Global Medical Coding Market Size, Share, Trends & Growth Forecast Report By Component, Classification System, End-user and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2026 to 2034

Market Size, 2025

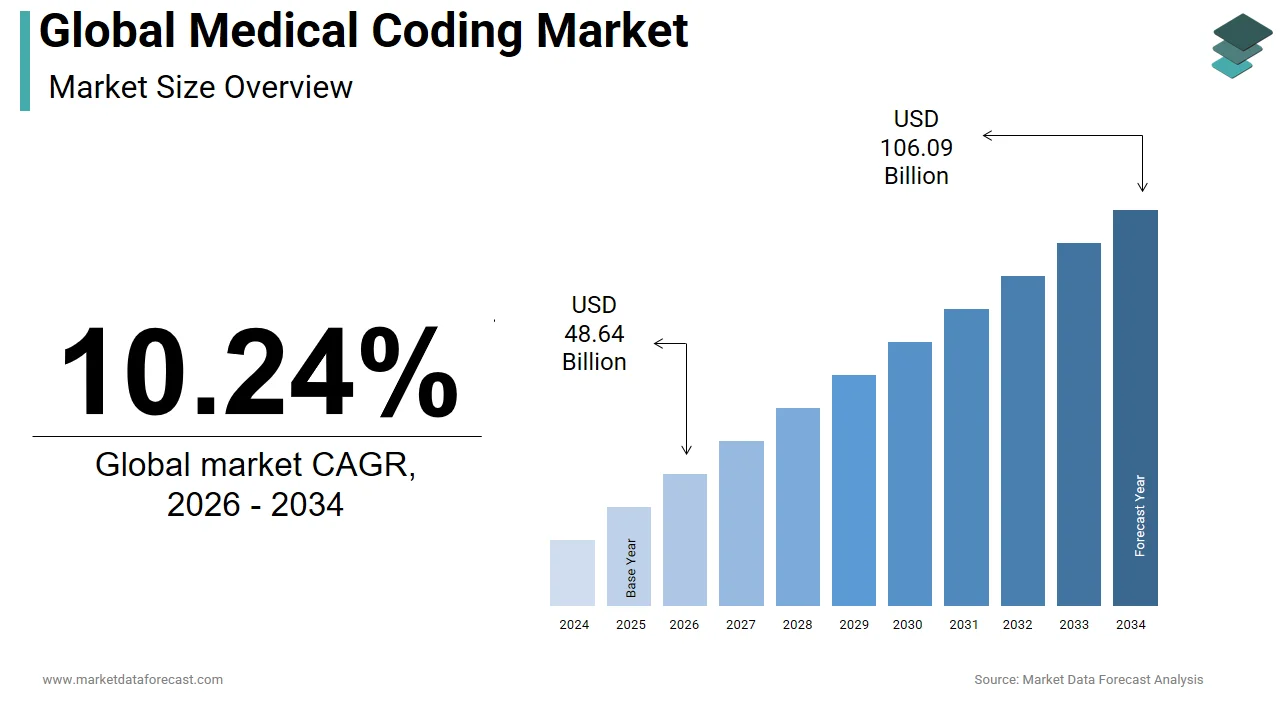

$44.12 BnMarket Estimate, 2026

$48.64 BnMarket Forecast, 2034

$106.09 BnCAGR, 2026–2034

10.24%Global Medical Coding Market Size

The global medical coding market was valued at USD 44.12 billion in 2025, is estimated to reach USD 48.64 billion in 2026, and is projected to reach USD 106.09 billion by 2034, growing at a CAGR of 10.24% from 2026 to 2034.

Medical coding constitutes the systematic translation of healthcare diagnoses, procedures, services, and equipment into standardized alphanumeric codes, serving as the linguistic backbone of health data interoperability and reimbursement infrastructure. As per the American Health Information Management Association, nearly all of U.S. hospitals utilize coded data for billing and analytics, while ICD-11 implementation is underway across many WHO Member States. Dozens of countries have started implementation activities, and a growing number are piloting or collecting data with ICD-11. The Centers for Medicare & Medicaid Services mandates code compliance for all claims processing, reinforcing its non-negotiable role in fiscal and clinical workflows. Healthcare systems that lack granular codification would be without the structural coherence needed for audit trails, epidemiological tracking, and payment integrity across all public and private payers.

MARKET DRIVERS

Growing Adoption of Electronic Health Records Boosting Medical Coding Demand

The global proliferation of electronic health records, which necessitate structured and machine-readable data for interoperability and value-based reimbursement, is primarily fuelling the growth of the medical coding market. As per the Office of the National Coordinator for Health IT, nearly all of the non-federal acute care hospitals in the United States had adopted certified EHR technology by 2021, which creates an operational dependency on accurate, real-time code assignment. According to the European Commission, digital patient record use among EU clinicians has increased substantially, with member-state eHealth indicators rising in recent years. This digitization wave, coupled with regulatory mandates like the U.S. 21st Century Cures Act, compels health systems to embed certified coders within clinical documentation improvement teams, thereby expanding workforce demand and operational budgets dedicated to coding integrity.

Regulatory Scrutiny and Fraud Prevention Fuel Demand for Accurate Medical Coding

The intensifying regulatory scrutiny surrounding coding accuracy is driven by governmental audits and fraud prevention initiatives, and is also propelling the expansion of the medical coding market. According to sources, Medicare and Medicaid are among the largest sources of improper-payment estimates; auditors and CMS reports quantify tens of billions of dollars in improper payments across federal health programs in FY2022. Similarly, National audits and payer reviews in several countries report measurable rates of DRG/DRG-style misclassification and coding errors. These enforcement mechanisms compel providers to invest in certified coding professionals and AI-assisted validation tools, thereby transforming compliance from administrative overhead into strategic financial safeguarding and inflating market demand for precision-driven coding solutions.

MARKET RESTRAINTS

Shortage of Certified Coding Professionals Limiting Market Expansion

The global shortage of certified coding professionals, exacerbated by demographic attrition and insufficient training pipelines, is an obstacle to the medical coding market's growth. As per the American Academy of Professional Coders, the U.S. alone faces a deficit of approximately 8,500 credentialed coders annually, with attrition rates exceeding 12% due to burnout and retirement. The medical coding workforce is under pressure in many markets. According to studies, there are point to persistent shortages and staffing stress in coding teams. This scarcity inflates labor costs, delays claim submissions, and increases error rates, which compels institutions to divert capital toward stopgap technologies rather than sustainable workforce development, thereby constraining scalable market expansion.

Fragmented Coding Systems Hindering Global Standardization

The fragmentation of coding classification systems across jurisdictions, which impedes standardization and escalates operational complexity, further slows down the expansion of the medical coding market. According to the World Health Organization, there has been a mix of legacy ICD-10 usage and active ICD-11 implementation efforts globally. As per research, some EU/EEA countries have not yet fully harmonized procedure-coding schemes with every international standard; harmonization status varies across member states. This dissonance elevates training, auditing, and software customization costs, particularly for global health networks and telehealth platforms. As a result, this suppresses market efficiency and deters investment in unified coding automation solutions.

MARKET OPPORTUNITIES

AI Integration Enabling Real-Time and Error-Free Medical Coding

The integration of artificial intelligence for real-time coding assistance, which enhances coder productivity while reducing human error, is expected to generate new opportunities for the medical coding market. As per research, AI-assisted coding tools demonstrated a reduction in code assignment time and a decrease in audit discrepancies during pilot studies. According to sources, facilities deploying NLP-enhanced coding interfaces improved coder throughput without compromising compliance. These technologies do not replace human coders but function as force multipliers, enabling existing staff to manage expanding caseloads, particularly valuable in regions with workforce shortages, thus unlocking latent market capacity and justifying premium pricing for augmented coding platforms.

Value-Based Care Models Creating Demand for Advanced Medical Coding

The global transition to value-based care models, which demand granular, longitudinal coding for risk adjustment and outcome measurement, is giving fresh opportunities for the expansion of the medical coding market. According to the Commonwealth Fund, many U.S. commercial insurers tie provider reimbursements to quality metrics derived from coded clinical data, while Several national health systems use risk adjustment and coding rules to calculate reimbursements. Germany is among the countries using risk-adjusted schemes. Many public hospital performance dashboards use coded data for benchmarking and transparency. This paradigm shift transforms coding from a back-office billing function into a strategic asset for care coordination and financial modeling, which incentivizes health systems to invest in advanced coder training and analytics-integrated coding platforms, thereby expanding the market’s functional scope and revenue potential.

MARKET CHALLENGES

Rapid Classification Updates Outpacing Coder Skill Development

The accelerating obsolescence of coder skill sets due to rapid classification system updates and evolving payer rules is a key impediment to the growth of the medical coding market. As per sources, a portion of coding professionals reported that keeping pace with annual ICD, CPT, and HCPCS revisions. This perpetual learning curve strains institutional training budgets and increases turnover, as coders migrate to less volatile sectors, thereby destabilizing service delivery and inflating operational risk for providers reliant on consistent, audit-ready code assignment.

Misaligned Clinical Documentation Hindering Accurate Coding

The misalignment between clinical documentation and coding requirements, which creates persistent gaps in data capture and reimbursement accuracy, is degrading the expansion of the medical coding market. According to sources, a portion of inpatient records in hospitals lacked sufficient specificity for accurate code assignment. As per studies, only a portion of consultant physicians consistently document comorbidities to the level required for risk-adjusted coding. This disconnect forces coders into interpretive roles beyond their scope by increasing compliance exposure and necessitating costly clinical documentation improvement programs, which fragment workflow efficiency and suppress scalable market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Classification System, End-user & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Aviacode Inc., Oracle Corporation, Nuance Communications Inc., athenahealth, Medical Record Associates LLC, Maxim Healthcare Services Inc., 3M Company, and Parexel International Corporation. |

SEGMENTAL ANALYSIS

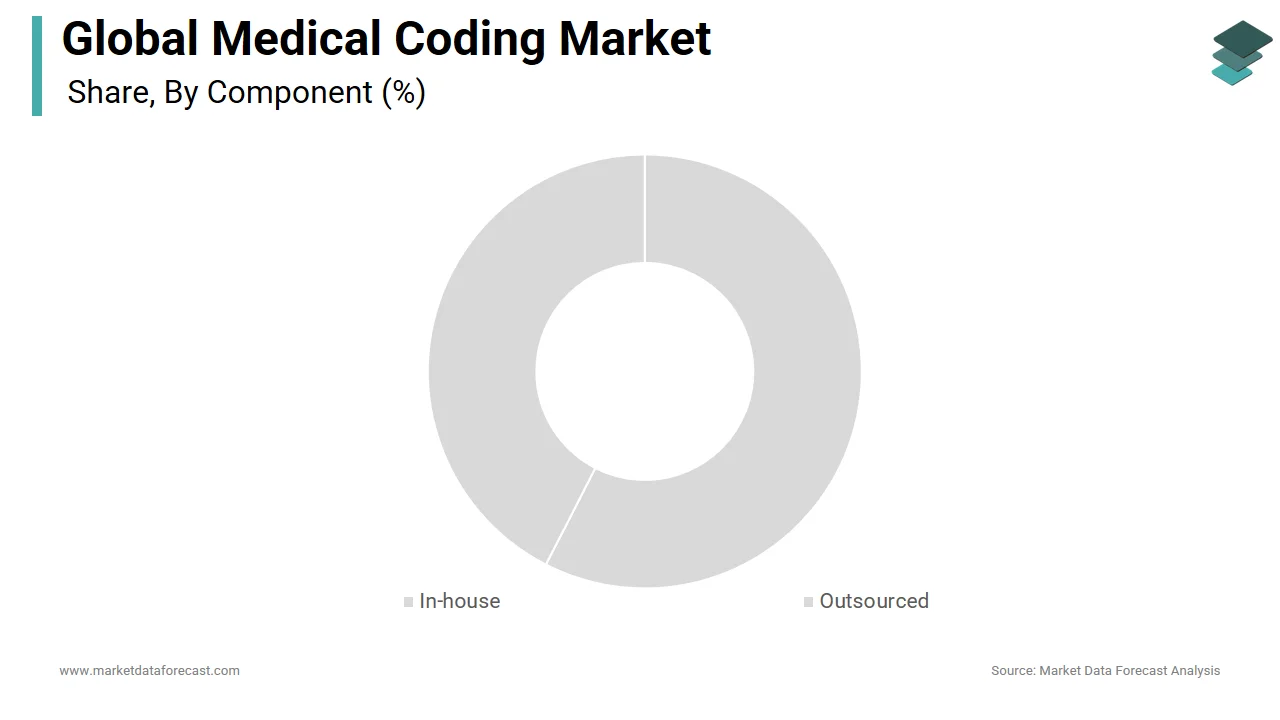

By Component Insights

In 2024, the in-house coding segment led the medical coding market by accounting for 627% share 2024. The pre-eminence of the in-house coding segment in the global market is mainly due to acute care institutions’ strategic imperative to retain direct control over revenue cycle integrity and compliance exposure. Large hospital systems, particularly in the United States and Western Europe, prioritize internal coding teams to ensure real-time alignment between clinical documentation and billing protocols, minimizing audit vulnerabilities. The American Hospital Association’s 2023 operational survey revealed that 74% of hospitals with over 300 beds maintain dedicated in-house coding departments, citing a 31% reduction in claim denials compared to outsourced models. The control mechanism is non-negotiable for institutions navigating value-based reimbursement, where misclassification directly impacts risk-adjusted payments. Regulatory intensification, including OIG’s heightened scrutiny of DRG upcoding, further entrenches institutional preference for direct oversight, which makes in-house coding not merely a cost center but a compliance firewall.

The outsourced coding segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 11.3% from 2026 to 2034. The growth of the outsourced coding segment is propelled by acute workforce shortages and the economic rationalization of non-core functions, particularly among mid-sized and rural providers. The U.S. Bureau of Labor Statistics projects an 8% growth in medical records and health information specialists, including coders, from 2022 to 2032. According to the Medical Group Management Association, 58% of physician groups with fewer than 20 practitioners now outsource coding to mitigate attrition-related disruptions, reporting a decrease in administrative overhead within months of transition. Simultaneously, cloud-based coding platforms with HIPAA-compliant workflows enable seamless vendor integration, which reduces latency. This convergence of labor economics, technological enablement, and global compliance pressure transforms outsourcing from a stopgap to a strategic lever.

By Classification System Insights

The International Classification of Diseases segment accounted for a significant share of the medical coding market in 2024. The domination of the International Classification of Diseases segment is attributed to universal adoption as the diagnostic lingua franca across public health, epidemiology, and reimbursement ecosystems. Every sovereign member of the WHO, 194 nations, is mandated to report mortality and morbidity statistics using ICD frameworks, embedding its use into national health information architectures. The U.S. National Center for Health Statistics confirmed that ICD-10-CM codes underpin 100% of inpatient and nearly all of outpatient diagnostic billing in Medicare, which processes over 5.2 billion claims annually. Germany’s Federal Statistical Office reported that ICD codes drive 89% of hospital case-mix funding allocations under its G-DRG system. Crucially, ICD-11’s semantic interoperability enhancements, including post-coordination and digital API compatibility, have triggered accelerated adoption. As per WHO’s adoption tracker, 42 countries implemented ICD-11 for mortality reporting by Q1 2024. The European Centre for Disease Prevention and Control mandates ICD harmonization for cross-border disease surveillance, further entrenching its infrastructural role. ICD's diagnostic breadth makes it indispensable for population health analytics, chronic disease registries, and pandemic response modeling. Its dominance transcends billing to become the scaffold of global health intelligence, unlike procedure-centric systems.

The Healthcare Common Procedure Coding System segment is expected to exhibit a noteworthy CAGR of 14.8% over the forecast period owing to the explosive growth in outpatient, ambulatory, and specialty procedural volumes, where HCPCS Level II codes govern device, drug, and non-physician service reimbursement. According to studies, there has been a year-over-year increase in HCPCS-coded drug administration events in hospital outpatient departments between 2022 and 2023, driven by biologic infusions and gene therapies. Simultaneously, CMS’s expansion of telehealth-covered services added 117 new HCPCS G-codes in 2023 alone, broadening applicability. Private payers, including UnitedHealthcare and Aetna, increasingly mirror CMS’s HCPCS adoption for specialty drug tracking, which creates market-wide standardization. Moreover, the rise of value-based bundled payments, such as CMS’s BPCI Advanced program, demands granular procedure costing, elevating HCPCS from a transactional tool to a financial modeling instrument. This procedural granularity, absent in ICD’s diagnostic focus, positions HCPCS as the engine of precision billing in modern care delivery.

By End-User Insights

The hospitals segment was the top-performing segment by occupying a substantial share of the global medical coding market in 2024. Hospitals generate the highest volume of complex, multi-code encounters requiring synchronized diagnostic, procedural, and revenue cycle coding, which contributes to the growth of the hospitals segment. The U.S. Agency for Healthcare Research and Quality’s Healthcare Cost and Utilization Project logged 36.5 million inpatient stays in 2022, each requiring an average of 14 discrete codes per discharge. As per Germany’s Federal Office of Statistics, hospitals account for 82% of all DRG-coded cases nationally, with each case involving cross-referencing between ICD, OPS, and pharmaceutical codes. Japan’s Ministry of Health, Labour and Welfare reported that acute care hospitals submit 91% of all nationally reimbursed coded claims, averaging 22 codes per patient episode. The complexity escalates with comorbidities. Regulatory frameworks like the U.S. Inpatient Prospective Payment System and Australia’s Activity-Based Funding model tie hospital reimbursement directly to coded case-mix indices, which makes coding accuracy a determinant of institutional solvency. No other setting matches this density of coding events, regulatory exposure, or financial consequence.

The diagnostic centers segment is predicted to witness the highest CAGR of 13.6% from 2026 to 2034 due to the decentralization of care delivery and the exponential rise in imaging, lab, and genetic testing volumes that demand discrete and high-frequency coding. India’s National Health Systems Resource Centre reported a year-over-year growth in diagnostic center claims submissions under Ayushman Bharat, which requires standardized coding for defined procedures. The proliferation of AI-powered diagnostics, such as CMS-covered AI-assisted mammography and retinal scans, introduces new HCPCS G-codes annually, expanding coding scope. Diagnostic centers, unlike hospitals, operate with leaner administrative teams, which makes outsourced and automated coding solutions essential, thereby accelerating market penetration. Their procedural focus, high throughput, and payer-driven standardization create a uniquely scalable coding demand curve unmatched by other segments.

REGIONAL ANALYSIS

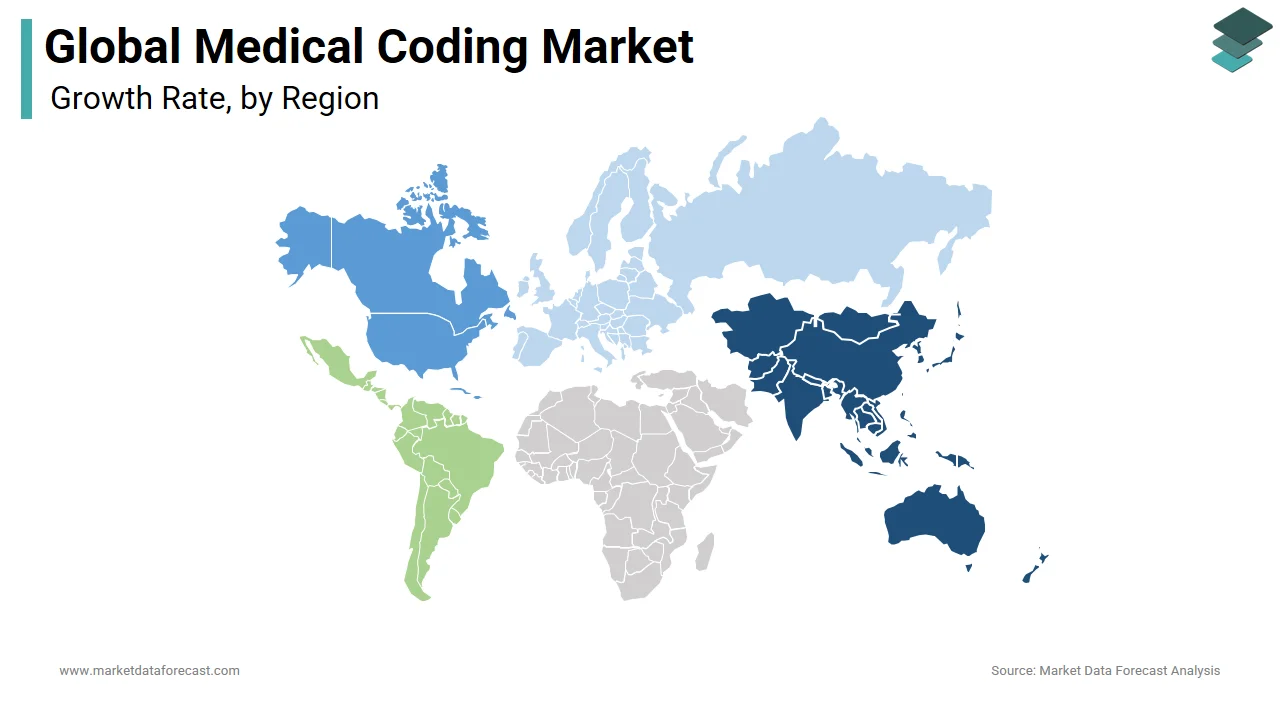

North America Medical Coding Market Analysis

North America dominated the global medical coding market with a 44.5% share in 2024. The domination of North America is fuelled by its hyper-regulated, high-volume, fee-for-service legacy transitioning into value-based complexity. The United States alone processes over 5.8 billion coded healthcare transactions annually, per the Centers for Medicare & Medicaid Services. As per Canada’s Canadian Institute for Health Information, 100% of provincial reimbursement is code-dependent, with Ontario alone requiring 12.4 million annually coded hospital separations. Regulatory density is unmatched. The U.S. Office of Inspector General recovered $2.3 billion in FY2023 from coding-related fraud, compelling institutional over-investment in compliance. Simultaneously, adoption of ICD-11 and AI-assisted coding is accelerating. The American Medical Informatics Association reported 61% of U.S. health systems piloted NLP-enhanced coding in 2023. Private payer influence further amplifies demand. This ecosystem of volume, regulation, technological adoption, and audit exposure creates a market depth and sophistication unrivaled globally, which makes North America not just the largest but the most innovation-intensive coding environment on earth.

Europe Medical Coding Market Analysis

Europe is the second largest in the medical coding market by capturing 28.6% share in 2024. The growth of Europe is driven by heterogeneous national systems converging under EU digital health mandates, creating both fragmentation and forced standardization. Germany’s Federal Joint Committee governs the largest single-payer DRG system in Europe, processing 19.7 million annually coded hospital cases using ICD-10-GM and OPS classifications. France’s National Health Data System reported 100% of hospital reimbursements are code-driven under its T2A model, with 8.3 million inpatient episodes coded in 2022. Eastern Europe is emerging as an outsourcing hub. Poland’s Health Information Systems Agency documented a 34% annual growth in outsourced coding contracts from Western European hospitals. Despite disparities in classification maturity, Sweden uses KSH97 while Bulgaria still relies on ICD-9, the EU’s regulatory harmonization is creating a unified, albeit complex, growth vector. Europe’s coding market is not monolithic but is being forcibly integrated, which makes it the world’s most politically engineered coding expansion zone.

Asia Pacific Medical Coding Market Analysis

Asia Pacific is rapidly expanding in the global medical coding market due to explosive healthcare digitization, insurance expansion, and leapfrog adoption of global coding standards. India’s National Health Authority reported that Ayushman Bharat processed 54 million coded hospital admissions in FY2023, requiring standardized ICD-10-AM and CPT-4 mappings across 25,000 empanelled facilities. Japan’s Ministry of Health confirmed 100% of hospital reimbursements are code-based under its DPC/PG system, with 16.8 million annually coded inpatient cases. China’s National Healthcare Security Administration mandated nationwide ICD-11 adoption by 2025, which triggered a surge in coder certification enrollments since 2021. Australia’s Independent Hospital Pricing Authority governs activity-based funding for all public hospitals using AR-DRGs, processing 11.4 million coded separations in 2022. The region’s coding demand is uniquely shaped by mobile health and telemedicine. Unlike Western markets, the Asia Pacific combines legacy paper-based systems with AI-native leapfrogging. Philippine BPOs now handle 22% of U.S. outsourced coding, as per the IT and Business Process Association of the Philippines. This duality of scale and innovation makes Asia Pacific the most dynamically bifurcated coding market globally.

Latin America Medical Coding Market Analysis

Latin America is moving ahead steadily in the global medical coding market, owing to uneven public-private adoption, which accelerates under insurance reform and digital health mandates. Brazil’s National Supplementary Health Agency governs 72 million privately insured lives, requiring ANS-compliant coding for 6,200 defined procedures across 5,400 accredited facilities. Mexico’s IMSS processed 4.7 million coded hospital discharges in 2022 using ICD-10, with a 2025 mandate for full CIE-10-Mexico alignment. Chile’s Superintendencia de Salud confirmed that 100% of Fonasa reimbursements are now code-dependent, covering 15.3 million beneficiaries. Outsourcing is surging. The region’s coding growth is uniquely propelled by mobile-first solutions. Public systems lag in granularity; private and hybrid models are racing toward OECD-level standardization. This is making Latin America the world’s most asymmetrically accelerating coding market.

Middle East and Africa Medical Coding Market Analysis

The Middle East and Africa are likely to grow in the medical coding market due to Gulf-led digitization and sub-Saharan leapfrogging by creating a dual-speed market. South Africa’s Council for Medical Schemes reported 100% of private medical scheme reimbursements are code-based, which covers 9.2 million beneficiaries under ICD-10 and private procedural codes. Kenya’s Ministry of Health documented a 53% annual growth in coded claims since digitizing NHIF reimbursements in 2022. Sub-Saharan Africa is bypassing legacy systems entirely. This region’s coding market is not scaled by volume but by the velocity of systemic overhaul, which makes it the most politically driven and technologically agile coding frontier globally.

COMPETITIVE LANDSCAPE

The medical coding market is intensifying as technology vendors, BPO giants, and health systems vie to redefine coding from an administrative chore to a strategic asset. Competition pivots on three axes: algorithmic precision, workflow integration depth, and global labor arbitrage. Incumbents like 3M and Optum leverage EHR entrenchment and regulatory fluency, while agile entrants like Artifact Health and Streamline Health disrupt with NLP-native platforms. Offshore coding firms in India and the Philippines compete on cost but now invest in AI to retain relevance. Differentiation lies not in code assignment accuracy alone, but in predictive documentation guidance, real-time audit defense, and coded data repurposing, which makes the battlefield multidimensional and innovation velocity the ultimate arbiter of dominance.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global medical coding market include

- Aviacode Inc.

- Oracle Corporation

- Nuance Communications Inc.

- athenahealth

- Medical Record Associates LLC

- Maxim Healthcare Services Inc.

- 3M Company

- Parexel International Corporation

Top Players in the Medical Coding Market

- 3M HIS pioneers AI-integrated coding workflows, embedding natural language processing into clinical documentation to auto-suggest codes with audit-grade precision. In 2023, it launched its 360 Encompass Platform with real-time coder-assist modules, reducing query resolution time. It collaborates with academic medical centers to train coders on ICD-11 transition protocols and integrates risk-adjustment logic for value-based care models. Its recent partnership with Epic Systems embeds coding intelligence directly into EHR charting, minimizing post-discharge coding lag and positioning 3M as the architect of proactive, not reactive, coding infrastructure.

- OptumInsight dominates through end-to-end revenue cycle orchestration, coupling outsourced coding services with proprietary audit analytics and compliance engines. In 2024, deployed CoderAssist AI across a large U.S. hospital network; trains thousands of coders annually. It acquired Healthfinch to embed coding logic into physician documentation workflows, closing the clinical-coding gap. Optum trains over 8,000 coders annually via its virtual academy and leads CMS pilot programs on HCPCS modernization. Its strategy merges labor scalability with algorithmic governance, making it the de facto standard for enterprise coding resilience.

- Ciox Health, post-merger with Datavant, redefined coding as a data liquidity engine, not just a billing function. It connects 17,000 U.S. providers to payer and research ecosystems via coded clinical data exchange. In 2023, it launched “CodeFlow,” an API-driven platform that auto-maps EHR notes to ICD-11 and CPT in real-time, adopted by 400+ ASCs. It powers risk adjustment for Medicare Advantage plans by validating HCC codes against source documents. Its recent integration with Flatiron Health enables oncology-specific coding for clinical trials, transforming coded data into research-grade assets and expanding coding’s value beyond reimbursement.

Top Strategies Used by Key Market Participants

Leading players deploy algorithmic workforce augmentation, embedding AI to reduce coder cognitive load while preserving human oversight for compliance-critical decisions. They vertically integrate with EHR and payer systems to embed coding logic upstream in clinical workflows, minimizing post-discharge latency. Strategic acquisitions target niche coding automation firms and offshore BPOs to scale capacity amid labor shortages. They pioneer real-time audit engines that flag coding anomalies before claim submission, turning compliance from a cost center to a revenue protector. Finally, they reposition coding as a clinical data infrastructure by enabling reuse for research, population health, and value-based contracting, which transcends billing to become strategic health intelligence.

GLOBAL MEDICAL CODING MARKET NEWS

- In 2021, athenahealth announced the general availability of its new athenaOne Medical Coding solution.

- In 2021, Innoventrum, developers of QPro products and services, in collaboration with Dental Medical Billing, announced the launch of its premier credentialing program for dental-to-medical cross-coding and billing.

MARKET SEGMENTATION

This market research report on the global medical coding market has been segmented and sub-segmented based on component, classification system, end-user, and region.

By Component

-

In-house

-

Outsourced

By Classification System

-

International Classification of Diseases (ICD)

- Healthcare Common Procedure Code System (HCPCS)

By End-User

- Hospitals

- Diagnostic Centers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the Medical Coding Market and what factors are driving its growth?

The Medical Coding Market involves services and technologies that convert healthcare information into standardized codes for billing, recordkeeping, and analytics. Growth drivers include rising adoption of telemedicine, increasing healthcare digitization, and demand for accurate billing

2. What role does computer-assisted coding (CAC) play in the Medical Coding Market?

CAC improves coding accuracy and efficiency by leveraging AI and natural language processing to automate coding from clinical documentation

3. How does outsourcing impact the Medical Coding Market?

Outsourcing medical coding is a rapidly growing segment, helping healthcare providers reduce costs and improve compliance with complex coding standards

4. Which regions hold the largest shares in the Medical Coding Market?

North America dominates the market due to advanced healthcare infrastructure and reimbursement models, with Asia-Pacific as the fastest growing region

5. What are the main challenges faced by the Medical Coding Market?

Challenges include complex and ever-evolving coding guidelines, shortage of qualified coders, and data privacy concerns

6. How is artificial intelligence transforming the Medical Coding Market?

AI automates tedious coding tasks, enhances accuracy, reduces errors, and supports faster reimbursement cycles

7. Who are the key players operating in the Medical Coding Market?

Key companies include Optum360, Cerner Corporation, 3M Health Information Systems, MModal, and Conduent

8. How is telemedicine influencing the Medical Coding Market?

Telemedicine introduces new coding complexities that require updated codes and training, increasing demand for specialized coding solutions

9. What coding classification systems are most commonly used in the Medical Coding Market?

ICD-10 and CPT codes are the standard systems, with HCPCS also widely used for insurance billing and claims

10. What role do medical coding training and certification play in the market?

Training and certification ensure coders are up-to-date with guidelines, essential for compliance and avoiding claim denials

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com