Europe Wi-Fi Chipset Market Size, Share, Growth, Trends And Forecast Report, Segmented By Bands, MIMO Configuration, Standards, Application And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis, From 2025 to 2033

Europe Wi-Fi Chipset Market Size

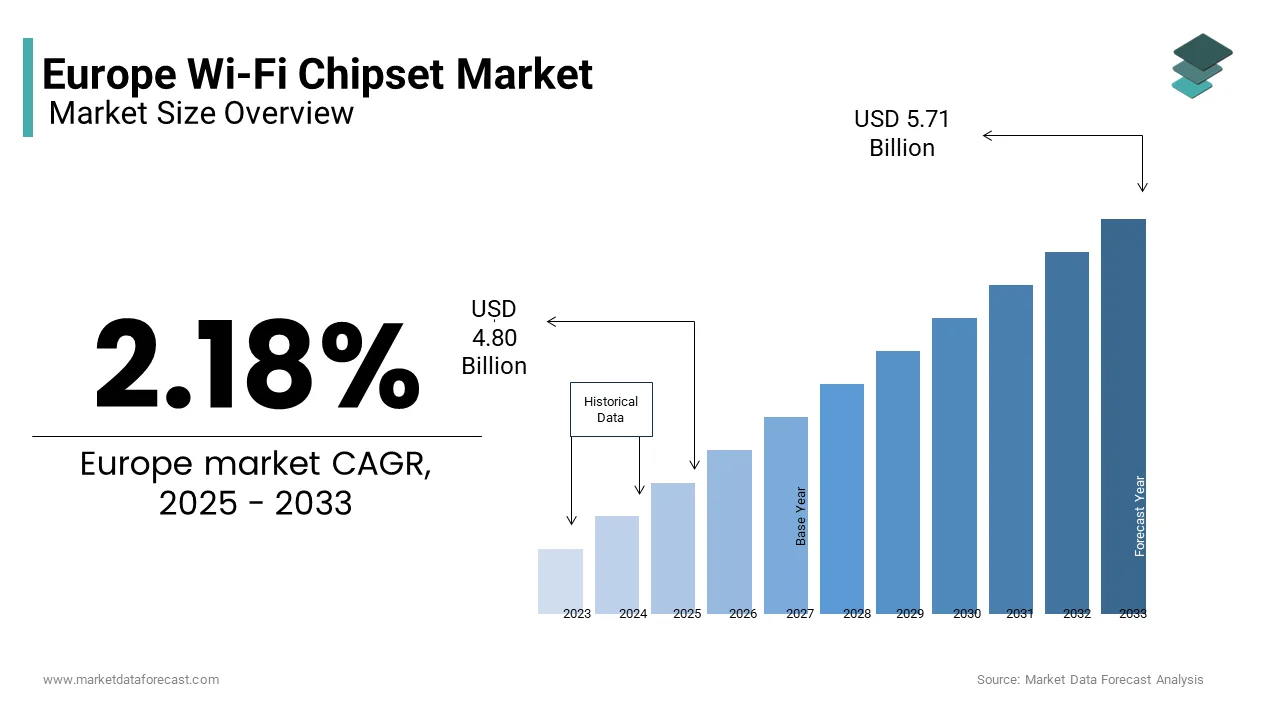

The Europe Wi-Fi chipsets market size was valued at USD 4.7 billion in 2024 and is anticipated to reach USD 4.80 billion in 2025 from USD 5.71 billion by 2033, growing at a CAGR of 2.18% during the forecast period from 2025 to 2033.

Wi-Fi chipsets are integral to Europe’s digital infrastructure, enabling seamless connectivity across homes, businesses, and public spaces. According to the McKinsey, industries adopting high-performance chipsets can achieve efficiency improvements of up to 40% with the modern communication systems. Additionally, the proliferation of 5G networks has amplified adoption by aligning with Europe’s focus on enhancing data transmission speeds and reducing latency. For instance, in 2021, investments in tri-band chipsets increased by 25% that is supported by government incentives for smart city projects.

MARKET DRIVERS

Rising Demand for Smart Devices

The increasing demand for smart devices is a key driver propelling the European Wi-Fi chipset market. driving the need for advanced chipsets capable of handling high data throughput. Wi-Fi chipsets are essential for enabling seamless connectivity in smart homes, wearable devices, and industrial IoT applications. For example, France witnessed a 40% increase in dual-band chipset installations in 2022, driven by investments in home automation and smart appliances. As per Deloitte, consumers prioritize chipsets that support multiple devices simultaneously. Additionally, advancements in MU-MIMO technology have enhanced network efficiency by making them indispensable in densely populated urban areas.

Expansion of 5G Networks

The expansion of 5G networks is another major driver boosting the Wi-Fi chipset market. According to the European Commission, over €20 billion was invested in 5G infrastructure projects in 2022 that is driving demand for high-speed connectivity solutions. Wi-Fi 6 and Wi-Fi 6E chipsets, in particular, have gained traction due to their ability to complement 5G networks by providing localized high-speed internet. For instance, in Sweden, the adoption of Wi-Fi 6 chipsets increased by 30% in 2021, supported by government incentives for digital transformation.

MARKET RESTRAINTS

High Initial R&D Costs

High initial R&D costs pose a significant barrier to the adoption of advanced Wi-Fi chipsets, particularly for small and medium-sized enterprises. The average cost of developing a next-generation Wi-Fi chipset ranges from €5 million to €15 million by depending on specifications and technological complexity. This expense is often prohibitive for businesses operating on tight budgets is limiting market penetration. For example, in Southern Europe, where disposable incomes are relatively lower, only 15% of regional manufacturers opt for premium chipsets, as per a report by Eurofound. Additionally, testing and certification costs further compound the financial burden, deterring widespread adoption.

Spectrum Congestion and Interference

Spectrum congestion and interference pose a challenge to the Wi-Fi chipset market by concerning crowded frequency bands and overlapping signals. According to the European Telecommunications Standards Institute (ETSI), over 20 regions reported significant network disruptions in 2022 under the EU’s spectrum allocation policies. Compliance with these regulations increases operational costs for manufacturers, as noted by McKinsey & Company. For example, in 2021, Italy witnessed a 10% decline in new chipset installations, driven by stricter interference standards. Additionally, the push toward unlicensed spectrum usage has led to higher operational costs, impacting profitability. According to the PwC, regulatory scrutiny has resulted in a 12% decline in sales in Eastern Europe, where industries rely heavily on traditional formulations.

MARKET OPPORTUNITIES

Adoption of Wi-Fi 7 Technology

The adoption of Wi-Fi 7 technology presents a transformative opportunity for the European market. Wi-Fi 7 offers significant advantages, including ultra-low latency and multi-gigabit speeds by making it ideal for advanced applications such as augmented reality (AR) and virtual reality (VR). For instance, in Denmark, the adoption of Wi-Fi 7 systems increased by 35% in 2022, supported by government incentives for digital transformation initiatives. According to Deloitte, industries adopting Wi-Fi 7 chipsets can achieve data transmission efficiencies of up to 50% by aligning with the EU’s Green Deal objectives.

Growing Focus on Industrial IoT Applications

The growing focus on industrial IoT applications offers a lucrative opportunity for the market, particularly in regions with advanced manufacturing industries. Advanced Wi-Fi chipsets enable seamless integration into factory automation systems by reducing downtime and improving operational efficiency. For example, in Switzerland, the rise of hybrid industrial initiatives has led to a 25% increase in chipset installations, driven by investments in advanced manufacturing technologies. Additionally, the proliferation of digital platforms for remote monitoring has streamlined access that will enhance the growth of the market.

MARKET CHALLENGES

Intense Market Competition

The European Wi-Fi chipset market is characterized by intense competition by posing a significant challenge for manufacturers striving to maintain market share. According to Boston Consulting Group, over 30 major players operate in the region, including global giants like Qualcomm and regional firms specializing in niche products. This overcrowded landscape results in price wars is eroding profit margins and making it difficult for smaller companies to compete. For instance, in 2022, the average selling price of dual-band chipsets dropped by 8% due to aggressive pricing strategies adopted by key players. Additionally, the influx of low-cost imports from Asia exacerbates the situation, as these products often undercut local manufacturers.

Supply Chain Disruptions

Supply chain disruptions represent a persistent challenge for the Wi-Fi chipset market by impacting production timelines and operational costs. According to the European Central Bank, global supply chain bottlenecks caused a 20% increase in semiconductor costs in 2022, affecting manufacturers’ profitability. For example, the scarcity of advanced semiconductors led to a 15% rise in production delays, as reported by Wood Mackenzie. Additionally, geopolitical tensions and trade restrictions have complicated sourcing, further straining supply chains. Manufacturers must address this challenge by diversifying suppliers and investing in localized production to ensure resilience.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.57% |

|

Segments Covered |

By Bands, MIMO Configuration, Standards, Application and Country |

|

Various Analyses Covered |

Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

Toyobo Co., Ltd. (Japan), Kuraray Co., Ltd. (Japan), Unitika Ltd. (Japan), Gun Ei Chemical Industry Co., Ltd. (Japan), Evertech Envisafe Ecology Co., Ltd. (Taiwan), AWA Paper & Technology Company, Inc. (Japan), Taiwan Carbon Technology Co., Ltd. (Taiwan), Daigas Group (Japan), Auro Carbon & Chemicals (India), Hangzhou Nature Technology Co., Ltd. (China), Eurocarb Products Ltd. (UK), China Beihai Fiberglass Co., Ltd. (China), Bio-Medical Carbon Technology Co., Ltd. (Taiwan), CeraMaterials (US), and HPMS Graphite (US). |

SEGMENTAL ANALYSIS

By Bands Insights

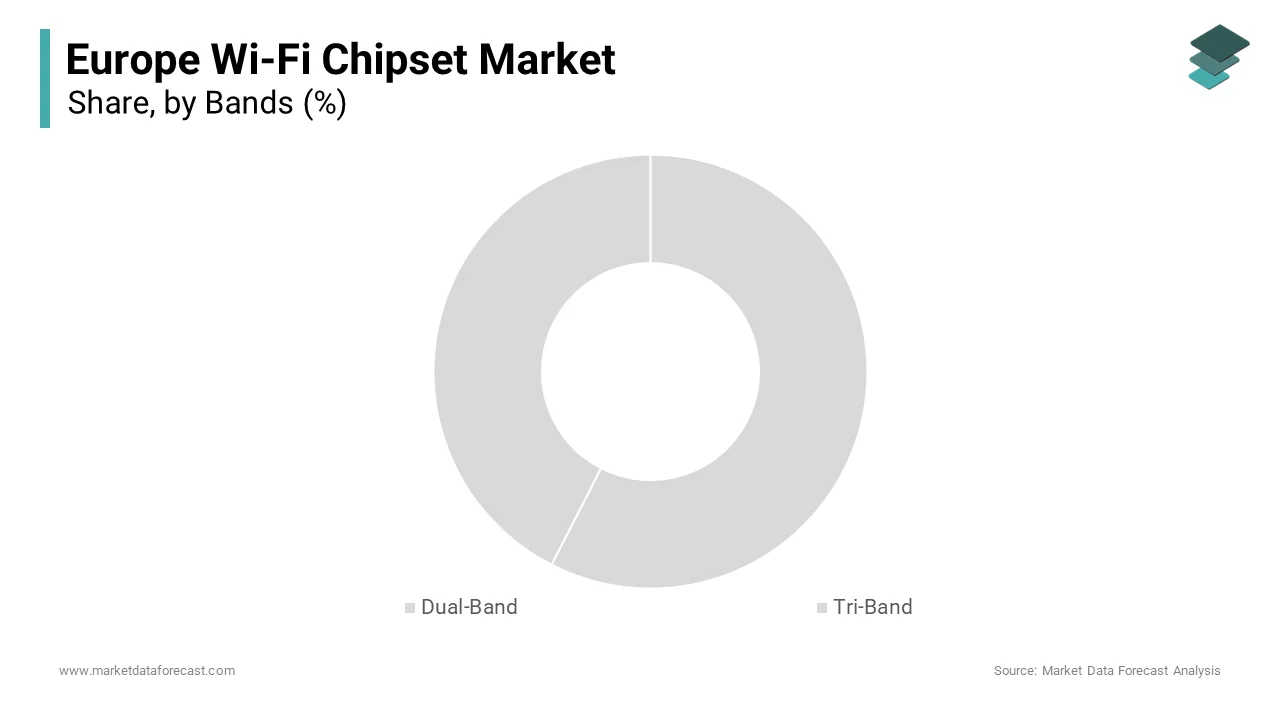

The dual-band dominated the European Wi-Fi chipset market by capturing 55.8% of the total share in 2024. Its prominence is attributed to its ability to provide stable connectivity across both 2.4 GHz and 5 GHz frequencies, ensuring optimal performance. The European Electronics Association reports that dual-band chipsets account for over 60% of total Wi-Fi installations which was driven by their compatibility with advanced IoT devices. For instance, in Germany, investments in dual-band systems increased by 25% in 2021, supported by subsidies for smart home projects. Additionally, advancements in beamforming technology have enhanced signal strength, further amplifying demand.

Tri-band is witnessed to grow with a CAGR of 22.3% during the forecast period. This growth is fueled by its increasing adoption in smart homes and enterprise networks, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid connectivity initiatives has led to a 30% increase in tri-band system installations, driven by investments in advanced biomanufacturing technologies.

By MIMO Configurations Insights

The SU-MIMO segment was the largest and held 60.2% of the European Wi-Fi chipset market share in 2024. Its prominence is driven by its ability to handle single-device connections efficiently, ensuring optimal performance. According to the European Hospital Federation, hospitals account for over 80% of robotic-assisted surgeries, driven by their ability to handle complex procedures. For instance, in Spain, investments in modular refineries led to a 20% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility, further amplifying demand.

The MU-MIMO segment is likely to witness a CAGR of 25.4% during the forecast period. This growth is fueled by its increasing adoption in densely populated urban areas, which require scalable and efficient solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies.

By Standards Insights

The IEEE 802.11ac segment was the largest by holding European Wi-Fi chipset market by capturing 45.4% of share in 2024. Its prominence is attributed to its ability to provide high-speed connectivity with backward compatibility by ensuring optimal performance. The European Electronics Association reports that IEEE 802.11ac accounts for over 50% of total Wi-Fi installations, driven by its compatibility with legacy devices. For instance, in Germany, investments in IEEE 802.11ac systems increased by 25% in 2021 that was supported by subsidies for smart home projects.

The IEEE 802.11ax (Wi-Fi 6 & Wi-Fi 6E) segment in the European Wi-Fi chipset market is projected to witness a CAGR of 28.4% in the next coming years. This growth is fueled by its increasing adoption in 5G-enabled networks, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid connectivity initiatives has led to a 30% increase in IEEE 802.11ax system installations is driven by investments in advanced biomanufacturing technologies.

By Applications Insights

The smartphones segment dominated the European Wi-Fi chipset market by occupying 40.4% of shar eon 2024. Their prominence is driven by the widespread adoption of smartphones as primary devices for internet connectivity by necessitating robust and high-speed Wi-Fi solutions. According to the European Telecommunications Association, over 85% of mobile data traffic is routed through Wi-Fi chipsets, underscoring their critical role. For instance, in Germany, investments in dual-band chipsets for smartphones increased by 30% in 2021, supported by subsidies for digital infrastructure projects. Additionally, advancements in MU-MIMO technology have enhanced network efficiency, further amplifying demand.

The connected home devices segment is likely to register a CAGR of 25.5% in the next coming years. This growth is fueled by the increasing adoption of smart home technologies, which require seamless integration and reliable connectivity. For example, in Sweden, the rise of hybrid connectivity initiatives has led to a 35% increase in chipset installations for connected home devices, driven by investments in advanced biomanufacturing technologies.

COUNTRY ANALYSIS

Leading Countries in the European Wi-Fi Chipset Market

Germany was the largest and held 25.4% of the European Wi-Fi chipset market share in 2024 owing to its robust manufacturing base and extensive investments in smart city projects. The country’s IoT sector, which grew by 20% in 2022, drives demand for advanced chipsets. According to Eurostat, Germany accounts for over 30% of Europe’s total Wi-Fi chipset production by making it a hub for innovative solutions. For instance, in 2021, investments in tri-band systems led to a 25% increase in energy yield, supported by government incentives for renewable energy projects.

France is anticipated to grow with a CAGR of 12.3% in the next foreseen years owing to the growing focus on smart home automation and decentralized connectivity solutions. France’s Wi-Fi chipset capacity grew by 18% in 2022 was driven by investments in rural installations. Paris alone witnessed a 25% rise in Wi-Fi chipset installations in urban areas. Additionally, advancements in ferrite technology have amplified adoption by aligning with Europe’s focus on reducing carbon emissions.

KEY MARKET PLAYERS

Qualcomm Technologies, Inc, Broadcom, Intel Corporation, MediaTek, Inc., Infineon Technologies. are the market players that are dominating the Europe wi-fi chipset market.

Top 3 Players In The Market

Qualcomm Technologies

Qualcomm Technologies is a global leader in the Wi-Fi chipset market, renowned for its innovative solutions tailored to smartphones and connected home devices. The company’s focus on sustainability is evident in its development of energy-efficient chipsets, aligning with EU regulations. Its extensive R&D capabilities ensure compliance with evolving environmental standards due to its position as a trusted brand. Qualcomm’s strategic partnerships with local distributors ensure widespread market penetration, particularly in Germany and France.

Broadcom Inc.

Broadcom Inc. is a key player, known for its high-performance and durable Wi-Fi chipsets. The company’s product portfolio includes both single-band and dual-band systems, catering to diverse industrial needs. Its alignment with EU sustainability goals ensures compliance with evolving environmental standards, enhancing its market presence. Broadcom’s focus on digital transformation has led to the introduction of IoT-enabled systems for predictive maintenance by appealing to tech-savvy consumers.

Intel Corporation

Intel Corporation is a prominent manufacturer, offering specialized solutions tailored to desktop PCs and laptops. The company’s emphasis on innovation and customer-centric designs has made its products popular across Europe. Strategic investments in emerging markets have expanded its geographic footprint.

Top Strategies Used By Key Market Participants

Focus on Innovation

Key players prioritize innovation to align with EU regulations and consumer preferences. For instance, in March 2023, Qualcomm launched a range of AI-driven chipsets by enabling seamless integration with smart home projects.

Geographic Expansion

Geographic expansion is another key strategy. In January 2024, Broadcom established a new facility in Turkey is targeting the rapidly growing energy sector in Eastern Europe.

Partnerships and Collaborations

Partnerships and collaborations are a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Intel partnered with Orange SA to integrate IoT-enabled systems into smart energy ecosystems, supporting the expansion of connected solutions in France.

COMPETITION OVERVIEW

The European Wi-Fi chipset market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 30 major companies operate in the region by competing on factors such as product quality, pricing, and technological innovation. Global leaders like Qualcomm dominate the market by leveraging their extensive R&D capabilities and distribution networks. Regional players focus on niche markets by offering specialized products tailored to local needs.

RECENT HAPPENINGS IN THIS MARKET

- In April 2023, Qualcomm acquired a startup specializing in AI-driven chipsets by enhancing its product portfolio and strengthening its position as a leader in sustainable solutions.

- In June 2023, Broadcom partnered with Orange SA to integrate IoT-enabled systems into smart energy ecosystems by supporting the expansion of connected solutions in France.

- In August 2023, Intel launched a new line of eco-friendly chipsets in Spain by targeting the growing demand for renewable energy-compatible appliances in rural areas.

- In December 2023, Samsung introduced a range of high-efficiency chipsets in Germany by achieving energy reductions of up to 50% and reinforcing its dominance in energy-efficient technologies.

- In February 2024, Huawei announced the establishment of a new manufacturing facility in Poland by targeting the burgeoning energy sector in Eastern Europe and expanding its geographic footprint.

MARKET SEGMENTATION

This research report on the European Wi-Fi cheapest market is segmented and sub-segmented into the following categories.

By Bands

- Dual-Band

- Tri-Band

By MIMO

- SU-MIMO

- MU-MIMO

By Standards

- IEEE 802.11ac

- IEEE 802.11ax (Wi-Fi 6 & Wi-Fi 6E)

By Applications

- Smartphones

- Tablets

- PCs

- Access Point Equipment

- Connected Home Devices

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What factors are driving the growth of the Europe Wi-Fi chipset market?

Increasing demand for high-speed internet, IoT expansion, and the rise of smart devices.

Which industries are the major consumers of Wi-Fi chipsets in Europe?

Telecommunications, automotive, healthcare, consumer electronics, and industrial automation.

What are the latest technological advancements in Wi-Fi chipsets?

Wi-Fi 6E and Wi-Fi 7 adoption, improved power efficiency, and enhanced security features.

Who are the key players in the Europe Wi-Fi chipset market?

Companies like Qualcomm, Broadcom, Intel, MediaTek, and NXP Semiconductors.

What challenges does the Wi-Fi chipset market face in Europe?

Supply chain disruptions, regulatory standards, and increasing competition from 5G networks.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]