Global Greenhouse Equipment Market Size, Share, Trends, And Growth Forecasts Report - Segmented By Equipment (Heating Systems, Cooling Systems, Others), Type (Glass Greenhouse, Plastic Greenhouse), Crop Type (Fruits & Vegetables, Flowers & Ornamental, Nursery Crops, Others) And By Region (North America, Latin America, Asia Pacific, Europe, Middle East and Africa) - Industry Analysis From 2025 to 2033

Global Greenhouse Equipment Market Size

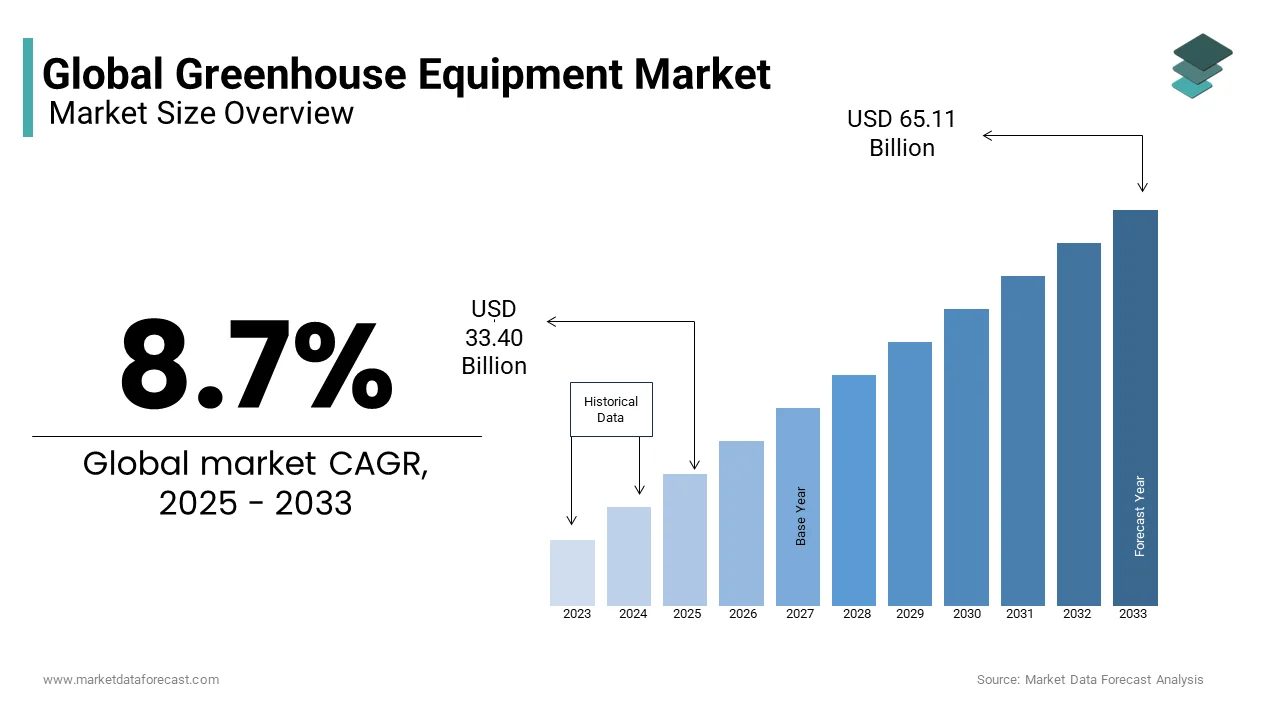

The global greenhouse equipment market was valued at USD 30.73 billion in 2024 and is anticipated to reach USD 33.40 billion in 2025 from USD 65.11 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2025 to 2033.

Greenhouse equipment include heating systems, cooling systems, irrigation equipment, lighting solutions, and climate control devices that collectively enhance crop yield, quality, and sustainability. According to the Food and Agriculture Organization (FAO), the global adoption of greenhouse farming has increased by 15% annually over the past decade owing to the need for efficient resource utilization and year-round crop cultivation.

Europe leads this trend in the global market, with countries like the Netherlands and Spain investing heavily in advanced greenhouse infrastructure to meet rising food demands while minimizing environmental impact. According to the United States Department of Agriculture (USDA), approximately 70% of greenhouse equipment is utilized for cultivating fruits and vegetables, which is indicating its critical role in addressing global food security challenges. Technological advancements, such as automated climate control systems and energy-efficient designs, have significantly reduced operational costs, making greenhouses an attractive option for both small-scale farmers and large agribusinesses. With the global population projected to reach 9.7 billion by 2050, as per the World Bank, the demand for sustainable agricultural solutions is expected to propel the greenhouse equipment market owing to the innovations aimed at enhancing productivity and reducing resource wastage.

MARKET DRIVERS

Increasing Demand for Year-Round Crop Production

The escalating demand for year-round crop production serves as a major driver propelling the greenhouse equipment market. According to the Food and Agriculture Organization (FAO), the global population is projected to grow by 2 billion over the next three decades, which is demanding for innovative agricultural solutions to ensure consistent food supply. Greenhouse equipment plays a crucial role in enabling uninterrupted cultivation, irrespective of seasonal constraints. The USDA reports that regions with extreme climates, such as Scandinavia and parts of North America, have witnessed a 25% increase in greenhouse adoption over the past five years, primarily to mitigate the impact of harsh weather conditions on crop yields. Heating and cooling systems, integral components of greenhouse infrastructure, account for nearly 40% of total equipment sales, as they maintain optimal growing conditions for high-value crops like tomatoes, cucumbers, and strawberries. Furthermore, the ability to produce crops off-season allows farmers to capitalize on premium pricing, driving profitability and fostering market growth.

Technological Advancements in Climate Control Systems

The rapid advancement of climate control technologies has emerged as another significant driver shaping the greenhouse equipment market. According to the International Energy Agency (IEA), automated climate control systems, including humidity regulators, CO2 enrichment devices, and smart sensors, have revolutionized greenhouse farming by optimizing resource efficiency and crop performance. According to the European Environment Agency, these innovations have reduced water consumption by up to 70% and energy usage by 40%, aligning with global sustainability goals. Additionally, the integration of IoT-enabled systems allows real-time monitoring and precise adjustments, enhancing productivity while minimizing human intervention. The USDA estimates that smart greenhouse technologies will account for 30% of the market by 2028, driven by their ability to address labor shortages and improve operational efficiency. This technological evolution not only attracts investment but also positions greenhouse farming as a cornerstone of modern agriculture.

MARKET RESTRAINTS

High Initial Investment Costs

One of the primary restraints impeding the growth of the greenhouse equipment market is the substantial initial investment required for setup and operation. According to the United States Department of Agriculture (USDA), the average cost of constructing a fully equipped greenhouse ranges between $10 and $30 per square foot, depending on the sophistication of the systems installed. This financial barrier disproportionately affects small-scale farmers and developing regions, where access to capital remains limited. The World Bank reports that nearly 60% of potential adopters cite high upfront costs as a deterrent, particularly in Sub-Saharan Africa and Southeast Asia, where agricultural modernization initiatives are still nascent. Additionally, the maintenance of advanced equipment, such as automated climate control systems and irrigation setups, requires specialized skills and regular servicing, further increasing operational expenses. These financial constraints hinder widespread adoption, particularly in rural areas where budget limitations are prevalent.

Energy Dependency and Sustainability Concerns

Another significant restraint facing the greenhouse equipment market is the heavy reliance on energy-intensive systems and the associated environmental concerns. According to the International Energy Agency (IEA), heating and cooling systems account for approximately 60% of a greenhouse's total energy consumption, contributing to elevated carbon emissions and operational costs. The European Environment Agency highlights that traditional fossil fuel-based heating systems remain prevalent in many regions, exacerbating the sector's carbon footprint. Furthermore, fluctuations in energy prices pose additional risks to profitability, particularly in regions lacking access to renewable energy sources. The FAO notes that nearly 40% of greenhouse operators consider energy dependency a major challenge, prompting calls for greater investment in solar-powered and geothermal alternatives. Despite advancements in energy-efficient technologies, the transition to sustainable solutions remains slow, limiting the market's ability to achieve long-term environmental and economic viability.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

The untapped potential of emerging markets presents a lucrative opportunity for the greenhouse equipment market. According to the World Bank, regions such as Sub-Saharan Africa, Southeast Asia, and Latin America are witnessing rapid urbanization and population growth, leading to increased demand for fresh produce and sustainable agricultural practices. In India, for instance, the Ministry of Agriculture has launched initiatives to promote protected cultivation, resulting in a 30% annual increase in greenhouse installations. Similarly, the African Development Bank highlights that agricultural modernization programs in Sub-Saharan Africa have spurred the adoption of greenhouse technologies to combat food insecurity and improve livelihoods. These regions benefit from favorable government policies and subsidies aimed at promoting agricultural productivity and resilience to climate change. Additionally, the rising disposable incomes and awareness of sustainable farming practices among consumers in these markets further bolster demand. The International Monetary Fund projects that emerging economies will account for over 45% of the global greenhouse equipment market by 2030, underscoring their pivotal role in shaping future growth trajectories.

Integration of Renewable Energy Solutions

The integration of renewable energy solutions offers another significant opportunity for the greenhouse equipment market. According to the International Renewable Energy Agency (IRENA), solar-powered and geothermal systems are increasingly being adopted to reduce energy dependency and operational costs in greenhouse farming. The European Commission highlights that the use of photovoltaic panels and thermal collectors has grown by 25% annually, driven by their ability to provide clean and affordable energy for heating, cooling, and lighting systems. Countries like the Netherlands and Germany have pioneered the development of energy-neutral greenhouses, achieving up to 90% reductions in carbon emissions. Furthermore, advancements in battery storage technologies have enhanced the reliability of renewable energy systems, ensuring uninterrupted power supply even during periods of low sunlight or wind. The USDA estimates that renewable energy integration will account for 35% of the market by 2028, driven by the dual benefits of cost savings and environmental sustainability. This shift not only addresses energy dependency but also aligns with global efforts to combat climate change.

MARKET CHALLENGES

Limited Awareness and Technical Expertise Among Farmers

A significant challenge impeding the widespread adoption of greenhouse equipment is the limited awareness and inadequate technical expertise among farmers regarding their proper installation and maintenance. According to the Food and Agriculture Organization (FAO), improper handling of advanced systems can lead to inefficiencies, safety hazards, and even crop losses. For instance, incorrect calibration of climate control systems may result in suboptimal growing conditions, negatively impacting yield and quality. The United Nations Industrial Development Organization (UNIDO) reports that nearly 60% of farmers in developing countries lack access to comprehensive training programs, which hampers the effective deployment of these technologies. This knowledge gap is particularly pronounced in rural areas, where literacy levels and technical expertise are relatively low. Moreover, the absence of standardized guidelines for equipment operation exacerbates the issue, leading to inconsistent outcomes and reduced consumer trust. Addressing this challenge requires collaborative efforts between manufacturers, governments, and educational institutions to develop targeted training initiatives and raise awareness about best practices.

Supply Chain Disruptions and Raw Material Scarcity

Another pressing challenge facing the greenhouse equipment market is the vulnerability of supply chains and the scarcity of raw materials essential for manufacturing key components. According to the International Trade Administration, disruptions caused by geopolitical tensions, natural disasters, and pandemics have led to delays in the procurement of critical materials, such as steel, glass, and polymers. The United States Geological Survey highlights that the availability of key raw materials, including aluminum and copper, has been constrained due to fluctuating prices and export restrictions in major producing countries. These factors have resulted in increased production costs and prolonged lead times, adversely impacting market dynamics. Furthermore, the reliance on imports for certain components exposes manufacturers to currency fluctuations and trade uncertainties. The World Trade Organization notes that over 25% of companies in the greenhouse equipment industry reported supply chain-related challenges in 2022, underscoring the need for diversification and localization strategies to mitigate risks and ensure business continuity.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.7% |

|

Segments Covered |

By Equipment, Greenhouse Type, Crop Type, Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Richel Group SA, Argus Control Systems Ltd, Certhon, Logiqs B.V, Lumigrow, Inc, Agra Tech, Inc, Rough Brothers, Inc, Nexus Corporation, Hort Americas, LLC, Heliospectra AB |

SEGMENT ANALYSIS

Global Greenhouse Equipment Market By Equipment

The heating systems segment dominated the market by holding 40.3% of the global market share in 2024 owing to their critical role in maintaining optimal temperatures for crop growth, particularly in colder climates. According to the USDA, heating systems are indispensable in regions like Scandinavia and Canada, where they enable year-round cultivation of high-value crops such as tomatoes and peppers. Technologies such as hot water boilers, radiant heaters, and heat pumps account for nearly 50% of all heating equipment sales, underscoring their versatility and widespread adoption. The European Environment Agency reports that advancements in energy-efficient heating systems have reduced operational costs by up to 30%, further solidifying their dominance in the market. Additionally, the ability to integrate renewable energy sources, such as solar and geothermal, enhances their appeal among environmentally conscious growers.

The cooling systems segment is anticipated to expand at a prominent CAGR of 8.5% during the forecast period. The ability of cooling systems to regulate temperature and humidity in warmer climates, ensuring optimal growing conditions for sensitive crops is boosting the expansion of the cooling systems segment in the global market. According to the FAO, cooling systems such as evaporative coolers and shade nets are increasingly favored in regions like the Middle East and Sub-Saharan Africa, where rising temperatures pose significant challenges to traditional farming methods. The USDA highlights that the demand for cooling systems has surged by 20% annually, supported by innovations in energy-efficient designs and the growing adoption of vertical farming. Furthermore, the integration of IoT-enabled sensors allows precise control over cooling parameters, enhancing productivity while minimizing resource wastage. Their compatibility with sustainable practices positions them as a key driver of future market growth.

Global Greenhouse Equipment Market By Type

The plastic greenhouses segment accounted for 61.4% of the global market share in 2024. The domination of plastic greenhouses segment is driven by affordability, ease of installation, and versatility across diverse climatic conditions. According to the USDA, plastic greenhouses are particularly popular in developing regions like Asia and Africa, where they are widely used for cultivating fruits, vegetables, and flowers. The lightweight nature of plastic materials, combined with their ability to retain heat and moisture, makes them ideal for small-scale farmers seeking cost-effective solutions. The European Environment Agency reports that the demand for polyethylene-based greenhouses has grown by 15% annually, supported by innovations in UV-resistant and biodegradable films. Additionally, the adaptability of plastic greenhouses to various crop types enhances their importance in addressing global food security challenges.

The glass greenhouses segment is another leading segment and is anticipated to progress at a healthy CAGR of 9.2% over the forecast period. The durability, superior light transmission, and aesthetic appeal of glass greenhouses make them a preferred choice for high-value crops and ornamental plants, which is majorly driving the growth of the glass greenhouses segment in the global market. According to the FAO, glass greenhouses are predominantly used in developed regions like Europe and North America, where precision farming and sustainability are prioritized. The USDA highlights that advancements in energy-efficient glazing technologies have reduced operational costs by up to 25%, further propelling their adoption. Additionally, the integration of automated climate control systems and renewable energy solutions enhances their appeal among commercial growers. The European Environment Agency notes that the demand for glass greenhouses is projected to grow by 20% annually, driven by their ability to deliver consistent yields while minimizing environmental impact.

Global Greenhouse Equipment Market By Crop Type

The fruits and vegetables segment held the largest share of 55.8% of the global market share in 2024. The growth of the fruits and vegetables segment is majorly driven by the increasing global demand for fresh produce, coupled with the need for efficient resource utilization and year-round cultivation. According to the USDA, high-value crops like tomatoes, cucumbers, and peppers account for nearly 70% of all greenhouse-grown produce, underscoring their critical role in addressing food security challenges. The European Environment Agency reports that the adoption of advanced greenhouse technologies has increased yields by up to 40%, while reducing water and fertilizer usage by 30%. Additionally, the ability to cultivate crops in controlled environments minimizes the impact of pests and diseases, enhancing profitability and sustainability. Their versatility and economic significance position fruits and vegetables as the cornerstone of the greenhouse equipment market.

The flowers and ornamental plants segment is predicted to progress at a CAGR of 10.5% over the forecast period owing to the growing demand for exotic and premium floral varieties, particularly in regions like Europe and North America. According to the FAO, greenhouse cultivation enables precise control over growing conditions, ensuring consistent quality and extended shelf life for cut flowers and potted plants. The USDA highlights that innovations in LED lighting and climate control systems have reduced production costs by 25%, further propelling their adoption. Additionally, the rise of e-commerce platforms and floriculture exports has amplified demand, creating new opportunities for growers. The European Environment Agency notes that the demand for greenhouse-grown flowers is projected to grow by 30% annually, driven by their ability to meet consumer preferences for sustainable and high-quality products.

REGIONAL ANALYSIS

Europe dominated the greenhouse equipment market globally by accounting for 33.7% of the global market share in 2024. The advanced agricultural infrastructure of Europe, stringent environmental regulations, and high adoption of precision farming technologies are driving the greenhouse equipment market in Europe. According to the Food and Agriculture Organization (FAO), countries like the Netherlands and Spain account for over 50% of Europe's greenhouse installations, leveraging innovations in energy-efficient designs and automated systems. The European Commission highlights that the demand for greenhouse equipment has grown by 20% annually, supported by government subsidies and investments in sustainable agriculture. Additionally, the region's focus on reducing carbon emissions and water usage aligns with global sustainability goals, further reinforcing its dominance in the market.

Asia-Pacific is a promising regional market for greenhouse equipment worldwide currently and is estimated to register the highest CAGR during the forecast period. The rapid urbanization, population growth, and increasing demand for fresh produce are fuelling the market growth in Asia-Pacific. According to the Asian Development Bank, countries like China and India have witnessed a 30% annual increase in greenhouse installations, driven by government-led initiatives to promote protected cultivation and address food security challenges. The USDA highlights that the adoption of cost-effective plastic greenhouses has surged by 25%, making them accessible to small-scale farmers. Additionally, the region's focus on agricultural modernization and technological innovation positions it as a key driver of future market expansion.

North America is one of the key regional markets for greenhouse equipment globally. Factors such as increasing demand for locally grown, pesticide-free produce and the adoption of advanced greenhouse technologies are propelling the North American market growth. According to the Environmental Protection Agency (EPA), the United States accounts for over 60% of North America's greenhouse installations, with states like California and Arizona leading the way. The USDA reports that innovations in renewable energy integration and automated climate control systems have reduced operational costs by 30%, further propelling adoption. Additionally, the rise of vertical farming and urban agriculture has amplified demand, creating new opportunities for market players.

Latin America accounts for a considerable share of the global greenhouse equipment market. The region's tropical climate and agricultural expertise have facilitated the adoption of greenhouse technologies to enhance crop yields and quality. According to the FAO, countries like Brazil and Mexico have witnessed a 25% annual increase in greenhouse installations, driven by government-led programs to promote sustainable agriculture. The USDA highlights that the demand for greenhouse equipment has surged by 20%, supported by innovations in energy-efficient designs and the growing popularity of organic farming. Additionally, the region's focus on export-oriented agriculture has increased the adoption of advanced greenhouse systems, enhancing their importance in the regional market.

The market in Middle East and Africa is projected to grow steadily over the forecast period. The region's growth is driven by the increasing adoption of greenhouse technologies to combat food insecurity and improve livelihoods. According to the FAO, countries like Egypt and South Africa have witnessed a 30% annual increase in greenhouse installations, driven by government-led initiatives to promote protected cultivation. The USDA highlights that the demand for cooling systems and shade nets has surged by 25%, addressing the challenges posed by rising temperatures and water scarcity. Additionally, the region's focus on agricultural modernization and sustainable practices positions it as a key driver of future market growth.

KEY MARKET PLAYERS

Richel Group SA, Argus Control Systems Ltd, Certhon, Logiqs B.V, Lumigrow, Inc, Agra Tech, Inc, Rough Brothers, Inc, Nexus Corporation, Hort Americas, LLC, Heliospectra AB. Some of the market players dominate the global greenhouse equipment market.

MARKET SEGMENTATION

This research report on the global greenhouse equipment market is segmented and sub-segmented based on Equipment Type, Greenhouse Type, Crop Type, and Region.

By Equipment

- Heating systems

- Cooling systems

- Others

By Greenhouse Type

- Glass greenhouse

- Horticulture glass

- Other greenhouse glass

- Plastic greenhouse

- Polyethylene

- Polycarbonate

- Polymethyl methacrylate (PMMA)

By Crop Type

- Fruits & vegetables

- Flowers & ornamentals

- Nursery crops

- Other crop types

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle-East & Africa

Frequently Asked Questions

What is the current market size of the global greenhouse equipment market?

The current market size of the global greenhouse equipment market 33.40 billion in 2025

What market drivers are driving the global greenhouse equipment market?

The adoption of greenhouses, owing to rapid innovation in technology and rising disposable incomes of people willing to invest in farming and greenhouse adoption technologies, and encouragement from governments also act as drivers of market growth.

Who are the market players that are dominating the greenhouse equipment market?

Richel Group SA, Argus Control Systems Ltd, Certhon, Logiqs B.V, Lumigrow, Inc, Agra Tech, Inc, Rough Brothers, Inc, Nexus Corporation, Hort Americas, LLC, Heliospectra AB. Some of the market players dominate the global greenhouse equipment market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]