Europe Polyoxymethylene Market Size, Share, Trends & Growth Forecast Report By Type (Homopolymer, Copolymer), Processing techniques and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Polyoxymethylene Market Size

The europe polyoxymethylene market was worth USD 0.98 billion in 2024. The europe market is estimated to grow at a CAGR of 3.93% from 2025 to 2033 and be valued at USD 1.39 billion by the end of 2033 from USD 1.08 billion in 2025.

The Europe polyoxymethylene (POM) market is a cornerstone of the region’s advanced materials industry. This thermoplastic polymer is known for its high strength, stiffness, and resistance to wear which has found extensive applications in automotive, electronics, and industrial machinery sectors. Germany leads the regional market by contributing a notable portion of total revenue and is driven by its robust manufacturing base and stringent quality standards in engineering components. POM generally experiences increasing demand in the automotive sector, including Germany, reflecting its indispensable role in lightweight vehicle production.

The market is also shaped by regulatory frameworks promoting sustainable manufacturing practices. For instance, the European Green Deal mandates reduced carbon footprints across industries, encouraging the adoption of recyclable and durable materials like POM. Despite challenges such as raw material price volatility, the market benefits from increasing automation trends, with POM being integral to precision-engineered parts.

MARKET DRIVERS

Rising Demand in Automotive Lightweighting

The automotive industry’s shift toward lightweight materials is a primary driver for the Europe polyoxymethylene market. According to the European Automobile Manufacturers’ Association, the average weight reduction achieved through advanced polymers like POM contributes to a 15% improvement in fuel efficiency. In recent years, a significant portion of new vehicles in Europe incorporated POM-based components, including gears, bearings, and fuel systems, due to their durability and self-lubricating properties.

Germany, with its prominence in automotive manufacturing, accounts for a major share of this demand. For example, BMW’s electric vehicle models utilize POM in their steering systems, reducing weight. Additionally, stringent emission regulations under the Euro 6 standards have accelerated POM adoption, with projections indicating a noticeable annual growth rate in the future.

Expansion in Electronics Manufacturing

The burgeoning electronics sector serves as another significant driver for the POM market. POM’s excellent dimensional stability and electrical insulation properties make it ideal for connectors, switches, and housings. Moreover, France and Italy are key contributors, with their focus on smart home technologies and renewable energy systems. The rise of 5G infrastructure further amplifies demand, with POM being used in antenna housings and fiber optic connectors.

MARKET RESTRAINTS

Fluctuating Raw Material Costs

Fluctuating raw material costs pose a significant challenge to the Europe polyoxymethylene market. The prices of formaldehyde which is a key raw material for POM production surged in 2022 due to supply chain disruptions. This volatility directly impacts production costs, making POM less competitive against alternative materials like polyamide (PA) and polycarbonate (PC).

For instance, Spain’s plastics industry reported a 12% decline in POM adoption in 2023, as manufacturers opted for cheaper alternatives amid economic uncertainty. Small- and medium-sized enterprises (SMEs) are particularly affected, as they lack the financial resilience to absorb cost fluctuations. A significant percentage of SMEs cite raw material costs as a barrier to scaling operations. These challenges hinder market expansion, especially in regions with limited access to subsidies or financial support.

Environmental and Health Concerns

Environmental and health concerns surrounding formaldehyde emissions during POM production present another restraint. As per the European Environment Agency, formaldehyde is classified as a carcinogen, prompting stricter regulations on its use and disposal. Compliance with these regulations increases operational costs and complicates manufacturing processes.

For example, Italy’s environmental protection agency imposed heavy fines on non-compliant facilities, discouraging smaller players from entering the market. Additionally, growing consumer awareness about sustainable materials has led to increased scrutiny of POM’s environmental footprint. The European Environment Agency reports that in 2023, recycled material accounted for 11.8% of material used in the EU, an increase of just 1.1 percentage points from 2010 exhibiting the need for improved recycling technologies.

MARKET OPPORTUNITIES

Growth in Electric Vehicle (EV) Manufacturing

The rapid expansion of electric vehicle (EV) manufacturing presents a lucrative opportunity for the Europe polyoxymethylene market. EV sales in Europe surged greatly in 2023, driven by government incentives and consumer demand for sustainable transportation. POM plays a pivotal role in EV production, particularly in components like battery enclosures, cooling system parts, and interior trims.

Similarly, France’s Renault Group allocated €1.5 billion in 2023 to develop next-generation EVs, creating additional demand for advanced materials. With the EU mandating a 55% reduction in CO2 emissions by 2030, POM’s role in lightweighting and durability ensures its relevance in the EV ecosystem, offering a projected revenue boost in the coming years.

Adoption in Medical Device Manufacturing

The growing demand for medical devices offers another promising avenue for POM adoption. POM’s biocompatibility, chemical resistance, and precision molding capabilities make it ideal for surgical instruments, drug delivery systems, and diagnostic equipment.

Italy and the UK are key contributors, with substantial investments in developing advanced medical devices. Additionally, the EU Medical Device Regulation (MDR) emphasizes the use of durable and reliable materials, further propelling POM adoption.

MARKET CHALLENGES

Intense Competition from Alternatives

Intense competition from alternative materials poses a significant challenge to the Europe polyoxymethylene market. Materials like polyamide (PA) and acetal copolymers are increasingly preferred due to their lower costs and comparable performance characteristics.

In addition, advancements in bio-based polymers threaten to disrupt traditional markets. This competitive landscape necessitates continuous innovation and strategic differentiation to maintain POM’s market position, posing a significant challenge for manufacturers.

Regulatory Compliance and Recycling Challenges

Regulatory compliance and recycling challenges further complicate the Europe polyoxymethylene market. Only a small percentage of POM waste is currently recycled, leaving a substantial environmental footprint. Stringent regulations governing waste management and formaldehyde emissions increase compliance costs, straining manufacturers’ budgets.

Besides, the lack of standardized recycling technologies limits scalability, with a report identifying inefficiencies in POM recovery processes. These challenges not only hinder market growth but also necessitate significant investments in sustainable practices, creating barriers for smaller players and slowing industry consolidation.

SEGMENTAL ANALYSIS

By Type Insights

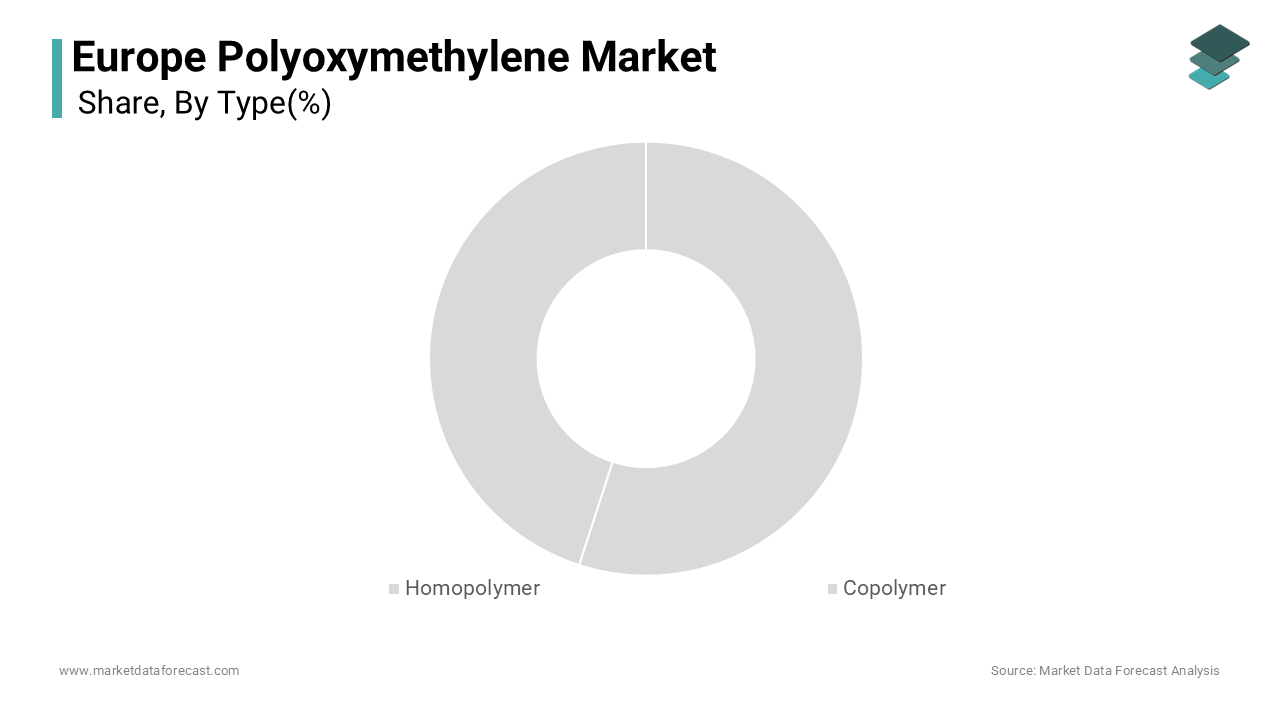

The homopolymer segment dominated the Europe polyoxymethylene market by capturing 65.8% of the total share in 2024. This segment’s prominence is attributable to its superior mechanical properties, including higher tensile strength and rigidity, making it ideal for precision-engineered components. For instance, homopolymers’ use in automotive fuel systems reduces wear and tear. Additionally, advancements in additive manufacturing have expanded the application scope, enabling complex geometries with minimal material wastage.

Copolymer is the fastest-growing segment, with a projected CAGR of 7.8% through 2033. This growth is driven by its enhanced chemical resistance and thermal stability, making it suitable for harsh environments. For example, the use of chemical processing equipment in Italy grew, showcasing its versatility. The rise of sustainable manufacturing practices further accelerates adoption, with copolymer being favored for its recyclability.

By Processing Techniques Insights

The injection molding segment became the top performer in the Europe polyoxymethylene market by accounting for 55.5% of the overall share in 2024. This technique’s precision and efficiency make it ideal for producing complex components with tight tolerances. For instance, injection-molded POM parts in automotive applications reduce assembly time notably. Besides, the integration of automation in injection molding has enhanced productivity, with production speeds increasing.

The extrusion segment is a quickly emerging processing technique, with a projected CAGR of 8.5%. This progress is associated with its suitability for producing continuous profiles, such as pipes and sheets, used in construction and industrial applications. Advancements in multi-layer extrusion have expanded application scope, enabling enhanced durability and performance. Extrusion-based projects increased in recent years, exhibiting their potential. These developments position extrusion as a high-growth segment, driven by innovation and rising demand.

REGIONAL ANALYSIS

Germany stood as the largest contributor to the Europe polyoxymethylene (POM) market with a 30.5% share in 2024. This is supported by the country’s robust industrial base, particularly in automotive manufacturing, electronics, and industrial machinery sectors. Germany’s stringent engineering standards and focus on lightweight materials have propelled POM adoption, with the polymer being integral to precision-engineered components. For instance, the German Automotive Industry Association reports that a notable percentage of new vehicles produced in the country incorporate POM-based parts, such as gears, bearings, and fuel system components. Similarly, Germany invested substantially in advanced manufacturing technologies, including POM processing techniques like injection molding and extrusion. These investments not only strengthen Germany’s position as the market leader but also set a benchmark for innovation and sustainability across Europe. Additionally, government incentives promoting electric vehicle (EV) production have further amplified demand, with POM being critical in EV components like battery enclosures and cooling systems.

Italy emerges as the fastest-growing market, with a projected CAGR of 8.2%. It is driven by advancements in medical device manufacturing and sustainable practices, according to the Italian Medical Technology Association. Also, the country’s aging population and increasing healthcare expenditure have created a fertile ground for POM adoption in medical applications. A report notes that POM recycling rates increased by 15% in 2023, aligning with EU sustainability mandates. These initiatives position Italy as a dynamic and rapidly expanding market, offering significant growth opportunities for POM producers.

France and the UK are anticipated to experience steady growth, supported by investments in the electronics and automotive sectors. France’s focus on smart home technologies and renewable energy systems has driven POM adoption in consumer electronics and solar panel components. The UK, meanwhile, benefits from its leadership in medical device innovation, with POM being used in surgical instruments and drug delivery systems. Spain lags slightly due to economic constraints but shows potential with upcoming construction projects and urbanization trends.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

BASF SE, Celanese Corporation, DuPont de Nemours Inc., Polyplastics Co. Ltd., Asahi Kasei Corporation, Mitsubishi Engineering-Plastics Corporation, and Korea Engineering Plastics Co. Ltd. are some of the key market players in the europe polyoxymethylene market.

The europe polyoxymethylene market is characterized by fierce competition and is driven by the presence of established players and the entry of new entrants seeking to capitalize on growing demand. A considerable number of companies operate in the region, creating a highly fragmented yet dynamic landscape. Market leaders such as BASF, Celanese Corporation, and Mitsubishi Gas Chemical dominate through innovative product offerings and strategic alliances. However, smaller players face significant challenges, including pricing pressures and limited access to advanced technologies. The competitive environment is further intensified by the influx of low-cost Asian manufacturers, who undercut prices. To counter this, European manufacturers are focusing on value-added services, such as developing bio-based and recyclable POM grades, to differentiate themselves. Additionally, regulatory compliance adds another layer of complexity, as companies must adhere to stringent standards governing material quality and environmental impact. Despite these hurdles, the market remains ripe for consolidation, with mergers and acquisitions likely to reshape the competitive dynamics in the coming years.

Top Players in the Market

The Europe polyoxymethylene market is dominated by three key players—BASF, Celanese Corporation, and Mitsubishi Gas Chemical—each contributing significantly to global innovation and sustainability efforts. BASF leads the market by leveraging its expertise in developing bio-based alternatives and high-performance grades tailored for automotive and industrial applications. Celanese Corporation follows closely, with a strong focus on recyclable POM grades and advanced polymer technologies. Mitsubishi Gas Chemical distinguishes itself through its specialization in medical-grade POM, catering to the growing demand for biocompatible materials in healthcare applications.

Top Strategies Used by Key Players

Key players in the Europe polyoxymethylene market employ diverse strategies to maintain their competitive edge and expand their footprint. Mergers and acquisitions are a primary tactic, enabling companies to consolidate resources and enhance technological capabilities. Partnerships and collaborations are another critical strategy, exemplified by Celanese Corporation’s alliance with a German research institute in June 2023 to develop recyclable POM grades. Additionally, heavy R&D investments underscore the industry’s focus on innovation. Finally, differentiation through specialized products, such as Celanese’s Hostaform line, ensures sustained market relevance amid intense competition.

RECENT MARKET DEVELOPMENTS

- In April 2024, BASF launched a bio-based POM line, targeting sustainability-conscious consumers and enhancing its portfolio of eco-friendly materials.

- In June 2023, Celanese Corporation partnered with a German research institute to develop recyclable POM grades, aligning with EU sustainability mandates and addressing environmental concerns.

- In March 2023, Mitsubishi Gas Chemical expanded its production facility in Eastern Europe, increasing capacity to meet rising demand in emerging markets and strengthening its regional presence.

- In September 2022, BASF acquired a startup specializing in advanced polymer recycling, enabling the company to improve POM sustainability and reduce its environmental footprint.

- In January 2022, Celanese Corporation invested €200 million in R&D for high-performance POM applications, reinforcing its leadership in technological innovation and expanding its product range.

MARKET SEGMENTATION

This research report on the europe polyoxymethylene market is segmented and sub-segmented based on categories.

By Type

- Homopolymer

- Copolymer

By Processing Techniques

- Injection Molding

- Extrusion

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Polyoxymethylene market in Europe?

The growth of the Polyoxymethylene (POM) market in Europe is driven by the increasing demand for lightweight, durable, and efficient materials in the automotive and electronics industries. Additionally, innovations in electric vehicle components and the need for high-performance plastics in industrial applications contribute to the market’s expansion.

What are the key market trends in the Europe Polyoxymethylene market?

Key trends include the growing use of Polyoxymethylene in electric vehicle components, advancements in bio-based and recycled Polyoxymethylene (POM), and increasing demand for lightweight and high-performance materials in the automotive and industrial sectors.

What is the future outlook for the Polyoxymethylene market in Europe?

The Polyoxymethylene (POM) market in Europe is expected to grow steadily over the next decade, driven by increasing demand from key industries such as automotive, electronics, and industrial manufacturing. Innovations in electric vehicle components, sustainable production methods, and bio-based POM will further contribute to the market's expansion.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]