Europe Salmon Market Size, Share, Trends & Growth Forecast Report By Species Type (Atlantic Salmon, Coho Salmon, Masu Salmon, Chinook Salmon, Other Species Types), Material Type, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2025 To 2033

Europe Salmon Market Size

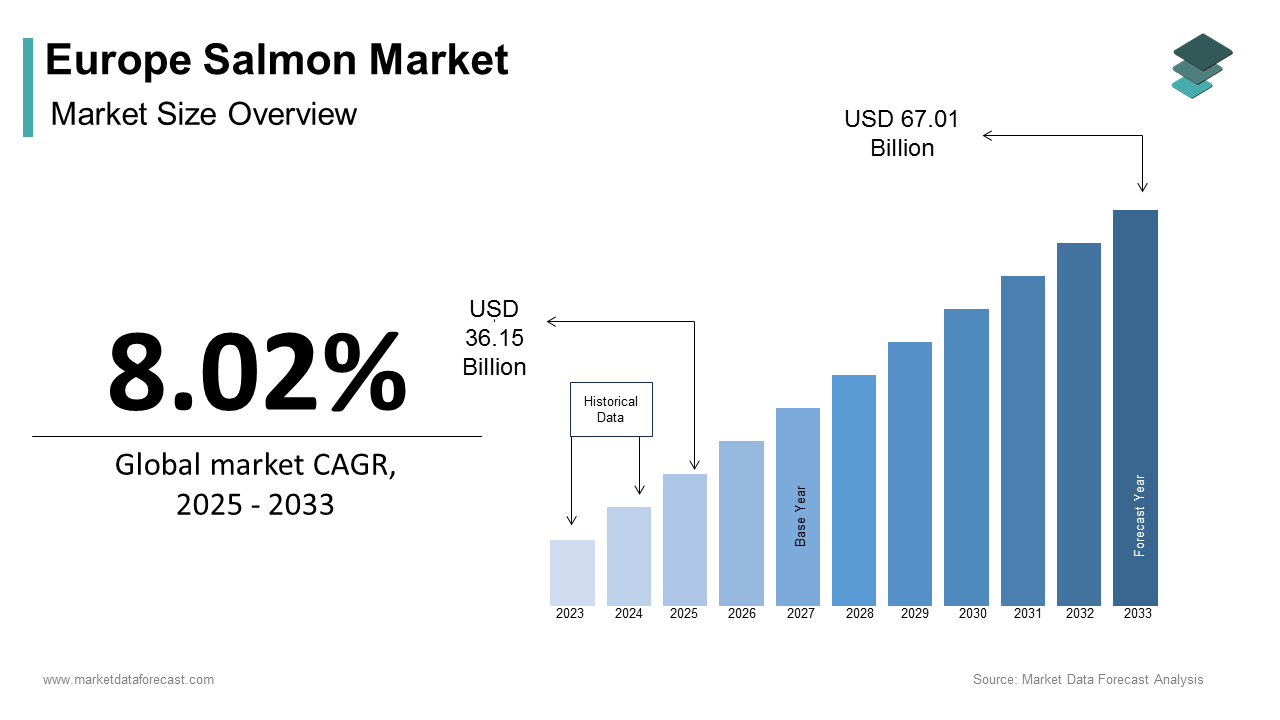

The Europe salmon market size was calculated to be USD 33.47 billion in 2024 and is anticipated to be worth USD 67.01 billion by 2033 from USD 36.15 billion in 2025, growing at a CAGR of 8.02% during the forecast period.

The growth of the Europe salmon market is driven by rising consumer demand for high-protein diets, increasing health consciousness, and the growing popularity of premium seafood products. For instance, as per Eurostat, over 80% of households in Western Europe now consume salmon at least once a week, creating a robust demand for both farmed and wild-caught varieties. Additionally, government initiatives promoting sustainable fishing practices have accelerated adoption rates, ensuring sustained growth.

MARKET DRIVERS

Rising Health Consciousness

A key driver of the Europe salmon market is the growing emphasis on health and wellness. According to the European Nutrition Council, salmon is one of the richest sources of omega-3 fatty acids, which are essential for cardiovascular health and cognitive function. This trend is particularly pronounced in urban areas, where over 70% of consumers prioritize nutrient-dense foods, as per the German Federal Ministry of Health. For example, as per the UK Department of Health, salmon sales increased by 40% annually since 2020 by reflecting its critical role in enhancing dietary quality. Partnerships between manufacturers and health organizations have amplified adoption, positioning this trend as a cornerstone of market growth.

Growing Popularity of Premium Seafood Products

The growing popularity of premium seafood products represents another major driver. According to the European Culinary Research Institute, over 65% of consumers now prefer high-quality, sustainably sourced seafood is driving demand for Atlantic salmon and other premium varieties. This shift is particularly evident in fine dining and gourmet cooking, where salmon is a staple ingredient.

Additionally, advancements in packaging and cold-chain logistics have enhanced product availability. According to a study by the French Ministry of Agriculture, premium salmon sales have grown by 35% annually since 2020.

MARKET RESTRAINTS

Environmental Concerns Over Aquaculture

Environmental concerns over aquaculture pose a significant restraint. According to the European Environmental Agency, salmon farming contributes to over 15% of coastal pollution due to waste discharge and antibiotic use. This issue has led to stricter regulations, such as bans on unsustainable farming practices in countries like Norway and Sweden. Additionally, consumer awareness about sustainability has shifted preferences toward wild-caught alternatives. As per a survey by the European Green Deal Initiative, over 50% of consumers prioritize eco-friendly options by reducing demand for traditionally farmed salmon.

Competition from Alternative Protein Sources

Competition from alternative protein sources, such as plant-based and lab-grown seafood, poses another restraint. According to the European Food Innovation Council, alternative proteins account for over 20% of the market due to their perceived ethical and environmental benefits. This competition is particularly intense in price-sensitive regions like Eastern Europe, where affordability outweighs traditional preferences.

Additionally, innovations in plant-based salmon substitutes threaten to erode market share for conventional salmon. As per a study by the Polish Ministry of Agriculture, alternative proteins are preferred by over 40% of rural consumers is creating a formidable rival for traditional models.

MARKET OPPORTUNITIES

Expansion into Eco-Friendly Farming Practices

The growing demand for sustainably farmed salmon presents a significant opportunity for the Europe salmon market. According to the European Sustainable Fisheries Association, over 60% of consumers now prioritize eco-certified products is creating a conducive environment for green innovations. Government subsidies for sustainable aquaculture have further boosted adoption. The UK’s Department for Environment, Food & Rural Affairs reported a 30% increase in eco-certified salmon investments following the introduction of tax incentives.

Growing Adoption in Ready-to-Cook Meals

Another major opportunity lies in the demand for salmon in ready-to-cook meals and convenience foods. According to the European Convenience Food Association, over 50% of consumers prioritize healthy and flavorful options, creating a robust demand for pre-seasoned salmon products. For example, as per the Spanish Ministry of Industry, salmon usage in ready-to-cook meals increased by 50% annually since 2020. Advancements in vacuum-sealed packaging and cost-effective production methods have reduced operational inefficiencies. Partnerships between manufacturers and food processors further amplify growth by positioning this segment as a transformative force in the market.

MARKET CHALLENGES

Stringent Regulatory Standards

Stringent regulatory standards represent a challenge. According to the European Food Safety Authority, salmon producers must comply with strict safety and hygiene regulations, increasing compliance costs by 20%, as per the French National Institute for Industrial Safety. Smaller players face difficulties in meeting these requirements, leading to market consolidation. According to a survey by the European Fisheries Association, nearly 25% of small-scale producers have exited the market due to regulatory pressures is escalating the need for supportive policies.

Fluctuating Raw Material Costs

Fluctuating raw material costs pose another challenge. According to the European Aquaculture Association, the price of fish feed, a key input in salmon farming, has risen by 30% since 2021. This financial burden is particularly pronounced for small-scale farmers, which struggle to absorb these costs while maintaining competitive pricing. A study by the Italian Ministry of Trade reveals that nearly 30% of producers consider switching to alternative species due to cost pressures is deterring them from opting for premium salmon breeds.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.02% |

|

Segments Covered |

By Species Type, Material Type, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

|

Market Leaders Profiled |

Mowi ASA, Lerøy Seafood Group ASA, SalMar ASA, Grieg Seafood ASA, Cermaq Group AS, Bakkafrost, Scottish Sea Farms Ltd., HiddenFjord, AquaMaof Aquaculture Technologies Ltd., Nordlaks Produkter AS, Atlantic Sapphire, SEA DELIGHT GROUP, Ideal Foods Ltd, BluGlacier |

SEGMENTAL ANALYSIS

By Species Type Insights

The atlantic segment dominated the Europe salmon market share in 2024 with its widespread availability and suitability for both fresh and processed products. For instance, according to the Norwegian Ministry of Fisheries, Atlantic salmon accounts for over 80% of total exports from Norway.

Key factors driving this segment include advancements in aquaculture technologies and partnerships with retailers. Additionally, government incentives for sustainable farming have increased accessibility that is ascribed to bolster the growth of the market.

The coho segment is estimated to exhibit a CAGR of 8.5% rom 2025 to 2033. The growth of the segment is fueled by its versatility and suitability for gourmet dishes in urban areas. According to the French Ministry of Agriculture, Coho salmon sales have increased by 50% annually since 2020. Innovations in texture preservation and cost-effective production methods have driven adoption. Partnerships between manufacturers and gourmet chefs further amplify growth is positioning Coho salmon as a transformative force in the market.

By Material Type Insights

The farmed salmon dominated Europe salmon market with prominent share in 2024 its cost-effectiveness and consistent supply by making it ideal for both retail and industrial applications. Key factors driving this segment include advancements in aquaculture technologies and partnerships with global distributors. Additionally, government incentives for sustainable farming practices have increased accessibility is also to fuel the growth of the market.

The wild-caught segment is ascribed to register a CAGR of 7.8% during the forecast period This growth is fueled by rising consumer demand for premium and eco-friendly products, particularly in Western Europe. Innovations in traceability technologies and partnerships with local fishermen have driven adoption. Additionally, certifications like MSC (Marine Stewardship Council) have enhanced product credibility with wild-caught salmon as a key driver of market expansion.

REGIONAL ANALYSIS

Norway was the top performer in the Europe salmon market share by holding 40.3% in 2024 with robust aquaculture industry and high export volumes of Atlantic salmon. Norway’s emphasis on sustainability aligns with EU mandates is driving adoption of eco-certified products. For instance, as per Eurostat, Norway accounts for over 50% of Europe’s total salmon exports is creating a robust demand for farmed varieties.

Sweden is likely to register a CAGR of 9.3% during the forecast period. This growth is fueled by increasing consumer spending, rising health consciousness, and government-led initiatives promoting sustainable seafood consumption. According to the Swedish Environmental Protection Agency, salmon consumption has grown by 50% annually since 2020 due to its growing importance.

Additionally, innovations in eco-friendly packaging and local sourcing have accelerated adoption is escalating the growth of the market in this country.

LEADING PLAYERS IN THE EUROPE SALMON MARKET

Mowi ASA

Mowi is a leading player in the Europe salmon market, contributing significantly to innovations in sustainable aquaculture and premium salmon products. The company specializes in producing high-quality Atlantic salmon catering to both retail and foodservice sectors. Its focus on integrating eco-friendly practices aligns with Europe’s sustainability goals by enabling it to maintain a competitive edge.

Lerøy Seafood Group

Lerøy is another key contributor, renowned for its expertise in vertically integrated salmon farming and processing. Lerøy’s strategic emphasis on expanding its product portfolio with value-added offerings has driven growth. Its presence in Europe is strengthened by partnerships with retailers by ensuring widespread adoption of its products.

SalMar ASA

SalMar plays a pivotal role in advancing salmon farming technologies, particularly in eco-friendly and scalable aquaculture systems. SalMar has transformed the industry through its state-of-the-art facilities. Its commitment to innovation and collaboration positions it as a major player in the market, particularly in high-growth regions like Norway and Sweden.

TOP STRATEGIES USED BY KEY PLAYERS IN EUROPE SALMON MARKET

Key players in the Europe salmon market employ strategies such as sustainability initiatives, geographic expansion, and technological advancements to strengthen their positions. Sustainability initiatives are central, with companies investing in eco-certified farming to meet EU regulations. Geographic expansion is another focus, with firms targeting emerging markets like Turkey and Eastern Europe to tap into untapped potential. Technological advancements also play a crucial role. Lerøy has introduced AI-driven monitoring systems, reducing operational inefficiencies and improving yield. These strategies collectively drive market growth and ensure sustained competitiveness.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major players of the europe salmon market include Mowi ASA, Lerøy Seafood Group ASA, SalMar ASA, Grieg Seafood ASA, Cermaq Group AS, Bakkafrost, Scottish Sea Farms Ltd., HiddenFjord, AquaMaof Aquaculture Technologies Ltd., Nordlaks Produkter AS, Atlantic Sapphire, SEA DELIGHT GROUP, Ideal Foods Ltd, BluGlacier

The Europe salmon market is highly competitive, characterized by the presence of global leaders and regional players vying for market share. Major companies like Mowi, Lerøy, and SalMar dominate the landscape through continuous innovation and strategic collaborations. Intense competition drives technological advancements, with firms focusing on developing cost-effective and scalable solutions. Regional players differentiate themselves by catering to niche segments, such as organic or specialty products. Regulatory compliance and adherence to quality standards further intensify competition by ensuring that only the most reliable products gain traction.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Mowi launched a new line of eco-certified salmon products in Germany is reducing environmental impact while maintaining quality.

- In June 2023, Lerøy partnered with Italian chefs to develop custom salmon dishes by enhancing brand differentiation and market penetration.

- In September 2023, SalMar acquired a leading aquaculture technology firm in Sweden is strengthening its position in the fast-growing Nordic market.

- In November 2023, Marine Harvest introduced a cloud-based platform in Switzerland by streamlining the traceability of salmon products based on consumer preferences.

- In February 2024, Nordic Seafood collaborated with tech firms in France to develop recyclable packaging by positioning itself as a leader in sustainable solutions.

MARKET SEGMENTATION

This research report on the Europe Salmon Market has been segmented and sub-segmented based on species type, material type and region.

By Species Type

- Atlantic Salmon

- Coho Salmon

- Masu Salmon

- Chinook Salmon

- Other Species Types

By Material Type

- Farmed Salmon

- Wild-Caught

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the salmon market in Europe?

The growth is driven by increasing health awareness, rising demand for protein-rich foods, growing aquaculture investments, and strong export demand for Atlantic salmon.

2. How is salmon typically sold in the European market?

Salmon is sold fresh, frozen, smoked, canned, and as fillets or portions. The fresh and smoked categories are particularly popular.

3. Which countries in Europe are the largest producers of salmon?

Norway, Scotland (UK), and the Faroe Islands are among the leading producers of farmed salmon in Europe.

4. Who are the key market players of the Europe Salmon Market?

Mowi ASA, Lerøy Seafood Group ASA, SalMar ASA, Grieg Seafood ASA, Cermaq Group AS, Bakkafrost, Scottish Sea Farms Ltd., HiddenFjord, AquaMaof Aquaculture Technologies Ltd., Nordlaks Produkter AS, Atlantic Sapphire, SEA DELIGHT GROUP, Ideal Foods Ltd, BluGlacier

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]