Global Healthcare IT Consulting Market Size, Share, Trends & Growth Forecast Report By Type, End-user, and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Healthcare IT Consulting Market Report Summary

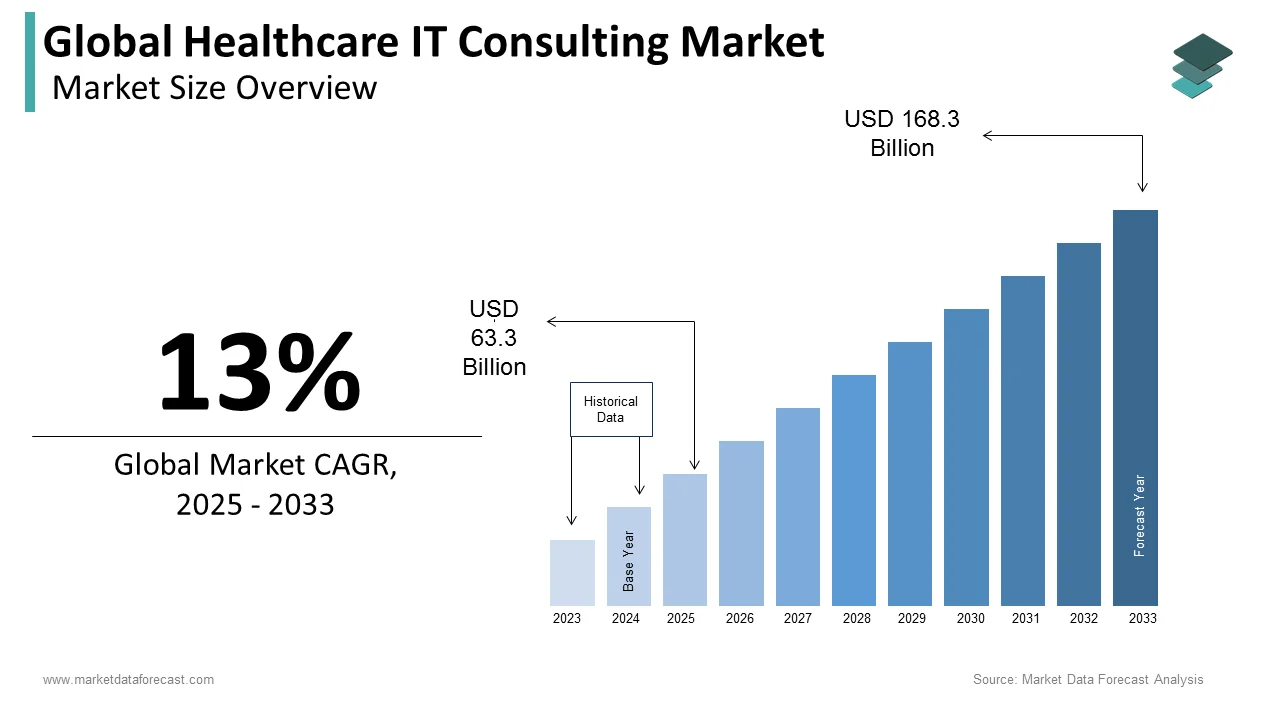

The global healthcare IT consulting market was valued at USD 63.3 billion in 2025 and is projected to grow from USD 71.53 billion in 2026 to USD 190.16 billion by 2034, registering a strong CAGR of 13% from 2026 to 2034. Market growth is driven by increasing digital transformation across healthcare systems, rising adoption of electronic health records (EHRs), and growing demand for data-driven healthcare management solutions. Healthcare providers are increasingly relying on IT consulting services to improve operational efficiency, strengthen cybersecurity frameworks, optimize patient care delivery, and ensure regulatory compliance. The expansion of cloud computing, AI-enabled healthcare analytics, and telehealth platforms is further accelerating market growth globally.

Key Market Trends

- Increasing adoption of electronic health records (EHR) and digital healthcare platforms.

- Rising demand for cybersecurity, compliance, and healthcare data protection consulting services.

- Growing integration of AI, cloud computing, and advanced analytics into healthcare systems.

- Expansion of telehealth and remote patient monitoring infrastructure.

- Strengthening focus on interoperability and value-based healthcare models.

Segmental Insights

- Based on type, the healthcare business process management segment dominated the healthcare IT consulting market in 2025 by accounting for 28.7% market share, driven by increasing demand for workflow optimization, operational efficiency, and cost reduction strategies.

- Based on end user, the hospitals and ambulatory care centers segment led the market by capturing 37.5% share in 2025, supported by rising investments in digital healthcare infrastructure and patient management systems.

Regional Insights

The global healthcare IT consulting market is witnessing strong growth across major regions, supported by healthcare modernization initiatives, increasing digital adoption, and rising investments in healthcare analytics and infrastructure.

- North America was the top performer in 2025 with 39.7% market share, driven by advanced healthcare infrastructure, high healthcare IT spending, and rapid adoption of digital health technologies.

- Europe held a significant position due to advanced healthcare systems, strong digital infrastructure, and coordinated policy initiatives supporting healthcare technology adoption across member states.

- Asia-Pacific is emerging as a rapidly expanding market, supported by increasing healthcare digitization, expanding hospital infrastructure, and growing government investments in healthcare modernization.

Competitive Landscape

The global healthcare IT consulting market is characterized by intense competition among technology companies, consulting firms, and healthcare software providers focusing on digital transformation and operational optimization solutions. Market players are emphasizing cloud integration, AI-driven healthcare analytics, cybersecurity enhancement, and interoperability services to strengthen market positioning. Strategic collaborations, acquisitions, and investments in healthcare digitalization initiatives are shaping competitive dynamics across the market.

Prominent companies operating in the global healthcare IT consulting market include Epic Systems Corporation, General Electric, Koninklijke Philips N.V., Cerner Corporation, Cisco, Cognizant, Genpact, Allscripts Healthcare LLC, Atos SE, HCL Technologies Limited, Hexaware Technologies, Infor, IBM Corporation, Deloitte Touche Tohmatsu Limited, Accenture, Infosys Limited, Larsen & Toubro Limited, Microsoft, McKesson Corporation, NTT Data, Inc., Oracle, SAP SE, Tata Consultancy Services Limited, and Wipro Limited.

Global Healthcare IT Consulting Market Size

The global healthcare IT consulting market was worth US$ 63.3 billion in 2025 and is anticipated to reach a valuation of US$ 190.16 billion by 2034 from US$ 71.53 billion in 2026, and it is predicted to register a CAGR of 13% during the forecast period 2026 to 2034.

Healthcare IT consulting is the practice of advising medical organizations, like hospitals and clinics, on how to select, implement, and optimize technology systems. Within the European context, this sector operates amid profound structural pressures, as the region confronts a documented deficit of roughly 1.2 million doctors, nurses, and midwives across the broader European zone, according to the Health at a Glance: Europe 2024 report. The World Health Organization emphasizes that structural staffing gaps across the continent will continue to worsen by 2030, intensifying the operational imperative for technology-enabled care delivery and workforce optimization models. Digital literacy variations across populations present another critical dimension, as data from the European Commission indicates that only 56 percent of EU citizens aged 16 to 74 years possessed at least basic overall digital skills, falling 24 percentage points short of the 80 percent Digital Decade target for 2030. Healthcare providers increasingly rely on external consulting expertise to navigate complex regulatory environments, including the General Data Protection Regulation, which governs health data processing across 27 member states. As per briefings from the European Parliamentary Research Service, the healthcare sector faces mounting pressure to modernize its digital and physical infrastructure while strictly maintaining patient safety and operational continuity. The convergence of workforce constraints regulatory complexity and technological advancement defines the contemporary European Healthcare IT Consulting landscape where strategic guidance becomes indispensable for sustainable digital health adoption.

MARKET DRIVERS

Escalating Regulatory Compliance Demands Drive Consulting Engagement

European healthcare organisations face intensifying regulatory obligations that necessitate specialised consulting support for compliance implementation, and thereby accelerate the growth of the healthcare IT consulting market. The General Data Protection Regulation imposes stringent requirements on health data processing with enforcement actions demonstrating substantial financial consequences for non compliance. According to enforcement data analysis, while the sheer volume of GDPR fines in the healthcare sector remains steady, the average penalty value has risen steeply, reflecting a shift in regulatory focus toward more severe enforcement for data mishandling. Healthcare IT consultants provide critical expertise in designing data governance frameworks conducting privacy impact assessments and implementing technical safeguards that align with Article 32 security requirements. The European Health Data Space initiative further amplifies compliance complexity by establishing new protocols for cross border health data exchange. Organisations require guidance to reconcile national implementations with EU wide standards while maintaining operational efficiency. Consulting engagements focused on regulatory navigation have expanded as healthcare providers recognise that proactive compliance strategies reduce long term risk exposure and avoid costly remediation efforts. The integration of artificial intelligence in clinical workflows introduces additional regulatory considerations under the EU AI Act which classifies certain healthcare applications as high risk requiring conformity assessments and ongoing monitoring. Consultants with multidisciplinary expertise in healthcare operations data protection law and technology architecture deliver value by translating regulatory text into actionable implementation roadmaps that support both compliance objectives and clinical innovation goals.

Chronic Healthcare Workforce Shortages Accelerate Technology Adoption

Persistent staffing deficits across healthcare systems create a compelling demand for technology solutions, which further contributes to the expansion of the healthcare IT consulting market. These solutions are needed to enhance operational efficiency and extend clinical capacity. The World Health Organization warns of a 'ticking timebomb' for the European health workforce, projecting a regional shortage of approximately 1.8 million healthcare workers by 2030 if current retention and recruitment strategies remain unchanged. This structural imbalance drives healthcare organisations to pursue digital transformation initiatives that automate administrative tasks optimise scheduling workflows and enable remote care delivery models. Healthcare IT consulting services facilitate the selection deployment and optimisation of technologies that address workforce constraints including telehealth platforms robotic process automation and clinical decision support systems. As highlighted in the Health at a Glance: Europe 2024 report, the European Union faces a critical structural deficit of approximately 1.2 million doctors, nurses, and midwives, creating immense pressure to adopt technology-driven care models. Consultants help organisations quantify return on investment for technology interventions that reduce clinician burnout improve patient throughput and enhance care coordination across fragmented service delivery networks. The adoption of artificial intelligence for diagnostic support documentation automation and predictive analytics represents a strategic response to workforce limitations that requires careful change management and workflow redesign. Healthcare IT consultants bridge the gap between technology capabilities and clinical realities ensuring that digital solutions align with frontline user needs while delivering measurable improvements in productivity and care quality.

MARKET RESTRAINTS

Fragmented Digital Infrastructure Impedes Consulting Project Scalability

European healthcare systems operate within highly decentralised administrative frameworks that create significant barriers to standardised technology deployment and consulting engagement scalability within the healthcare IT consulting market. According to the European Court of Auditors' Special Report 25/2024, the EU's healthcare digitalisation efforts are hampered by significant disparities in digital maturity and governance across Member States, complicating the deployment of cross-border consulting and infrastructure projects. This heterogeneity forces consulting firms to develop customised implementation approaches for each jurisdiction increasing project complexity timelines and costs. The absence of unified technical specifications for electronic health records means that consultants must navigate multiple vendor ecosystems proprietary data formats and legacy system dependencies when designing integration architectures. Data from the OECD indicates that a substantial portion of the European health workforce, ranging from 30% to 70% depending on the region, lacks essential digital competencies, creating a significant barrier to the effective adoption of advanced clinical information systems. This skills gap necessitates extensive training components within consulting engagements further straining project budgets and delaying value realisation. The challenge intensifies when consulting projects span multiple countries requiring coordination across different regulatory regimes procurement processes and organisational cultures. Healthcare IT consultants must balance the pursuit of best practice methodologies with the pragmatic realities of local infrastructure constraints often compromising optimal solution design to accommodate existing technical limitations. These structural impediments constrain the ability of consulting firms to deliver standardised service offerings and achieve economies of scale that would otherwise enhance affordability and accessibility for smaller healthcare providers.

Limited Digital Health Literacy Constrains Technology Adoption Success

Widespread deficiencies in digital health literacy among populations and healthcare professionals create a major hurdle for the healthcare IT consulting market. This knowledge gap severely restricts the overall effectiveness of Healthcare IT Consulting engagements. Research from the EU-funded IDEAHL project reveals that approximately 40% of European citizens possess problematic digital health literacy, significantly limiting their ability to effectively utilize digital tools for self-care and disease management. This limitation affects patient engagement with telehealth platforms mobile health applications and patient portals that consulting projects frequently implement. Within healthcare workforces digital competency varies substantially with some clinicians reporting discomfort using advanced clinical information systems or data analytics tools. The OECD Patient-Reported Indicator Surveys (PaRIS) highlight that digital health confidence remains low among primary care patients aged 45 and older with chronic conditions, underscoring the need for user-friendly technology designs in the 'Silver Economy. Healthcare IT consultants must therefore allocate substantial resources to change management user training and ongoing support activities that extend beyond initial technology deployment. The necessity of addressing literacy gaps increases project timelines and costs while potentially diluting the anticipated benefits of digital transformation initiatives. Consultants face the dual challenge of designing intuitive user interfaces that accommodate varying skill levels while simultaneously advocating for long term investments in digital skills development across healthcare organisations. Without parallel investments in workforce training and patient education even well designed technology solutions may fail to achieve intended adoption rates and clinical impact metrics.

MARKET OPPORTUNITIES

Expansion of Artificial Intelligence Applications Creates New Consulting Niches

The accelerating integration of artificial intelligence into regional healthcare delivery generates substantial openings for the expansion of the healthcare IT consulting market. This trend creates a strong demand for specialized Healthcare IT Consulting services focused on AI strategy implementation and governance. According to European Commission health-tech assessments, a rapidly expanding majority of healthcare systems are prioritizing AI investments and planning long-term adoption, positioning digital automation as a key infrastructure driver across the region. Healthcare IT consultants with expertise in machine learning model validation clinical workflow integration and ethical AI frameworks are uniquely positioned to guide organisations through the complexities of responsible AI deployment. The European Union AI Act establishes a risk based regulatory framework that classifies certain healthcare AI applications as high risk requiring conformity assessments ongoing monitoring and human oversight mechanisms. Consultants can deliver value by helping healthcare organisations navigate these requirements while maximising the clinical and operational benefits of AI enabled tools. Historical industry data tracks a steady upward trajectory in European healthcare organizations deploying AI technologies for disease diagnostics, indicating substantial headroom for scalability across additional clinical and administrative domains. Consulting engagements focused on AI opportunity assessment use case prioritisation data preparation and model governance represent high growth service lines that align with strategic healthcare priorities. The convergence of AI capabilities with existing electronic health record infrastructure creates opportunities for consultants to design integrated solutions that enhance clinical decision support population health management and operational efficiency while maintaining regulatory compliance and patient trust.

Cross Border Health Data Exchange Initiatives Unlock Regional Consulting Demand

The development of the European Health Data Space and related cross border health data exchange frameworks offers significant opportunities for firms within the Healthcare IT Consulting market. These are firms with expertise in interoperability standards data governance and multi-jurisdictional compliance. According to the European Commission, the European Health Data Space (EHDS) aims to empower individuals to control their medical data while enabling researchers, innovators, and policymakers to securely access high-quality health data for public interest purposes. This ambitious initiative requires substantial technical and organisational investments to establish secure scalable and privacy preserving data sharing infrastructures across 27 member states. Healthcare IT consultants can support healthcare providers research institutions and technology vendors in preparing for EHDS participation by conducting readiness assessments designing data sharing agreements and implementing technical interfaces that comply with common specifications. As evaluated in the European Court of Auditors' Special Report 25/2024, achieving seamless cross-border health data exchange requires resolving persistent infrastructure challenges related to semantic interoperability, unified patient identification, and regional consent management. Consultants with deep knowledge of HL7 FHIR standards GDPR requirements and national health information system architectures can deliver critical guidance that accelerates EHDS implementation timelines and reduces integration risks. The opportunity extends beyond initial deployment to encompass ongoing governance support performance monitoring and continuous improvement activities that ensure sustainable cross border data sharing capabilities. Healthcare organisations that proactively engage consulting expertise to prepare for EHDS participation position themselves to benefit from enhanced care coordination research collaboration and innovation partnerships across the European region.

MARKET CHALLENGES

Interoperability Fragmentation Complicates System Integration Efforts

Persistent interoperability challenges across healthcare information systems are a fundamental obstacle to the healthcare IT consulting market. Addressing these is essential for Healthcare IT Consulting engagements to deliver successful digital transformation outcomes. According to data from the U.S. Office of the National Coordinator for Health IT, while domestic acute care hospital EHR adoption exceeds 96%, organizations globally continue to struggle with cross-system data exchange due to proprietary vendor formats and fragmented interoperability standards. European healthcare environments exhibit similar patterns with multiple electronic health record vendors regional health information exchanges and national eHealth infrastructures operating with limited technical alignment. Healthcare IT consultants face the complex task of designing integration architectures that accommodate diverse data models communication protocols and security requirements while maintaining clinical workflow integrity. Industry workforce assessments demonstrate that operational interoperability failures frequently stem not from technical capability gaps, but from misaligned institutional incentives and commercial barriers that slow data sharing. Consultants must navigate these political and economic realities while advocating for standards based approaches that prioritise patient centred data access and care coordination. The emergence of Fast Healthcare Interoperability Resources offers promise for improved data exchange but adoption remains inconsistent across European jurisdictions requiring consultants to implement hybrid integration strategies that bridge legacy and modern systems. Success in this domain demands deep technical expertise combined with stakeholder management skills that enable consensus building around shared interoperability goals.

Cybersecurity Threats Escalate Risk Management Complexity for Consulting Projects

Regional healthcare organisations face an intensifying cybersecurity threat landscape, which significantly elevates their risk profile and impedes the expansion of the healthcare IT consulting market. This reality dramatically increases the complexity of Healthcare IT Consulting engagements focused on digital transformation. According to the IBM and Ponemon Institute Cost of a Data Breach Report 2024 healthcare data breaches incur an average cost of 9.77 million dollars per incident exceeding twice the global average across all industries and reflecting the high value of protected health information to malicious actors. European healthcare entities face additional exposure under the General Data Protection Regulation which imposes substantial fines for security failures involving personal data. Healthcare IT consultants must therefore integrate robust security considerations into every phase of technology planning deployment and optimisation activities. As documented in landmark ransomware studies by Emsisoft, cyberattacks targeting hospital networks regularly disrupt over 140 clinical facilities in a single calendar year, severely compromising patient care continuity and institutional data integrity. Consultants support organisations in implementing zero trust architectures multi factor authentication endpoint detection and regular penetration testing that collectively reduce breach likelihood and impact. The challenge intensifies when consulting projects involve cloud migration mobile health applications or internet connected medical devices that expand the attack surface requiring specialised security expertise. Healthcare IT consultants must balance security requirements with usability considerations ensuring that protective measures do not impede clinical workflows or patient access to care. Success demands ongoing collaboration with information security teams continuous threat monitoring and adaptive risk management strategies that evolve alongside emerging cyber threats targeting the healthcare sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13% |

| Segments Covered | By Type, End-user, and Region. |

|

Various Analyses Covered | Global, Regional, and country-level analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Epic Systems Corporation, General Electric, Koninklijke Philips N.V., Cerner Corporation, Cisco, Cognizant, Genpact, Allscripts Healthcare, LLC, Atos SE, HCL Technologies Limited, Hexaware Technologies, Infor, IBM Corporation, Deloitte Touche Tohmatsu Limited, Accenture, Infosys Limited, Larsen & Toubro Limited, Microsoft, Mckesson Corporation, Ntt Data, Inc., Oracle, Sap SE, Tata Consultancy Services Limited and Wipro Limited, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The Healthcare Business Process Management segment maintained the dominance within the Healthcare IT Consulting Market and accounted for a 28.7% share in 2025. This dominance of the segment was driven by healthcare organizations intensifying efforts to streamline clinical and administrative workflows while maintaining regulatory compliance and care quality standards. The implementation of process management frameworks enables healthcare professionals to redirect focus toward patient centered care while realizing operational efficiencies through standardized protocols and automated decision pathways. According to the European Commission's digital transformation initiatives, modernizing regional healthcare infrastructure has accelerated institutional demand for business process optimization services that integrate legacy systems with modern cloud-based platforms. The rising adoption of value based care models further amplifies consulting demand as providers require sophisticated process mapping to align reimbursement structures with clinical outcomes. Major consulting firms have expanded their business process management capabilities through strategic partnerships with technology vendors enabling end to end service delivery that addresses workflow redesign change management and performance analytics. Research published in peer-reviewed healthcare administration literature demonstrates that implementing systematic business process management strategies yields measurable operational cost reductions alongside elevated patient satisfaction scores. The segment's continued dominance is reinforced by increasing regulatory complexity requiring specialized expertise to navigate data governance interoperability standards and cybersecurity frameworks within evolving healthcare delivery ecosystems.

But the Healthcare Enterprise Reporting and Data Analytics segment is likely to experience the fastest CAGR of 19.7% from 2026 to 2034 due to healthcare organizations urgent need to transform raw clinical and operational data into actionable intelligence that supports population health management clinical decision support and financial performance optimization. According to data architecture indices, the healthcare sector exhibits the fastest data volume growth rate of any global industry, creating unprecedented opportunities for analytics-enabled consulting services to extract value from complex datasets. The segment benefits from rising adoption of artificial intelligence and machine learning technologies that enable predictive modeling for disease outbreaks patient risk stratification and resource allocation optimization. According to clinical informatics studies, healthcare providers leveraging advanced predictive analytics report meaningful long-term improvements in clinical outcomes alongside notable reductions in unnecessary hospital readmissions. Consulting engagements focused on analytics strategy data governance framework development and real time dashboard implementation have become essential as healthcare leaders seek to meet value based care mandates while controlling costs. The proliferation of interoperability standards such as Fast Healthcare Interoperability Resources further catalyzes analytics consulting demand by enabling seamless data aggregation across disparate systems. Organizations investing in enterprise reporting capabilities position themselves to capitalize on emerging opportunities in precision medicine clinical research and population health initiatives that require sophisticated data integration and visualization expertise.

By End User Insights

The Hospitals and Ambulatory Care Centers segment led the Healthcare IT Consulting Market and captured a 37.5% share in 2025. This leading position of the segment was attributed to the substantial scale and complexity of hospital operations which necessitate comprehensive IT consulting support for electronic health record implementation revenue cycle management cybersecurity infrastructure and clinical workflow optimization. According to data from the Office of the National Coordinator for Health IT, over 96 percent of non-federal acute care hospitals in the United States have adopted certified electronic health record technology, driving demand for consulting services that support optimization and interoperability. The transition from fee for service to value based reimbursement models intensifies consulting demand as hospitals require sophisticated analytics capabilities to track quality metrics manage population health contracts and optimize care coordination across fragmented delivery networks. As evaluated by global healthcare technology benchmarks, hospitals investing in strategic IT advisory partnerships consistently achieve accelerated technology adoption timelines and significantly higher end-user satisfaction scores. The segment's dominance is further reinforced by increasing regulatory requirements related to data privacy cybersecurity and interoperability that necessitate specialized expertise beyond internal IT department capabilities. Consulting engagements focused on digital transformation strategy change management and performance optimization enable hospitals to navigate technological complexity while maintaining clinical excellence and financial sustainability in an increasingly competitive healthcare landscape.

On the other hand, the Public and Private Payers segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 16.5% during the forecast period owing to payers intensifying focus on leveraging technology to enhance claims processing efficiency fraud detection capabilities and member engagement strategies while adapting to value based payment models. According to the Centers for Medicare and Medicaid Services, Medicare Advantage enrollment has surged past 32 million beneficiaries, representing substantial growth in complex payment arrangements that require sophisticated care management infrastructure. Consulting services supporting payers encompass claims system modernization risk adjustment analytics provider network optimization and member portal development that collectively enable more effective cost management and quality improvement initiatives. The segment's growth is further catalyzed by increasing regulatory mandates related to price transparency interoperability and health equity that require payers to implement sophisticated data governance frameworks and reporting capabilities. Consulting partnerships enable payers to navigate evolving regulatory landscapes while developing member centric digital experiences that improve engagement and health outcomes. The convergence of artificial intelligence predictive analytics and cloud based platforms creates new opportunities for consulting firms to deliver innovative solutions that transform payer operations from transactional processing to proactive health management partnerships.

REGIONAL ANALYSIS

North America Healthcare IT Consulting Market Analysis

North America was the top performer in the Healthcare IT Consulting market and accounted for a 39.7% share in 2025 because of the region's advanced healthcare infrastructure, substantial information technology investments, and complex regulatory environment that collectively drive sustained demand for specialized consulting expertise. According to the Office of the National Coordinator for Health Information Technology over 96 percent of non federal acute care hospitals in the United States have adopted certified electronic health record technology creating ongoing consulting opportunities for system optimization interoperability enhancement and user experience improvement initiatives. The United States healthcare system's transition toward value based care models intensifies consulting demand as providers require sophisticated analytics capabilities to manage population health contracts track quality metrics and optimize care coordination across fragmented delivery networks. According to official projections from the Centers for Medicare & Medicaid Services, national healthcare spending in the United States has scaled past 4.8 trillion dollars, representing an unmatched capital baseline for technology-enabled care transformation and strategic advisory initiatives. The presence of leading global consulting firms technology vendors and healthcare organizations creates a robust ecosystem that accelerates innovation adoption and knowledge transfer across the regional market. Regulatory frameworks including the Health Insurance Portability and Accountability Act and the 21st Century Cures Act establish compliance requirements that necessitate specialized consulting expertise in data governance cybersecurity and interoperability standards. North America's continued market leadership is reinforced by substantial research and development investments in artificial intelligence predictive analytics and digital health platforms that create new consulting opportunities across clinical operational and strategic domains.

Europe Healthcare IT Consulting Market Analysis

Europe was the next prominent player within the Healthcare IT Consulting market due to advanced healthcare systems strong digital infrastructure and coordinated policy initiatives that drive technology adoption across member states. According to the European Commission the European Health Data Space initiative aims to establish secure scalable frameworks for cross border health data exchange creating substantial consulting demand for interoperability standards implementation data governance design and privacy compliance strategies. Research shows that Germany maintains a leading position within the European healthcare IT sector, driven by substantial national healthcare expenditures, progressive digital prescription frameworks, and accelerated adoption of analytics solutions across regional hospital networks. The General Data Protection Regulation establishes stringent requirements for health data processing that necessitate specialized consulting expertise in privacy impact assessments technical safeguard implementation and cross border data transfer mechanisms. As evaluated in the European Court of Auditors' Special Report 25/2024, healthcare digitalization efforts across Member States exhibit substantial variation, creating widespread opportunities for consulting firms to guide infrastructure modernization, workforce training, and regional change management initiatives. The region's universal healthcare coverage models and aging population demographics intensify demand for technology enabled care delivery solutions that require strategic consulting guidance for implementation and optimization. Consulting engagements focused on artificial intelligence governance telehealth platform deployment and population health analytics enable European healthcare organizations to enhance care quality while controlling costs within resource constrained environments. Europe's market position is further strengthened by collaborative research initiatives public private partnerships and innovation hubs that accelerate digital health adoption across the regional ecosystem.

Asia Pacific Healthcare IT Consulting Market Analysis

Asia Pacific is a rapidly expanding regional player within the Healthcare IT Consulting market. This accelerated growth trajectory reflects substantial government investments in healthcare digitalization rising adoption of electronic health records and increasing demand for technology enabled care delivery solutions across diverse healthcare systems. According to global demographic data, the vast population baseline across the Asia-Pacific region provides an unprecedented scale for digital health initiatives, demanding sophisticated, strategic consulting support for regional deployment and localized optimization. India's Ayushman Bharat Digital Mission (ABDM) establishes a unified national health information infrastructure designed to connect over 1.4 billion citizens, generating immense consulting demand for interoperability framework development, system design, and large-scale public implementation. According to digital infrastructure data from the Ministry of Electronics and Information Technology, India hosts more than 930 million internet users, representing a massive connectivity foundation that enables widespread digital health service delivery across both urban and rural settings. China's healthcare sector continues to invest substantially in artificial intelligence medical imaging analytics and telemedicine platforms that require specialized consulting expertise for regulatory compliance clinical validation and operational integration. The region's diverse healthcare financing models varying regulatory frameworks and evolving workforce capabilities create complex implementation challenges that amplify demand for localized consulting expertise with global best practice knowledge. Consulting partnerships enable Asia Pacific healthcare organizations to navigate technological complexity while building sustainable digital health capabilities that improve access quality and affordability across diverse population segments.

Latin America Healthcare IT Consulting Market Analysis

Latin America is a steadily expanding regional player within the Healthcare IT Consulting market owing to increasing healthcare expenditure growing technology adoption and government initiatives supporting digital transformation across public and private healthcare systems. Brazil leads the regional market accounting for the largest share of consulting demand driven by the country's universal healthcare system substantial private insurance sector and increasing focus on electronic health record implementation. Mexico's healthcare sector continues to invest in telehealth platforms population health analytics and cybersecurity infrastructure that require specialized consulting expertise for regulatory compliance and operational optimization. The region's diverse healthcare financing models varying regulatory frameworks and evolving workforce capabilities create implementation complexities that amplify demand for localized consulting expertise with global best practice knowledge. Consulting engagements focused on interoperability standards data governance frameworks and change management enable Latin American healthcare organizations to build sustainable digital capabilities while navigating resource constraints and infrastructure limitations. The region's market growth is further supported by increasing private sector participation public private partnerships and innovation hubs that accelerate digital health adoption across diverse healthcare delivery settings.

Middle East and Africa Healthcare IT Consulting Market Analysis

The Middle East and Africa is expected to showcase a promising CAGR in the Healthcare IT Consulting market from 2026 to 2034 due to substantial healthcare infrastructure investments growing technology adoption and government initiatives supporting digital transformation across public and private healthcare systems. Gulf Cooperation Council countries lead regional market development driven by substantial public sector investments in smart hospital initiatives artificial intelligence enabled diagnostics and telehealth platforms that create significant consulting demand for implementation and optimization support. South Africa demonstrates the fastest growth potential within the regional market driven by increasing private sector participation public private partnerships and innovation hubs that accelerate digital health adoption across diverse healthcare delivery settings. The region's varying regulatory frameworks evolving workforce capabilities and infrastructure limitations create implementation complexities that amplify demand for localized consulting expertise with global best practice knowledge. Consulting engagements focused on cybersecurity frameworks data governance standards and workforce development enable Middle East and Africa healthcare organizations to build sustainable digital capabilities while navigating resource constraints and operational challenges. The region's market growth is further supported by increasing international collaboration technology transfer initiatives and capacity building programs that accelerate digital health adoption across emerging healthcare ecosystems.

COMPETITIVE LANDSCAPE

The Healthcare IT Consulting Market exhibits moderately consolidated competitive dynamics characterized by presence of global technology conglomerates specialized healthcare consulting firms and emerging digital health specialists. Large multinational corporations leverage extensive resources established client relationships and comprehensive service portfolios to maintain market dominance while specialized firms compete through deep industry expertise customized solutions and agile delivery models. Market consolidation activity remains substantial with larger players acquiring niche consultancies to expand service capabilities geographic presence and technological expertise that enhance competitive positioning. Strategic alliances between technology providers and healthcare specialists create integrated service offerings that combine technical capabilities with domain knowledge addressing complex healthcare transformation requirements. Regional market variations influence competitive dynamics with different players holding strong positions in specific geographical areas based on local market knowledge regulatory expertise and client relationships. Innovation and adaptability increasingly determine competitive success as healthcare organizations seek partners who can deliver measurable outcomes while navigating evolving regulatory requirements technological complexities and workforce constraints. Future market success depends on companies ability to demonstrate clear value propositions through quantifiable improvements in care quality operational efficiency and financial performance that justify consulting investments within resource constrained healthcare environments.

KEY MARKET PLAYERS

The key players operating in the healthcare IT consulting market include

- Epic Systems Corporation

- General Electric

- Koninklijke Philips N.V.

- Cerner Corporation

- Cisco

- Cognizant

- Genpact

- Allscripts Healthcare, LLC

- Atos SE

- HCL Technologies Limited

- Hexaware Technologies

- Infor

- IBM Corporation

- Deloitte Touche Tohmatsu Limited

- Accenture

- Infosys Limited

- Larsen & Toubro Limited

- Microsoft

- McKesson Corporation

- NTT Data, Inc.

- Oracle

- SAP SE

- Tata Consultancy Services Limited

- Wipro Limited

TOP PLAYERS IN THE MARKET

- Accenture maintains prominent positioning within the global Healthcare IT Consulting Market through comprehensive service portfolios that encompass digital transformation strategy cloud migration cybersecurity and artificial intelligence enablement. The company leverages deep healthcare domain expertise combined with advanced technology capabilities to deliver end to end consulting solutions that address clinical operational and strategic challenges across diverse healthcare settings. Recent strategic initiatives include partnerships with leading electronic health record vendors development of proprietary healthcare analytics platforms and investments in workforce training programs that enhance service delivery quality. The company's global delivery model enables scalable consulting engagements that combine local market knowledge with international best practices supporting healthcare organizations across North America Europe Asia Pacific and emerging markets. Accenture continues to invest substantially in research and development focused on emerging technologies including generative artificial intelligence predictive analytics and interoperability frameworks that address evolving healthcare priorities. The company's commitment to sustainability health equity and inclusive innovation further differentiates its market positioning among healthcare clients seeking partners who align with broader societal objectives.

- IBM Corporation maintains significant influence within the Healthcare IT Consulting Market through integrated solutions that combine artificial intelligence cloud computing and data analytics capabilities with deep healthcare domain expertise. The company's consulting practice focuses on enabling healthcare organizations to leverage Watson AI platforms hybrid cloud infrastructure and advanced analytics to improve clinical outcomes operational efficiency and patient engagement. Recent strategic initiatives include development of industry specific AI models for clinical decision support population health management and revenue cycle optimization that address pressing healthcare challenges. The company's global consulting network enables delivery of complex transformation programs that combine technology implementation change management and workforce development across diverse healthcare settings. IBM continues to invest substantially in research focused on responsible artificial intelligence healthcare interoperability and cybersecurity frameworks that address evolving regulatory requirements and technological complexities. The company's commitment to open standards collaborative innovation and ethical technology deployment further differentiates its market positioning among healthcare clients seeking sustainable digital transformation partnerships.

- Cognizant maintains strong positioning within the Healthcare IT Consulting Market through specialized service offerings that encompass digital health strategy electronic health record optimization data analytics and cybersecurity enablement. The company leverages healthcare domain expertise combined with technology implementation capabilities to deliver consulting solutions that address clinical workflow optimization regulatory compliance and patient experience enhancement across diverse healthcare settings. Recent strategic initiatives include development of proprietary healthcare analytics platforms artificial intelligence enabled clinical decision support tools and interoperability frameworks that address evolving industry priorities. The company's global delivery model enables scalable consulting engagements that combine local market knowledge with international best practices supporting healthcare organizations across North America Europe and emerging markets. Cognizant continues to invest substantially in workforce development research and development and client success programs that enhance consulting service quality and client satisfaction. The company's commitment to innovation sustainability and inclusive healthcare solutions further differentiates its market positioning among clients seeking partners who align with broader societal objectives and technological advancement priorities.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key participants in the Healthcare IT Consulting Market employ strategic acquisition programs to expand service capabilities geographic reach and industry expertise that strengthen competitive positioning. Leading firms invest substantially in research and development focused on artificial intelligence predictive analytics and interoperability frameworks that address evolving healthcare priorities and technological complexities. Strategic partnerships with technology vendors healthcare organizations and academic institutions enable knowledge transfer innovation acceleration and solution co development that enhance service quality and market relevance. Workforce development initiatives including specialized training certification programs and talent acquisition strategies ensure consulting teams possess current healthcare domain knowledge and technical capabilities. Client success programs focused on measurable outcomes continuous improvement and long term relationship building differentiate market positioning among healthcare organizations seeking sustainable digital transformation partnerships. Geographic expansion strategies targeting high growth regions including Asia Pacific Latin America and Middle East enable market share growth and revenue diversification across global healthcare ecosystems.

MARKET SEGMENTATION

This research report on the global healthcare IT consulting market has been segmented and sub-segmented based on type, end-user, and region.

By Type

- HCIT Strategy and Project/Program Management

- Healthcare Application Analysis, Design, And Development

- HCIT Integration and Migration

- HCIT Change Management

- Healthcare/Medical System & Security Set-Up and Risk Assessment

- Healthcare Enterprise Reporting and Data Analytics Services

- Production Go-Live/Post Go-Live Support

- Healthcare Business Process Management

- Regulatory Compliance

- Others Consulting Services

By End-User

-

Healthcare Providers

-

Hospitals, Physician Groups, and IDNs

- Ambulatory Care Centers

- Home Healthcare Agencies, Nursing Homes, And Assisted Living Facilities

- Diagnostic and Imaging Centers

- Other End Users (Pharmacies and Diagnostic & Pathological Laboratories)

-

- Healthcare Payers

- Private Payers

- Public Payers

- Other End Users

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What drives growth in the global healthcare IT consulting market?

Growth is driven by rising digital transformation, AI adoption, telehealth expansion, strict healthcare data regulations, and need for interoperability solutions globally

2. Which service segment dominates the global healthcare IT consulting market?

Healthcare business process management leads due to demand for workflow automation and cost reduction solutions in the healthcare IT consulting market

3. How significant is cybersecurity consulting in healthcare IT consulting?

Cybersecurity consulting is critical in the global healthcare IT consulting market because of increasing cyber threats and strict healthcare privacy laws

4. What role does telehealth play in the global healthcare IT consulting market?

Telehealth expansion drives demand for IT consulting services focused on virtual care platforms, connectivity, and patient data management

5. Which regions lead the global healthcare IT consulting market?

North America leads with the largest market share, followed by Europe; Asia-Pacific shows fastest growth due to rising healthcare digitization

6. How do AI and data analytics influence the global healthcare IT consulting market?

AI enables predictive analytics, personalized care, and operational efficiency, boosting demand for consulting services in healthcare IT consulting

7. What challenges affect the global healthcare IT consulting market?

Challenges include high implementation costs, data privacy concerns, integration complexity, and shortage of skilled IT healthcare professionals

8. How important is regulatory compliance consulting in healthcare IT?

Compliance with HIPAA, GDPR, and other regulations makes consulting for risk assessment and system audits essential in the healthcare IT consulting market

9. Who are leading companies in the global healthcare IT consulting market?

Key players include IBM, Deloitte, Accenture, Cognizant, Infosys, and Tata Consultancy Services in the global healthcare IT consulting market

10. How do healthcare providers benefit from IT consulting services?

Healthcare IT consulting improves patient care quality, streamlines processes, ensures data security, and supports digital transformation initiatives

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com