Pharma Inc., Primus Pharmaceuticals Inc., Mead Johnson & Company, LLC, Abbott, and Nestlé, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

Based on product, the powder segment had the leading share of the global medical foods market in 2024 and is anticipated to hold a promising occupancy during the forecast period. The growth of the segment is majorly driven by the ease of use and longer shelf life compared to other forms of medical foods. In addition, the versatility and cost-effectiveness of powered medical foods boost the growth rate of the segment. The growing patient population with chronic diseases and rapid adoption of technological developments in the manufacturing of medical foods such as improvements in taste, texture, and ease of consumption further promote segmental growth.

The liquid segment is estimated to witness the fastest CAGR during the forecast period owing to factors such as easier to consume, higher absorption rate, convenience for medical conditions, increasing prevalence of chronic diseases, rapid adoption of technological advancements and the growing aging population.

By Application Insights

Based on application, the nutritional deficiency segment held the major share of the global medical foods market in 2024 and the segmental domination is estimated to continue during the forecast period. Factors such as the increasing prevalence of chronic diseases, the growing aging population, and changes in lifestyle such as increased consumption of processed foods and sedentary habits are majorly resulting in the incidence of nutritional deficiencies and the same is contributing to the segmental growth. The growing trend of preventive healthcare and awareness of the importance of proper nutrition further fuel the growth rate of the segment.

The diabetic neuropathy segment is another notable segment and captured a substantial share of the worldwide market in 2024 and is expected to grow at a prominent CAGR during the forecast period. Factors such as the rising prevalence of diabetes, lack of effective pharmaceutical treatments and a growing awareness of the link between nutrition and nerve health among healthcare professionals drive the segmental growth.

By Route of Administration Insights

Based on the route of administration, the oral segment dominated the market in 2024 and the same trend is anticipated to continue in the global market during the forecast period. Convenience, ease to use and cost-effectiveness of oral administration majorly contribute to the segmental growth. The development of advanced technologies and the availability of various forms of oral medical foods, such as capsules, tablets, and powders further fuel the growth rate of the segment. The growing trend of preventive healthcare, rising awareness of the importance of proper nutrition, increasing awareness among people regarding the benefits of a healthy diet and lifestyle and growing use of medical foods for nutritional deficiencies, diabetes, and neurological disorders boost the segmental growth.

By Sales Channel Insights

Based on sales channels, the institutional segment that includes hospitals, home care facilities and facilities for the disabled held the largest share of the global market in 2024 and is anticipated to remain dominant throughout the forecast period. Factors such as the critical role it plays in the distribution and administration of medical foods and the reliability and security it offers are majorly driving the growth of the segment. The rising demand for medical foods in institutional settings further fuels the growth rate of the segment.

REGIONAL ANALYSIS

North America dominated the medical foods market in 2024 and the regional domination is anticipated to continue during the forecast period.

The growth of the North American market is primarily driven by factors such as the growing prevalence of chronic diseases such as diabetes, obesity, and cardiovascular diseases in North America, the growing geriatric population, rising awareness of medical foods, and the presence of many key market players such as Nestle Health Science, Abbott Laboratories, and Danone Nutricia. In addition, favorable government initiatives and policies regarding medical foods and their coverage under insurance schemes contribute to the North American market growth. The U.S. held the largest share of the North American market in 2024, followed by Canada. The rising prevalence of chronic diseases such as diabetes and the presence of several market players primarily drives the growth of the U.S. market. According to the Centers for Disease Control and Prevention (CDC), more than 34 Americas have diabetes.

Europe is a lucrative regional market for medical foods and is anticipated to hold a noteworthy share of the worldwide market during the forecast period. The growing aging population in Europe, increasing awareness of the benefits of medical foods and growing patient population of chronic diseases majorly boost the growth rate of the European market. The presence of several leading manufacturers of medical foods in Europe and favorable government regulations and policies supporting the use of medical foods for specific diseases and health conditions promote the European medical foods market growth. The launch of new and innovative products specifically designed for the European market further promotes regional market growth. Germany held the largest share of the European market in 2024 and is anticipated to register a healthy CAGR during the forecast period.

APAC is estimated to showcase the fastest CAGR among all the regions in the worldwide market during the forecast period. The rising prevalence of chronic diseases, increasing healthcare expenditure, and rising disposable income majorly drive the medical foods market in the Asia-Pacific region. In addition, the growing geriatric population, changing lifestyles, and increasing awareness of the benefits of medical foods fuel the growth rate of the APAC market. Furthermore, the rising emphasis of international market participants to capture the potential of the APAC market and the launch of new products specifically designed for the Asian market promote regional market growth. Japan captured the leading share of the APAC market in 2024 and is expected to grow substantially during the forecast period owing to the growing consumption of medical foods and rapid adoption of these products by the patient population of various diseases in Japan.

Latin America had a considerable share of the worldwide market in 2024 and is anticipated to grow at a healthy CAGR during the forecast period. The growing patient population with diabetes and obesity, the availability of government initiatives and policies supporting the use of medical foods, and increasing healthcare expenditure fuel the medical foods market in Latin America.

MEA occupied a moderate share of the worldwide market in 2024 and is predicted to register a steady CAGR during the forecast period.

MARKET KEY PLAYERS

Fresenius Kabi AG, Danone, Targeted Medical Pharma Inc., Primus Pharmaceuticals Inc., Mead Johnson & Company, LLC, Abbott, and Nestlé are some of the notable players in the global medical foods market.

MARKET SEGMENTATION

This research report on the global medical foods market has been segmented and sub-segmented based on product, application, route of administration, sales channel, and region.

By Product

- Powder

- Pills

- Others

- Liquid

- Gel

- Semi-Solid

By Application

- Nutritional Deficiency

- Alzheimer’s Disease

- Depression

- Diabetic Neuropathy

By Route of Administration

- Oral

- Enteral

By Sales Channel

- Institutional

- Retail

- Online

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

what is the compound annual growth rate (CAGR%) of the global medical foods market during the forecast period?

The global medical foods market is expected to grow at a CAGR of 6.3% during the forecast period.

Which Region holds the largest revenue share during the forecast period in the global medical foods market ?

The North American medical foods market is expected to grow significantly and hold the largest revenue share during the forecast period.

who are the key players of the global medical foods market ?

Fresenius Kabi AG, Danone, Targeted Medical Pharma Inc., Primus Pharmaceuticals Inc, Mead Johnson & Company, LLC, Abbott, and Nestlé are some of the key market players in medical foods market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]