Europe Wholesale Voice Carrier Market Size, Share, Trends, & Growth Forecast Report By Services (Voice Termination, Interconnect Billing, and Fraud Management), Transmission Network, Technology, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Wholesale Voice Carrier Market Size

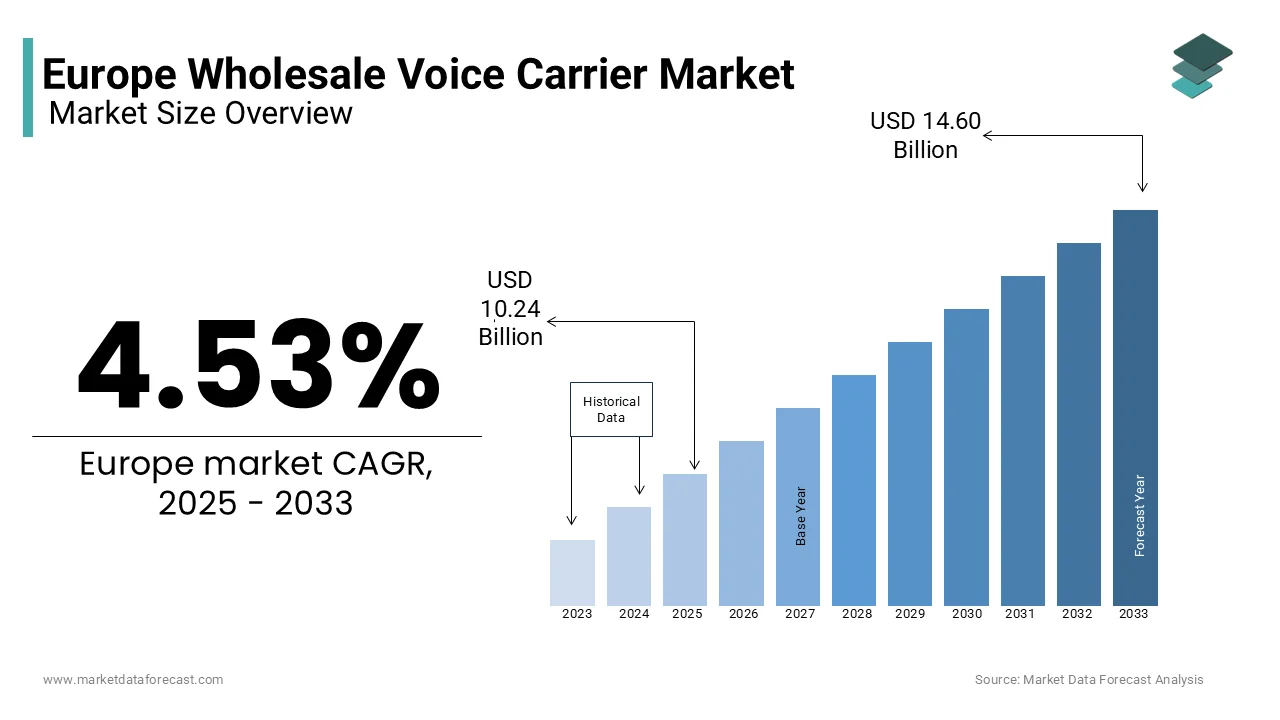

The Europe wholesale voice carrier market was worth USD 9.80 billion in 2024. The European market is projected to reach USD 14.60 billion by 2033 from USD 10.24 billion in 2025, growing at a CAGR of 4.53% from 2025 to 2033.

Wholesale voice carrier facilitates the seamless exchange of voice traffic between carriers, service providers, and enterprises across international borders. As noted by Telecoms.com, the wholesale voice market remains integral to global connectivity despite the growing adoption of over-the-top (OTT) services like WhatsApp and Zoom, which have disrupted traditional voice communication models.

In 2023, the European wholesale voice carrier market has witnessed steady demand due to the need for reliable and scalable communication solutions. Europe accounts for 25% of global wholesale voice traffic, with an estimated volume of 180 billion minutes annually. The advanced telecom infrastructure and high penetration of mobile and fixed-line services in Europe are likely to drive the European wholesale voice carrier market during the forecast period. However, declining voice revenues due to regulatory pressures and the rise of IP-based communication platforms are negatively impacting the market growth in this region. Despite these headwinds, innovations in Voice over Internet Protocol (VoIP) and advancements in 5G networks are creating new opportunities for growth. According to a study by Analysys Mason, VoIP traffic now constitutes over 70% of total wholesale voice traffic in Europe, which is reflecting the industry's shift toward digitalization. Furthermore, partnerships between traditional carriers and OTT players are emerging as a strategic response to maintain relevance in an evolving landscape.

MARKET DRIVERS

Growing Demand for International Connectivity

The increasing demand for international voice communication serves as a significant driver for the European wholesale voice carrier market. The strategic geographic position of Europe as a hub for global trade and migration has amplified the need for cross-border communication solutions. According to Eurostat, international call volumes from Europe exceeded 50 billion minutes in 2022, with businesses accounting for nearly 60% of this traffic. The proliferation of multinational corporations and the rise of remote work have further fueled this demand, as seamless communication becomes critical for operational efficiency. Additionally, the European Union’s Digital Decade initiative emphasizes enhancing connectivity infrastructure, which indirectly supports the growth of wholesale voice services. As noted by the International Telecommunication Union (ITU), Europe’s robust telecom regulatory framework ensures high-quality international calling standards, making it an attractive market for global carriers seeking reliable partnerships.

Transition to IP-Based Technologies

The rapid adoption of Internet Protocol (IP)-based technologies is another key driver propelling the European wholesale voice carrier market forward. Traditional circuit-switched networks are being replaced by Voice over IP (VoIP) and Session Initiation Protocol (SIP) trunking solutions, enabling cost-efficient and scalable communication services. As per a report by the European Commission, VoIP traffic now accounts for over 75% of all wholesale voice traffic in the region owing to the investments in next-generation networks. Furthermore, the deployment of 5G infrastructure across Europe, as documented by the European Telecommunications Network Operators’ Association (ETNO), has accelerated the integration of IP-based systems, which is enhancing call quality and reducing latency. This technological shift not only lowers operational costs for carriers but also aligns with sustainability goals by reducing energy consumption. The transition to IP-based systems ensures that the wholesale voice market remains relevant amidst the growing competition from OTT platforms, offering a future-proof solution for voice communication needs.

MARKET RESTRAINTS

Declining Voice Revenues Due to Regulatory Pressures

Regulatory interventions and pricing pressures have significantly restrained the European wholesale voice carrier market. The stringent telecom regulations of the European Union that are aimed at promoting fair competition have led to a decline in termination rates, which is the fees carriers charge each other for connecting calls. According to the Body of European Regulators for Electronic Communications (BEREC), average mobile termination rates in Europe dropped by 80% between 2015 and 2022, reducing carrier profitability. This regulatory push has forced carriers to lower their prices, squeezing margins in an already competitive market. Additionally, fixed-line voice revenues have plummeted by over 40% in the past decade, as reported by Eurostat, due to the shift toward digital communication platforms. These regulatory measures, while beneficial for consumers, have created financial challenges for traditional voice carriers, compelling them to explore alternative revenue streams to sustain operations in an evolving telecom landscape.

Intense Competition from Over-the-Top (OTT) Services

The rapid rise of Over-the-Top (OTT) communication platforms has emerged as a major restraint for the European wholesale voice carrier market. Services such as WhatsApp, Zoom and Microsoft Teams have captured a significant share of the communication market that offer free or low-cost alternatives to traditional voice calls. As per a study by the European Telecommunications Network Operators’ Association (ETNO), OTT services now account for over 60% of international communication traffic in Europe, drastically reducing reliance on conventional voice carriers. Furthermore, Statista reports that the number of OTT users in Europe surpassed 400 million in 2023 owing to the widespread smartphone adoption and affordable data plans. This shift has not only eroded the customer base of wholesale voice carriers but also intensified price wars, further straining their revenue models. As consumer preferences continue to evolve, carriers face mounting pressure to innovate and differentiate themselves to remain competitive in this disrupted market.

MARKET OPPORTUNITIES

Rising Demand for Cloud-Based Communication Solutions

The European wholesale voice carrier market is witnessing a significant opportunity in the growing adoption of cloud-based communication solutions owing to the increasing need for scalable and cost-effective services. According to Eurostat, the adoption of cloud computing services across Europe has grown by 18% annually over the past five years, with businesses increasingly shifting from traditional on-premises systems to cloud-based platforms. This trend is particularly evident in the telecommunications sector, where wholesale voice carriers are leveraging cloud technologies to enhance service delivery and operational efficiency. For instance, cloud-based Voice over Internet Protocol (VoIP) solutions have gained traction to enable carriers to offer high-quality voice services at reduced costs. According to the European Telecommunications Network Operators' Association, VoIP traffic in Europe is projected to grow at an exponential CAGR owing to the rising demand for unified communication platforms that integrate voice, video, and messaging services. The scalability of cloud-based solutions allows wholesale carriers to cater to both small enterprises and large multinational corporations to expand their customer base. Furthermore, the integration of artificial intelligence and machine learning into cloud platforms has enabled carriers to offer advanced features such as real-time analytics and automated customer support, enhancing user experience. This technological shift not only reduces infrastructure costs but also positions wholesale voice carriers as key enablers of digital transformation in the European business landscape.

Expansion into Emerging Markets and Rural Connectivity Initiatives

Another major opportunity for the European wholesale voice carrier market lies in the untapped potential of emerging markets and rural connectivity initiatives. According to the European Investment Bank, approximately 25% of the European population resides in rural areas, many of which still lack access to reliable and affordable voice communication services. Governments and regulatory bodies across Europe are actively investing in digital infrastructure to bridge this gap, creating opportunities for wholesale carriers to expand their reach. For example, the European Commission’s Digital Decade initiative aims to achieve 100% broadband coverage by 2030, allocating €2 billion in funding for rural connectivity projects. This initiative has already spurred partnerships between wholesale carriers and local governments, enabling the deployment of advanced voice and data networks in underserved regions. Additionally, emerging economies in Eastern Europe, such as Poland and Romania, are experiencing rapid urbanization and industrial growth, driving demand for robust communication infrastructure. According to the International Telecommunication Union, the telecommunications market in these regions is expected to grow by 10% annually over the next five years. By leveraging their expertise in network deployment and management, European wholesale voice carriers can establish a strong foothold in these markets, diversifying their revenue streams and contributing to regional economic development. This strategic expansion not only aligns with broader digital inclusion goals but also strengthens the competitive positioning of carriers in the global telecommunications landscape.

MARKET CHALLENGES

Cybersecurity Threats in Voice Communication Networks

The increasing reliance on digital infrastructure has made cybersecurity a critical challenge for the European wholesale voice carrier market. As carriers transition to IP-based systems, they become more vulnerable to cyberattacks such as Distributed Denial of Service (DDoS) and toll fraud. The European Union Agency for Cybersecurity (ENISA) reported that telecom-related cyber incidents surged by 30% in 2022, with voice networks being a prime target due to their widespread connectivity. These attacks not only disrupt services but also lead to significant financial losses, estimated at €1 billion annually across Europe, according to ENISA. Furthermore, the General Data Protection Regulation (GDPR) imposes strict penalties for data breaches, adding regulatory pressure on carriers to enhance security measures. Addressing these vulnerabilities requires substantial investment in advanced encryption and monitoring technologies that smaller carriers often struggle to afford, which is creating an uneven playing field in the market.

Fragmented Regulatory Landscape Across Europe

The fragmented regulatory environment across European countries poses another major challenge for the wholesale voice carrier market. While the European Union aims to harmonize telecom regulations, disparities remain in national policies, creating operational complexities for carriers operating across borders. According to a report by the Body of European Regulators for Electronic Communications (BEREC), compliance costs for multinational carriers have risen by 25% over the past five years due to varying national requirements. For instance, some countries impose higher taxes on international call traffic, while others enforce stricter data localization laws. Additionally, as per Eurostat, cross-border disputes over termination rates and service quality standards have increased by 40% since 2020, delaying network upgrades and stifling innovation. This lack of uniformity hinders seamless collaboration between carriers and undermines efforts to create a truly unified European telecom market, impeding long-term growth prospects.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

4.53% |

|

Segments Covered |

By Services, Transmission Network, Technology, Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

At&T Inc., Bics, Bt Group, Deutsche Telekom Ag, Idt Corporation, Lumen Technologies, Orange S.A., Telefónica S.A., Tata Communication, and Verizon Communications, Inc. |

SEGMENTAL ANALYSIS

By Services Insights

The voice termination segment accounted for 6.2% of the European wholesale voice carrier market share in 2024 owing to its critical role in routing international calls across networks to ensure seamless global communication. Despite declining termination rates, the voice termination segment remains vital due to high call volumes, with over 180 billion minutes processed annually. The shift to IP-based systems to enable cost-efficient operations is further contributing to the expansion of the voice termination segment in the European market.

The fraud management segment is anticipated to progress at a CAGR of 12.5% over the forecast period owing to the growing telecom fraud in Europe and increasing demand for advanced AI-driven solutions. BEREC highlights a 50% reduction in fraud incidents through real-time detection systems, underscoring their importance. As cyber threats escalate, carriers prioritize fraud prevention to protect networks and comply with GDPR, making this segment pivotal for sustainable growth.

By Transmission Network Insights

The owned networks segment held 55.1% of the European market share in 2024 owing to the superior control over infrastructure of owned networks the enable carriers to deliver high-quality voice services with minimal latency. The Body of European Regulators for Electronic Communications (BEREC) highlights that carriers using owned networks reduce operational costs by 15% compared to leased alternatives. Additionally, investments in 5G and fiber-optic technologies have enhanced their capacity, with ETNO reporting a 20% improvement in service reliability. Owned networks are pivotal for handling IP-based traffic, which constitutes over 70% of voice traffic, ensuring scalability and long-term competitiveness in the evolving telecom landscape.

The leased networks segment is predicted to witness the fastest CAGR of 8.3% over the forecast period owing to the increasing demand for cost-effective solutions, particularly among smaller carriers and in underserved regions. According to Eurostat, leased networks enable rapid expansion without heavy capital investment, making them ideal for cloud-based communication platforms. The rise of VoIP and SIP trunking has further fuelled adoption, with leased networks supporting 40% of new IP-based connections. Their flexibility and scalability are critical in meeting dynamic market needs, ensuring broader connectivity across Europe while complementing the limitations of owned networks in remote areas.

By Technology Insights

The VoIP segment ruled the market by occupying a share of 70.3% in the European market in 2024. The growth of the VoIP segment is fuelled by cost-efficiency, reducing call termination costs by up to 40% compared to traditional switching, according to BEREC. The adoption of 5G and fiber-optic networks has further accelerated its growth, with ETNO reporting that over 80% of new voice traffic in Europe is IP-based. VoIP’s scalability and ability to integrate with cloud services make it essential for modern communication needs, supporting features like video conferencing and unified communications. As carriers transition to digital infrastructure, VoIP ensures future-proof solutions, driving its dominance in the market.

REGIONAL ANALYSIS

Germany dominated the European wholesale voice carrier market with 22.7% of the European market share in 2024. The dominating position of Germany in the European market is primarily due to its robust telecom infrastructure that supports high volumes of international voice traffic. The investments by the German government in 5G and fiber-optic networks have further strengthened its position, which is enabling seamless IP-based communication. According to the Body of European Regulators for Electronic Communications (BEREC), the strategic location of Germany as a hub for cross-border trade amplifies demand for reliable wholesale voice services. Additionally, the presence of major carriers like Deutsche Telekom has enhanced the country’s capacity to handle over 30 billion voice minutes annually, making it a critical player in the European market.

The UK follows Germany closely and accounted for a prominent share of the European market in 2024. The growth of the UK market is driven by its status as a global fintech and tech innovation hub, with London serving as a gateway for international communication. The advanced regulatory framework of the UK, overseen by Ofcom, ensures high-quality voice services and fosters competition. As per the research by the International Telecommunication Union (ITU), the UK accounts for nearly 25% of Europe’s VoIP traffic, which is indicating its rapid adoption of digital technologies. Furthermore, partnerships between traditional carriers and OTT platforms have positioned the UK as a leader in integrating legacy systems with next-generation solutions, ensuring sustained growth in the wholesale voice market.

France secures the third position in the European market. The focus of France on digital transformation, particularly in AI and smart city initiatives, has fueled demand for scalable voice solutions. The French government’s push for universal broadband coverage and 5G deployment has significantly enhanced network capabilities, enabling efficient voice termination services. BEREC reports that France processes over 20 billion international voice minutes annually, driven by its strong industrial and commercial sectors. Additionally, the presence of leading carriers like Orange has bolstered France’s ability to innovate and maintain a competitive edge in the European wholesale voice carrier market, ensuring long-term relevance amidst evolving communication trends.

KEY MARKET PLAYERS

The major players in the Europe wholesale voice carrier market include At&T Inc., Bics, Bt Group, Deutsche Telekom Ag, Idt Corporation, Lumen Technologies, Orange S.A., Telefónica S.A., Tata Communication, and Verizon Communications, Inc.

MARKET SEGMENTATION

This research report on the Europe wholesale voice carrier market is segmented and sub-segmented into the following categories.

By Services

- Voice Termination

- Interconnect Billing

- Fraud Management

By Transmission Network

- Owned Network

- Leased Network

By Technology

- VoIP

- Traditional Switching

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What drives the demand for wholesale voice services in Europe?

The demand is driven by increased international call traffic, VoIP adoption, enterprise communication needs, and growing mobile and fixed-line connections.

Which industries rely the most on wholesale voice carriers in Europe?

Key industries include telecom operators, call centers, financial services, travel and hospitality, and multinational corporations that require global communication solutions.

What role does artificial intelligence play in the Europe Wholesale Voice Carrier Market?

AI is used for fraud detection, traffic optimization, predictive analytics, and automated troubleshooting to enhance network efficiency and security.

What is the future outlook for the Europe Wholesale Voice Carrier Market?

The market is expected to continue evolving with the growth of cloud-based voice solutions, 5G expansion, and increased adoption of AI-driven telecom services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]