Global Immune Response Testing Market Size, Share, Trends & Growth Forecast Report By Test Type, Application, End-user and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Immune Response Testing Market Size

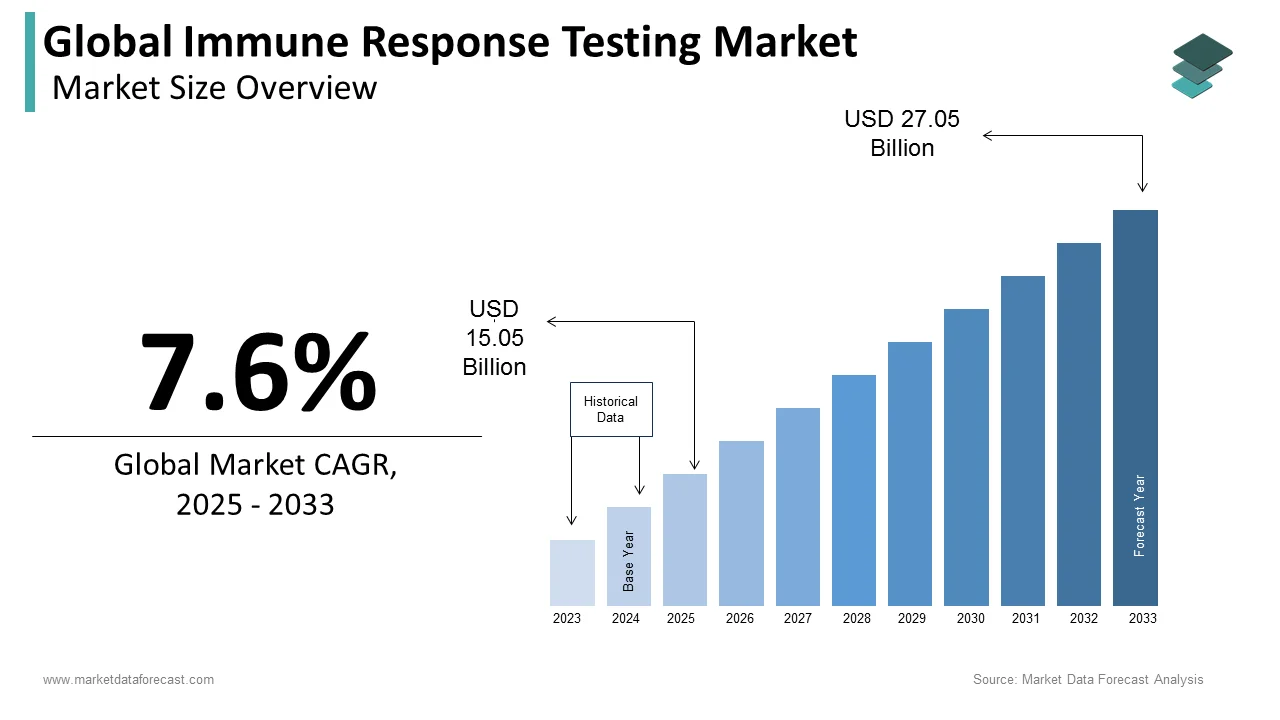

The global immune response testing market was valued at USD 15.05 billion in 2025. The global market is anticipated to grow at a CAGR of 7.6% from 2026 to 2034 and be worth USD 29.10 billion by 2034 from USD 16.19 billion in 2026.

Immune response testing constitutes a sophisticated diagnostic paradigm that quantifies the body’s immunological reactivity to specific antigens, pathogens, or therapeutic interventions. This domain encompasses diverse methodologies, including serological assays, cellular immunity assessments, and cytokine profiling, which collectively enable clinicians to evaluate both innate and adaptive immune functions. The clinical imperative for such testing has intensified significantly, driven by the necessity to monitor vaccine efficacy, manage autoimmune disorders, and optimize personalized immunotherapies in oncology. As per the World Health Organization, the global burden of infectious diseases remains substantial, with millions of new cases of tuberculosis and hepatitis reported annually, necessitating robust immune monitoring frameworks to track disease progression and treatment outcomes. Furthermore, according to the American Autoimmune Related Diseases Association, the rising prevalence of autoimmune conditions affects approximately 5% to 8% of the global population, which underscores the critical role of precise immune diagnostics in early detection and management.

MARKET DRIVERS

Rising Autoimmune Disease Prevalence Fuels Diagnostic Demand

The escalating global prevalence of autoimmune disorders is driving the expansion of the global immune response testing market. Autoimmune conditions, where the immune system mistakenly attacks healthy tissues, require precise diagnostic monitoring to guide therapeutic interventions and assess disease activity. According to the American Autoimmune Related Diseases Association, approximately 50 million Americans suffer from some form of autoimmune disease, representing a significant portion of the population that necessitates regular immunological assessment. This substantial patient pool drives consistent demand for advanced serological tests and cellular immunity assays that can detect specific autoantibodies and inflammatory markers. Furthermore, the complexity of these diseases often requires longitudinal monitoring, ensuring recurring revenue streams for diagnostic providers. As per data from the National Institutes of Health, the incidence of many autoimmune conditions has risen steadily over the past two decades, with type 1 diabetes and multiple sclerosis showing notable increases in younger demographics. This trend compels healthcare systems to adopt more sophisticated testing platforms capable of differentiating between various autoimmune etiologies. The clinical necessity to minimize false positives and negatives in such critical diagnoses further propels the adoption of high-sensitivity multiplex assays. Consequently, the growing burden of chronic immune-mediated diseases creates a sustained imperative for robust diagnostic infrastructure, fostering innovation in testing methodologies that offer greater specificity and faster turnaround times for clinicians managing complex patient cases.

Global Vaccination Programs Drive Need for Immune Monitoring

The widespread implementation of vaccination programs globally has significantly amplified the requirement for immune response verification and monitoring. Vaccines function by stimulating the body’s adaptive immune system to produce antibodies and memory cells, making the quantification of these responses essential for evaluating individual and population-level protection. According to the World Health Organization, immunization currently prevents between 3 and 5 million deaths every year from diseases like diphtheria, tetanus, pertussis, influenza, and measles, underscoring the massive scale of global vaccination efforts. This extensive coverage necessitates reliable post-vaccination serology to confirm seroconversion, particularly in immunocompromised individuals who may not mount an adequate defense. As per the Centers for Disease Control and Prevention, routine antibody titer testing is recommended for certain high-risk groups to ensure continued immunity against pathogens like hepatitis B and varicella. The recent global health crises have further accentuated the importance of measuring neutralizing antibodies to determine the duration and efficacy of vaccine-induced protection. Healthcare providers increasingly rely on quantitative immunoassays to make informed decisions regarding booster doses and personalized vaccination schedules. This shift toward evidence-based immunization strategies drives the integration of immune response testing into standard clinical workflows, creating a robust demand for scalable, accurate diagnostic solutions that can support large-scale public health initiatives and individual patient care simultaneously.

MARKET RESTRAINTS

High Operational Costs and Reimbursement Challenges Limit Accessibility

The substantial financial burden associated with advanced immune response testing is impeding the growth of the immune response testing market, particularly in resource-constrained healthcare settings. Sophisticated methodologies such as flow cytometry and multiplex cytokine assays require expensive instrumentation, specialized reagents, and highly trained personnel, driving up the cost per test. According to the World Bank, out-of-pocket expenditure accounts for nearly 18% of total health spending globally, which discourages patients from undergoing non-emergency diagnostic procedures. Furthermore, inconsistent reimbursement policies across different regions create financial uncertainty for healthcare providers. As per data from the Kaiser Family Foundation, coverage gaps for specialized diagnostic tests remain prevalent, with many insurance plans imposing strict prior authorization requirements or limiting the frequency of covered tests. This regulatory fragmentation forces laboratories to absorb higher operational costs or pass them on to patients, thereby reducing test utilization rates. In low-income countries, where health expenditure per capita often remains below 100 dollars annually, according to World Health Organization statistics, the high cost of imported diagnostic kits and equipment makes routine immune monitoring economically unfeasible. Consequently, the lack of standardized global pricing and adequate financial support mechanisms restricts market penetration, preventing equitable access to critical immune diagnostics for large segments of the population who would benefit most from early detection and monitoring of immune-related conditions.

Complexity of Sample Handling and Standardization Issues Hinder Reliability

The technical intricacies involved in sample collection, storage, and processing is further hampering the global market expansion, particularly cytokines and certain antibodies, which are highly labile and susceptible to degradation if not handled under strict temperature-controlled conditions. According to the Clinical and Laboratory Standards Institute, pre-analytical errors account for approximately 70% of all laboratory mistakes, with improper sample handling being a primary contributor. Variability in centrifugation speeds, time delays between collection and analysis, and freeze-thaw cycles can significantly alter test results, leading to false negatives or positives. As per findings published by the National Institutes of Health, inter-laboratory variability in immune assay results can exceed 20% due to differences in protocol adherence and calibration standards. This lack of harmonization undermines clinician confidence in test outcomes, prompting hesitation in relying on these diagnostics for critical treatment decisions. Additionally, the requirement for specialized logistics, such as cold chain transportation for biological samples, adds layers of complexity and cost, particularly in remote or rural areas. According to the International Federation of Clinical Chemistry, the absence of universally accepted reference ranges for many immune markers further complicates interpretation. These standardization challenges necessitate rigorous quality control measures that many smaller laboratories struggle to maintain, thereby limiting the scalability and reliability of immune response testing services across diverse healthcare environments.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Diagnostic Precision and Efficiency

The convergence of artificial intelligence with immune response testing presents a promising opportunity for the immune response testing market. Traditional manual interpretation of multiplex assays often struggles to identify subtle patterns across numerous biomarkers, whereas machine learning algorithms can detect nuanced correlations that predict disease progression or treatment response with superior accuracy. According to a study published in Nature Medicine, AI-driven models have demonstrated the ability to predict patient responses to immunotherapy with an accuracy rate exceeding 85%, significantly outperforming conventional clinical criteria. This technological synergy allows for the development of predictive diagnostic tools that can stratify patients more effectively, reducing trial-and-error prescribing. As per data from the International Data Corporation, global spending on artificial intelligence in healthcare is projected to reach 10 billion dollars by 2027, reflecting the intense investment in these capabilities. Furthermore, according to recent implementations in major clinical laboratories, AI facilitates the automation of routine analytical tasks, reducing turnaround times by up to 40%. This efficiency gain not only lowers operational costs but also enhances patient throughput. The ability to process vast datasets from electronic health records alongside immune profiling results creates a holistic view of patient health, fostering the emergence of next-generation diagnostic platforms. Consequently, the integration of computational biology into immune testing offers a pathway to highly personalized medicine, driving demand for smart diagnostic solutions that deliver actionable insights faster and more reliably than traditional methods.

Expansion of Point-of-Care Testing Devices Improves Accessibility and Speed

The miniaturization of diagnostic technologies has opened significant opportunities for point-of-care immune response testing, shifting critical assessments from centralized laboratories to bedside or community settings. Rapid, portable devices capable of measuring specific antibodies or inflammatory markers enable immediate clinical decision-making, which is crucial in emergency care and remote locations. According to the World Health Organization, approximately 50% of the global population lacks access to essential diagnostic services, highlighting the urgent need for decentralized testing solutions. Point-of-care systems address this gap by providing results within minutes rather than days, facilitating timely interventions for conditions like sepsis or acute allergic reactions. As per market analysis, the global point-of-care diagnostics market is expected to grow at a compound annual growth rate of 6.5% through 2030, driven by technological advancements in microfluidics and biosensors. These compact devices require minimal sample volumes, often just a finger-prick of blood, making them less invasive and more patient-friendly. Furthermore, the deployment of such devices in primary care clinics reduces the burden on hospital laboratories and lowers overall healthcare costs associated with delayed diagnoses. The increasing availability of connected point-of-care units also allows for real-time data transmission to central health systems, enhancing surveillance capabilities during outbreaks. This shift toward decentralized, rapid immune monitoring represents a pivotal opportunity to democratize access to advanced diagnostics and improve health outcomes in underserved regions.

MARKET CHALLENGES

Regulatory Heterogeneity and Compliance Burdens Impede Global Market Entry

The fragmented regulatory landscape across different geographical regions is challenging the growth of the immune response testing market. Each jurisdiction imposes distinct validation requirements, quality standards, and approval timelines, forcing companies to navigate complex bureaucratic hurdles that delay product launches and increase development costs. According to the European Commission, obtaining conformity marking for in vitro diagnostic devices under the new In Vitro Diagnostic Regulation requires extensive clinical performance studies, which can extend time-to-market by 12 to 18 months compared to previous directives. Similarly, as per the U.S. Food and Drug Administration, the premarket approval process for novel high-complexity assays involves rigorous scrutiny of analytical and clinical validity, often necessitating multiple rounds of data submission and review. This regulatory discordance creates significant operational inefficiencies, as manufacturers must maintain separate documentation and testing protocols for each target market. According to the World Health Organization, only 40% of low- and middle-income countries have functional regulatory authorities for medical products, further complicating distribution strategies in emerging economies. Consequently, smaller diagnostic firms often lack the resources to manage these multifaceted compliance demands, leading to market consolidation where only large multinational corporations can sustain the financial burden. This barrier stifles innovation by discouraging entry from niche players who might otherwise introduce specialized testing solutions, ultimately limiting the diversity of available diagnostic tools for clinicians worldwide.

Shortage of Skilled Personnel Limits Operational Capacity and Quality

A critical shortage of qualified laboratory professionals and immunology specialists severely restricts the scalability and reliability of immune response testing services, which is further challenging the global market expansion. Advanced techniques such as flow cytometry and next-generation sequencing require highly trained technicians who can operate sophisticated equipment and interpret complex data accurately. According to the American Society for Clinical Pathology, the United States faces a projected shortfall of over 10,000 medical laboratory scientists by 2030, exacerbated by an aging workforce and insufficient training programs. This deficit is even more pronounced in developing nations, where the World Health Organization reports a global density of health workers remains below the threshold of 4.45 skilled professionals per 1,000 population needed to achieve sustainable development goals. The lack of expertise leads to increased error rates, longer turnaround times, and inconsistent test results, undermining clinician confidence. As per data from the College of American Pathologists, laboratories experiencing staff shortages report a 15% increase in specimen rejection rates due to improper handling or processing errors. Furthermore, the rapid evolution of testing technologies outpaces the availability of continuous education programs, leaving many existing practitioners ill-equipped to handle new methodologies. This skills gap forces healthcare facilities to invest heavily in recruitment and training, straining already tight budgets. Without a robust pipeline of trained personnel, the industry struggles to meet rising demand, creating bottlenecks that hinder the widespread adoption of advanced immune diagnostics and compromise patient care quality.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Test Type, Application, End-user, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Abbott Laboratories, F. Hoffmann-La Roche Ltd, Euroimmun AG, Quest Diagnostics. |

SEGMENTAL ANALYSIS

By Test Type Insights

The enzyme-linked immunosorbent assay (ELISA) segment commanded the market by capturing 36.3% of the global market share in 2025. The dominance of the ELISA segment in the global market can be credited to its entrenched position in routine clinical diagnostics and research. The primary factor sustaining this dominance is the method’s unparalleled versatility and cost-efficiency for high-volume screening. According to the National Institutes of Health, ELISA remains the gold standard for detecting specific antibodies and antigens in autoimmune diseases, infectious diseases, and allergy testing due to its high sensitivity and specificity. The widespread availability of standardized kits for conditions such as HIV, hepatitis, and Lyme disease ensures consistent demand across hospital laboratories and diagnostic centers. As per data from the Centers for Disease Control and Prevention, millions of ELISA tests are performed annually in the United States alone for infectious disease surveillance, underscoring its critical role in public health infrastructure. Furthermore, the relatively low capital investment required for ELISA platforms compared to more complex molecular techniques makes it accessible to a broader range of healthcare facilities, including those in resource-limited settings. According to the World Health Organization, ELISA-based diagnostics are integral to national control programs for diseases like tuberculosis and dengue, where affordable and reliable screening is essential. This broad applicability, combined with a well-established regulatory framework and extensive clinician familiarity, solidifies ELISA’s position as the backbone of immune response testing, ensuring steady revenue generation despite the emergence of newer technologies.

On the other hand, the rapid test segment is projected to register the highest CAGR of 10.4% during the forecast period, owing to the urgent need for point-of-care diagnostics and decentralized testing solutions and the shifting healthcare paradigm toward immediate clinical decision-making, particularly in emergency and primary care settings. According to the World Health Organization, the deployment of rapid diagnostic tests has been instrumental in managing recent global health crises, with billions of units distributed worldwide to facilitate quick isolation and treatment decisions. This massive scale-up has normalized the use of rapid immune assays among both clinicians and patients, creating lasting demand for convenient testing options. As per findings from the Bill and Melinda Gates Foundation, rapid tests reduce the time to diagnosis from days to minutes, significantly improving patient outcomes in acute conditions like sepsis or severe allergic reactions. Furthermore, technological advancements in lateral flow assays have enhanced their sensitivity and specificity, making them viable alternatives to laboratory-based methods for certain applications. According to the International Federation of Clinical Chemistry, the integration of digital readers with rapid test strips allows for quantitative results, bridging the gap between qualitative screening and precise monitoring. This evolution, coupled with increasing consumer preference for home-based testing kits, propels the rapid test segment forward, offering substantial growth opportunities for manufacturers innovating in user-friendly, high-accuracy formats.

By Application Insights

The allergy testing segment accounted for 31.3% of the global market share in 2025. The growth of the allergy testing segment in the global market is driven by the escalating global burden of allergic disorders and the critical need for precise allergen identification. The dramatic rise in allergic sensitization across both developed and developing nations is further contributing to the expansion of the allergy testing segment in the global market. According to the World Allergy Organization, allergic diseases affect between 30% and 40% of the world’s population, with projections indicating that half of all Europeans will suffer from some form of allergy. This widespread prevalence necessitates routine diagnostic interventions, including specific IgE testing and skin prick tests, to manage conditions such as asthma, rhinitis, and food allergies effectively. As per data from the Centers for Disease Control and Prevention, the prevalence of food allergies among children in the United States increased by 50% between 1997 and 2011, creating a sustained demand for pediatric allergy diagnostics. Furthermore, the complexity of modern environments, characterized by increased exposure to pollutants and processed foods, has intensified immune reactions, prompting clinicians to rely on comprehensive immune profiling. According to the American Academy of Allergy, Asthma, and Immunology, accurate diagnosis is essential for implementing avoidance strategies and immunotherapy, which are cost-effective long-term management solutions. Consequently, the high volume of patients requiring initial diagnosis and periodic monitoring ensures that allergy testing remains the most lucrative application segment, supported by robust reimbursement policies and established clinical guidelines.

However, the cancer segment is anticipated to witness the fastest growth and is estimated to showcase a CAGR of 13.2% during the forecast period, owing to the revolutionary integration of immune checkpoint inhibitors and personalized cancer vaccines into oncology practice and the paradigm shift toward immuno-oncology, where treatment efficacy is directly linked to the patient’s immune profile. According to the American Society of Clinical Oncology, immunotherapies now account for over 50% of new drug approvals in oncology, necessitating rigorous pre-treatment biomarker testing to identify responsive patients. As per findings from the National Cancer Institute, tests measuring tumor mutational burden and PD-L1 expression have become standard of care for many solid tumors, driving substantial uptake of advanced immune response assays. Furthermore, the rising incidence of cancer globally amplifies this demand because the World Health Organization reports that cancer cases are expected to rise by 77% by 2050 due to aging populations and lifestyle factors. This demographic shift creates a larger patient pool requiring immune monitoring throughout their treatment journey. Additionally, according to researchers at the Memorial Sloan Kettering Cancer Center, the development of neoantigen-based vaccines relies heavily on detailed immune repertoire analysis. These advancements compel healthcare providers to adopt sophisticated multiplex platforms capable of detecting subtle immune changes, thereby fueling rapid market expansion in the oncology sector as precision medicine becomes increasingly mainstream.

By End-User Insights

The hospital segment led the market by holding 46.2% of the global market share in 2025. The growth of the hospital segment in the global market can be credited to the concentration of critical care units and emergency departments, where immediate immune diagnostics are vital for patient management. According to the American Hospital Association, there are over 6,000 registered hospitals in the United States alone, which collectively perform millions of laboratory tests annually, including extensive immune profiling for sepsis, autoimmune crises, and infectious diseases. The integration of advanced laboratory information systems within hospital networks allows for seamless ordering and result tracking, fostering high utilization rates of complex assays like flow cytometry and multiplex cytokine panels. As per data from the World Health Organization, hospitals in high-income countries account for the majority of specialized diagnostic procedures due to their access to skilled personnel and sophisticated instrumentation. Furthermore, the rising prevalence of chronic conditions requiring long-term monitoring ensures a steady stream of repeat testing within these facilities. According to the Centers for Medicare and Medicaid Services, hospital outpatient departments have seen a significant increase in volume for specialized diagnostic services, reflecting a shift toward centralized care models. This structural advantage, combined with robust reimbursement mechanisms for inpatient and outpatient services, solidifies the hospital sector’s leading position, enabling it to absorb the high capital costs associated with next-generation immune testing platforms while delivering comprehensive clinical insights.

However, the diagnostic centers segment is projected to register the highest CAGR of 12.5% during the forecast period, owing to the increasing trend of healthcare providers outsourcing laboratory services to specialized third-party facilities and the economic imperative for hospitals and clinics to reduce operational overheads by leveraging the economies of scale offered by large diagnostic chains. According to the Association for Diagnostics and Laboratory Medicine, independent laboratories process nearly 7 billion tests annually in the United States, demonstrating their critical role in the healthcare ecosystem. These centers offer faster turnaround times and broader test menus than many hospital-based labs, attracting referrals from smaller physician practices. As per findings from McKinsey and Company, the consolidation of the diagnostic industry has led to improved efficiency and standardization, making outsourced testing more reliable and cost-effective. Furthermore, the proliferation of standalone diagnostic centers in urban and semi-urban areas enhances patient accessibility, reducing wait times and improving convenience. According to the World Bank, private sector participation in healthcare diagnostics is growing rapidly in emerging economies, where public infrastructure often lacks capacity. This geographic expansion, coupled with the adoption of digital health platforms that facilitate remote sample collection and result delivery, positions diagnostic centers as the fastest-growing end-user segment, catering to a demand for efficient, high-quality immune response testing outside traditional hospital settings.

REGIONAL ANALYSIS

North America Immune Response Testing Market Analysis

North America held 36.7% of the global market share in 2025 and is anticipated to experience robust market demand and sustain its prominent position over the next few years as the region aggressively adopts precision medicine protocols and expands its specialized diagnostic frameworks. The United States, as the primary contributor, benefits from widespread adoption of precision medicine and substantial investment in biomedical research. According to the Centers for Medicare and Medicaid Services, national health expenditure in the United States reached 4.5 trillion dollars in recent years, facilitating the procurement of sophisticated diagnostic technologies. The presence of major diagnostic manufacturers and a favorable reimbursement landscape further accelerates market growth. As per data from the National Institutes of Health, federal funding for immunology research exceeds 10 billion dollars annually, fostering innovation in novel assay development. Additionally, the high prevalence of chronic conditions such as autoimmune diseases and cancer necessitates regular immune monitoring. According to the American Autoimmune Related Diseases Association, approximately 50 million Americans suffer from autoimmune disorders, creating a consistent demand for specialized testing. Regulatory support from the Food and Drug Administration for the rapid approval of innovative diagnostics also plays a crucial role. This combination of financial resources, technological leadership, and clinical need ensures North America remains the largest and most mature market for immune response testing globally.

Europe Immune Response Testing Market Analysis

Europe is expected to see reliable and structured market advancement over the next few years due to its highly integrated public healthcare networks and progressive shifts toward standardized clinical guidelines. The implementation of the In Vitro Diagnostic Regulation by the European Union has standardized quality requirements, enhancing confidence in diagnostic accuracy across member states. According to Eurostat, over 20% of the European Union population is aged 65 or older, a demographic segment with higher incidence rates of cancers and autoimmune conditions requiring frequent immune assessment. Germany and France are key contributors, boasting well-established public healthcare systems that prioritize comprehensive diagnostic coverage. As per the World Health Organization, Europe accounts for a significant proportion of global autoimmune disease cases, driving steady demand for serological and cellular immunity tests. Furthermore, strong government initiatives promoting early detection and personalized medicine have integrated immune profiling into standard care pathways. According to the European Federation of Pharmaceutical Industries and Associations, increasing collaboration between academia and industry is accelerating the translation of research into commercial diagnostic tools. This regulatory coherence, combined with demographic pressures and robust public health funding, sustains Europe’s prominent position in the global immune response testing landscape.

Asia Pacific Immune Response Testing Market Analysis

The Asia Pacific region is poised to chart exceptional growth vectors over the next few years as rapid economic transformations and large-scale hospital modernization programs fundamentally scale up laboratory capabilities. The Asia Pacific region is witnessing the most rapid growth, rising medical tourism, and increasing awareness of preventive diagnostics. Countries like China, India, and Japan are leading this expansion through significant government investments in hospital modernization and diagnostic laboratory networks. According to the World Bank, health expenditure in East Asia and the Pacific has grown at an average annual rate of 8% over the past decade, reflecting a concerted effort to improve healthcare access. The rising prevalence of infectious diseases such as hepatitis and tuberculosis, alongside growing rates of lifestyle-related autoimmune conditions, drives demand for accurate immune testing. As per data from the Ministry of Health in India, the diagnostic sector is expected to grow at a double-digit compound annual growth rate, supported by private sector participation and technological adoption. Japan’s aging population further contributes to market expansion, with high demand for cancer immunotherapy monitoring. According to the Asian Development Bank, improved insurance coverage in several Asia Pacific nations is reducing out-of-pocket expenses, making advanced diagnostics more accessible. This convergence of economic growth, demographic shifts, and policy support positions the Asia Pacific as a critical growth engine for the global immune response testing market.

Latin America Immune Response Testing Market Analysis

Latin American markets are projected to demonstrate steady but gradual improvements over the next few years as access to modernized urban diagnostic hubs expands across key territories. Brazil and Mexico are the primary markets, driven by expanding middle-class populations and greater private insurance penetration. According to the Pan American Health Organization, strategic regional health initiatives are increasingly focused on improving diagnostic infrastructure for maternal health and chronic disease management, which slowly paves the way for scalable immune screening platforms across primary healthcare networks.

COMPETITIVE LANDSCAPE

The competition in the immune response testing market is characterized by intense rivalry among established multinational corporations and emerging regional players, driven by rapid technological advancements and increasing demand for precision diagnostics. Major competitors differentiate themselves through innovation in assay sensitivity, automation capabilities, and integrated digital solutions. The market sees frequent strategic alliances and acquisitions as companies seek to expand their product portfolios and geographic reach, particularly in high-growth regions like the Asia Pacific. Regulatory compliance and quality standards serve as significant barriers to entry, favoring incumbents with robust infrastructure. However, niche players focusing on specialized applications, such as point-of-care testing or specific autoimmune markers, are gaining traction by offering cost-effective and accessible solutions. Price competition remains moderate, with value-added services and technical support playing crucial roles in customer retention. The dynamic landscape requires continuous investment in research and development to keep pace with evolving clinical needs and emerging pathogens, ensuring that only agile and innovative organizations sustain long-term competitiveness in this critical diagnostic sector.

KEY MARKET PLAYERS

Leading companies in the global immune response testing market include:

- Abbott Laboratories

- Hoffmann-La Roche Ltd

- Thermo Fisher Scientific

- Euroimmun AG

- Roche Diagnostics

- Danaher Corporation

- Quest Diagnostics

- Bio-Rad Laboratories Inc.

- Charles River

- Creative Diagnostics

TOP PLAYERS IN THE MARKET

- Thermo Fisher Scientific maintains a formidable presence in the Asia Pacific immune response testing landscape through its comprehensive portfolio of reagents, instruments, and services. The company actively strengthens its position by expanding manufacturing capabilities in key hubs like China and India, ensuring localized supply chain resilience. Recent strategic initiatives include launching advanced multiplex immunoassay platforms tailored for high-throughput clinical laboratories in the region. Thermo Fisher collaborates extensively with regional research institutions to support vaccine development and infectious disease surveillance, thereby embedding its technologies into public health frameworks. Their focus on digital integration allows seamless data management for Asian healthcare providers, enhancing operational efficiency. By offering robust technical support and training programs, the company ensures optimal utilization of its sophisticated diagnostic tools, fostering long-term partnerships with hospitals and diagnostic centers across diverse Asia Pacific markets.

- Danaher Corporation leverages its subsidiary brands, including Beckman Coulter and Leica Biosystems, to deliver innovative immune response testing solutions throughout the Asia Pacific region. The company focuses on automation and precision, recently introducing next-generation flow cytometers designed for complex immunophenotyping in oncology and autoimmune diagnostics. Danaher strengthens its market stance through strategic acquisitions of local distributors and technology firms, enabling deeper penetration into emerging economies such as Southeast Asia. Their commitment to sustainability and digital health aligns with regional regulatory trends, facilitating smoother product approvals. By establishing dedicated application centers in major cities, Danaher provides hands-on training for laboratory professionals, ensuring high-quality test outcomes. This customer-centric approach, combined with continuous product innovation, solidifies their reputation as a trusted partner for advanced immune diagnostics in the rapidly evolving Asia Pacific healthcare sector.

- Roche Diagnostics plays a pivotal role in the Asia Pacific immune response testing market by providing integrated solutions that combine hardware, reagents, and informatics. The company recently expanded its production facilities in Singapore and India to meet surging demand for high-quality immunoassays. Roche focuses on personalized healthcare, offering specialized tests for cancer immunotherapy monitoring and viral load assessment, which are critical in the region. Strategic partnerships with local governments have enabled Roche to support large-scale screening programs for infectious diseases, enhancing its public health impact. The introduction of cloud-based data analytics platforms allows Asian healthcare providers to manage large volumes of immune testing data efficiently. By prioritizing regulatory compliance and investing in local talent development, Roche ensures sustained growth and reliability, reinforcing its leadership in delivering precise and actionable immune diagnostic insights across the Asia Pacific region.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the immune response testing market predominantly employ strategies centered on technological innovation, strategic partnerships, and geographic expansion. Companies heavily invest in research and development to create high-sensitivity multiplex assays and automated platforms that reduce turnaround times. Collaborations with academic institutions and government bodies facilitate clinical validation and regulatory approvals, particularly in emerging markets. Mergers and acquisitions are frequently utilized to acquire niche technologies or expand distribution networks, enhancing product portfolios. Additionally, firms focus on digital integration, offering cloud-based data management solutions to improve laboratory efficiency. Localized manufacturing and supply chain optimization help mitigate logistical challenges, ensuring consistent product availability. These multifaceted approaches enable companies to maintain competitive advantages, address diverse clinical needs, and capitalize on the growing demand for precise immune diagnostics globally.

MARKET SEGMENTATION

This research report on the global immune response testing market can be segmented by test type, application, end-user, and region.

By Test Type

- Elisa Test

- RT-PCR

- Rapid Test

- Other

By Application

- Allergy Testing

- HIV disease

- Cancer

- Rheumatoid Arthritis

- Systemic Lupus Erythematosis

- Others

By End-User

- Hospital

- Diagnostic Centers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which regions dominate the global immune response testing market?

North America leads in the global immune response testing market followed by Europe, with Asia-Pacific growing the fastest during the forecast period

2. What are the major drivers of the global immune response testing market?

Drivers include rising zoonotic diseases, adoption of at-home immune tests, preventive healthcare trends, and growing investments in pandemic preparedness

3. What types of tests are included in the global immune response testing market?

The global immune response testing market comprises antibody testing, cytokine testing, cellular immunity testing, and complement system diagnostics

4. How is transplant compatibility testing impacting the global immune response testing market?

Transplant compatibility testing fuels demand in the global immune response testing market by ensuring successful organ matches and preventing rejection

5. What role does preventive healthcare play in the global immune response testing market?

Preventive healthcare adoption drives market expansion by increasing early disease detection via immune response tests globally

6. How important is at-home immune testing in the global immune response testing market?

Rising preference for at-home testing solutions accelerates growth in the global immune response testing market by improving patient convenience and access

7. Who are the major end-users in the global immune response testing market?

Hospitals, diagnostic labs, research institutes, and home care settings form the primary end users within the global immune response testing market

8. What challenges does the global immune response testing market face?

Challenges include high testing costs, regulatory hurdles, and the complicated interpretation of immune response results globally

9. How is technology advancing the global immune response testing market?

Advancements in multiplex immunoassays, molecular diagnostics, and automation are enhancing test specificity and throughput in the global immune response testing market

10. What are the emerging trends in the global immune response testing market?

Key trends include personalized immunotherapy monitoring, point-of-care testing, and integration with artificial intelligence in the global immune response testing market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com