Europe Renewable Energy Market Size, Share, Trends & Growth Forecast Report By Type (Wind Energy, Solar Energy), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2025 To 2033

Europe Renewable Energy Market Size

The Europe Renewable Energy Market size was calculated to be USD 142.52 billion in 2024 and is anticipated to be worth USD 245.95 billion by 2033 from USD 151.43 billion in 2025, growing at a CAGR of 6.25% during the forecast period.

The European renewable energy market has emerged as a cornerstone of the continent's transition towards sustainable development. As per the International Renewable Energy Agency, Europe accounted for nearly 30% of global renewable energy capacity additions in the past decade showcasing its influence in clean energy adoption. The region's commitment is further underscored by ambitious targets set under the European Green Deal, which aims for carbon neutrality by 2050. According to Eurostat, renewables contributed over 22% of the EU's gross final energy consumption in 2022 reflecting steady progress amidst geopolitical and economic challenges.

Germany, Spain, and France remain frontrunners in deploying wind and solar technologies, driven by supportive policies and declining installation costs. As per the Fraunhofer Institute, Germany alone installed over 7 gigawatts of solar capacity in 2022. Meanwhile, offshore wind projects in the North Sea have gained momentum, with the UK leading in operational capacity. However, supply chain disruptions and regulatory hurdles continue to pose risks. The Wood Mackenzie notes that permitting delays slowed project completions by approximately 15% across key markets last year. Despite these obstacles, investor confidence remains robust, fueled by corporate power purchase agreements and green financing initiatives.

MARKET DRIVERS

Regulatory Frameworks and Policy Commitments

The European renewable energy market is significantly propelled by stringent regulatory frameworks and bold policy commitments. The European Union's Renewable Energy Directive sets a binding target of achieving at least 42.5% of energy from renewable sources by 2030, as per the European Commission. This legislative push has catalyzed investments in clean energy technologies across member states. For instance, countries like Germany and France have introduced feed-in tariffs and tax incentives to encourage solar and wind energy adoption. According to the International Energy Agency, Europe’s renewable capacity additions surged by 39 gigawatts in 2022 driven largely by such policies. Furthermore, the REPowerEU plan, aimed at reducing dependence on fossil fuels, has earmarked €210 billion for renewable projects by 2027. This financial commitment underscores how regulatory initiatives are transforming demand dynamics. Additionally, national strategies, such as Spain’s goal to install 60 gigawatts of renewable capacity by 2030, reflect localized ambitions that collectively bolster regional growth. These measures not only ensure compliance with international climate goals but also create a stable environment for long-term investments, fostering confidence among stakeholders.

Economic Competitiveness of Renewables

The declining cost of renewable energy technologies is another critical driver shaping the European market. As indicated by BloombergNEF, the levelized cost of electricity (LCOE) for onshore wind fell notably between 2010 and 2022, while solar photovoltaic costs dropped substantially. These reductions have made renewables the cheapest source of new power generation in many regions. For example, in 2022, the Fraunhofer Institute reported that utility-scale solar projects in southern Europe achieved LCOEs as low as €30 per megawatt-hour, outcompeting coal and gas. This economic advantage has spurred private sector participation, with corporations signing over 10 gigawatts of power purchase agreements (PPAs) in Europe during 2022, as per the International Renewable Energy Agency. Moreover, rising carbon prices under the EU Emissions Trading System, which exceeded €100 per ton in 2023, have further incentivized businesses to transition to cleaner energy sources. This dual impact of affordability and regulatory pressure ensures that renewables remain a dominant force in meeting Europe’s growing energy needs while driving decarbonization efforts forward.

MARKET RESTRAINTS

Grid Infrastructure Limitations and Bottlenecks

A major restraint hindering the European renewable energy market is the inadequacy of grid infrastructure to accommodate the rapid expansion of clean energy projects. According to ENTSO-E, the European Network of Transmission System Operators for Electricity, over 70% of renewable energy projects face delays due to grid connection issues, with some regions reporting lead times exceeding five years. This bottleneck is caused by the outdated transmission networks that were not designed to handle decentralized and intermittent energy sources like wind and solar. For instance, offshore wind farms in the North Sea often require extensive upgrades to connect to mainland grids, a process that can cost billions of euros and take several years. Apart from these, cross-border interconnections remain underdeveloped, limiting the ability to balance supply and demand across regions. As per the International Energy Agency, only 4% of Europe’s total electricity demand can currently be met through cross-border trade, creating inefficiencies in resource allocation. These structural limitations not only increase project costs but also deter investors who seek faster returns on their investments, thereby slowing down the pace of renewable energy deployment.

Supply Chain Disruptions and Material Shortages

Supply chain vulnerabilities have emerged as another critical restraint affecting the European renewable energy market. The global semiconductor shortage and rising demand for rare earth elements, such as neodymium used in wind turbines, have significantly impacted production timelines. The Wood Mackenzie notes that the cost of key materials like polysilicon for solar panels surged by nearly 300% between 2020 and 2022, causing delays in large-scale installations. Furthermore, geopolitical tensions, particularly Europe's reliance on Chinese imports for critical components exacerbate these challenges. A report by the Fraunhofer Institute stresses that over 80% of solar modules installed in Europe are imported making the market susceptible to price volatility and trade restrictions. Labor shortages also compound these issues, with skilled technicians required for installation and maintenance being in short supply. For example, WindEurope estimates that the industry requires an additional 50,000 trained workers by 2030 to meet projected growth targets. These factors collectively strain the market’s ability to scale renewable energy adoption at the desired pace.

MARKET OPPORTUNITIES

Corporate Demand for Renewable Energy and PPAs

The burgeoning demand for renewable energy from corporations presents a significant growth avenue for Europe’s clean energy market. Based on the findings by the BloombergNEF, corporate power purchase agreements (PPAs) in Europe reached a record 10.4 gigawatts in 2022 supported by companies seeking to meet sustainability targets and hedge against volatile fossil fuel prices. Industries such as technology, manufacturing, and retail are increasingly committing to net-zero goals, with tech giants like Google and Microsoft leading the charge by signing large-scale PPAs. For instance, Amazon became Europe’s largest corporate buyer of renewable energy in 2022 securing over 3 gigawatts of capacity across the region. This trend is further supported by initiatives like the RE100, a global coalition of companies committed to 100% renewable electricity, which includes over 400 members operating in Europe. As per the International Renewable Energy Agency, corporate procurement could account for 20% of Europe’s total renewable energy capacity additions by 2030. This growing appetite for clean energy not only creates new revenue streams for developers but also fosters innovation in energy trading platforms and financial instruments tailored to corporate buyers.

Green Hydrogen and Decarbonization of Hard-to-Abate Sectors

Green hydrogen represents a transformative opportunity for Europe’s renewable energy market, particularly in decarbonizing sectors like steel, chemicals, and heavy transport. The European Commission estimates that green hydrogen could meet up to 24% of the EU’s energy demand by 2050 requiring investments of €470 billion by 2030. According to Wood Mackenzie, Europe making up 60% of global green hydrogen project announcements in 2022 reflecting its command in this emerging sector. Also, Germany alone has earmarked €9 billion for hydrogen infrastructure under its National Hydrogen Strategy. Pilot projects such as the HyDeal Ambition initiative aim to produce green hydrogen at €1.5 per kilogram by 2030, making it competitive with fossil-based alternatives. In addition, the EU’s Carbon Border Adjustment Mechanism (CBAM), set to take full effect in 2026 will incentivize industries to adopt low-carbon solutions like green hydrogen to avoid tariffs. These developments position Europe as a hub for hydrogen innovation creating opportunities for renewable energy integration and fostering cross-sector collaborations that drive economic growth while advancing climate goals.

MARKET CHALLENGES

Public Resistance and Land Use Conflicts

Among the prime challenges faced by the European renewable energy market is public resistance to new projects, often stemming from land use conflicts and environmental concerns. Large-scale wind and solar farms need vast tracts of land, which can lead to opposition from local communities and environmental groups. Similarly, As noted by the WindEurope, over 60% of wind project delays in Europe are associated with permitting issues, many of that arise from public protests or legal challenges. For instance, in France, several onshore wind projects have encountered cancellations due to concerns about their impact on landscapes and biodiversity. Like, solar farms in Spain have faced resistance from agricultural communities fearing the loss of arable land. The European Environment Agency notes that balancing renewable energy development with ecological preservation remains a contentious issue, as poorly sited projects can disrupt habitats for endangered species. Additionally, lengthy legal battles further exacerbate delays, with some projects taking up to seven years to secure approval, as per the Fraunhofer Institute. This resistance not only hampers deployment timelines but also increases costs showcasing the efficiency of clean energy transitions.

Financing Gaps in Emerging Markets

While Western Europe has made eye catching strides in renewable energy adoption, financing gaps remain a critical challenge in Central and Eastern Europe (CEE). The European Bank for Reconstruction and Development brings to attention that the CEE region requires an estimated €78 billion annually to meet its renewable energy targets by 2030 yet current investments fall short by nearly 40%. In addition, high upfront capital costs and perceived risks deter private investors, particularly in countries with weaker institutional frameworks and unstable regulatory environments. For example, Romania and Bulgaria saw a 50% decline in renewable energy investments between 2015 and 2020, as reported by the International Renewable Energy Agency. Moreover, limited access to green bonds and other innovative financing mechanisms further compounds the issue. Also, reliance on EU funding programs like the Just Transition Fund often results in bureaucratic delays slowing project implementation. These financial barriers hinder the equitable spread of renewable energy across Europe, leaving emerging markets lagging behind and jeopardizing the continent’s collective climate goals.Top of Form

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.25% |

|

Segments Covered |

By Type And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

|

Market Leaders Profiled |

Enel Spa, Ørsted A/S, Iberdrola SA, Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, EDF Renewables, RWE AG, Acciona Energia, Statkraft AS, and EDP Renewables |

SEGMENTAL ANALYSIS

By Type Insights

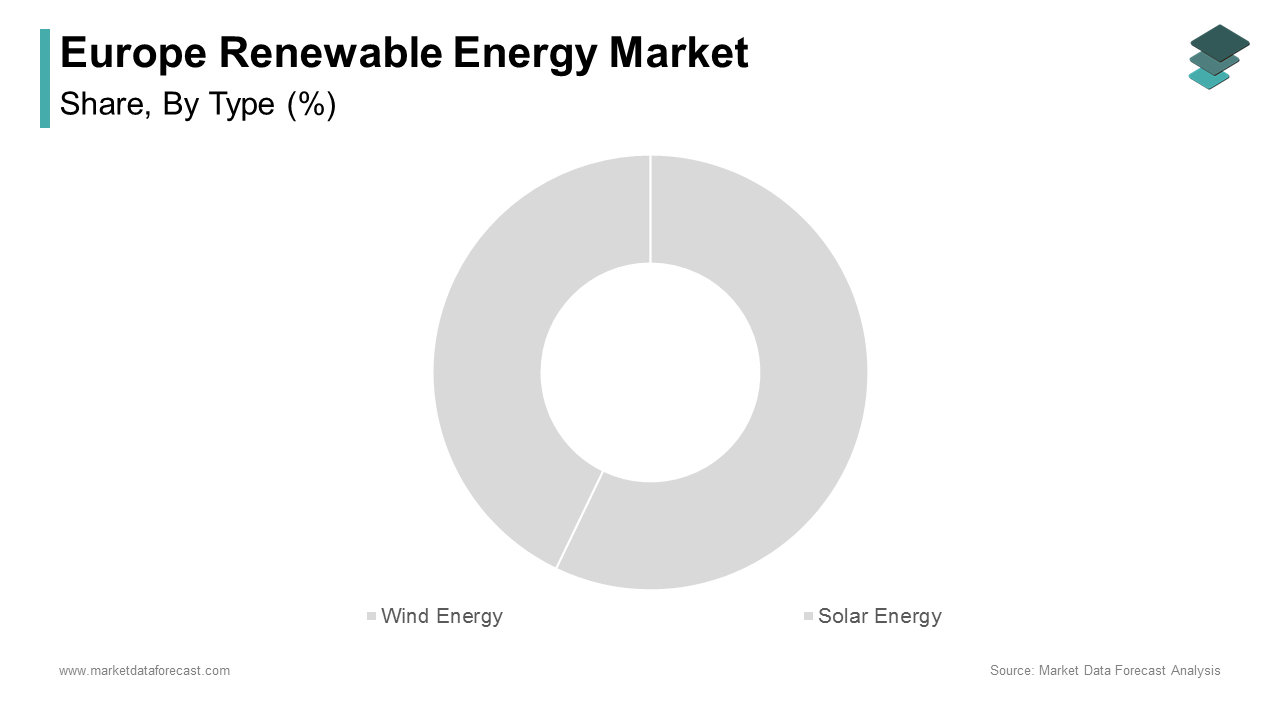

The segment that dominated the European renewable energy market was wind energy by accounting for 40.3% of the total installed capacity in 2024. This pre-eminence is supported by Europe’s favorable geographic conditions, especially its extensive coastlines and strong wind corridors in the North Sea, which make it ideal for both onshore and offshore wind projects. Also, offshore wind alone contributed over 30 gigawatts of capacity in 2022, with the UK and Germany leading installations. A key driver of this control is technological advancements that have greatly reduced costs as BloombergNEF reports that the levelized cost of electricity (LCOE) for offshore wind dropped by 48% between 2015 and 2022 making it increasingly competitive with fossil fuels. Besides these, supportive policies like the EU’s Renewable Energy Directive mandating a 42.5% renewable share by 2030 have spurred investments in wind infrastructure. The Fraunhofer Institute emphasizes that over €50 billion was invested in European wind energy projects in 2022 reflecting robust investor confidence. Furthermore, the rise of corporate power purchase agreements (PPAs), with companies like Amazon securing over 3 gigawatts of wind energy in Europe, has reinforced the segment’s growth. These factors collectively ensure wind energy remains the largest and most impactful contributor to Europe’s clean energy transition.

The solar energy segment is the fastest-growing in the European renewable energy market, with a CAGR of 17.2% projected between 2025 and 2033 Mackenzie. This rapid expansion is propelled by the plummeting costs of solar photovoltaic (PV) technology, which has seen an 85% decrease in costs since 2010, according to the International Energy Agency. Europe in 2022 alone added over 41 gigawatts of solar capacity marking a 47% year-on-year increase, as reported by SolarPower Europe. One major factor fueling this progress is the region’s increasing focus on energy security amidst geopolitical uncertainties, particularly following the Ukraine crisis. For instance, Germany introduced the “Easter Package,” accelerating solar deployment by streamlining permitting processes. Another critical aspect is the surging adoption of rooftop solar systems, with over 1 million households installing panels in 2022, backed by subsidies and tax incentives. Additionally, the European Commission’s Solar Rooftops Initiative aims to double solar capacity by 2025 further propelling development. These initiatives, coupled with the rising demand for decentralized energy solutions, position solar energy as the most dynamic and rapidly expanding segment in Europe’s renewable energy landscape.

REGIONAL ANALYSIS

Germany remained the largest renewable energy market in Europe by holding a 28.3% share of the region’s total installed capacity as of 2024. This influence is associated with its robust policy framework including the Renewable Energy Sources Act (EEG) which incentivizes clean energy adoption. Also, the EU nation added over 7 gigawatts of solar capacity in 2022 alone, as per Fraunhofer ISE, driven by favorable feed-in tariffs and tax benefits. Moreover, its supremacy is pivotal for Europe’s energy transition, as it accounts for nearly 40% of the EU’s wind energy output. Germany’s commitment to phasing out coal by 2038 further amplifies its role in driving decarbonization.

Spain is the fastest-growing renewable energy market in Europe, with a CAGR of 11.1% projected between 2025 and 2033. This growth is fueled by ambitious targets such as achieving 74% renewable electricity by 2030. Spain in 2022 installed 7.5 gigawatts of new renewable capacity which were primarily solar and supported by streamlined permitting processes under the National Integrated Energy and Climate Plan. BloombergNEF states that solar PV costs in Spain are among the lowest in Europe at €30/MWh, attracting significant foreign investments. The country’s focus on green hydrogen, with plans to install 4 gigawatts by 2030, shows its transformative role in Europe’s clean energy future.

The UK is poised to strengthen its offshore wind sector, targeting 50 gigawatts by 2030, as per the UK Department for Business, Energy & Industrial Strategy. On the other hand, France is emphasizing on nuclear-renewable hybrids, with solar capacity expected to triple by 2028, according to the French Ministry of Energy Transition. Besides these, Italy that is aiming for 72% renewable electricity by 2030 is investing heavily in rooftop solar, with over 1 million installations anticipated by 2025, as reported by Gestore dei Servizi Energetici. Collectively, these nations will play critical roles in diversifying Europe’s renewable energy portfolio.

LEADING PLAYERS IN THE EUROPE RENEWABLE ENERGY MARKET

Ørsted (Denmark)

Ørsted is a global leader in offshore wind energy, contributing over 30% of Europe’s total offshore wind capacity. The company operates over 7.6 gigawatts of offshore wind farms globally, with significant projects like Hornsea One in the UK. According to BloombergNEF, Ørsted’s investments in green energy have positioned it as a key player in reducing carbon emissions across Europe. Its global presence extends to the US and Asia, where it aims to develop 30 gigawatts of renewable capacity by 2030.

Enel Green Power (Italy)

Enel Green Power dominates Europe’s solar and wind sectors, with over 54 gigawatts of installed capacity worldwide. In Europe, it leads in utility-scale solar projects, particularly in Spain and Italy. As per the International Renewable Energy Agency, Enel’s focus on hybrid systems integrating renewables with storage has strengthened its global influence.

Siemens Gamesa (Spain/Germany)

Siemens Gamesa is a major turbine manufacturer, supplying over 110 gigawatts of wind capacity globally. It plays a pivotal role in Europe’s wind energy expansion, particularly in Germany and the UK. The company’s innovations in offshore turbines have set benchmarks for efficiency and sustainability.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in Europe’s renewable energy market employ strategies such as mergers and acquisitions, partnerships, and technological innovation. For instance, companies like Ørsted and Enel Green Power frequently acquire smaller firms to expand their project pipelines. Strategic collaborations with governments and research institutions are also common, enabling access to subsidies and cutting-edge technologies. Additionally, investments in digitalization and energy storage solutions enhance operational efficiency. These strategies collectively bolster market control and foster sustainable growth.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Europe Renewable Energy Market include Enel Spa, Ørsted A/S, Iberdrola SA, Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, EDF Renewables, RWE AG, Acciona Energia, Statkraft AS, and EDP Renewables

The European renewable energy market is highly competitive and is characterized by the hegemony of established giants like Ørsted, Enel Green Power, and Siemens Gamesa, alongside emerging regional players. According to Wood Mackenzie, the market’s fragmented nature encourages innovation and cost reductions, driving healthy competition. Offshore wind and solar segments witness intense rivalry, with companies vying for government contracts and PPAs. Strategic alliances, such as joint ventures and technology-sharing agreements, are prevalent. Regulatory support from the EU further intensifies competition, as companies race to capitalize on subsidies and carbon reduction mandates. This dynamic landscape ensures rapid advancements in clean energy technologies while fostering a robust ecosystem for sustainable growth.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Ørsted acquired a 50% stake in the German offshore wind project, Gode Wind 3, enhancing its portfolio with an additional 245 megawatts of capacity.

- In June 2023, Enel Green Power partnered with the Spanish government to develop a 1.2-gigawatt solar park in Andalusia, marking its largest solar investment in Europe.

- In August 2023, Siemens Gamesa launched the SG 14-236 DD offshore turbine, capable of powering 20,000 homes annually, setting new standards for efficiency.

- In October 2023, Iberdrola completed the acquisition of French renewable developer Aalto Power, expanding its footprint in France with 700 megawatts of projects.

- In December 2023, RWE signed a €1 billion deal with the Dutch government to construct a 1.4-gigawatt offshore wind farm in the North Sea, solidifying its position as a key player in Europe.

MARKET SEGMENTATION

This research report on the Europe Renewable Energy Market has been segmented and sub-segmented based on type and region.

By Type

- Wind Energy

- Solar Energy

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the Europe Renewable Energy Market?

Key drivers include supportive government policies, rising environmental awareness, technological advancements, and increasing investments in clean energy infrastructure.

2. Who are the major players in the Europe Renewable Energy Market?

Some of the leading companies include Enel Spa, Ørsted A/S, Iberdrola SA, Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, and EDF Renewables.

3. Which country holds the largest share in the Europe Renewable Energy Market?

Germany currently holds the largest market share, followed by the United Kingdom and France.

4. How is government regulation influencing market growth?

Policies such as the European Green Deal, national subsidies, and feed-in tariffs are positively influencing market expansion

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]