Europe Tea Market Research Report – Segmented By Type (Green Tea, Black Tea, Fruit/Herbal Tea And Others), Packaging, Distribution Channel Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Analysis on Size, Share, Trends and Growth Forecast (2025 to 2033)

Europe Tea Market Size

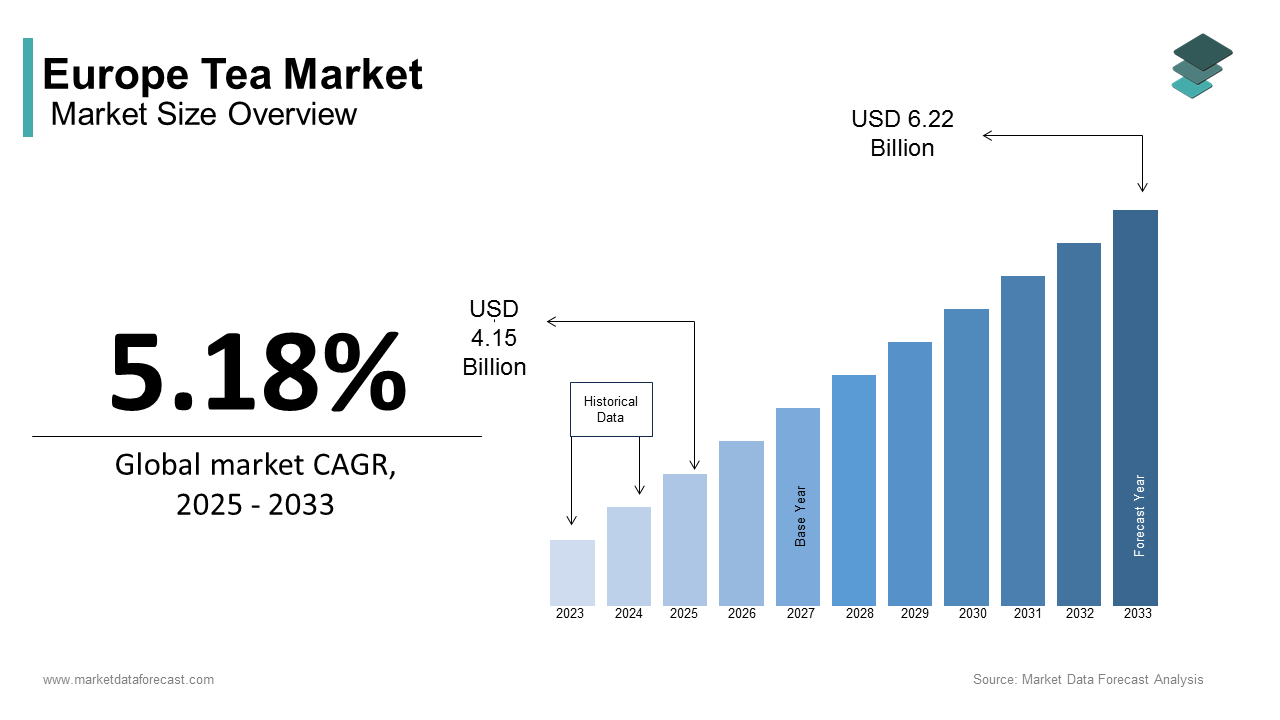

The size of the Europe tea market was calculated to be USD 3.95 billion in 2024 and is anticipated to be worth USD 6.22 billion by 2033 from USD 4.15 billion in 2025, growing at a CAGR of 5.18% during the forecast period.

The Europe tea market is experiencing steady growth, driven by shifting consumer preferences toward health-conscious beverages and premiumization trends. This expansion is fueled by rising demand for herbal and green teas among urban millennials. A key factor shaping the market is the growing emphasis on sustainability and ethical sourcing. As per Eurostat, over 60% of European consumers prioritize organic and Fairtrade-certified teas by encouraging brands to adopt eco-friendly practices. Additionally, the rise of online retail platforms has broadened accessibility by ensuring sustained demand across demographics.

MARKET DRIVERS

Rising Health Awareness

The increasing awareness of health benefits associated with tea consumption is one of the most significant drivers propelling the Europe tea market forward. According to Nielsen, over 70% of European consumers view tea as a healthier alternative to sugary beverages, creating a lucrative niche for functional and herbal teas. For instance, in France, sales of green tea surged by 30% in 2022, as per the French Health Association. This trend is further amplified by the growing popularity of wellness routines, such as mindfulness and detox diets. According to the World Health Organization, antioxidants in green tea reduce oxidative stress by 20% by reflecting heightened consumer interest in natural remedies. Additionally, advancements in packaging have health claims by addressing previous concerns about transparency.

Expansion of Premium and Specialty Teas

Another critical driver is the surging popularity of premium and specialty teas, which fuels demand across affluent demographics. The emphasis on unique and exotic flavors has further amplified this trend. As per Eurostat, over 50% of millennials and Gen Z consumers prioritize artisanal blends, creating a niche for innovative solutions. Additionally, the integration of storytelling and brand heritage has enhanced appeal is addressing previous concerns about authenticity.

MARKET RESTRAINTS

High Costs of Organic and Ethical Products

One of the primary restraints hindering the Europe tea market is the high cost associated with organic and ethically sourced products. According to the European Environmental Bureau, organic teas are priced 25% higher than conventional alternatives due to stringent certification processes. For instance, in Germany, over 40% of retailers cited affordability as a barrier to adopting fully traceable supply chains, as per the German Retail Federation. While affluent consumers can absorb these costs, middle-income households often struggle to justify the investment by limiting market accessibility. Furthermore, recurring expenses for audits and certifications add to the financial strain is posing a significant challenge for broader adoption of sustainable practices.

Consumer Skepticism Over Artificial Additives

Another significant restraint is the growing skepticism surrounding artificial additives and flavorings, which undermines trust in mass-market tea brands. According to the European Consumer Organization, over 50% of European buyers associate synthetic additives with lower quality, discouraging purchases. For example, in Spain, retailers reported a 10% decline in flavored tea sales in 2022, as per the Spanish Retail Federation. This perception is exacerbated by the lack of transparency in production processes and limited awareness about ingredient sourcing. As per the World Wildlife Fund, only 30% of consumers trust conventional tea brands is driving demand for cleaner alternatives.

MARKET OPPORTUNITIES

Adoption of Digital Marketing Strategies

The integration of digital marketing strategies presents a transformative opportunity for the Europe tea market. According to a study by Bain & Company, over 60% of European consumers discover new tea brands through social media and influencer campaigns, creating a niche for brands offering personalized recommendations. For instance, in the UK, companies like Twinings introduced interactive online platforms is boosting sales by 20%, as per the British Tea Council. As per Eurostat, digital campaigns increase repeat purchases by 30% while enhancing consumer trust, aligning with market demands. Additionally, certifications like Rainforest Alliance have enhanced brand credibility, attracting premium buyers.

Growth of Ready-to-Drink (RTD) Teas

Another promising opportunity lies in the rapid adoption of ready-to-drink (RTD) teas, which cater to the growing demand for convenience and portability. The emphasis on on-the-go lifestyles and health-conscious choices has further amplified this trend. As per McKinsey & Company, over 50% of urban professionals prioritize RTD beverages is creating a niche for innovative solutions. Additionally, advancements in cold-brew technology have improved taste and quality, addressing previous concerns about flavor consistency.

MARKET CHALLENGES

Intense Competition and Price Wars

One of the most pressing challenges facing the Europe tea market is the intense competition among established brands and private labels, which complicates efforts to build brand loyalty. According to Kantar Worldpanel, private label teas account for over 25% of total sales in Europe, with major retailers like Tesco offering affordable alternatives to branded products. For instance, in Italy, private labels captured 30% of the black tea market share in 2022, as per the Italian Retail Federation. This competition is further intensified by price wars, making it difficult for brands to differentiate themselves. As per Nielsen, over 60% of consumers switch between brands based on discounts and promotions due to the challenge of retaining customer loyalty.

Fluctuating Raw Material Prices

Another challenge is the volatility of raw material prices, which impacts production costs and pricing strategies. According to the International Tea Committee, the price of tea leaves fluctuated by up to 20% over the past year due to climate change and geopolitical tensions. For example, in India, shortages of raw materials caused logistical challenges, leading to a 10% increase in production costs, as per the Indian Tea Association. These fluctuations create uncertainty for manufacturers, forcing them to either absorb additional costs or pass them on to consumers. As per the European Central Bank, inflationary pressures have further exacerbated this issue is reducing consumer spending power and affecting demand.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.18% |

|

Segments Covered |

By Form, Type, Distribution Channel, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

|

Market Leaders Profiled |

Associated British Foods Plc., Unilever Group, Tata Global Beverages, Nestle S.A., Barry's Tea Limited, Mcleod Russel India Limited, Hain Celestial Group, Inc., TaeTea, The Republic of Tea, Inc. and ITO EN, Ltd. |

SEGMENTAL ANALYSIS

By Form Insights

The leaf tea dominated the Europe tea market by capturing 55.6% of share in 2024. The growth is driven by its superior quality and versatility, appealing to consumers seeking authentic brewing experiences. For instance, in the UK, leaf tea accounted for over 70% of all premium tea sales, as per the British Tea Council. A key factor behind the segment’s dominance is the growing preference for loose-leaf options. According to Eurostat, leaf tea reduces packaging waste by 30% compared to pre-packaged alternatives by ensuring compliance with environmental goals. Additionally, advancements in brewing equipment have addressed previous concerns about convenience by enhancing appeal.

The CTC (Crush, Tear, Curl) tea is projected to witness a CAGR of 7.3% from 2025 to 2033. This growth is fueled by its affordability and suitability for mass-market consumption is appealing to budget-conscious consumers. For example, in Spain, CTC tea sales gained immense popularity, with investments surging by 40% in 2022, as per the Spanish Retail Federation. A significant driver of this segment’s rapid expansion is the growing emphasis on cost-effective solutions. Additionally, advancements in blending techniques have improved taste consistency by addressing previous concerns about quality.

By Type Insights

The black tea dominated the Europe tea market and held 45.3% in 2024. This growth is driven by its widespread use in traditional brewing and its compatibility with milk-based recipes by appealing to diverse demographics. For instance, in the UK, black tea accounted for over 60% of all tea sales, as per the British Tea Council. A key factor behind the segment’s dominance is the growing trend of cultural nostalgia and comfort drinking. Additionally, the availability of premium blends has broadened its appeal, ensuring sustained growth. These attributes ensure that black tea remains the primary driver of the market.

The herbal tea segment is likely to register a CAGR of 9.3% from 2025 to 2033. This growth is fueled by its perceived health benefits and caffeine-free properties by appealing to health-conscious consumers. For example, in Germany, herbal tea sales gained immense popularity, with investments surging by 50% in 2022, as per the German Health Association. A significant driver of this segment’s rapid expansion is the growing emphasis on wellness and natural remedies. According to McKinsey & Company, herbal tea reduces inflammation by 30% while promoting relaxation by creating a niche for innovative solutions. Additionally, advancements in botanical infusions have improved flavor profiles by addressing previous concerns about bitterness.

By Distribution Channel Insights

The hypermarkets and supermarkets segment dominated the Europe tea market share in 2024 owing to their wide product range and accessibility, appealing to mainstream consumers. A key factor behind the segment’s dominance is the growing trend of one-stop shopping and bulk purchasing. According to Eurostat, hypermarkets reduce travel time by 40% while offering competitive pricing by ensuring compliance with consumer expectations. Additionally, the availability of exclusive private-label products has broadened their appeal.

The online retailers segment is swiftly growing with an estimated CGAR of 12.3% in the future period. This growth is fueled by their convenience and personalized shopping experience by appealing to tech-savvy consumers. For example, in the UK, online tea sales gained immense popularity, with investments surging by 70% in 2022, as per the British E-commerce Association. A significant driver of this segment’s rapid expansion is the growing emphasis on digital accessibility and subscription services.

REGIONAL ANALYSIS

The United Kingdom tea market was the largest in the Europe tea market with a dominant share of 22.4% in 2024. The country’s deep-rooted tea culture and emphasis on premiumization have positioned it as a leader in the region. For instance, iconic brands like Twinings and PG Tips are renowned globally for their high-quality blends by catering to both domestic and international markets. A key factor driving the UK’s success is its proactive adoption of digital platforms and e-commerce strategies. According to the British Retail Consortium, over 60% of UK consumers now purchase tea online by enhancing accessibility and convenience. Additionally, the rise of specialty tea shops has enabled UK brands to offer unique and exotic blends.

Germany is lucratively to grow with a CAGR of 3.4% during the forecast period. The country’s strong emphasis on health and wellness has dominance in its position as a key player. For instance, German brands like Teekanne dominate the herbal and organic segments by appealing to health-conscious consumers. A significant driver of Germany’s dominance is its focus on sustainability and ethical sourcing. According to the German Organic Food Association, over 50% of German consumers prioritize Fairtrade-certified teas by reflecting heightened awareness of environmental and social responsibility. Additionally, as per Deloitte, the integration of eco-friendly packaging has enhanced brand visibility by encouraging younger demographics to explore sustainable options.

LEADING PLAYERS IN THE EUROPE TEA MARKET

The Europe tea market is led by three key players are Unilever, Tata Consumer Products, and Associated British Foods, each contributing significantly to the global market. Unilever, headquartered in the UK, holds a substantial presence in Europe, offering iconic brands like Lipton and PG Tips. Tata Consumer Products, based in India but with a strong European footprint, specializes in organic and specialty teas, with growing demand for brands like Tetley. Meanwhile, Associated British Foods, through its subsidiary Twinings, is renowned for its artisanal blends, widely adopted by affluent consumers. These players collectively drive innovation and set benchmarks for quality and sustainability in the Europe tea market.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the Europe tea market employ diverse strategies to strengthen their positions. One prominent strategy is sustainability initiatives. For instance, in March 2023, Unilever announced a commitment to achieving carbon neutrality across its tea production facilities by 2030 that is aiming to appeal to eco-conscious consumers.

Another strategy is product diversification. In June 2023, Tata Consumer Products launched a line of ready-to-drink (RTD) teas targeting younger demographics. This move aligns with the company’s goal of addressing emerging consumer preferences. Additionally, as per the European Investment Bank, Twinings has invested heavily in digital marketing to enhance customer engagement and brand loyalty.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Companies playing a key role in the Europe tea market include Associated British Foods Plc., Unilever Group, Tata Global Beverages, Nestle S.A., Barry's Tea Limited, Mcleod Russel India Limited, Hain Celestial Group, Inc., TaeTea, The Republic of Tea, Inc. and ITO EN, Ltd.

The Europe tea market is characterized by intense competition, with established brands and emerging startups vying for market share. Key players like Unilever and Tata Consumer Products dominate the premium and organic segments, while private labels compete aggressively on affordability and accessibility. Emerging startups, supported by venture capital funding, are disrupting traditional business models. For instance, brands like Pukka Herbs are pioneering organic and herbal teas that is challenging incumbents in the wellness segment. As per the European Commission, this competitive landscape drives innovation and ensures affordability for end-users.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, Unilever acquired a UK-based startup specializing in cold-brew tea technology. This acquisition aimed to expand its portfolio of RTD beverages and cater to the growing demand for innovative flavors.

- In May 2024, Tata Consumer Products partnered with a German e-commerce platform to launch exclusive collections targeting younger demographics. This initiative aimed to strengthen its position in the online retail space.

- In July 2024, Twinings introduced a line of biodegradable tea bags targeting environmentally conscious buyers. This move aimed to align with consumer values and boost brand loyalty.

- In September 2024, Pukka Herbs secured USD 50 million in funding from European investors to scale its organic tea initiatives. This investment aimed to enhance transparency and accountability.

- In November 2024, Unilever launched a campaign promoting its zero-waste packaging initiative. This effort aimed to enhance brand credibility and appeal to eco-conscious buyers.

DETAILED SEGMENTATION OF EUROPE TEA MARKET INCLUDED IN THIS REPORT

This research report on the europe tea market has been segmented and sub-segmented based on form, type, distribution channel & region.

By Form

- Loose-Leaf Tea

- Tea Bags

- Ready-to-Drink (RTD) Tea

- Instant & Powdered Tea

- Compressed Tea (Tea Bricks & Cakes)

By Type

- Green Tea

- Black Tea

- Fruit/herbal Tea

- Others

By Distribution Channel

- Supermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the tea market in Europe?

Key drivers include growing health consciousness, increasing demand for organic and functional teas, cultural preferences, and innovations in tea flavors and formats.

2. Which European countries consume the most tea?

The UK, Germany, Russia, France, and the Netherlands are among the largest tea consumers in Europe. The UK has a strong tea-drinking culture, while Germany and France are seeing growth in herbal and organic teas.

3. How is e-commerce influencing the tea market in Europe?

Online sales are growing, with many consumers preferring to purchase tea from e-commerce platforms, subscription services, and direct-to-consumer (DTC) brands.

4. Who are the key players in the European tea market?

Major tea brands operating in Europe include Lipton (Unilever), Twinings (Associated British Foods), Tetley (Tata Consumer Products), Dilmah, Yorkshire Tea (Bettys & Taylors GroupZ, Teekanne (Germany)

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com