Global Healthcare/Medical Simulation Market Size, Share, Trends & Growth Forecast Report By Products & Services (Healthcare Anatomical Models, Web-Based Simulators, Healthcare Simulation Software and Simulation Training Services), End-User, and Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Industry Analysis From 2025 to 2033.

Healthcare/Medical Simulation Market Size

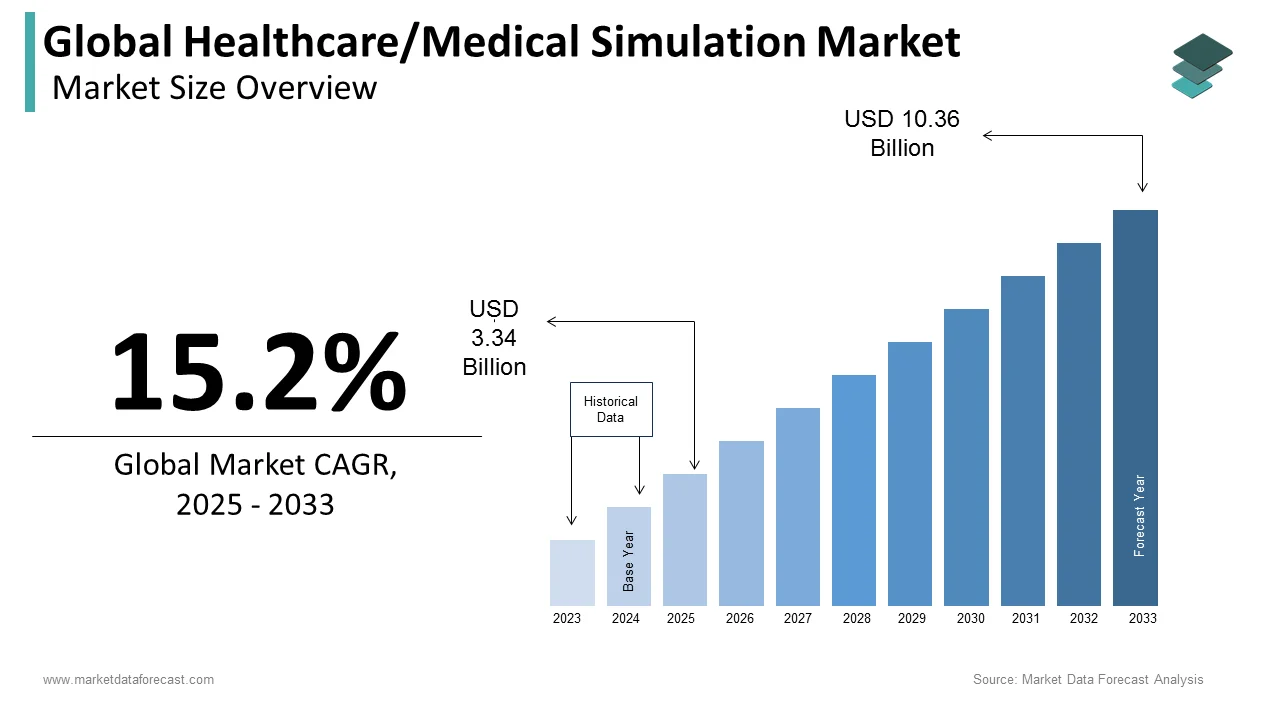

The size of the global medical simulation market was worth USD 2.9 billion in 2024. The global market is anticipated to grow at a CAGR of 15.2% from 2025 to 2033 and be worth USD 10.36 billion by 2033 from USD 3.34 billion in 2025.

Medical simulation is a new approach for training healthcare professionals using advanced educational technologies. Human-simulated patients, animated simulants, holographic simulants, or their combinations are used in medical simulation to create an artificial representation of real-life clinical scenarios. It also aids in the management of situations that arise in clinical practice. Healthcare practitioners can now simulate procedures to teach learners securely and efficiently due to technical advancements in communication, research, and education. Medical simulation has many uses in educational institutions, research centers, healthcare facilities, and military services.

Reliability of the software, interactive, and reality technologies are used in medical simulation. Haptic technology employs the sense of touch to help in practical and multisensory learning by applying forces, vibrations, and movements. On the other side, virtual and reality technology uses a computer-simulated world. It enables surgeons to practice surgery without having to operate on real people. Students’ confidence and skills improve because of simulation. It is also an essential method for demonstrating crisis resource management abilities. The simulation will benefit the multidisciplinary team, individual learners, and the hospital. Medical training institutes are driving the demand, and hospitals in North America primarily focus on standardizing their teaching practices to improve patient safety.

MARKET DRIVERS

The growing population infected by various diseases and the growing usage of simulation in healthcare propel the medical simulation market growth. Increased concern around patient safety, rising healthcare costs, and increasing demand for minimally invasive treatments are anticipated to promote market growth during the forecast period. According to the Institute of Medicine, medical errors during treatment cause between 46,000 and 98,000 deaths annually. This has increased the need for medical simulation as it allows physicians and surgeons to understand procedures better and prevent potentially fatal errors during treatment or surgery.

Technological advancements in medical simulations and increased adoption of animated and web-based simulations are expected to contribute to the growth of the medical simulation market. Advantages such as specialized training in complicated and standard situations drive up demand for medical simulation. In addition, the increasing importance of various health apps, medical visualization, surgical robots, and preventive medicines encourages the increased adoption of advanced healthcare simulation technologies.

The scarcity of healthcare professionals, growing awareness of simulation education in developing countries, and technological advances are expected to generate lucrative opportunities for market players. Surgeons are switching from open surgery to medical simulation, primarily laparoscopy and robotic surgery. However, effective medical simulation procedures, especially laparoscopy, and robotic surgery necessitate skilled surgeons. Cholecystectomy, appendectomy, gastric bypass, ventral hernia repair, colectomy, prostatectomy, tubal ligation, hysterectomy, and myomectomy procedures have rapidly adopted the medical simulation. The METIman simulator, built by CAE simulators, is one of the most powerful and realistic simulators in recent times. The growing geriatric population in the United States and Canada and the rising number of hospital admissions are expected to increase patient safety and adequate treatment demand, which will likely boost the regional healthcare simulation market's growth. The rising demand for minimally invasive surgical procedures in the Healthcare Simulation Market is expected to create lucrative opportunities.

MARKET RESTRAINTS

The high-end cost of medical simulators is hampering the medical simulation market growth. The budget constraints have led to less investment in the development of these types of simulation systems. The lack of technology in healthcare facilities in emerging countries hinders the market's growth and, if not rectified, will continue to do so. In addition, the lack of medical simulator-making companies in certain areas has led to less demand for these products. Still, this challenge can be overcome by better government initiatives and the entry of new market players. Lack of funding, less time for simulation activities, release from the work environment, and a lack of management interest are challenges to hospitals implementing simulation products and services. In addition, operational difficulties are major factors expected to limit market growth to some degree during the forecast period.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Products and Services, End User, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

CAE Inc., 3d Systems, Laerdal Medical, Gaumard Scientific Company, Kyoto Kagaku, Limbs & Things, Mentice Ab, Simulab Corporation, Simulaids, Intelligent Ultrasound Group Plc, Operative Experience, Inc. |

SEGMENTAL ANALYSIS

By Products & Services Insights

The healthcare anatomical model segment had the largest market share in 2024 and is expected to grow at a promising rate during the forecast period. Healthcare anatomical models can be further divided into patient simulators, task trainers, interventional/surgical, endovascular, ultrasound, dental, and eye simulators. The primary factor driving the healthcare anatomical model segment is the wide variety of applications of such models in several fields, such as academics, training & practicing in hospitals and military organizations. Among these divisions, the patient simulator is expected to grow faster during the forecast period. The key factor for the patient simulator's growth is the various advantages like better understanding and gaining knowledge the patient simulator offers. Therefore, it is helpful in military organizations and academic institutes.

The web-based simulator segment is expected to grow the fastest during the forecast period. The main reason for high growth is the Internet service available in most areas. Other advantages of web-based simulators are a predictable environment for learning and controlled access to simulation procedures. In addition, the increase in population and improvement of healthcare facilities will eventually propel the market growth throughout the forecast period.

By End-User Insights

The academic institutes had the highest market share in 2024 and are expected to grow at a promising CAGR during the forecast period. The main factor driving the growth of this sub-segment is the increasing importance of patient safety. In addition, the lack of appropriate knowledge for minimally invasive surgeries is expected to increase medical training demand in academic institutes during the forecast period.

The hospital segment is expected to grow with the highest CAGR during the forecast period. The availability of the latest healthcare technology in hospitals to provide the best possible treatment and the growing adoption of medical simulation are boosting the growth of the hospital segment. In addition, the large variety of medical simulators and increasing demand for minimum-invasive procedures are expected to contribute to this segment's growth positively.

REGIONAL ANALYSIS

North America dominated the global simulator market among all regions in 2024 and is expected to continue the dominating trend throughout the forecast period. The market in North America is driven by rising medical training institutes and hospitals, which greatly emphasize patient safety. In addition, the rise in the geriatric population in North American countries such as USA and Canada is further favoring the healthcare simulation market in this region. The U.S. medical simulation market had a significant share in North America in 2024.

Europe is expected to be the second-largest market during the forecast period. The increase in the geriatric population and healthcare facility improvement is the primary positive contributing factors. In addition, the rising government initiatives will make people more aware of the medical simulation market and thus boost market growth.

The Asia-Pacific region will exhibit the highest growth rate during the forecast period. The rising demand for medical simulation and increased spending on healthcare facilities will drive the market's growth. In addition, ease of doing business due to low cost and more labor will help Asian countries to grow in this field. The increasing population in India and China is also a major contributing factor to the growth rate of the medical simulation market in the Asia-Pacific.

Latin America is estimated to grow at a notable CAGR during the forecast period.

The market in the Middle East and Africa is expected to showcase a moderate CAGR during the forecast period.

KEY MARKET PARTICIPANTS

CAE Inc., 3d Systems, Laerdal Medical, Gaumard Scientific Company, Kyoto Kagaku, Limbs & Things, Mentice Ab, Simulab Corporation, Simulaids, Intelligent Ultrasound Group Plc, Operative Experience, Inc., Surgical Science Sweden AB, Cardionics Inc., Virtamed AG, Synbone AG, Vrmagic Holding AG., Ossimtech, HRV Simulation, Synaptive Medical, and Inovus Medical, are some of the companies playing a leading role in the global medical simulation market.

RECENT MARKET DEVELOPMENTS

- In September 2020, Vexos. Inc. received Health Canada Approval for the MVM Ventilator.

- Canada Aviation Electronics retools mannequin medical simulator in August 2020 to build ventilators for COVID-19 fight.3D Systems Delivers New Innovation for its VSP® System receives 510(k) Clearance for Improved Patient-Matched Surgical Guidance in October 2020.

MARKET SEGMENTATION

This market research report on the global medical simulation market has been segmented and sub-segmented based on products and services, end-user, and regions.

By Products & Services

- Healthcare Anatomical Models

- Web-Based Simulators

- Healthcare Simulation Software

- Simulation Training Services

By End-User

- Academic institutes

- Military organizations

- Hospitals

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

How much was the global medical simulation market worth in 2024?

Companies playing a leading role in the medical simulation market are CAE Inc., 3d Systems, Laerdal Medical, Gaumard Scientific Company, Kyoto Kagaku, Limbs & Things, Mentice Ab, Simulab Corporation, Simulaids, Intelligent Ultrasound Group Plc, Operative Experience, Inc., Surgical Science Sweden AB, Cardionics Inc., Virtamed AG, Synbone AG, Vrmagic Holding AG., Ossimtech, HRV Simulation, Synaptive Medical, and Inovus Medical.

Who are the leading players in the medical simulation market?

The Asia-Pacific medical simulation market is anticipated to be worth USD 10.36 billion by 2033.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]