Global Hematology Analyzers Market Size, Share, Trends & Growth Forecast Report Segmented By Product/Services (Flow Cytometry, Electrical Impedance, Laser Diffraction, Selection of Hematology Analyzers, Blood Test Parameters), Application and Region (North America, Europe, Asia Pacific, Latin America and Middle East & Africa), Industry Analysis From 2025 to 2033

Global Hematology Analyzers Market Size

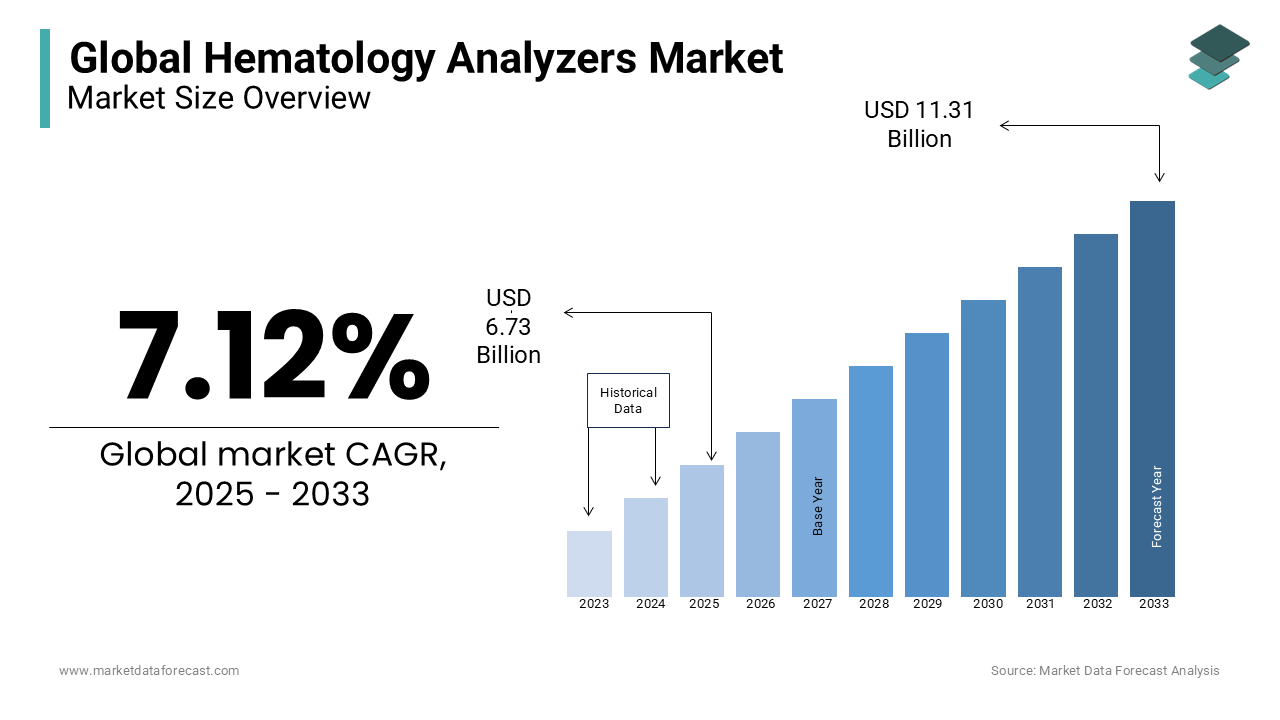

The global hematology analyzers market size was estimated at USD 6.31 billion in 2024 and is projected to reach USD 11.31 billion by 2033 from USD 6.73 billion in 2025, growing at a CAGR of 7.12% from 2025 to 2033.

Hematology analyzers are pivotal components of modern diagnostics with automated solutions for blood analysis. These devices are essential in medical laboratories for conducting complete blood counts (CBCs), identifying blood disorders, and supporting critical clinical decisions. Hematology analyzers have evolved from basic 3-part differential systems to advanced 6-part differential models that include reticulocyte counts and other specialized parameters with advancements in technology.

Emerging trends highlight a growing adoption of compact wherepoint-of-care analyzers alongside high-throughput systems in large hospitals. Additionally, AI integration is enhancing the accuracy and speed of blood sample analysis by minimizing manual intervention and errors. The rising prevalence of hematological disorders like anemia and leukemia continues to drive demand for these devices globally. Innovation in reagent compatibility and data connectivity further underscores their critical role in ensuring reliable diagnostics in both developed and developing healthcare markets.

MARKET DRIVERS

Rising Prevalence of Hematological Disorders

The increasing incidence of blood-related disorders, such as anemia, leukemia, and hemophilia, is a major driver of the hematology analyzer market. According to the World Health Organization (WHO), anemia affects over 1.62 billion people globally, with the highest prevalence in low- and middle-income countries. Additionally, leukemia accounts for 2.5% of all new cancer cases worldwide, as reported by GLOBOCAN. Hematology analyzers are essential for early detection, diagnosis, and monitoring of these conditions by enabling timely intervention and improved patient outcomes. This growing burden of hematological disorders is fueling demand for advanced diagnostic tools in hospitals and specialized clinics.

Expanding Healthcare Access in Emerging Markets

Improved healthcare infrastructure in developing countries is driving demand for hematology analyzers. Governments and organizations are investing in diagnostic capabilities to address public health challenges like anemia, which affects 40% of children under 5 in regions like South Asia and sub-Saharan Africa, according to WHO. The World Bank reports that healthcare spending in low- and middle-income countries has grown by 5-6% annually, with a focus on strengthening diagnostic services. Portable and cost-effective hematology analyzers are increasingly being deployed in rural and underserved areas, creating significant growth opportunities for manufacturers in these underpenetrated markets.

MARKET RESTRAINTS

High Cost of Advanced Hematology Analyzers

The high cost of advanced hematology analyzers is a significant barrier, particularly in low- and middle-income countries (LMICs). According to the World Bank, healthcare spending in LMICs remains limited with many countries allocating less than 5% of their GDP to healthcare. This financial constraint limits the adoption of high-end analyzers, especially in rural and underfunded healthcare facilities. As a result, many regions rely on outdated or manual diagnostic methods is hindering market growth and access to advanced diagnostic solutions.

Lack of Skilled Laboratory Technicians

The effective operation of hematology analyzers requires trained laboratory technicians, which are in short supply in many regions. The World Health Organization (WHO) estimates a global shortage of 18 million healthcare workers with the most acute gaps in LMICs. This shortage is particularly pronounced in specialized fields like laboratory diagnostics. The full potential of advanced hematology analyzers cannot be realized without skilled personnel that leads to underutilization and inefficiencies This restraint is exacerbated in rural areas, where training programs and educational resources are often lacking which further limiting the adoption and effectiveness of these devices.

MARKET OPPORTUNITIES

Development of Portable and Point-of-Care (POC) Hematology Analyzers

The demand for portable and point-of-care (POC) hematology analyzers is growing, especially in remote and resource-limited settings. These devices enable rapid, on-the-spot diagnosis, reducing the need for centralized laboratories. Portable hematology analyzers are particularly valuable in combating diseases like anemia, which affects 40% of children under 5 in developing regions as per a report by WHO. Manufacturers can capitalize on this trend by developing cost-effective, user-friendly devices tailored to low-resource settings.

Integration of Artificial Intelligence (AI) and Automation

The integration of AI and automation into hematology analyzers offers significant opportunities to enhance diagnostic accuracy and efficiency. AI-powered systems can analyze complex data patterns, reducing human error and improving diagnostic precision. For example, the National Institutes of Health (NIH) highlights that AI can improve diagnostic accuracy by 20-30% in certain medical applications. Additionally, automation can streamline workflows in high-volume laboratories, where the Centers for Disease Control and Prevention (CDC) reports that 70% of medical decisions rely on laboratory test results. By incorporating AI and automation, hematology analyzers can meet the growing demand for faster, more reliable diagnostics.

MARKET CHALLENGES

Stringent Regulatory Approvals and Compliance

The hematology analyzer market faces significant challenges due to stringent regulatory requirements for medical devices. Obtaining approvals from agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) can be time-consuming and costly. For instance, the FDA’s approval process for medical devices can take 6-12 months or longer, delaying product launches. Additionally, compliance with evolving regulations, such as the In Vitro Diagnostic Regulation (IVDR) in the EU, increases operational complexity. These hurdles can slow down innovation and limit market entry for smaller manufacturers, impacting overall market growth.

Maintenance and Operational Costs

Hematology analyzers require regular maintenance and calibration to ensure accuracy, leading to high operational costs. According to the World Health Organization (WHO), many healthcare facilities in low- and middle-income countries struggle with limited budgets, making it difficult to afford ongoing maintenance. Additionally, the cost of reagents and consumables can be prohibitive, with some labs spending 30-40% of their budget on these supplies. This financial burden can deter healthcare providers from adopting advanced hematology analyzers, particularly in resource-constrained settings, limiting market penetration and accessibility.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product/services, Application, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leader Profiled |

Sysmex Corporation, Beckman Coulter, Inc., Abbott Laboratories, HORIBA, Ltd., Siemens Healthineers, Mindray Medical International Limited, Bio-Rad Laboratories, Inc., Boule Diagnostics AB, Roche Diagnostics, Nihon Kohden Corporation. |

SEGMENTAL ANALYSIS

By Product/Services Insights

Electrical Impedance is the largest segment with 40% of the global market share. This dominance is attributed to the widespread adoption of electrical impedance technology in hematology analyzers, which offers reliable and cost-effective cell counting and sizing. Its importance lies in providing accurate complete blood counts (CBCs) which is essential for diagnosing conditions like anemia and infections. The simplicity and efficiency of electrical impedance methods have made them a standard in many clinical laboratories worldwide.

Conversely, Flow Cytometry is the fastest-growing segment with a Compound Annual Growth Rate (CAGR) of around 8% in the global market. This rapid growth is driven by the technology's ability to provide detailed cell analysis, including immunophenotyping and detection of rare cell populations, which is crucial in diagnosing hematological malignancies such as leukemia and lymphoma. The increasing demand for precise and comprehensive blood analysis with advancements in flow cytometry instruments shall expand the role in modern diagnostics.

By Application Insights

Anemia represents the largest application segment by accounting 35% of the global market share. This prominence is due to the high global prevalence of anemia, affecting over 1.62 billion individuals, particularly in developing regions. Hematology analyzers are essential for diagnosing and monitoring anemia by providing complete blood counts (CBCs) and red blood cell indices, facilitating timely intervention and management.

The Blood Cancer segment is solely to have a Compound Annual Growth Rate (CAGR) of 7.5% during the forecast period 2025-2033. This acceleration is driven by the increasing incidence of hematological malignancies such as leukemia, lymphoma, and myeloma. Hematology analyzers play a crucial role in detecting abnormal cell populations and monitoring treatment efficacy, making them indispensable in oncology diagnostics. Advancements in analyzer technology shall improve patient outcomes with the flow cytometry integration and their capability to identify and quantify malignant cells.

REGIONAL ANALYSIS

North America dominates the global hematology analyzer market, holding approximately 35-40% of the market share in 2024. According to the Centers for Disease Control and Prevention (CDC), the U.S. has seen a steady rise in the prevalence of blood disorders, such as anemia and leukemia, with over 1.5 million new cases of blood cancers reported annually, driven by advanced healthcare infrastructure and high adoption of automated diagnostic tools. The U.S. accounts for over 85% of the regional market share with significant healthcare spending, which reached $4.3 trillion in 2022 according to Centers for Medicare & Medicaid Services. Canada also contributes to the growth, with its aging population projected to reach 25% of the population over 65 by 2030 as per Statistics Canada is driving demand for hematology analyzers. Major players like Abbott Laboratories and Beckman Coulter further strengthen the region's market position.

Europe is the second-largest market for hematology analyzers. According to the European Centre for Disease Prevention and Control (ECDC), the region has seen a rise in chronic diseases, including blood disorders with over 1.2 million new cancer cases reported annually. The market is projected to grow significantly with the government initiatives and increasing healthcare expenditure. Germany leads the region by contributing over 20% of the European market share by its advanced medical device industry. The UK and France also play significant roles, with the UK’s National Health Service (NHS) investing heavily in diagnostic technologies. According to Eurostat, healthcare spending in the EU reached €1.2 trillion in 2022, further fueling market growth. The region’s focus on early disease detection and the adoption of cost-effective analyzers in rural areas will drive future performance.

The Asia-Pacific region is swiftly emerging in hematology analyzers market by growing with a CAGR of 8% during the forecast period. According to the World Health Organization (WHO), the region faces a high burden of blood disorders, with over 60% of global anemia cases occurring in Asia. Improving healthcare infrastructure and rising healthcare spending are key factors promoting the growth rate of the market. China dominates the regional market, accounting for over 40% of the share, with its healthcare expenditure reaching $1.2 trillion in 2022 according to National Health Commission of China. India is also a key contributor with its diagnostic market projected to grow at 10% annually, according to the Indian Brand Equity Foundation (IBEF). Japan and South Korea are contributing the significant opportunities for the market with the advanced healthcare systems and high adoption of innovative technologies. The region’s growth is further fueled by government initiatives to modernize healthcare systems and the increasing prevalence of chronic diseases.

Latin America market is projected to grow healthy, driven by increasing healthcare investments and the expansion of private diagnostic laboratories. According to the Pan American Health Organization (PAHO), the region faces a growing burden of blood disorders with anemia affecting over 20% of the population in some countries. The Brazil is the largest market in the region, accounting for over 40% of the share, with its healthcare expenditure reaching $200 billion in 2022 as per Brazilian Ministry of Health report. Mexico is another key contributor, with its diagnostic market growing at 6% annually, according to INEGI (National Institute of Statistics and Geography). Despite economic challenges, the region’s growth is supported by government initiatives to improve healthcare access and the rising adoption of automated hematology analyzers.

The Middle East and Africa market is expected to grow significantly by increasing healthcare investments and government initiatives to improve healthcare infrastructure. According to the World Health Organization (WHO), the region faces a high burden of infectious diseases, such as malaria and anemia, with over 200 million cases reported annually. The UAE leads the region, with healthcare spending reaching $20 billion in 2024, according to Dubai Health Authority. Saudi Arabia is another key market, with its Vision 2030 initiative aiming to modernize healthcare systems. South Africa also contributes to the growth, with its diagnostic market expanding due to the rising prevalence of blood disorders. Despite being underdeveloped, the region shows significant growth potential, particularly in urban areas where access to advanced diagnostic tools is improving.

KEY MARKET PLAYERS

Sysmex Corporation, Beckman Coulter, Inc., Abbott Laboratories, HORIBA, Ltd., Siemens Healthineers, Mindray Medical International Limited, Bio-Rad Laboratories, Inc., Boule Diagnostics AB, Roche Diagnostics, Nihon Kohden Corporation are some of the key market players.

MARKET SEGMENTATION

This research report on the hematology analyzers market is segmented and sub-segmented into the following categories.

By Product/Services

- Flow Cytometry

- Electrical Impedance

- Laser Diffraction

- Selection of Hematology Analyzers

- Blood Test Parameters

By Application

- Anemia

- Blood Cancer

- Infection

- Autoimmune and Genetic Blood Diseases

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What factors are driving the growth of the hematology analyzers market?

Key factors driving market growth include the rising prevalence of blood-related disorders, advancements in technology, increasing demand for point-of-care testing, and the expansion of healthcare infrastructure globally.

Which regions dominate the hematology analyzers market?

The regions dominating the hematology analyzers market include North America, due to advanced healthcare systems and high technology adoption; Europe, with its strong presence of diagnostic laboratories; and Asia-Pacific, with rapid healthcare development and an increasing prevalence of diseases.

What challenges are faced in the hematology analyzers market?

Challenges in the hematology analyzers market include the high costs of advanced devices, limited access in low-income regions, and the need for skilled personnel for the operation and maintenance of the equipment.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]