Europe Sporting Goods Market Size, Share, Trends & Growth Forecast Report By Product Type (Football, Team Sports, Tennis, Bike Sports, Racket Sports, Outdoor Sports, Fitness, Running, Water Sports, Winter Sports, Golf, Other Sports) and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2025 to 2033.

Europe Sporting Goods Market Size

The sporting goods market size in Europe was valued at USD 176 billion in 2024. The European market is estimated to be worth USD 324.14 billion by 2033 from USD 188.65 billion in 2025, growing at a CAGR of 7% from 2025 to 2033.

Sporting goods are products such as athletic footwear, apparel, equipment, and accessories designed for sports, fitness, and outdoor activities. These products cater to a diverse range of consumers, from professional athletes to casual fitness enthusiasts, reflecting the growing emphasis on health, wellness, and active lifestyles. The rising participation in sports, gym memberships, and outdoor recreational activities are fuelling the demand for sporting goods in Europe. Germany, France, and the United Kingdom are the largest contributors, collectively accounting for over 60% of total sales. The UK Office for National Statistics highlights that the athleisure trend has significantly boosted demand for sportswear, with athletic apparel and footwear seeing a 15% annual growth rate since 2020. Additionally, Italy’s Ministry of Economic Development notes that Europe’s leadership in manufacturing high-quality sporting goods, particularly in cycling and winter sports equipment, positions it as a global hub for innovation and exports. The European Commission emphasizes that sustainability is becoming a key focus, with 40% of consumers now prioritizing eco-friendly materials like recycled polyester and biodegradable fabrics. As urbanization, health consciousness, and digital fitness platforms continue to rise, the European sporting goods market is poised for sustained expansion, blending functionality, style, and environmental responsibility to meet modern consumer needs.

MARKET DRIVERS

Rising Health Consciousness and Active Lifestyles

A key driver of the European sporting goods market is the growing emphasis on health and fitness, fueled by increased awareness of preventive healthcare. Eurostat reports that over 60% of Europeans now engage in regular physical activities, such as jogging, cycling, and gym workouts, boosting demand for athletic footwear, apparel, and equipment. The UK Office for National Statistics highlights that gym memberships have risen by 20% since 2020, particularly among millennials and Gen Z, who prioritize active lifestyles. Additionally, Germany’s Federal Ministry of Health notes that government campaigns promoting physical activity have further accelerated this trend, with sports participation rates increasing by 15% in urban areas. This shift toward healthier living has created a robust market for performance-driven products, ensuring steady growth. As consumers increasingly view sports and fitness as integral to their well-being, the sporting goods market continues to expand, driven by innovation and functionality.

Athleisure Trend and Fashion Integration

Another significant driver is the athleisure trend, which has blurred the lines between sportswear and casual fashion, appealing to a broader demographic. The UK Office for National Statistics reports that athleisure sales account for 35% of total sporting goods revenue, with athletic apparel and footwear seeing a 15% annual growth rate. Italy’s Ministry of Economic Development highlights that luxury brands like Gucci and Prada have entered the athleisure space, blending style with functionality to attract affluent consumers. Furthermore, Eurostat notes that 45% of urban professionals now incorporate sportswear into their daily wardrobes, reflecting its versatility. The rise of remote work and flexible lifestyles has further amplified this trend. By combining comfort, aesthetics, and performance, athleisure has redefined consumer preferences, driving sustained demand and innovation in the European sporting goods market.

MARKET RESTRAINTS

High Costs of Premium Sporting Goods

A significant restraint in the European sporting goods market is the high cost of premium products, which limits accessibility for price-sensitive consumers. Eurostat reports that high-end athletic footwear and equipment are priced 30-50% higher than standard alternatives, making them unaffordable for low-income households. The UK Office for National Statistics highlights that only 25% of consumers in Eastern Europe purchase premium sporting goods, compared to over 60% in affluent regions like Germany and France. Additionally, Italy’s Ministry of Economic Development notes that small and medium-sized enterprises (SMEs) struggle to compete with global giants like Nike and Adidas, which dominate the premium segment. While these products offer superior quality and performance, their affordability remains a concern, particularly in economically disadvantaged areas. This financial barrier restricts market penetration, hindering broader adoption and growth potential among diverse demographics.

Environmental Concerns Over Material Usage

Another major restraint is the growing scrutiny over the environmental impact of materials used in sporting goods production. The European Environment Agency states that traditional materials like synthetic fibers and non-recyclable plastics contribute significantly to pollution, with less than 10% of sporting goods currently made from sustainable materials. France’s Ministry of Ecology highlights that regulatory pressures under the EU Circular Economy Action Plan are pushing manufacturers to adopt eco-friendly practices, but compliance increases production costs by up to 25%. Furthermore, Eurostat reports that only 30% of consumers actively seek out sustainable sporting goods, reflecting a gap between awareness and action. As environmental concerns mount, balancing affordability, sustainability, and regulatory compliance remains a critical challenge, impacting both production strategies and consumer adoption rates in the sporting goods market.

MARKET OPPORTUNITIES

Growing Demand for Sustainable and Eco-Friendly Products

A significant opportunity in the European sporting goods market lies in the rising demand for sustainable products, driven by increasing environmental awareness. The European Environment Agency reports that 45% of consumers now prioritize eco-friendly sporting goods, such as those made from recycled polyester or biodegradable materials. Italy’s Ministry of Economic Development highlights that brands incorporating sustainability into their designs have seen a 20% increase in sales among environmentally conscious buyers. Additionally, Eurostat notes that outdoor and fitness equipment made from recycled materials accounts for 15% of total sales, with projections of further growth under the EU Circular Economy Action Plan. The UK Office for National Statistics emphasizes that younger demographics, particularly Gen Z, are willing to pay a premium for sustainable options. By aligning with consumer values and regulatory standards, manufacturers can tap into this lucrative trend, fostering innovation while enhancing brand loyalty and market share.

Expansion of Digital Fitness and Smart Equipment

Another key opportunity is the integration of digital fitness solutions and smart sporting goods, fueled by advancements in technology and the rise of home workouts. Eurostat reports that smart fitness equipment, such as connected treadmills and wearable devices, has grown by 25% annually since 2020, driven by the popularity of apps like Strava and Peloton. Germany’s Federal Ministry of Health highlights that over 50% of urban consumers aged 18-35 own wearable fitness trackers, boosting demand for compatible gear. Additionally, the UK Office for National Statistics notes that subscription-based models for digital fitness platforms have gained traction, ensuring recurring revenue streams. As digital adoption accelerates, combining IoT-enabled equipment with personalized fitness experiences offers a competitive edge, driving innovation and long-term growth in the European sporting goods market.

MARKET CHALLENGES

Intense Competition and Market Saturation

A significant challenge in the European sporting goods market is the intense competition and market saturation, driven by an influx of global brands and low-cost imports. Eurostat reports that over 40% of sporting goods sold in Europe are imported from Asia, where production costs are significantly lower, pressuring local manufacturers to reduce prices. The UK Office for National Statistics highlights that small and medium-sized enterprises (SMEs) face a 15% decline in profit margins due to this competitive pricing environment. Additionally, Germany’s Federal Ministry of Economic Affairs notes that consumers in price-sensitive regions, such as Eastern Europe, prioritize affordability over quality, intensifying competition. This price-driven environment stifles innovation and limits investments in sustainable practices, making it challenging for brands to differentiate themselves while maintaining profitability in an increasingly crowded market.

Balancing Innovation with Affordability

Another major challenge is balancing innovation with affordability, particularly as consumer expectations rise alongside economic uncertainties. The European Environment Agency states that while 60% of consumers demand advanced features like smart technology and eco-friendly materials, only 30% are willing to pay a premium for these innovations. France’s Ministry of Economy highlights that incorporating cutting-edge technologies, such as IoT-enabled equipment, increases production costs by up to 35%, deterring budget-conscious buyers. Furthermore, Eurostat reports that less than 20% of rural consumers adopt high-tech sporting goods due to limited awareness and higher costs. As manufacturers strive to meet evolving preferences, addressing affordability without compromising quality or innovation remains a critical hurdle, impacting both market accessibility and long-term growth potential in the sporting goods industry.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product Type and Country. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe. |

|

Market Leader Profiled |

Adidas AG, Nike, Inc., Under Armour, Inc., PUMA SE, Amer Sports, Odlo, Hammer Sports, Polar Electro, KETTLER, WaterRower, and Others |

SEGMENTAL ANALYSIS

By Product Type Insights

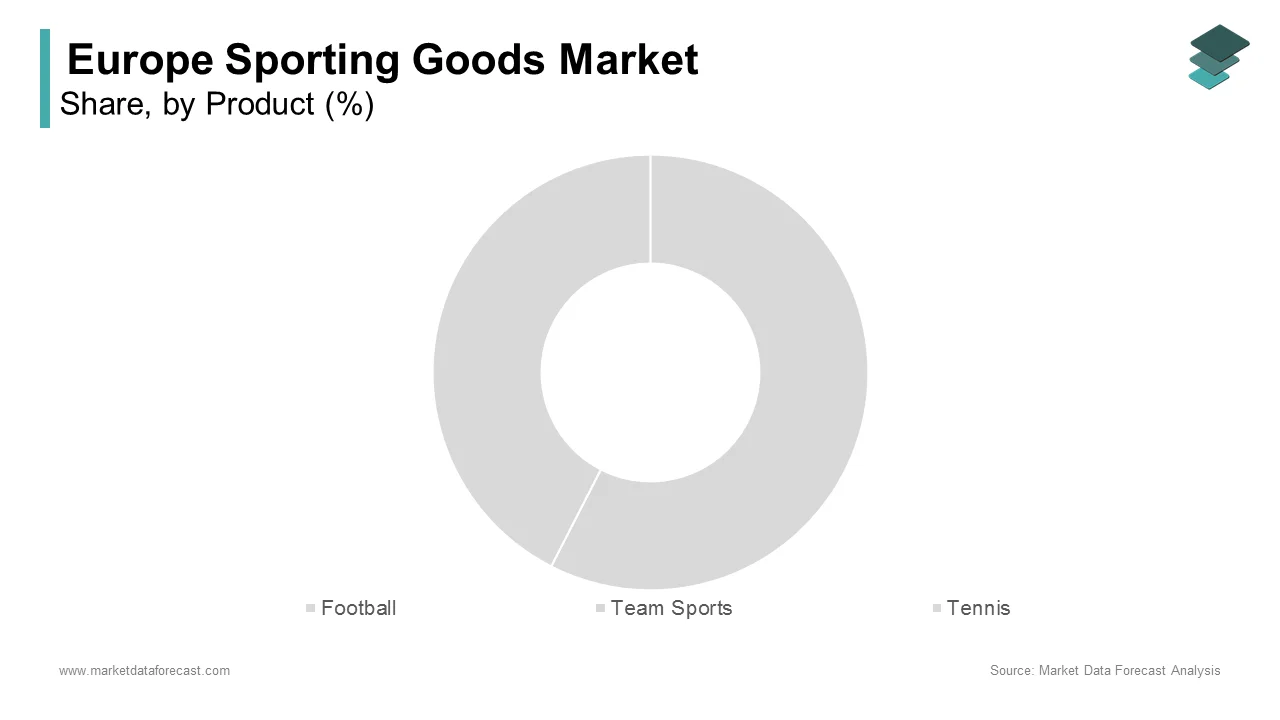

The football segment held 25.8% of the European market share in 2024. The unparalleled popularity of football in Europe is majorly propelling the domination of football segment in the European sporting goods market. According to the Federal Ministry of Sports of Germany, over 60% of Europeans engage with the sport. The UK Office for National Statistics notes that countries like England and Spain drive demand for boots, balls, and training gear due to their globally recognized leagues. Grassroots programs and school initiatives further boost participation rates. As clubs and fans invest heavily in high-quality equipment, football remains integral to the market, ensuring consistent demand while fostering innovation in design and functionality, making it a cornerstone of the sporting goods industry.

On the other hand, the fitness segment is predicted to showcase a promising CAGR of 10.1% during the forecast period owing to the rising health consciousness and digital fitness trends. The UK Office for National Statistics reports that 45% of urban consumers aged 18-35 prioritize fitness activities, driving demand for gym equipment and wearables. Italy’s Ministry of Health highlights that smart fitness devices, such as connected treadmills, have grown by 25% annually. Additionally, home workout trends and subscription-based platforms ensure recurring revenue streams. By combining technology, convenience, and health-focused solutions, the fitness segment addresses evolving consumer preferences, reshaping active lifestyles and driving long-term growth in the sporting goods market.

REGIONAL ANALYSIS

Germany was the largest regional segment for sporting goods in Europe and held 22.7% of the European market share in 2024. The growth of the German market is driven by high sports participation rates, with Germany’s Federal Ministry of Sports highlighting that over 70% of Germans engage in regular physical activities. The country’s robust manufacturing sector and focus on quality have positioned it as a global leader in producing premium sporting goods, particularly for football and winter sports. Additionally, the UK Office for National Statistics notes that Germany’s emphasis on sustainability aligns with consumer preferences, with eco-friendly products accounting for 30% of sales. Urban centers like Munich and Berlin also foster fitness trends, boosting demand for gym equipment and activewear. By combining innovation, accessibility, and environmental responsibility, Germany remains pivotal to the market’s growth.

The United Kingdom market is another lucrative market for sporting goods in Europe and is anticipated to expand at a CAGR of 9.1% over the forecast period due to its strong football culture and rising fitness consciousness, as per the UK Office for National Statistics. England’s Premier League drives significant demand for football-related goods, while grassroots initiatives amplify participation. Additionally, Eurostat reports that the athleisure trend has boosted sportswear sales, with athletic apparel growing by 15% annually among urban professionals. The European Commission highlights that digital fitness platforms have further accelerated growth, particularly in cities like London. Furthermore, the UK’s diverse sporting landscape, including cycling and running, ensures steady demand across product categories. By leveraging its cultural affinity for sports and embracing modern fitness trends, the UK continues to shape the European sporting goods market.

Italy is projected to grow at a CAGR of 7.12% during the forecast period owing to its reputation for design excellence and outdoor sports enthusiasm, according to Italy’s Ministry of Economic Development. Italian manufacturers excel in producing high-quality cycling and winter sports equipment, catering to both domestic and international markets. Eurostat highlights that Italy’s mountainous regions drive demand for skiing gear, while coastal areas boost water sports products. Additionally, the UK Office for National Statistics notes that Italy’s focus on sustainable materials, such as recycled polyester, appeals to environmentally conscious consumers. The country’s Mediterranean climate fosters outdoor activities, further propelling demand. By blending craftsmanship, innovation, and regional diversity, Italy maintains a strong foothold in the European sporting goods market while influencing global trends.

KEY MARKET PLAYERS

Some notable companies that dominate the Europe sporting goods market profiled in this report are Adidas AG, Nike, Inc., Under Armour, Inc., PUMA SE, Amer Sports, Odlo, Hammer Sports, Polar Electro, KETTLER, WaterRower, and Others.

MARKET SEGMENTATION

This Europe sporting goods market research report is segmented and sub-segmented into the following categories.

By Product Type

- Football

- Team Sports

- Tennis

- Bike Sports

- Racket Sports

- Outdoor Sports

- Fitness

- Running

- Water Sports

- Winter Sports

- Golf

- Other Sports

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the expected growth of the Europe sporting goods market?

The Europe sporting goods market is forecasted to grow from USD 188.65 billion in 2025 to USD 324.14 billion by 2033, at a CAGR of 7%.

2. What are the key drivers of growth in this market?

Rising health consciousness, the athleisure trend, and increasing participation in sports and fitness activities.

3. What are the challenges faced by the industry?

High costs of premium products and environmental concerns regarding material sustainability.

4. What opportunities exist in the Europe sporting goods market?

Demand for eco-friendly products and the integration of smart, digital fitness solutions.

5. How does the athleisure trend impact the Europe sporting goods market?

Athleisure, blending sportswear with casual fashion, has led to increased sales of athletic apparel and footwear.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]