Global Medical Device Technologies Market Size, Share, Trends & Growth Forecast Report By Device Type (Electro-medical Equipment, Irradiation Apparatus, Dental Apparatus, In Vitro Diagnostics (IVD) Devices, Kidney/Dialysis Devices, Diagnostic Imaging Devices, Ophthalmology Devices, Orthopedic Devices, Endoscopy Devices, Diabetes Care Devices, Anaesthesia & Respiratory Care Devices and Wound Management Devices), Technology and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2025 to 2033)

Global Medical Device Technologies Market Size

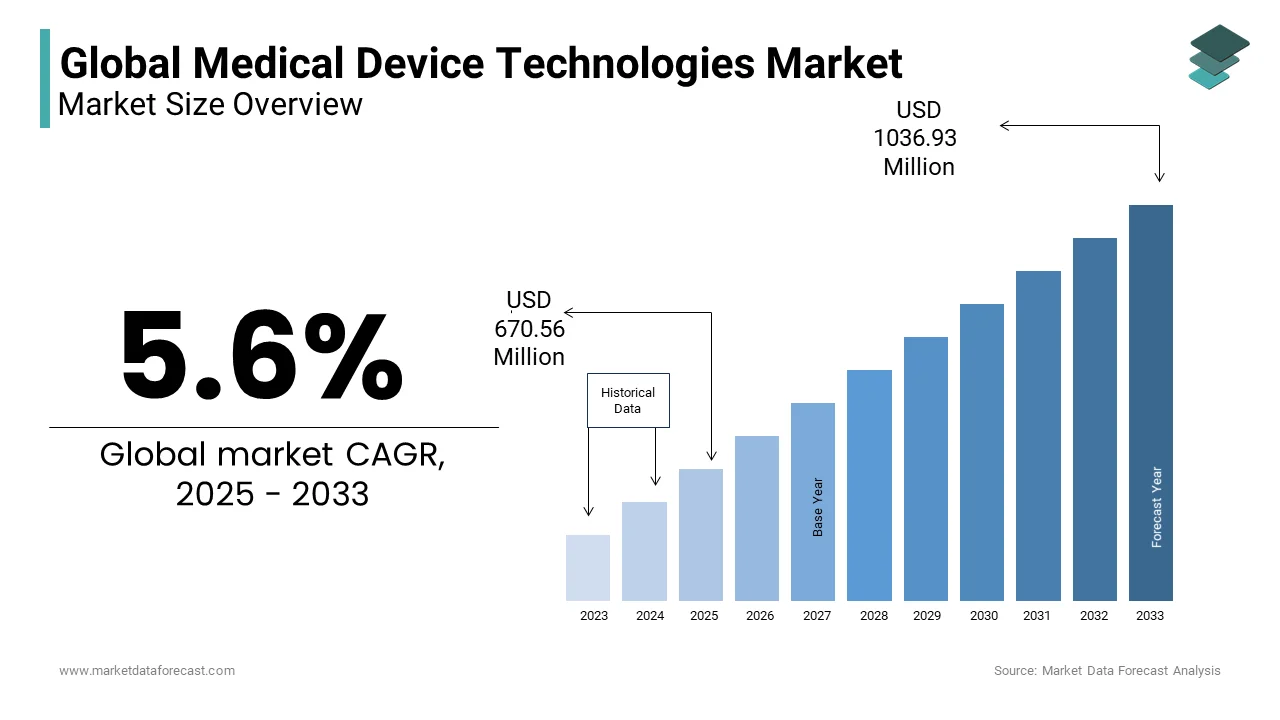

The global medical device technologies market worth USD 635 Million in 2024. The global market is predicted to grow to USD 1036.93 Million by 2033 from USD 670.56 Million in 2025, rising at a CAGR of 5.6 % from 2025 to 2033.

The Medical Device Technologies range from implantable devices such as cardiac pacemakers and neurostimulators to non-invasive systems like MRI scanners, point-of-care testing units, and robotic surgical platforms. Unlike conventional medical tools, modern device technologies increasingly incorporate artificial intelligence, real-time data analytics, and connectivity via the Internet of Medical Things (IoMT). According to the World Health Organization, over 1.5 million medical device-related adverse events were reported globally between 2018 and 2022, prompting a paradigm shift toward smarter, failure-resistant designs.

MARKET DRIVERS

Escalating Global Burden of Chronic Diseases Requiring Advanced Monitoring and Intervention

The rising prevalence of non-communicable diseases such as cardiovascular disorders, diabetes, and chronic respiratory conditions is amplifying the growth of the Medical Device Technologies market. According to the World Health Organization, chronic diseases account for 74% of all deaths globally, with over 415 million adults living with diabetes with a figure projected to reach 642 million by 2040. This epidemiological shift has intensified demand for continuous glucose monitors, insulin pumps, implantable cardioverter-defibrillators, and remote patient monitoring systems. The International Diabetes Federation reports that in 2023, over 30 million individuals in North America and Europe used connected glucose sensing devices, reflecting a 22% year-on-year increase. These technologies enable real-time glycemic tracking and reduce hospitalization rates by up to 35%, as demonstrated in a longitudinal study by the Mayo Clinic.

Integration of Artificial Intelligence and Machine Learning in Diagnostic and Surgical Systems

Artificial intelligence is transforming medical device functionality by enabling predictive diagnostics, image interpretation, and autonomous decision support, which is driving the growth of the Medical Device Technologies market. AI-powered imaging devices, such as digital pathology scanners and AI-enhanced CT systems, have demonstrated diagnostic accuracy comparable to or exceeding that of human radiologists in specific applications. According to a study published in Nature Medicine, an AI-driven echocardiography system developed by researchers at Mount Sinai Hospital achieved a 94% accuracy rate in detecting left ventricular dysfunction, significantly outperforming traditional screening methods. Furthermore, the U.S. Food and Drug Administration has cleared over 520 AI-enabled medical devices as of 2024, with a 68% increase in approvals since 2020.

MARKET RESTRAINTS

Stringent Regulatory Pathways and Prolonged Approval Timelines for High-Risk Devices

The development and commercialization of medical device technologies are constrained by rigorous regulatory scrutiny for Class III and implantable devices requiring premarket approval, which is restricting the growth of the Medical Device Technologies market. In the United States, the FDA’s PMA process for high-risk devices averages 1,090 days from submission to approval, as reported by the Regulatory Affairs Professionals Society. This extended timeline increases R&D costs and delays market entry, discouraging innovation in smaller firms. Similarly, the European Union’s transition to the Medical Device Regulation (MDR) in 2021 led to a 40% decline in new device certifications by notified bodies, as per data from MedTech Europe. The stringent clinical evidence requirements and post-market surveillance obligations under MDR have forced over 30% of mid-tier manufacturers to restructure or discontinue product lines.

Cybersecurity Vulnerabilities in Connected Medical Devices

The growing risks of cyberattacks that can compromise patient safety and data integrity is additionally hampering the growth of the medical devices technologies market. The U.S. Department of Health and Human Services recorded 678 healthcare-related cybersecurity incidents in 2023, with over 22% involving connected infusion pumps, imaging systems, or pacemakers. According to a report by the Food and Drug Administration, nearly 1,200 medical devices were recalled between 2018 and 2023 due to software vulnerabilities, including the 2023 voluntary recall of certain Medtronic insulin pumps over remote exploit risks. The Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency (CISA) warns that legacy devices lacking encryption or patch management are particularly susceptible.

MARKET OPPORTUNITIES

Expansion of Point-of-Care and Portable Diagnostic Devices in Low- and Middle-Income Countries

The expansion of healthcare industry with the advanced technologies is setting up new opportunities for the growth of the medical devices technologies market. According to the World Bank, over 4.5 billion people in low- and middle-income countries lack access to basic diagnostic services, creating demand for affordable, portable, and easy-to-operate devices. The Foundation for Innovative New Diagnostics (FIND) reports that rapid molecular testing units, such as the GeneXpert system, have been deployed in over 130 countries to detect tuberculosis and HIV with 95% sensitivity. Similarly, Butterfly Network’s handheld, AI-integrated ultrasound device has been adopted in rural clinics across India and sub-Saharan Africa by enabling real-time diagnostics without requiring specialist training.

Integration of Wearable Sensors and Remote Patient Monitoring Platforms

The proliferation of wearable medical devices such as smart patches, ECG-enabled watches, and respiratory sensors offers unprecedented opportunities for continuous health tracking and early disease detection is also to promote the growth of the medical devices technologies market. According to the International Data Corporation, global shipments of wearable health devices surpassed 200 million units in 2023, with medical-grade devices accounting for 38% of the market. The Apple Heart Study, conducted in collaboration with Stanford Medicine, demonstrated that irregular pulse notifications from the Apple Watch led to timely diagnosis of atrial fibrillation in 0.5% of participants, prompting clinical evaluation.

MARKET CHALLENGES

High Development and Commercialization Costs for Next-Generation Devices

The financial burden associated with designing, testing, and launching advanced medical devices for startups and academic spin-offs is to restrict the growth of the medical devices technologies market in the coming years. According to the National Institutes of Health, bringing a Class III medical device from concept to market requires an average investment of USD 94 million and spans over seven years. This includes expenses for clinical trials, regulatory compliance, intellectual property protection, and manufacturing scale-up. A report by the Advanced Medical Technology Association (AdvaMed) reveals that 60% of early-stage medtech firms fail to secure Series B funding due to investor hesitancy over prolonged ROI timelines. Additionally, reimbursement uncertainties in both public and private healthcare systems further deter commercialization.

Ethical and Clinical Validity Concerns Surrounding AI-Driven Medical Devices

AI-integrated medical technologies face challenges regarding algorithmic bias, transparency, and clinical reliability, which is to hamper the growth of the medical devices technologies market. A 2023 investigation by the British Medical Journal found that 85% of AI-based diagnostic tools evaluated on diverse patient populations exhibited reduced accuracy among underrepresented racial and ethnic groups, raising equity concerns. For example, dermatology AI systems trained predominantly on lighter skin tones demonstrated a 34% lower sensitivity in detecting melanoma in patients with darker pigmentation, as per research from the University of California, San Francisco. Additionally, the “black box” nature of deep learning models complicates clinician trust and regulatory assessment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Device Type, Technology, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Market Players | Abbott Laboratories Inc., Becton Dickinson and Company, GE Healthcare, Novartis Diagnostics, bioMerieux Inc., Biomerica Inc., Johnson and Johnson Diagnostics Inc., Olympus Corporation, Qiagen N.V., Siemens AG, Thermo Fischer Scientific Inc., and Zenith Healthcare Ltd. |

SEGMENTAL ANALYSIS

By Device Type Insights

The In Vitro Diagnostics (IVD) Devices segment was the largest and held 18.2% of the global medical device technologies market share in 2024 with the indispensable role IVDs play in early disease detection, treatment monitoring, and public health surveillance. According to the Foundation for Innovative New Diagnostics (FIND), over 4.3 billion IVD tests were conducted globally in 2023 for HIV, tuberculosis, and hepatitis, with rapid antigen and molecular assays forming the backbone of decentralized testing strategies.

The Diabetes Care Devices segment is expected to grow with an expected CAGR of 10.6% during the forecast period with the escalating global diabetes epidemic and the shift toward continuous, real-time glucose monitoring. Over 537 million adults were living with diabetes in 2023, a figure projected to rise to 643 million by 2030, necessitating advanced self-management tools. Furthermore, the U.S. Food and Drug Administration approved 17 new integrated insulin pump-CGM systems between 2022 and 2024, enabling automated insulin delivery. The American Diabetes Association reports that CGM usage among insulin-dependent patients in the U.S. surged from 25% in 2019 to 68% in 2023 with the rapid patient and provider acceptance.

By Technology Insights

The biomarkers segment accounted for the largest share of the worldwide market in 2024 and the domination of the segment is likely to continue during the forecast period. The growth of the segment is primarily driven by the increasing patient population suffering from chronic diseases, increasing developments in genomics and proteomics, rapid adoption of personalized medicine, and growing investments by the market participants in R&D. In addition, the growing number of developments in the healthcare infrastructure among the developing countries and increasing per capita income favoring the segment’s growth rate.

On the other hand, the bio-implants and molecular diagnostics segment is predicted to grow promisingly owing to the increasing use of bone, soft tissue, and skin implants, along with the increasing research and development in molecular chemistry.

REGIONAL ANALYSIS

North America Medical Device Technologies Market Insights

North America was the largest contributor of the global medical device technologies market with 32.2% of the share in 2024 with highly sophisticated healthcare infrastructure, robust R&D investments, and strong regulatory support for innovation. The United States alone accounts for over 40% of global medical device expenditures, driven by high patient demand for cutting-edge therapies and widespread insurance coverage for advanced diagnostics and implantables. According to the National Institutes of Health, U.S. public and private entities invested USD 22.4 billion in medical device research in 2023, with a significant portion directed toward AI-integrated imaging and robotic surgery. Additionally, the Food and Drug Administration’s Breakthrough Devices Program accelerated the review of 312 high-impact technologies in 2023 by fostering rapid commercialization.

Europe Medical Device Technologies Market Insights

Europe was positioned second by holding 31.3% of share in 2024 with a mature and highly regulated medical device landscape, with Germany, France, and the United Kingdom serving as primary innovation and distribution hubs. European healthcare systems emphasize cost-effective, evidence-based technologies, driving demand for reusable endoscopic systems, dialysis machines, and orthopedic implants. According to the European Commission, over 500,000 hip and knee replacements were performed annually across EU member states between 2021 and 2023, supported by aging demographics and national reimbursement frameworks. The transition to the Medical Device Regulation (MDR) has enhanced patient safety but also intensified compliance burdens, with notified bodies conducting over 12,000 audits in 2023 alone.

Asia Pacific Medical Device Technologies Market Insights

Asia Pacific medical technologies market growth is lucratively growing with prominent CAGR in the next coming years owing to the rising healthcare expenditure, expanding insurance coverage, and government-led modernization of medical infrastructure in countries like China, Japan, and South Korea. Japan’s Ministry of Health, Labour and Welfare reports that over 70% of Japanese hospitals now utilize robotic-assisted surgical systems, particularly in urology and minimally invasive procedures. India’s Ayushman Bharat Digital Mission has enabled interoperability for over 350 million health records, facilitating the deployment of connected diagnostic devices in public hospitals.

Latin America Medical Device Technologies Market Insights

Latin America medical device technologies market is anticipated to grow steadily in the next coming years by witnessing steady growth in device adoption, particularly in Brazil, Mexico, and Chile, where urban healthcare centers are upgrading to digital imaging and dialysis technologies. Brazil’s Ministry of Health allocated BRL 4.1 billion in 2023 for the acquisition of diagnostic imaging equipment and ICU ventilators, aiming to reduce regional disparities in care access. The prevalence of diabetes and cardiovascular diseases is rising. According to PAHO, over 70 million people in Latin America live with diabetes, which is driving demand for glucose monitors and cardiovascular implants.

Middle East & Africa Medical Device Technologies Market Insights

Middle East & Africa medical device technologies market is to have steady pace in the future period. The Gulf Cooperation Council (GCC) countries are leading regional adoption through Vision 203 is amplifying the healthcare modernization initiatives. The UAE invested AED 9.2 billion in medical technology upgrades between 2021 and 2023, including the installation of AI-powered diagnostic systems in Dubai’s smart hospitals.

KEY MARKET PLAYERS

Companies leading the global Medical Device Technologies Market profiled in the report are Abbott Laboratories Inc., Becton Dickinson and Company, GE Healthcare, Novartis Diagnostics, bioMerieux Inc., Biomerica Inc., Johnson and Johnson Diagnostics Inc., Olympus Corporation, Qiagen N.V., Siemens AG, Thermo Fischer Scientific Inc., and Zenith Healthcare Ltd.

TOP LEADING PLAYERS IN THE MARKET

Medtronic plc

Medtronic has established a formidable presence in the Asia Pacific medical device technologies market through its comprehensive portfolio of cardiac rhythm management systems, minimally invasive surgical tools, and diabetes monitoring solutions. The company has deepened its regional integration by establishing innovation centers in Singapore and Shanghai, focusing on co-developing cost-effective devices tailored for diverse healthcare settings. In 2023, Medtronic launched its Hugo™ robotic-assisted surgery system in Japan and Australia, receiving regulatory approval and entering partnerships with leading hospitals for clinical adoption. It also expanded its manufacturing footprint in Malaysia to enhance supply resilience.

Siemens Healthineers AG

Siemens Healthineers has emerged as a pivotal player in the Asia Pacific medical device landscape by advancing diagnostic imaging, laboratory diagnostics, and digital health ecosystems. The company has localized production in India and China to meet rising demand for MRI, CT, and ultrasound systems in public and private hospitals. In 2023, it introduced the teamplay digital health platform across Southeast Asia, enabling hospitals in Thailand, Indonesia, and Vietnam to centralize imaging data and optimize workflow efficiency. Siemens also partnered with Japan’s National Hospital Organization to deploy AI-powered radiology solutions that reduce diagnostic turnaround time by up to 30%. Its commitment to sustainability is evident in energy-efficient imaging units now installed in over 1,200 facilities across the region.

Philips Healthcare

Philips Healthcare has intensified its focus on integrated care solutions in the Asia Pacific region, emphasizing remote monitoring, AI-enhanced diagnostics, and home-based medical technologies. The company has invested heavily in digital infrastructure, launching its HealthSuite platform in India and South Korea to support tele-ICU and chronic disease management programs. In 2023, Philips inaugurated a new research hub in Taiwan dedicated to developing wearable sensors and AI algorithms for early detection of respiratory deterioration. It also supplied over 10,000 portable ultrasound devices to rural clinics in Indonesia and the Philippines through government health initiatives. By aligning with national digital health strategies in countries like Australia and Malaysia, Philips is embedding its technologies into public health frameworks. Its emphasis on human-centered design and sustainable innovation has positioned it as a preferred partner for hospitals seeking to transition from reactive to preventive care models across urban and underserved areas.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Medical Device Technologies Market employ strategies such as product innovation, geographic expansion, strategic partnerships, digital integration, and regulatory agility. Companies are prioritizing AI and IoT-enabled devices to enhance clinical decision-making and remote monitoring capabilities. Expansion into high-growth regions like Asia Pacific and Latin America is achieved through localized manufacturing, joint ventures, and regulatory alignment. Collaborations with hospitals, tech firms, and governments accelerate adoption of integrated care systems. Investment in post-market surveillance and cybersecurity strengthens compliance and patient trust. Additionally, firms are streamlining R&D pipelines using real-world evidence and adaptive trial designs to expedite approvals and ensure clinical relevance in evolving healthcare ecosystems.

COMPETITION OVERVIEW

The competitive environment in the Medical Device Technologies Market is marked by intense rivalry among global leaders, regional innovators, and emerging digital health startups. Incumbents leverage scale, regulatory expertise, and diversified portfolios to maintain dominance, while agile entrants disrupt niche segments with AI-driven diagnostics and wearable sensors. Differentiation increasingly hinges on interoperability, data analytics, and patient-centric design rather than hardware alone. Regulatory divergence across regions complicates market entry, favoring firms with robust compliance infrastructure. In Asia Pacific, local manufacturers are gaining traction by offering cost-optimized alternatives by prompting multinationals to adopt hybrid models combining premium innovation with scalable solutions. Strategic mergers, such as those between device makers and healthtech firms, reflect a shift toward ecosystem-based competition, where integration with electronic health records and telemedicine platforms defines market relevance.

RECENT MARKET DEVELOPMENTS

- In March 2023, Medtronic launched its Hugo™ robotic-assisted surgery system in Japan, marking its entry into the country’s advanced surgical robotics market and expanding its minimally invasive therapy footprint in Asia Pacific.

- In July 2023, Siemens Healthineers partnered with Thailand’s Ministry of Public Health to deploy AI-enhanced CT imaging systems in 15 regional hospitals, which is improving diagnostic accuracy and reducing radiologist workload.

- In October 2023, Philips Healthcare inaugurated a research and development center in Taiwan focused on AI-powered wearable devices for respiratory and cardiac monitoring in home care settings.

- In January 2024, Medtronic received approval from Australia’s Therapeutic Goods Administration for its next-generation LINQ II insertable cardiac monitor by enhancing remote patient monitoring capabilities across Oceania.

- In May 2024, Siemens Healthineers expanded its manufacturing facility in Pune, India, to increase production of portable ultrasound and point-of-care testing devices for distribution across South and Southeast Asia.

MARKET SEGMENTATION

This research report on the global medical device technologies market has been segmented based on the device type, technology, and region.

By Device Type

- Electro-medical Equipment

- Pacemakers

- MRI Systems

- Patient Monitoring System

- Ultrasonic Scanning System

- Diagnostic Imaging System

- Irradiation Apparatus

- X-Ray Devices

- Tomography Devices

- Surgical And Medical Apparatus

- Dental Apparatus

- Dentists

- Dental Hygienists

- Laboratories

- In Vitro Diagnostics (IVD) Devices

- Kidney/Dialysis Devices

- Diagnostic Imaging Devices

- Ophthalmology Devices

- Orthopedic Devices

- Endoscopy Devices

- Diabetes Care Devices

- Anaesthesia & Respiratory Care Devices

- Wound Management Devices

By Technology

- Biomarkers

- Bio-implants

- Molecular Diagnostics

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1.How much is the global medical device technologies market going to be worth by 2033?

As per our research report, the global medical device technologies market size is projected to be USD 1036.93 million by 2033.

2.At What CAGR, the global medical device technologies market is expected to grow from 2024 to 2033?

The global medical device technologies market is estimated to grow at a CAGR of 5.6% from 2024 to 2033.

3. Which region is anticipated to witness considerable growth in the medical device technologies market?

Geographically, the APAC medical device technologies market is predicted to have the fastest growth rate in the global market from 2024 to 2033.

4. Which are the significant players operating in the medical device technologies market?

Abbott Laboratories Inc., Becton Dickinson and Company, GE Healthcare, Novartis Diagnostics, bioMerieux Inc., Biomerica Inc., and Johnson and Johnson Diagnostics Inc are some of the significant players operating the medical device technologies market

5. How is AI impacting the Medical Device Technologies Market?

AI is enhancing diagnostics, treatment personalization, and device connectivity, fueling innovation and market growth.

6.Who are the leading companies in the Medical Device Technologies Market?

Top companies include Abbott Laboratories, Roche Diagnostics, Philips, Siemens Healthineers, and Medtronic.

7. How is the Medical Device Technologies Market evolving with telehealth?

Integration of IoT and remote monitoring devices is expanding telehealth, offering personalized, timely, and cost-effective care.

8.What technological advancements are shaping the Medical Device Technologies Market?

Key tech includes AI, 3D printing, robotic surgery, wearable sensors, and miniaturized implants.

9.How do chronic diseases influence the Medical Device Technologies Market?

Increasing chronic diseases drive demand for diagnostic, monitoring, and therapeutic devices in the market.

10. How does the Medical Device Technologies Market address aging population needs?

Devices targeting age-related conditions and improving quality of life are a significant growth driver in this market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com