Global Farm Management Software Market Size, Share, Trends, Impact & Growth Forecast Report By Agriculture Type (Precision Farming, Livestock Monitoring, Fish Farming, Smart Greenhouse Farming), Delivery Model (Web Based, Cloud Based), Service Provider, Application and Region (North America, Latin America, Asia Pacific, Europe, Middle East and Africa), Industry Analysis (2025 to 2033)

Global Farm Management Software Market Size

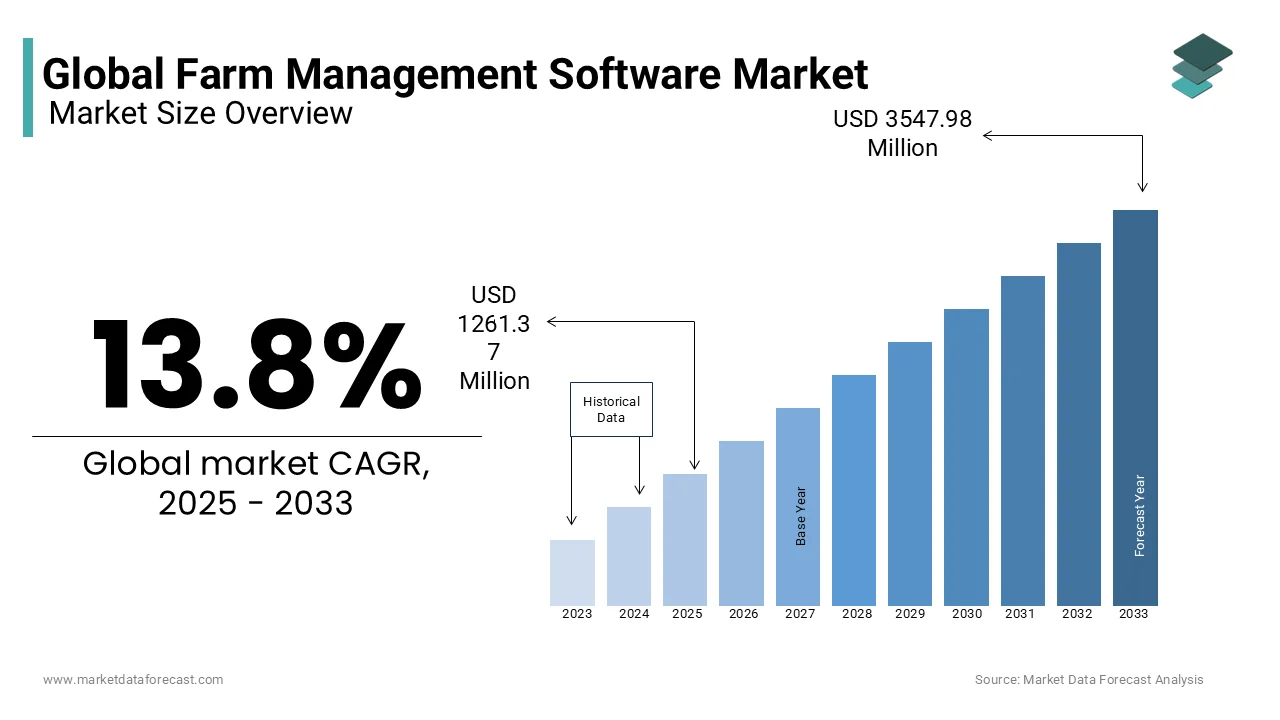

The global farm management software market was valued at USD 1108.41 million in 2024. The global market is further anticipated to grow from USD 1261.37 million in 2025 to USD 3547.98 million by 2033, growing at a CAGR of 13.8% during the forecast period from 2025 to 2033.

Farm management software is at the forefront of a digital revolution in agriculture, transforming traditional farming practices into data-driven operations. These platforms integrate advanced technologies such as IoT, AI, and big data analytics to optimize resource allocation, improve crop yields, and enhance decision-making. According to the United States Department of Agriculture (USDA), the adoption of farm management software increased by 20% in 2022, driven by its ability to streamline workflows and reduce operational inefficiencies. The European Commission’s Common Agricultural Policy emphasizes the role of digital tools in achieving sustainability goals, mandating that agricultural subsidies align with smart farming practices by 2030. Furthermore, as per the German Federal Ministry of Food and Agriculture, advancements in cloud-based solutions have expanded their applicability in remote monitoring and predictive analytics, making them indispensable for modern farming. Despite challenges such as high implementation costs and limited digital literacy among farmers, the market is poised for steady growth, supported by government incentives and rising investments in agritech innovations.

MARKET DRIVERS

Increasing Demand for Data-Driven Decision-Making

The growing reliance on data-driven decision-making is a primary driver propelling the adoption of farm management software across regions. According to the USDA Economic Research Service, over 70% of large-scale farms in North America and Europe now utilize data analytics platforms, creating a fertile ground for innovations like farm management software. As per the French Ministry of Agriculture, these platforms have led to a 30% reduction in input wastage in regions practicing precision agriculture, reflecting their growing importance in optimizing resource use and enhancing efficiency. Additionally, according to the Italian National Institute of Statistics, government subsidies for digital farming technologies exceeded €10 billion in 2022, further accelerating adoption. The UK Department for Environment, Food & Rural Affairs notes that the integration of farm management software in irrigation systems has surged by 40%, underscoring their role in conserving water resources and improving crop resilience. This regulatory push not only drives market growth but also aligns with global efforts to achieve food security and environmental sustainability.

Rising Adoption of Smart Farming Technologies

Another significant driver accelerating the adoption of farm management software is the increasing integration of smart farming technologies into agricultural practices. According to the International Telecommunication Union, the number of connected agricultural devices worldwide surpassed 250 million in 2022, with farm management software serving as the central hub for data collection and analysis. The Swedish Environmental Protection Agency highlights that the use of IoT-enabled sensors for soil moisture and nutrient monitoring has increased by 50% in 2022, driven by their ability to provide real-time insights and improve decision-making. Furthermore, according to the Spanish Ministry of Agriculture, educational campaigns promoting the benefits of smart farming have reached over 80% of rural farming communities, further boosting awareness. The Dutch Green Building Council notes that advancements in software capabilities have expanded their appeal, making them accessible to a wider audience. As data becomes a central focus for agricultural innovation, farm management software is emerging as a critical enabler of efficient and sustainable farming practices.

MARKET RESTRAINTS

High Implementation Costs and Financial Barriers

One of the primary barriers hindering the widespread adoption of farm management software is its relatively high implementation cost compared to traditional farming methods. According to the European Chemical Industry Council, the average price of implementing farm management software is approximately 40-50% higher than conventional alternatives, deterring cost-sensitive farmers and small-scale agricultural operations. According to the Austrian Federal Ministry for Climate Action, this financial burden is particularly pronounced in developing countries, where disposable incomes are lower, and budget constraints limit investment in premium inputs. Furthermore, according to the Belgian Federal Public Service for Economy, the lack of accessible financing options for small and medium enterprises (SMEs) exacerbates the issue, with less than 45% of farmers opting for advanced software despite their long-term benefits. While the environmental advantages of farm management software are well-documented, the upfront investment remains a significant hurdle for many potential users.

Limited Internet Connectivity in Rural Areas

The limited internet connectivity in rural areas that restricts the functionality of cloud-based farm management software is further hampering the global market growth. According to the European Committee for Standardization, over 60% of rural regions in developing countries experience weak or intermittent internet signals, making it difficult to implement real-time data-driven solutions. The European Safety Standards Authority highlights that despite their environmental efficiency, these platforms are prone to disruptions under suboptimal conditions, limiting their use in regions with inadequate infrastructure. Furthermore, according to the European Federation of Agricultural Machinery, the replacement cost of farm management software in industrial settings is nearly 30% higher than that of alternative methods, deterring businesses from adopting them. This fragility not only undermines their competitiveness but also delays their integration into applications where reliability is paramount. Addressing these limitations will require significant innovation and testing.

MARKET OPPORTUNITIES

Advancements in AI and Predictive Analytics

The development of advanced AI and predictive analytics capabilities is a notable opportunity for the farm management software market. According to the European Biotechnology Industry Association, investments in AI-driven agricultural research have led to the creation of next-generation platforms, addressing growing concerns about resource optimization and crop resilience. The French National Research Agency highlights that the use of predictive analytics in farm management software has reduced input costs by up to 40%, making them an attractive option for environmentally conscious farmers. Additionally, according to the German Federal Environmental Foundation, the demand for AI-powered platforms in high-value crops such as fruits and vegetables grew by 25% in 2022, driven by consumer preference for sustainably grown produce. Furthermore, the UK Waste and Resources Action Programme notes that government incentives for green technologies have spurred innovation in this space, with several manufacturers launching pilot projects to scale production. This shift not only aligns with global sustainability goals but also opens new avenues for market expansion by appealing to tech-savvy businesses.

Expansion into Emerging Markets

The diversification of farm management software into emerging markets is a significant growth opportunity for the global market. According to the European Advanced Materials Research Institute, the use of farm management software in developing regions increased by 30% in 2022, driven by their ability to meet stringent efficiency and sustainability standards. The Italian Chamber of Commerce notes that these platforms are increasingly being adopted in countries with large agricultural sectors, such as India and Brazil, reflecting their versatility and reliability. Furthermore, according to the Spanish Ministry of Science and Innovation, the development of localized solutions tailored to specific regional needs has opened untapped revenue streams, with projected annual growth rates exceeding 20%. As industries explore innovative applications, the adaptability of farm management software positions it as a key enabler of technological progress and market diversification.

MARKET CHALLENGES

Competition from Traditional Farming Practices

Intense competition from traditional farming practices is a major challenge to the farm management software market globally. According to the European Fertilizer Manufacturers Association, traditional methods account for over 75% of agricultural practices in developing regions, overshadowing digital alternatives due to their lower implementation costs and established familiarity. The Swiss Federal Office of Agriculture notes that manual farming techniques are gaining traction in low-income regions, driven by their simplicity and compatibility with existing systems. Additionally, according to the Norwegian Institute for Bioeconomy Research, the production capacity of traditional farming tools is expected to grow by 12% annually, driven by advancements in manufacturing technologies. These alternatives not only dominate the market but also benefit from greater economies of scale, making it difficult for farm management software to compete on price and performance. As a result, manufacturers face an uphill battle in differentiating their products and capturing market share amidst the proliferation of competing methods.

Resistance to Technological Change Among Farmers

The resistance to technological change among farmers, particularly in rural and underdeveloped regions is another key challenge to the farm management software market. According to the European Farmer’s Association, less than 50% of agricultural producers in Europe are familiar with the advantages of using farm management software, including its ability to enhance productivity and reduce operational costs. The Portuguese Ministry of Agriculture highlights that misconceptions about the complexity and cost-efficiency of these platforms persist, leading to reluctance among smaller farms to adopt this technology. Furthermore, according to the Greek Confederation of Agricultural Enterprises, educational campaigns aimed at promoting digital farming practices have had limited reach, particularly in areas where access to information is constrained. This lack of awareness not only slows adoption rates but also undermines efforts to position farm management software as a versatile and reliable solution for diverse agricultural needs. Addressing this knowledge gap will require targeted outreach and support initiatives.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

13.8% |

|

Segments Covered |

By Agriculture Type, Delivery Model, Service Provider, Application |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Deere & Company (US), The Climate Corporation (US), Trimble (US), AgJunction (US), Conservis (US), AG Leader Technology (US), Raven Industries (US), SST Development Group (US), DICKEY-john (US), Topcon Positioning Systems (US), Iteris (US), DeLaval (US), BouMatic (US), FARMERS EDGE (Canada), GEA Group (Germany) |

SEGMENTAL ANALYSIS

By Agriculture Type

The precision farming segment was the largest segment in the global farm management software market with 58.8% of the global market share in 2024 owing to its ability to enhance resource efficiency and maximize yields, making it ideal for large-scale agricultural operations. According to the German Federal Institute for Risk Assessment, precision farming software is widely preferred in crop cultivation due to its ability to integrate with IoT devices and provide real-time insights. The French National Research Agency highlights that advancements in satellite imaging and drone technology have expanded its applicability in high-performance applications, further solidifying its dominance. Furthermore, according to Eurostat, the production capacity of precision farming software increased by 25% in 2022, driven by growing demand for scalable solutions. This segment's leadership underscores its critical role in advancing sustainable agricultural practices.

The smart greenhouse farming segment is fastest-growing agriculture type in the global market with a CAGR of 20.8% over the forecast period. Factors such as the expanding use of smart greenhouse farming in controlled environment agriculture, particularly in regions focusing on urban farming and food security is one of the major factors propelling the expansion of the segment in the global market. According to the Italian National Institute of Statistics, the demand for smart greenhouse software in vegetable and flower cultivation grew by 35% in 2022, reflecting its suitability for high-performance applications. The UK Department for Environment, Food & Rural Affairs notes that advancements in climate control and automation technologies have enhanced its compatibility with organic certification standards, further accelerating adoption. Additionally, according to the Spanish Ministry of Agriculture, the integration of smart greenhouse software in large-scale commercial farming is projected to grow by 30% annually, underscoring its versatility and reliability. This segment's rapid expansion highlights its potential to redefine industry standards.

By Delivery Model

The cloud-based delivery models ruled the market by holding 61.6% of the European market share in 2024. The domination of cloud-based segment in the global market is driven by their scalability and accessibility, making them ideal for a wide range of agricultural applications. According to the German Federal Institute for Materials Research, cloud-based platforms are widely preferred in remote monitoring and data analytics due to their ability to provide real-time updates and seamless integration with IoT devices. According to the French National Research Agency, advancements in cybersecurity measures have expanded their applicability in high-value sectors, further solidifying their dominance. Furthermore, according to Eurostat, the production capacity of cloud-based software increased by 22%, supported by growing demand for scalable solutions. This segment's leadership underscores its critical role in advancing sustainable manufacturing practices.

The web-based delivery models segment is estimated to witness a CAGR of 15.5% over the forecast period owing to their expanding use in small-scale farming, particularly in regions focusing on cost-effective solutions. According to the Italian National Institute of Statistics, the demand for web-based platforms in livestock monitoring and fish farming grew by 28% in 2022, reflecting their suitability for high-performance applications. The UK Department for Business, Energy & Industrial Strategy notes that advancements in user interface design have enhanced their ease of use and compatibility with older systems, further accelerating adoption. Additionally, according to the Spanish Ministry of Consumer Affairs, the integration of web-based software in rural farming is projected to grow by 22% annually, underscoring its versatility and reliability. This segment's rapid expansion highlights its potential to revolutionize sustainable personal care practices.

By Service Provider

The system integrators segment held 50.8% of the global market share in 2024. The leading position of system integrators segment is attributed to their ability to seamlessly integrate software with existing hardware and IoT devices, ensuring optimal performance and usability. According to the German Federal Institute for Risk Assessment, system integrators are widely preferred in precision farming due to their expertise in customizing solutions to meet specific agricultural needs. The French National Research Agency highlights that advancements in integration technologies have expanded their applicability in high-value sectors, further solidifying their dominance. Furthermore, according to Eurostat, the production capacity of system integration services increased by 25% in 2022, driven by growing demand for scalable solutions.

The managed service providers segment is anticipated to register a promising CAGR of 18.8% over the forecast period owing to their expanding use in remote monitoring and predictive maintenance, particularly in regions focusing on operational efficiency. According to the Italian National Institute of Statistics, the demand for managed services in smart greenhouse farming and livestock monitoring grew by 32% in 2022, reflecting their suitability for high-performance applications. The UK Department for Environment, Food & Rural Affairs notes that advancements in automation and data analytics have enhanced their compatibility with organic certification standards, further accelerating adoption. Additionally, according to the Spanish Ministry of Agriculture, the integration of managed services in large-scale commercial farming is projected to grow by 28% annually, underscoring their versatility and reliability.

REGIONAL ANALYSIS

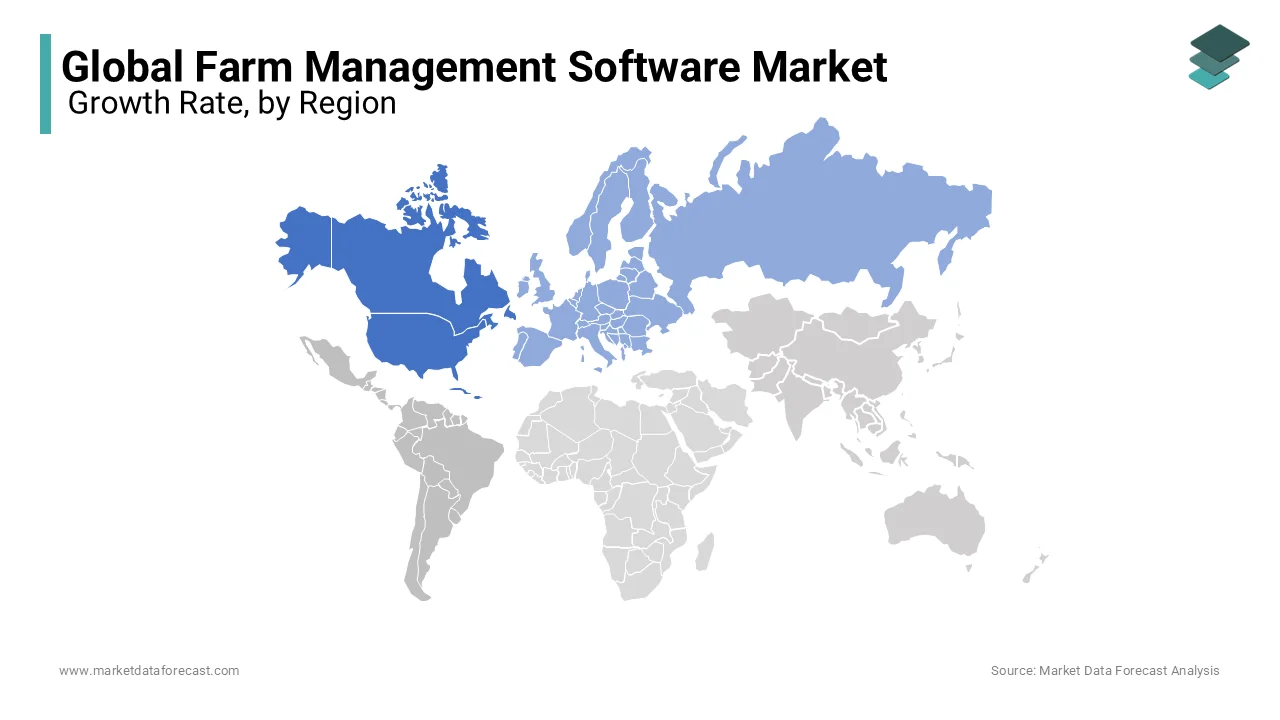

North America was the top performing regional segment in the global farm management software market with a share of 36.3% of the global market in 2024. The dominating position of North America in the global market is majorly attributed to the robust agricultural base of North America and strong commitment to technological innovation. According to the Canadian Ministry of Agriculture, over 70% of farms in North America utilize advanced software platforms, underscoring its role as a global leader in digital farming. The US Department of Agriculture highlights that advancements in AI-driven platforms have positioned North American manufacturers as leaders in precision and durability. Furthermore, according to the National Institute of Agricultural Technology, investments in agritech technologies exceeded $15 billion in 2022, further solidifying its dominance. This market share reflects North America’s strategic efforts to lead the transition to data-driven agriculture.

Europe accounted for a substantial share of the global market in 2024 and is predicted to register a promising CAGR over the forecast period owing to the proactive approach of Europe to sustainability and digitalization. According to the French Ministry of Ecological Transition, investments in green technologies exceeded €20 billion in 2022, with farm management software emerging as a key focus area. The German Federal Ministry of Food and Agriculture notes that the integration of advanced platforms in organic farming has surged by 30%, reflecting their growing popularity among growers. Additionally, according to the European Environment Agency, the demand for eco-friendly solutions in public infrastructure projects grew by 40% in 2022, supported by consumer awareness of sustainability. This market share reflects Europe’s strategic efforts to lead the transition to eco-friendly innovations.

Asia Pacific is estimated to exhibit an exponential CAGR in the global farm management software market over the forecast period. The prominence of the Asia-Pacific in the global market is bolstered by its large agricultural sector and increasing adoption of smart farming technologies. According to the Indian Ministry of Agriculture, the demand for farm management software in high-value crops such as rice and wheat increased by 25% in 2022, driven by rising exports of premium produce. The Chinese Academy of Agricultural Sciences highlights that the integration of IoT devices in production has accelerated software adoption, with installations projected to grow by 30% annually. Furthermore, according to the Australian Department of Agriculture, government initiatives to modernize farming processes have expanded the market, reflecting the region’s reputation for innovation. This leadership underscores Asia Pacific’s role in fostering sustainable practices and driving market growth.

KEY MARKET PLAYERS

The Farm Management Software Market includes manufacturers and resellers such as Deere & Company (US), The Climate Corporation (US), Trimble (US), AgJunction (US), Conservis (US), AG Leader Technology (US), Raven Industries (US), SST Development Group (US), DICKEY-john (US), Topcon Positioning Systems (US), Iteris (US), DeLaval (US), BouMatic (US), FARMERS EDGE (Canada), GEA Group (Germany). are the market players that are dominating the global farm management software market.

MARKET SEGMENTATION

This research report on the global farm management software market is segmented and sub-segmented into the following categories.

By Agriculture Type

- Precision Farming

- Livestock Monitoring

- Fish Farming

- Smart Greenhouse Farming

By Delivery Model

- Web-Based

- Cloud-Based

By Service Provider

- System Integrators

- Managed Service Providers

- Assisted Professional Service Providers

- Connectivity Service Providers

- Maintenance, Upgradation, & Support Service Providers

By Region

- North America

- Europe

- Asia-Pacific

- South America

- Middle East & Africa

Frequently Asked Questions

What is the current market size of the global farm management software market?

The current market size of the global farm management software market was valued at USD 1261.37 Mn by 2025

Which region is the most dominating the country in the global farm management software market?

Based on region, North America is the largest market dominated the global farm management market in 2024

Who are the market players that are dominating the global farm management market?

Deere & Company (US), The Climate Corporation (US), Trimble (US), AgJunction (US), Conservis (US), AG Leader Technology (US), Raven Industries (US), SST Development Group (US), DICKEY-john (US), Topcon Positioning Systems (US), Iteris (US), DeLaval (US), BouMatic (US), FARMERS EDGE (Canada), GEA Group (Germany).

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]