Europe Real-Time Payments Market Size, Share, Trends, & Growth Forecast Report By Type of Payment (P2P and P2B), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Real-Time Payments Market Size

The Europe real-time payments market was worth USD 6.52 billion in 2024. The European market is expected to reach USD 17.45 billion by 2033 from USD 7.27 billion in 2025, rising at a CAGR of 11.56% from 2025 to 2033.

Real-time payments (RTP) refer to electronic fund transfers that are processed instantly, enabling individuals and businesses to send and receive money without delays or settlement lags. This system contrasts sharply with traditional payment methods, which often involve batch processing and clearing times of one to three days. According to Eurostat, over 60% of European consumers now expect immediate transaction confirmations, reflecting a cultural shift towards speed and convenience in financial interactions. The European Central Bank (ECB) highlights that real-time payment systems like SEPA Instant Credit Transfer (SCT Inst) have gained significant traction, with transaction volumes surpassing €5 billion monthly in 2023.

In Europe, the adoption of RTP is further fueled by regulatory initiatives such as the Revised Payment Services Directive (PSD2) that mandates open banking and fosters innovation in payment solutions. Additionally, the European Payments Council emphasizes that RTP enhances financial inclusion by providing underserved populations with access to efficient payment systems. As Europe continues its transition to a cashless economy, real-time payments are becoming integral to sectors like retail, healthcare, and logistics, ensuring faster settlements and improved liquidity management. With advancements in AI, blockchain, and cloud computing, the real-time payments ecosystem is poised to redefine how transactions are conducted, fostering economic growth and consumer satisfaction across the continent.

MARKET DRIVERS

Growing Demand for Instantaneous Transactions in Europe

The increasing demand for instantaneous transactions is a major driver of the European real-time payments market. According to Eurostat, over 60% of European consumers now expect immediate payment confirmations, driven by the rise of e-commerce and digital wallets. The European Central Bank (ECB) highlights that systems like SEPA Instant Credit Transfer (SCT Inst) have processed over €5 billion in monthly transactions, underscoring the shift towards faster payment methods. Additionally, Statista notes that the surge in mobile banking app usage, which grew by 25% in 2022, has further fueled this demand. Real-time payments enable businesses to improve cash flow management and enhance customer satisfaction by reducing settlement times. As Europe transitions to a cashless economy, the need for seamless, instant transactions is becoming critical. This trend is particularly evident in sectors like retail and logistics, where faster settlements translate to improved operational efficiency and competitiveness.

Regulatory Support and Open Banking Initiatives

Regulatory support, particularly through frameworks like the Revised Payment Services Directive (PSD2), is another key driver of the European real-time payments market. The European Payments Council emphasizes that PSD2 mandates open banking, fostering innovation by enabling third-party providers to develop advanced payment solutions. Eurostat reports that open banking adoption has increased by 40% since its implementation, with over 300 fintech companies now offering real-time payment services. Furthermore, the ECB highlights that regulatory initiatives have standardized cross-border instant payments, ensuring interoperability across the EU. These measures have reduced transaction costs by 15%, making RTP more accessible to small and medium-sized enterprises (SMEs). By promoting transparency and security, regulatory frameworks are accelerating the adoption of real-time payments, positioning them as a cornerstone of Europe’s digital financial ecosystem while enhancing consumer trust and participation.

MARKET RESTRAINTS

High Implementation Costs for Financial Institutions

The high implementation costs associated with adopting real-time payment systems is a major restraint to the European market. The European Banking Authority highlights that upgrading legacy infrastructure to support RTP systems can cost financial institutions between €500,000 and €2 million per entity, depending on their size and complexity. Eurostat reports that 40% of smaller banks and credit unions in Europe face budgetary constraints, limiting their ability to invest in advanced payment technologies. Additionally, the European Central Bank (ECB) notes that ongoing maintenance and compliance with regulatory standards further increase operational expenses. These financial barriers slow the widespread adoption of RTP, particularly among smaller institutions serving rural or underserved areas. As a result, disparities in access to real-time payment solutions persist, hindering the goal of achieving universal financial inclusion across Europe despite the growing demand for instant transactions.

Cybersecurity Risks and Consumer Trust Issues

Cybersecurity risks and consumer trust issues represent are further hindering the growth of the European real-time payments market. The European Union Agency for Cybersecurity (ENISA) reports that cyberattacks targeting payment systems have increased by 35% over the past two years, raising concerns about data breaches and fraud. Eurostat highlights that 50% of consumers express hesitation in adopting real-time payments due to fears of unauthorized transactions and insufficient protection measures. Furthermore, the ECB emphasizes that while RTP systems are designed to be secure, the speed of transactions leaves limited time for fraud detection and prevention, increasing vulnerabilities. These challenges undermine consumer confidence and slow market growth. Addressing these concerns requires significant investments in advanced encryption, AI-driven fraud detection, and public awareness campaigns, which remain ongoing challenges for stakeholders in the ecosystem of European payments.

MARKET OPPORTUNITIES

Expansion of Cross-Border Real-Time Payments

The expansion of cross-border real-time payments is a lucrative opportunity for the European market, driven by initiatives like SEPA Instant Credit Transfer (SCT Inst). The European Central Bank (ECB) reports that cross-border RTP volumes have grown by 45% annually since SCT Inst’s launch, with over €5 billion processed monthly in 2023. Eurostat highlights that 70% of European businesses view faster international transactions as critical for improving liquidity and competitiveness. Additionally, the European Payments Council emphasizes that interoperability frameworks are enabling seamless payments across 20+ EU countries, reducing transaction costs by 20%. As globalization intensifies, demand for instant cross-border solutions is expected to surge, particularly among SMEs engaged in e-commerce. By addressing currency conversion and settlement inefficiencies, RTP systems can enhance trade and economic integration, positioning Europe as a leader in global payment innovation while fostering financial inclusion for underserved regions.

Integration with Emerging Technologies Like AI and Blockchain

The integration of real-time payments with emerging technologies such as AI and blockchain are other major opportunities for the European market. The European Commission highlights that AI-driven fraud detection systems have reduced payment-related fraud by 30%, enhancing security and consumer trust. Eurostat reports that blockchain adoption in financial services has grown by 50% over the past three years, with its decentralized nature ensuring transparency and immutability in transactions. Furthermore, Statista projects that combining RTP with AI and blockchain could reduce operational costs by 25% while increasing transaction speeds by 15%. These technologies enable predictive analytics, smart contracts, and automated reconciliation, making RTP more efficient and scalable. As Europe prioritizes digital transformation, leveraging these innovations will not only drive adoption but also position RTP as a cornerstone of the future financial ecosystem, catering to evolving consumer and business needs.

MARKET CHALLENGES

Fragmentation in Payment Systems Across Member States

The fragmentation of payment systems across European member states is a major challenge to the real-time payments market. The European Central Bank (ECB) highlights that while SEPA Instant Credit Transfer (SCT Inst) aims to unify RTP, only 75% of EU banks have adopted the system as of 2023, leaving gaps in accessibility. Eurostat reports that cross-border RTP adoption varies widely, with countries like Germany and France leading at 80%, while smaller nations lag at less than 40%. This disparity creates inefficiencies, particularly for SMEs operating across borders. Additionally, the European Payments Council notes that differences in regulatory interpretations and technical standards further complicate interoperability. These inconsistencies hinder the seamless flow of instant payments, undermining Europe’s goal of a unified digital economy. Addressing these challenges requires greater harmonization and investment in standardized infrastructure to ensure equal access and functionality across all regions.

Resistance to Change Among Traditional Financial Institutions

Resistance to change among traditional financial institutions are further challenging the growth of the European real-time payments market. The European Banking Authority reports that 60% of legacy banks are reluctant to fully transition to RTP due to concerns about disrupting existing systems and revenue models. Eurostat highlights that only 45% of traditional banks have integrated real-time capabilities into their core operations, with many citing high costs and complexity as barriers. Furthermore, the ECB notes that consumer habits also play a role, as 30% of Europeans still prefer traditional payment methods like cash or batch processing. This resistance slows innovation and limits the scalability of RTP solutions. Overcoming this challenge requires targeted incentives, regulatory mandates, and public awareness campaigns to encourage both institutions and consumers to embrace the benefits of instant payments, ensuring broader adoption and market growth.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

11.56% |

|

Segments Covered |

By Type of Payment, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

ACI Worldwide Inc., Fiserv Inc., Paypal Holdings Inc., Mastercard Inc., and VISA Inc. |

SEGMENTAL ANALYSIS

By Type of Payment Insights

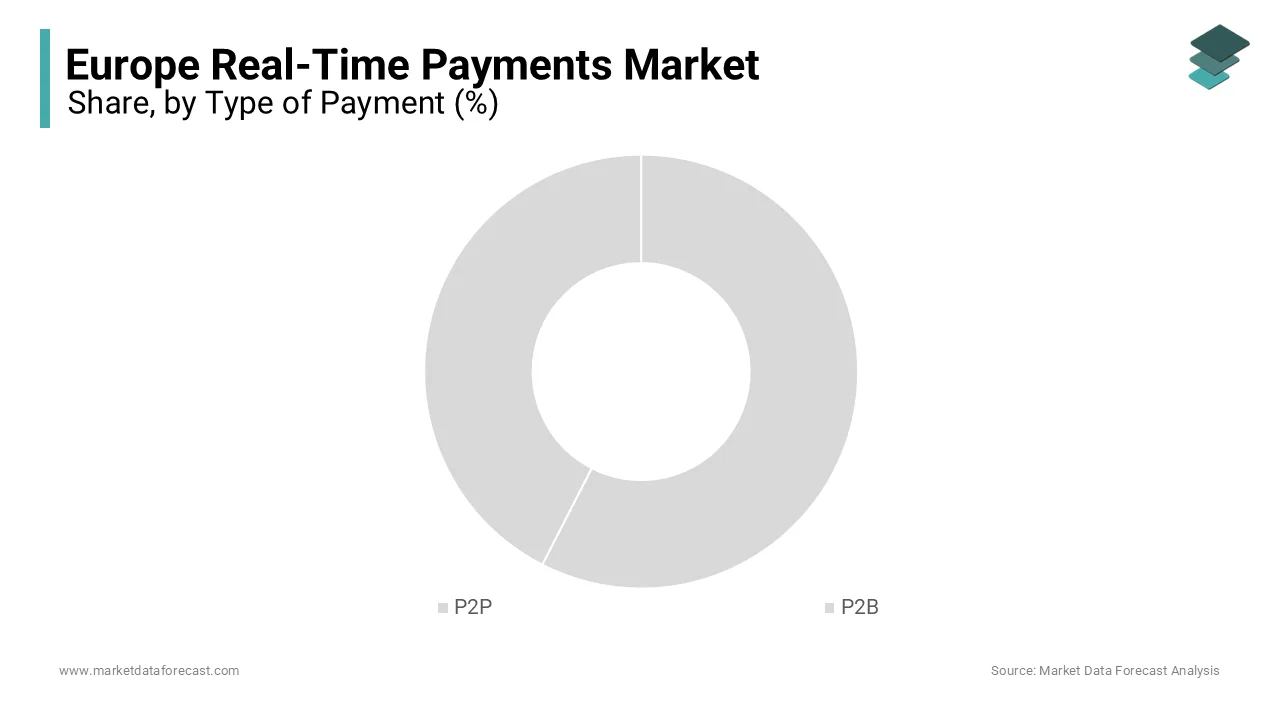

The P2B segment had the dominating share of 60.9% in the European market in 2024. The dominating position of P2B segment in the European market is driven by the rapid adoption of instant payment solutions in e-commerce and retail, where businesses benefit from faster settlements and improved cash flow. Eurostat highlights that P2B transactions reduce settlement times by 90%, enhancing operational efficiency. Additionally, Statista projects the e-commerce sector, a key driver of P2B growth, will expand at a CAGR of 12% through 2030. Regulatory frameworks like PSD2 have further encouraged integration, ensuring secure and seamless transactions. This segment’s prominence underscores its critical role in driving economic activity and supporting Europe’s digital-first economy.

The P2P segment is growing remarkably and is expected to witness the highest CAGR of 35.8% over the forecast period due to the increasing adoption of mobile banking apps and digital wallets, with platforms like Revolut and Wise gaining popularity among tech-savvy consumers. Eurostat notes that P2P transactions account for 40% of all real-time payment volumes, driven by the demand for instant, convenient transfers. The European Central Bank highlights that initiatives like SEPA Instant Credit Transfer have accelerated cross-border P2P usage, enabling seamless international transactions. As Europe transitions to a cashless society, P2P payments are becoming integral to everyday financial interactions, fostering financial inclusion and reducing reliance on traditional methods, making it a transformative force in the real-time payments landscape.

REGIONAL ANALYSIS

Germany occupied the major share of 24.9% in the European market in 2024. The growth of the German in the European market is primarily driven by the robust financial infrastructure and high adoption of SEPA Instant Credit Transfer (SCT Inst), with over 80% of German banks integrated into the system, as highlighted by the European Central Bank (ECB). Eurostat reports that Germany’s strong e-commerce sector, which grew by 25% in 2022, drives demand for instant transactions. Additionally, the country’s focus on digital transformation and regulatory compliance under PSD2 fosters innovation in payment solutions. Germany’s proactive approach to upgrading legacy systems and promoting financial inclusion ensures its dominance in the RTP landscape, making it a model for other EU nations striving to enhance their payment ecosystems.

The UK accounted for a promising share of the European real-time payments market in 2024 and is expected to grow at a healthy CAGR over the forecast period. The thriving fintech ecosystem of the UK with Statista reporting that over 70% of Britons use mobile banking apps, accelerating RTP adoption and driving the UK market expansion. The Financial Conduct Authority (FCA) highlights that open banking initiatives under PSD2 have spurred innovation, enabling platforms like Revolut and Wise to dominate the P2P space. Furthermore, the ECB notes that the UK’s advanced digital infrastructure supports seamless cross-border transactions, particularly with EU nations. As consumer expectations shift towards instant, secure payments, the UK’s emphasis on technological advancements and user-centric solutions solidifies its position as a frontrunner in the European real-time payments market.

France is estimated to progress at a CAGR of 18.3% over the forecast period owing to the strong regulatory support, with the ECB emphasizing that 90% of French banks have adopted SCT Inst, ensuring widespread accessibility. Eurostat reports that France’s e-commerce sector, which accounts for €150 billion annually, drives demand for instant payments, particularly in P2B transactions. Additionally, the European Payments Council highlights that France’s focus on cybersecurity and fraud prevention has increased consumer trust in RTP systems. By aligning with sustainability goals and promoting financial inclusion, France is emerging as a key innovator in the RTP market, leveraging its robust regulatory framework and growing digital economy to drive adoption across Europe.

KEY MARKET PLAYERS

The major players in the Europe real-time payments market include ACI Worldwide Inc., Fiserv Inc., Paypal Holdings Inc., Mastercard Inc., and VISA Inc.

MARKET SEGMENTATION

This research report on the Europe real-time payments market is segmented and sub-segmented into the following categories.

By Type of Payment

- P2P

- P2B

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of real-time payments in Europe?

The growth of real-time payments in Europe is driven by regulatory initiatives like SEPA Instant Credit Transfer (SCT Inst), increasing consumer demand for faster transactions, and the adoption of digital banking solutions by businesses and financial institutions.

What industries benefit the most from real-time payments in Europe?

Retail, e-commerce, banking, financial services, and gig economy platforms benefit the most from real-time payments due to faster transaction settlements and improved cash flow management.

What is the role of fintech companies in the European real-time payments market?

Fintech companies play a key role in accelerating real-time payment adoption by offering innovative solutions, improving user experience, and partnering with traditional banks to enhance payment processing capabilities.

What future trends are expected in the European real-time payments market?

Future trends include the expansion of instant payments beyond Europe, increased integration with digital wallets and cryptocurrencies, greater adoption of open banking APIs, and enhanced regulatory frameworks to ensure security and compliance.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]