Global K-12 Online Education Market Size, Share, Trends & Growth Forecast Report By Grade (Kindergarten, Elementary, Middle School and High School), Platform (Gamification, Mobile, Tablet, Laptops/Chrome Books and Others), Big Data & Analytics (LMS/ Virtual Learning Environments and Others), Deployment Mode (Cloud and On-Premises) & Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2024 to 2033

Global K-12 Online Education Market Size

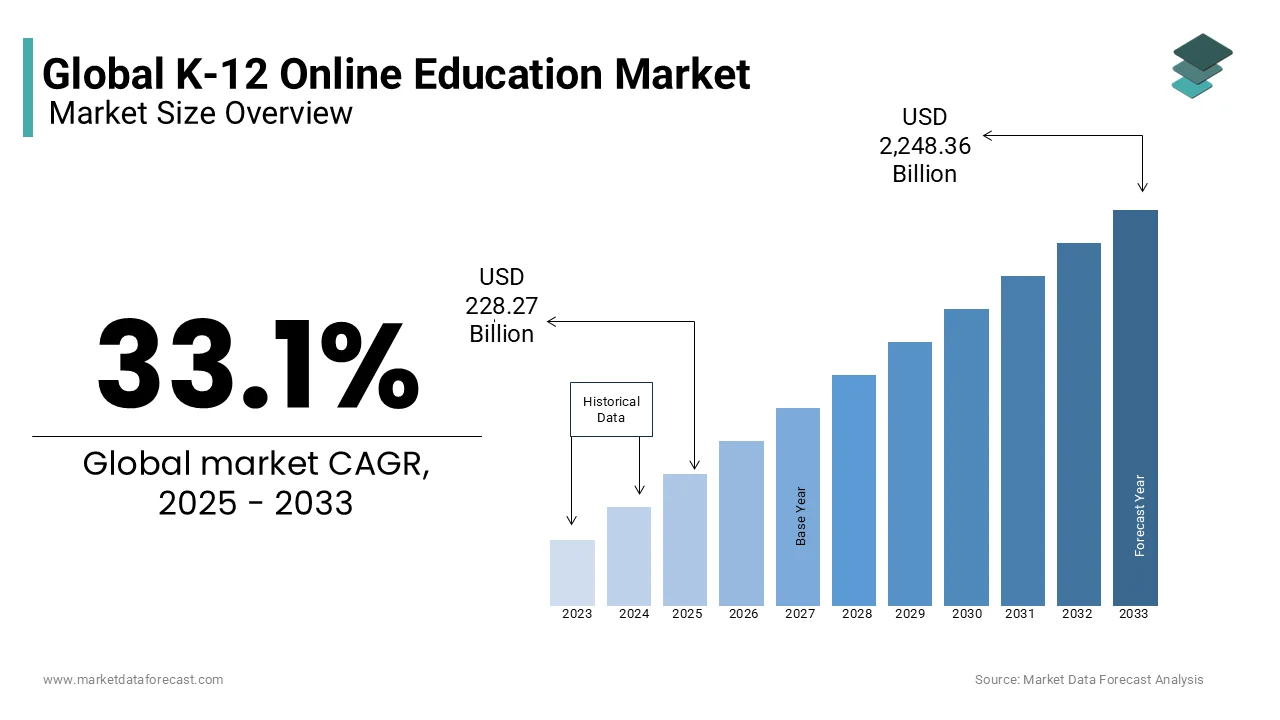

The global K-12 online education market was worth USD 171.5 billion in 2024. The global market size is expected to be worth USD 2,248.36 billion by 2033 from USD 228.27 billion in 2025, growing at a CAGR of 33.1% during the forecast period 2025 to 2033.

The K12 is an education management platform that offers online learning opportunities and curricula. The K12 course materials are aimed at students in kindergarten through grade 12. K–12 learning management systems focus on the classroom, teacher, and student experiences. They specialize in assisting instructors in developing and managing course materials, frequently concerning assessment management. LMSs also allow parents and parents to monitor their children's academic progress. The K-12 Online Learning Solutions provides online and blended solutions to schools and districts that deal with the issues of access, equity, individualized instruction, and future readiness. Students can interact with teachers and instructors directly through online Learning. In addition, the advanced technological platform, extensive digital courseware, and consultative assistance will enable students with a better future.

MARKET DRIVERS

Shifting traditional education systems to digital education systems in recent years is driving the growth of the K-12 online education market. Also, governments across the globe are promoting online K12 Learning owing to the emergence of the global pandemic COVID-19. In addition, globalization is leading to having a positive impact on the online education market. Online education enables students to communicate directly with teachers and instructors. Private organizations are increasing their initiative to promote online education. Hence, private organization is increasing their support to educational institutions to adopt digital learning technologies. Online Education offers innovative, affordable, and scalable solutions to students; owing to these benefits, the market is expected to boost the market.

Technological advancements in the Education system are supporting the market growth. The advancements include big data. The Growing demand for big data is increasing the popularity of learning analytics in the educational industry. In addition, the growing applications provide a personalized form of Learning. As a result, Key companies are developing innovative online educational platforms. Increasing acceptance of virtual Learning by teachers, students, and parents is likely to accelerate the market growth. Features such as time and cost-saving also offer students competency-based Learning. Moreover, the growing awareness among the people in the urban areas positively influences the market growth. Digital education systems are expected to benefit from artificial intelligence significantly. AI algorithms offer personalized content depending on student performance, profile, and active behavior. To track progress, it can also produce helpful content in the form of tests, quizzes, and videos.

MARKET RESTRAINTS

Infrastructure limitations hinder the growth of the k-12 online education market, the lack of measurability and the absence of personalization. Several schools, particularly those in rural areas, lack suitable technological equipment or systems to support a Learning Management System (LMS). Certain issues are due to the utilization of information and communication technologies (ICTs), which consist of insufficient internet networks and old systems. Moreover, the market growth rate is also affected by the restricted usage of hybrid or virtual formats for education. Likewise, in the United States, the biggest hurdle faced during the study was that the majority of schools in the country had used digital or hybrid formats for teaching or education in restricted manners, involving online teaching for either a single kind of course (for example, scheduling conflicts, credit recovery, college credit coursework, modern placement, other assignments or homework not accessible at the school) or an occasional substitute to in-person education to evade loss of academic learning hours because of climate (like, hurricanes).

MARKET CHALLENGES

Tracking professional development, teacher and student adaptation, current training and maintenance, safeguarding student data, device and internet access, administrative and policy obstructions, high cost of learning and limited availability of quality information are some of the key challenges derailing the expansion of the K-12 online education market. Apart from these issues, a clear national policy, restricted availability of internet and technology in rural places, absence of knowledge, power outages or scarcity and poverty and inequality are other factors decreasing the market growth rate. Moreover, there is an urgent need to prioritize investments by educational establishments and companies in digital training and infrastructure. Another challenge associated with this is the exorbitant initial costs of buying and setting up the learning management system, which can be a deterrent for some schools, impacting the market expansion. Furthermore, there are also barriers to applying asynchronous online education in developing markets. These involve restricted availability of technology and internet networks, language constraints, and the requirement for localized curriculum and content.

MARKET OPPORTUNITIES

Admission management, minimizing risks, raising learning outcomes and performance evaluation are some of the crucial areas which are being changed by digital technologies in the educational industry. These four are expected to be the focal point regarding the opportunities for the k-12 online education market. Moreover, asynchronous online education can assist in addressing some of the issues by providing access to educational training and resources and giving opportunities that may not be obtainable otherwise. According to UNESCO as well as World Bank data, since 2021, there has been an increase of 6 million in the number of out-of-school children, and as of now, the overall figure stands at 262 million. Also, sub-Saharan Africa holds nearly about 30% of total out-of-school children worldwide. 1in every 5 African children is not going to school, i.e., 19.7% percent. Only around 50% of children go to higher secondary school. However, since COVID-19, the majority of students can still afford a decent education even in this newly formed digital ecosystem because teachers and tutors have already begun to charge premium amounts for high-quality online educational content and more interactive ways of learning. Hence, it provides a huge population of lower- and lower-middle-class students who are devoid of learning and boosts market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

33.1% |

|

Segments Covered |

By Component, End User, Deployment, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Bettermarks, Scoyo, Languagenut, Beness Holding, Inc., New Oriental Education & Technology, AMBO, XUEDA, Ifdoo, CDEL, XRS, and others. |

SEGMENTAL ANALYSIS

By Grade Insights

The high school segment held the largest share of the global market in 2024 and is expected to hold the lead in the global market throughout the forecast period because they are more responsive to online Learning and can grab the activities quickly. In addition, the online school platform uses cutting-edge technology to make Learning engaging, while the virtual high school curriculum is based on the theories of how kids learn. Moreover, educational organizations or institutions with high schools are swiftly providing online learning through partnering with network companies because of escalating competition in the market. The research also found that around 10 million college-going students have opted for distance learning courses. Also, roughly 54% of college students chose distance education programs in 2022 against 75% in 2020 and approximately 1.1 million students were enrolled in the primary online colleges. Further, in 2022, more than 50% of college students registered for a virtual class. That totals up to about 10 million college students consuming online classes.

By Platform Insights

The LMS/ Virtual Learning Environment segment is currently the most prevailing category of the K-12 online education market. This can be attributed to the benefits of personalized learning, data-driven insights, and integration of other technologies. It simplifies educational methods, improving organization and productivity for both students and educators and facilitating an effortless learning curve. In addition, the emergence of artificial intelligence., augmented reality (AR) and Virtual Reality (VR) have significantly boosted the segment’s market size. Presently, 21 percent of teachers or professors utilize the chatbot to write or produce assignment prompts, with 4 percent creating a whole plan for lessons via its assistance. While those figures are modest, they only show that AI-powered solutions are forming an element of the entire learning curve. According to a study, it is expected that by the end of 2024, the number of users of LMS will be around 73.8 million.

By Deployment Mode Insights

The cloud segment spearheaded the K-12 online education market with more than 50% of the share of the global market in 2024. The sudden growth of cloud solutions under the realm of online K-12 learning can be credited to the affordability, versatility and scalability it provides. Moreover, with the drastic decline in the need for investments in on-premise hardware and the capability to ascend up or down based on requirements, cloud-based solutions are especially attractive to educational organizations running and functioning on tight budgets. Also, by 2023, more than 95% of ed-tech start-ups reported utilizing cloud-first policies and approaches, emphasizing the segment's vitality and market size.

REGIONAL ANALYSIS

North America and Europe are anticipated to record a significant share in the K-12 Online educational market during the forecast period. The presence of key market players, high disposable income, and adoption of advanced technology are pushing the market growth. As per the market reports, North America and Europe account for 40% of global market revenue. The United States is projected to showcase staggering growth in the North American K-12 online Education market. Factors such as the growing awareness about e-learning and technological advancements are boosting the market growth. In addition, the high penetration of the internet and AI technology is providing students with a new learning experience.

The Asia Pacific is predicted to be growing at a faster CAGR during the forecast period. The growing acceptance of online education and the increasing number of initiatives by regional governments support the market. Further, the emerging countries in the region, such as Japan, China, India, and Malaysia, are significantly contributing to the APAC regional market growth. The Indian K-12 Online Education market is witnessing rapid share in the Asia Pacific region as the recent COVID-19 outbreak has increased the demand for online education. In addition, private and government organizations are increasing their support to promote online education, positively influencing the country's market growth.

KEY MARKET PLAYERS

Companies such as Bettermarks, Scoyo, Languagenut, Beness Holding, Inc., New Oriental Education & Technology, AMBO, XUEDA, Ifdoo, CDEL and XRS are playing a leading role in the global k-12 online education market.

RECENT HAPPENINGS IN THE MARKET

- In December 2023, Veranda Learning Solutions, a prominent company of online education solutions, and Illinois Institute of Technology (Illinois Tech), a globally acclaimed research university, press released a strategic collaboration to provide technology-oriented courses and dual credit programs for K–12. This partnership intends to furnish students with the important knowledge and skills they require to propel them into the 21st-century environment.

MARKET SEGMENTATION

This research report on the global K-12 online education market has been segmented and sub-segmented based on component, end-user, deployment and region.

By Grade

- Kindergarten

- Elementary

- Middle School

- High School

By Platform

- Gamification

- Mobile

- Tablet

- Laptops / Chrome Books

- Others

- Big Data & Analytics

- LMS / Virtual Learning Environments

- Other

By Deployment Mode

- Cloud

- On-Premises

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What are the key factors driving growth in the global K-12 online education market?

Key growth factors include the rise in internet accessibility, increasing use of smart devices, greater demand for flexible learning solutions, growing investments in educational technology, and the ongoing digital transformation of traditional schooling.

What types of online education platforms are most popular in the K-12 market?

Popular online education platforms in the K-12 market include Learning Management Systems (LMS), video conferencing tools (like Zoom and Google Meet), gamified learning platforms, digital content libraries, and AI-powered personalized learning platforms. Companies like Google Classroom, Khan Academy, and Microsoft Teams are widely used.

What role does government policy play in the development of the K-12 online education market globally?

Government policies play a crucial role in shaping the development of the K-12 online education market. Many governments are actively promoting digital education through grants, subsidies, and partnerships with private ed-tech firms. Policies around curriculum digitalization, teacher training, and online safety standards also significantly impact market growth.

What technological innovations are driving the K-12 online education market?

Key technological innovations driving the market include artificial intelligence (AI) for personalized learning, virtual and augmented reality (VR/AR) for immersive experiences, machine learning for adaptive assessments, cloud computing for scalable learning environments, and the integration of big data for tracking student performance.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]