Europe Stationary Fuel Cell Market Size, Share, Trends & Growth Forecast Report By Capacity (<3 kW, 3 kW – 10 kW, 10 kW – 50 kW, >50 kW), End-Use, Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Stationary Fuel Cell Market Size

The Europe Stationary Fuel Cell market size was valued at USD 188.44 million in 2024. The European market size is estimated to be worth USD 394.64 million by 2033 from USD 204.57 million in 2025, growing at a CAGR of 8.56% from 2025 to 2033.

The European stationary fuel cell market is gaining momentum as countries explore sustainable energy alternatives and decentralized power generation. Nations like Germany, France, and the UK are leading adoption efforts, supported by strong climate policies and investments in renewable energy infrastructure. Stationary fuel cells are increasingly considered for combined heat and power (CHP) applications in both residential and commercial settings. Technological innovations, including the development of hydrogen-based systems, are improving performance and efficiency. In parallel, regulatory initiatives such as the EU Green Deal are shaping the sector's direction by promoting low-carbon technologies and encouraging cleaner energy transitions across member states.

MARKET DRIVERS

Growing Demand for Clean Energy Solutions

Clean energy adoption is a key driver of the stationary fuel cell market, particularly in Europe’s advanced economies. According to the European Environment Agency, renewable sources accounted for 24.5% of the EU’s final energy consumption in 2023, creating demand for reliable and sustainable power solutions. The rise of smart cities further accelerates this trend, with IoT-enabled fuel cells optimizing energy distribution. Additionally, government subsidies further accelerate adoption.

Increasing Adoption of Combined Heat and Power (CHP) Systems

CHP systems are another significant driver and is fueled by the growing need for energy-efficient solutions in residential and commercial sectors. Industries like healthcare and manufacturing utilize these systems to reduce operational costs and enhance reliability. Government initiatives, such as tax incentives for eco-friendly technologies, further accelerate adoption. These innovations align with consumer preferences for sustainability making CHP a key growth driver in the coming years.

MARKET RESTRAINTS

High Initial Investment Costs

One of the primary restraints is the high cost of implementing stationary fuel cell systems. While larger corporations can afford these technologies, SMEs often struggle to justify the expense, particularly in regions with lower GDP per capita. Maintenance costs further exacerbate the financial burden. Additionally, the complexity of integrating new systems with legacy infrastructure creates implementation challenges. These barriers limit market penetration where industrial modernization lags behind Western counterparts.

Limited Hydrogen Infrastructure

Limited hydrogen infrastructure poses another significant restraint, with rising demand for hydrogen-based fuel cells outpacing supply capabilities. According to the European Hydrogen Association, Europe is actively expanding its hydrogen refueling infrastructure which is not enough and is hindering widespread adoption. This disparity creates inequalities in energy accessibility, particularly for rural areas. Additionally, older demographics face challenges adapting to new technologies. These issues create barriers to widespread adoption, slowing market growth in certain regions.

MARKET OPPORTUNITIES

Expansion of Hydrogen-Based Fuel Cells

Hydrogen-based fuel cells present a lucrative opportunity for the market, driven by Europe’s commitment to sustainability. Innovations such as solar-powered liquid cooling systems reduce reliance on grid electricity, achieving decrease in operational costs. For instance, Equinix and Siemens are involved in sustainability-related initiatives. Government incentives, such as tax breaks for eco-friendly technologies, further accelerate adoption. These factors position renewable energy integration as a key growth driver, outpacing traditional cooling methods in the coming years.

Rise of Edge Computing Solutions

Edge computing solutions offer another significant opportunity, particularly in urban areas with limited space and high latency demands. Liquid cooling technologies, such as direct-to-chip solutions, enable seamless integration into small-scale facilities, reducing energy consumption. Additionally, innovations like modular designs enhance scalability. These initiatives align with consumer preferences for low-latency services, making edge computing a key growth driver.

MARKET CHALLENGES

Integration with Legacy Systems

Integrating stationary fuel cell systems with legacy infrastructure remains a significant challenge. Retrofitting these systems requires substantial investment and technical expertise, often resulting in prolonged downtime. Compatibility issues between platforms create interoperability hurdles, limiting flexibility. These challenges hinder the seamless adoption of innovative solutions, particularly in traditional industries.

Regulatory Compliance Complexity

Regulatory compliance poses another major challenge, with stringent standards like GDPR and the EU Emissions Trading System impacting implementation decisions. According to the European Data Protection Board, a notable portion of data center operators face difficulties ensuring compliance, particularly when handling sensitive industrial data. Cybersecurity threats further exacerbate risks, with ransomware attacks increasing in 2023, as per Europol. These issues create a cautious investment climate, delaying the adoption of advanced stationary fuel cell solutions and slowing market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.56% |

|

Segments Covered |

By Capacity, End-Use, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Bloom Energy, Cummins, Fuji Electric Europe, FuelCell Energy, AFC Energy, Ballard Power Systems, Nuvera Fuel Cells, Plug Power, SFC Energy, Siemens Energy, and Toshiba Energy Systems and Solutions Corporation, and others. |

SEGMENT ANALYSIS

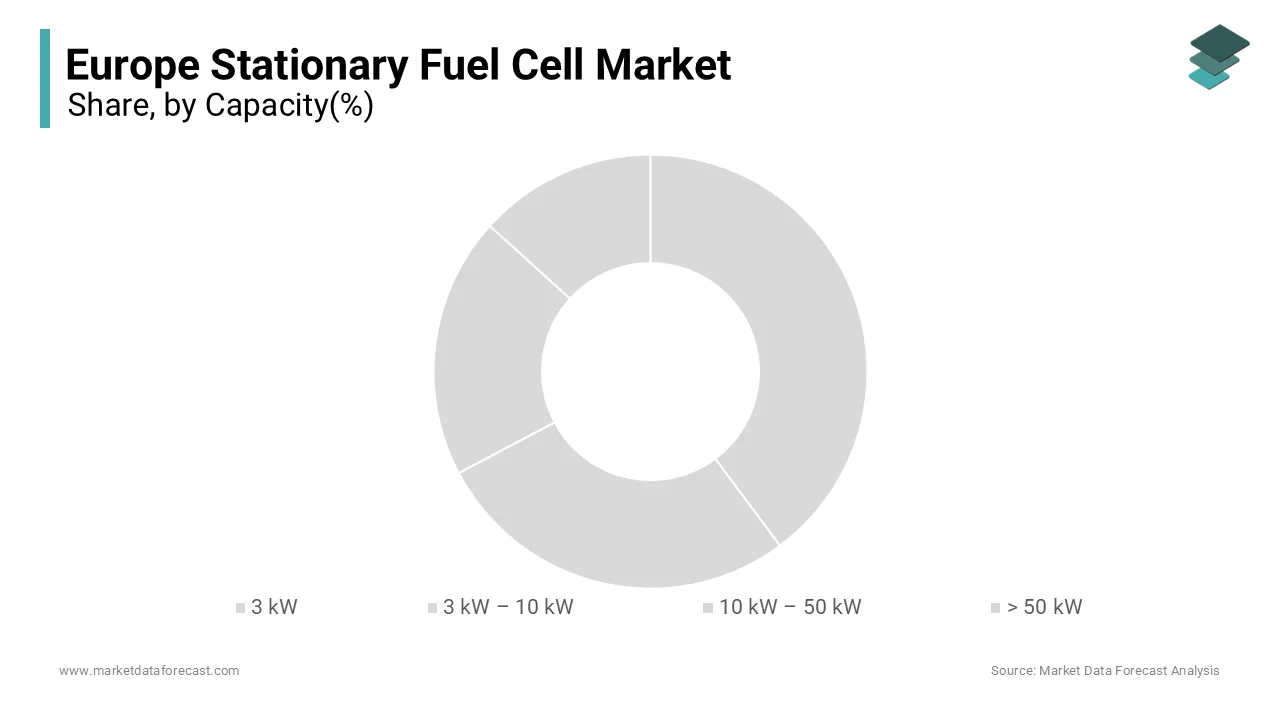

By Capacity Insights

The 10 kW – 50 kW capacity segment dominated the European stationary fuel cell market by holding a 45.7% share in 2024. This dominance is because of its suitability for medium-scale applications, such as commercial buildings and small industrial facilities. Countries like Germany and France lead adoption. According to Eurostat, these systems achieve a reduction in energy costs, ensuring consistent performance. Also, innovations like modular designs enhance scalability, addressing urban real estate constraints. These factors collectively sustain the segment’s place, despite the growing popularity of higher-capacity systems.

The >50 kW segment is the fastest-growing, with a CAGR of 18.3%. This growth is fueled by the increasing demand for large-scale energy solutions, particularly in industrial and utility sectors. Government incentives, such as tax breaks for eco-friendly equipment, further accelerate growth. For instance, the UK offers subsidies for electric cranes, boosting sales. Technological advancements. These factors position >50 kW systems as the future of the market, outpacing traditional segments in growth potential.

By End-Use Insights

The residential applications segment commanded the European stationary fuel cell market by accounting for 40.6% of the total share in 2024. This is propelled by the sector’s reliance on decentralized energy solutions, which reduce reliance on grid electricity. Germany, Europe’s largest hub for fuel cell adoption, utilizes these systems in residential facilities. According to Eurostat, these systems reduce energy costs, ensuring consistent quality. Additionally, innovations like smart home integration enhance usability, addressing diverse homeowner needs. These factors collectively sustain the segment’s leadership, despite the growing demand from commercial sectors.

Industrial/utility applications are the fastest-growing end-use segment, with a CAGR of 20.2%. This development is caused by the need for scalable and reliable energy solutions, particularly in manufacturing and power generation. Countries like France and Spain lead adoption, with companies. Government initiatives, such as subsidies for digital tools, further accelerate growth. For instance, Enel achieved increase in energy efficiency in 2023, driven by fuel cell integration. These factors position industrial/utility applications as a key growth driver, outpacing traditional industries in the coming years.

By Application Insights

CHP applications prevailed in the European stationary fuel cell market by accounting for 51.1% of the total share in 2024. This is caused by the sector’s reliance on energy-efficient solutions, which reduce operational costs and enhance reliability. Germany and the UK lead adoption, with a notable portion of installations in residential and commercial sectors. According to Eurostat, these systems improve energy efficiency, ensuring optimal resource allocation. Also, innovations like IoT-enabled monitoring enhance scalability, addressing regulatory compliance requirements. These factors collectively sustain the segment’s leadership, despite the growing demand from other applications.

Prime power applications segment is the fastest-growing segment, with a CAGR of 16.8% in the future. This growth is driven by the need for reliable and scalable energy solutions, particularly in remote and off-grid locations. Countries like France and Italy lead adoption, with companies. Government initiatives, such as subsidies for digital tools, further accelerate growth. These factors position prime power as a key growth driver, outpacing traditional applications in the coming years.

REGIONAL ANALYSIS

Germany led the European stationary fuel cell market, commanding a 25.4% share in 2024. Its dominance stems from a robust manufacturing base and advanced logistics networks. The country’s GDP per capita is great, enabling higher investments in automation. Additionally, Germany’s strategic location facilitates cross-border trade, with a significant portion of shipments originating or transiting through the country.

France exhibits the highest growth rate, with a CAGR of 16.3%. Urbanization and government initiatives, such as subsidies for green data centers, drive demand for advanced warehousing solutions. Paris alone accounts for a major share of France’s market activities, supported by government subsidies for eco-friendly equipment.

Italy and Spain show moderate growth, driven by industrial modernization. The UK faces challenges post-Brexit but remains competitive in smart warehousing solutions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Bloom Energy, Cummins, Fuji Electric Europe, FuelCell Energy, AFC Energy, Ballard Power Systems, Nuvera Fuel Cells, Plug Power, SFC Energy, Siemens Energy, and Toshiba Energy Systems and Solutions Corporation are playing dominating role in Europe stationary fuel cell market.

Competition in the European stationary fuel cell market is intense, with established players vying for dominance through innovation and specialization. Bloom Energy leads with its comprehensive product portfolio, while Siemens focuses on sustainability and digital transformation. Plug Power differentiates itself with expertise in hydrogen fuel cell technology, catering to the growing demand from energy and manufacturing sectors.

Price wars and technological advancements further intensify rivalry. Smaller players leverage niche offerings to compete with larger players. Regulatory compliance and data privacy remain key battlegrounds, shaping the future of the market.

TOP PLAYERS IN THIS MARKET

Bloom Energy

Bloom Energy is a global leader in stationary fuel cell solutions, commanding a notable market share in Europe. Its innovative product portfolio includes hydrogen-based systems tailored for industries like manufacturing and utilities.

Siemens Energy

Siemens specializes in energy-efficient solutions, capturing a considerable market share. Its focus on sustainability includes adopting IoT-enabled systems, aligning with the EU Green Deal.

Plug Power

Plug Power excels in hydrogen fuel cell technology, holding a key share. Its partnerships with tech firms ensure seamless integration of AI-driven analytics, enhancing operational efficiency.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players employ strategies like digital transformation and localization. Companies invest in AI-driven analytics to personalize learning experiences. Pearson partners with tech firms to develop adaptive platforms, ensuring scalability.

Localization is another focus area, with Coursera offering multilingual content to cater to diverse audiences. Collaborations with governments secure subsidies for digital tools, accelerating adoption. Mergers and acquisitions also play a pivotal role, with Duolingo acquiring niche providers to expand its capabilities.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, Bloom Energy launched a hydrogen-based fuel cell system, enhancing energy efficiency for industrial facilities across Europe.

- In June 2023, Siemens introduced IoT-enabled predictive maintenance tools, reducing downtime by 25% for clients in France and Spain.

- In March 2023, Plug Power acquired a niche provider, strengthening its AI-driven analytics capabilities and expanding its footprint in the telecommunications sector.

- In July 2023, Microsoft partnered with Cisco to develop IoT-enabled fuel cell platforms, improving energy exchange and operational efficiency for clients in the BFSI industry.

- In February 2024, Enel expanded its fuel cell offerings in Spain, increasing adoption rates by 15%.

MARKET SEGMENTATION

This research report on the Europe stationary fuel cell market is segmented and sub-segmented into the following categories.

By Capacity

- 3 kW

- 3 kW – 10 kW

- 10 kW – 50 kW

- > 50 kW

By End Use

- Residential

- Commercial

- Industry/Utility

By Application

- Prime Power

- CHP

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the projected market size of the Europe Stationary Fuel Cell industry by 2033?

The market is estimated to reach USD 394.64 million by 2033, growing at a CAGR of 8.56% from 2025 to 2033

2. What factors are driving the growth of the stationary fuel cell market in Europe?

Key drivers include government incentives like subsidies and grants, policies promoting renewable energy and reducing greenhouse gas emissions, advancements in hydrogen infrastructure, and the increasing demand for decentralized and clean power generation solutions

3. What challenges does the stationary fuel cell market face?

High upfront costs for fuel cell systems and supporting infrastructure, limited hydrogen production and distribution networks, and financial barriers such as expensive refueling stations pose significant challenges

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]